No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

On one hand, the past year has been guided by a modern miracle, with effective vaccines developed and deployed faster than ever to combat the ongoing pandemic. But this year has also been complicated with new virus variants, uneven vaccination rates, closed borders, and bitter politics.

People continue to adapt in creative ways. When AFIRE members were surveyed in March 2021 for the association’s Annual International Investor Survey, they expressed an overall sense of optimism thanks to the adaptations and the hope that the pandemic might soon pass.1

Historically, AFIRE has only conducted this survey annually— but this year’s survey research project was necessarily adapted to meet the needs of the “new normal,” thus warranting a mid-year sentiment “pulse” survey, or follow-up to the March questionnaire.2

When this pulse survey was conducted in August 2021, the optimistic outlook explicated in Q1 2021 had evolved, reflecting a greater emphasis on risk aversion and more concern for critical issues across business, real estate fundamentals, and social and political trends.

INVESTOR CONCERNS

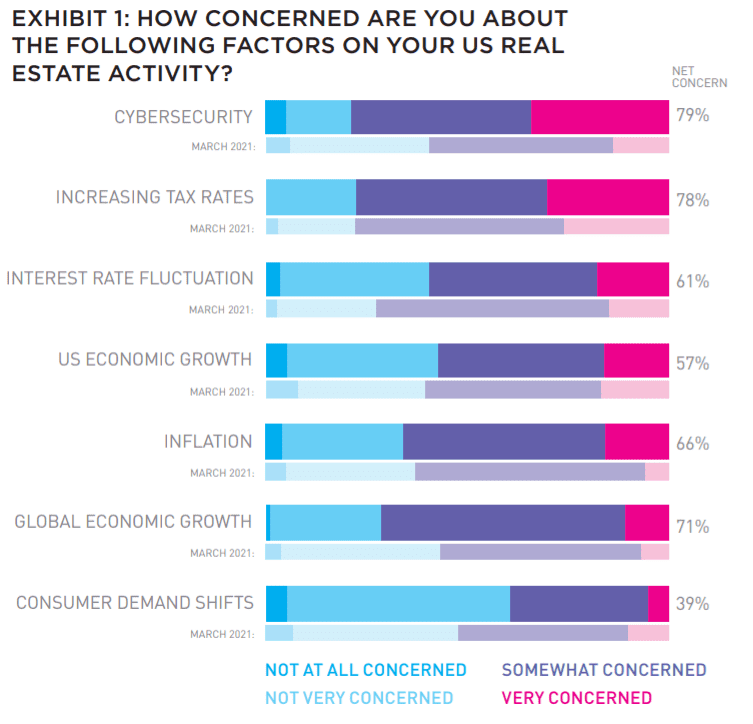

To compare changes in attitudes related to the general business climate, respondents were asked to rate their concern about seven key business factors. In March 2021, increasing tax rates ranked as a top concern (78% net concern), followed by interest rate fluctuation (73%), and inflation (63%).

While concerns about increasing tax rates have not meaningfully changed over the past several months (remaining at 78% net concern), and concerns a bout inflation have grown slightly (from 63% to 66%), cybersecurity has skyrocketed to the top of the list, ranking at 79% net concern, up from 60% earlier this year.

These concerns are interrelated. For example, concerns about economic conditions (e.g., interest rate fluctuations, inflation, and economic growth) have mostly subsided in recent months, perhaps reflecting the stabilization of pandemic-related uncertainties as the world becomes more organized in its fight against COVID-19.

Similarly, the subsidence of some of these uncertainties (e.g., shifts in consumer demand) has correspondingly heightened concerns in other related areas, especially around cybersecurity, which has become even more integral to consumer confidence through and beyond the pandemic.

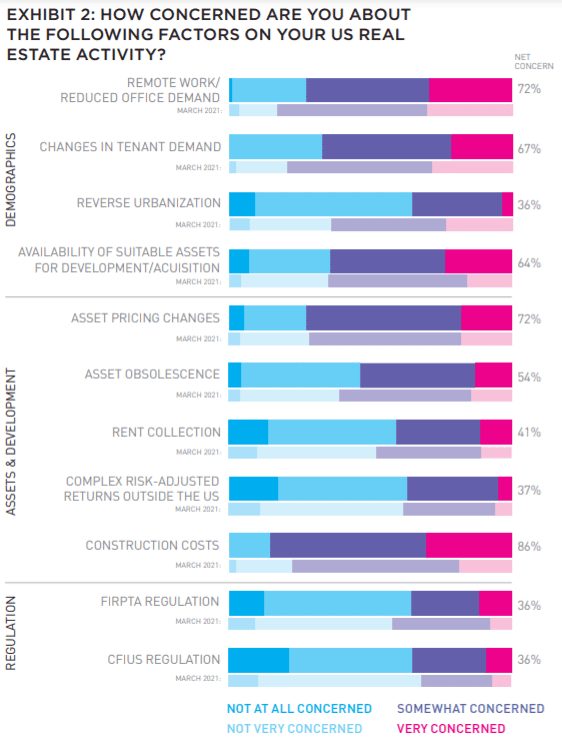

Investor concerns about real estate fundamentals across demographics, asset types, and regulation have declined over the past several months.

The most substantial declines have occurred around remote work/office demand (72% net concern, down from 83%) and changes in tenant demand (67%, down from 80%), reflecting market adaptation to prolonged pandemic conditions.

Concerns about migration out of cities has also seen significant decline (36% net concern, down from 53%), while concerns around rent collection, asset pricing, obsolescence, and/ or availability have remained notably stable. And even as most concerns have declined or stayed the same, construction costs have grown to the area of greatest concern (86%). This trend could continue, especially in the face of ongoing supply chain challenges.

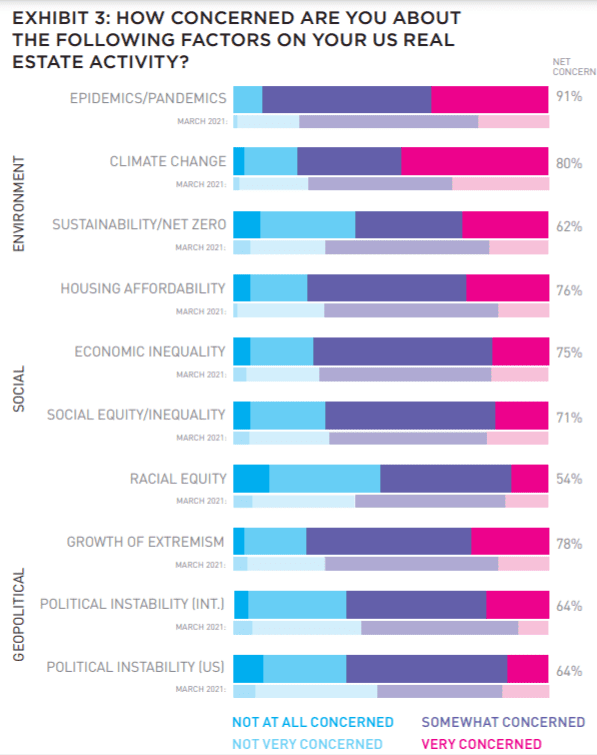

However, the Delta strain upended that optimism by mid-year, and markets battened down for a prolonged pandemic, as reflected by the increase to 91% net concern for pandemics—nearly universal.

Concerns around climate change, affordable housing, and economic and social inequity also saw slight increases in concern, though concerns about pathways towards progress in these areas (e.g., sustainability and racial equity) saw moderate declines. However, concerns related to political instability and extremism, globally and in the US, have increased over the past several months.

RISK MANAGEMENT

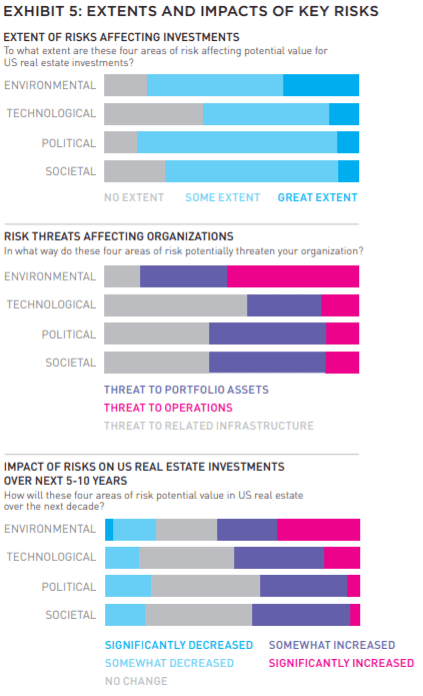

In the face of evolving concerns across business, real estate, and socio-political conditions, risk management has become increasingly critical, especially as our dominant areas of risk—including those related to political, social, climate, and technological concerns— also threaten to be novel in their manifestation (e.g., large-scale climate events, malicious ransomware, disease strains, etc.).

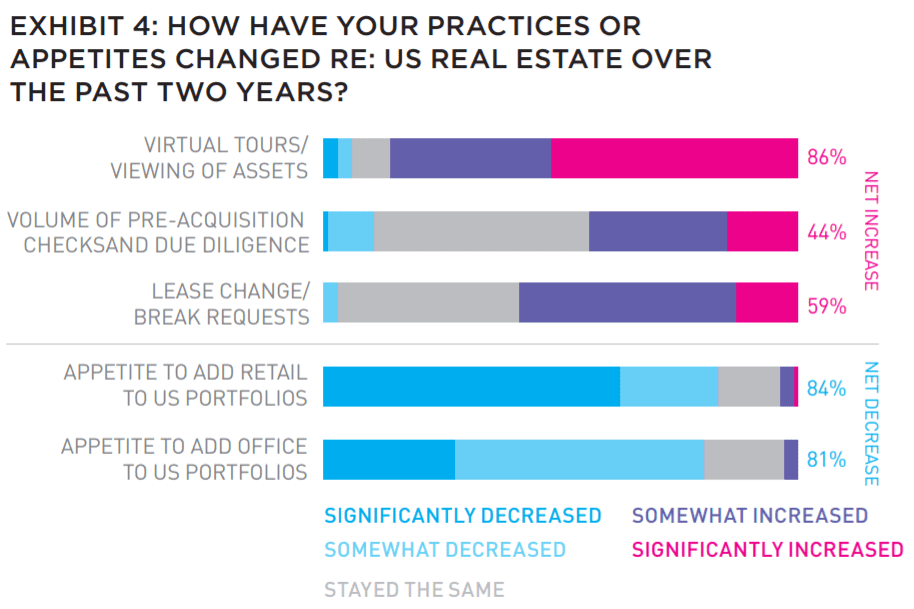

This prioritization of risk management has seen notable changes in standard real estate practices, such as due diligence and lease negotiation processes, as well as appetites for adding retail and office assets to US portfolios (net decrease of 84% and 81%, respectively). Similarly, political and economic risks are forecasted to have the greatest impact on US real estate over the next decade.

The primary risks detailed in this survey focused on four key areas:

(1) environmental risk (e.g., rising sea levels, weather events, etc.)

(2) technological risk (e.g., phishing, malware, ransomware, etc.)

(3) political risk (e.g., changing tax landscape, regulatory changes, etc.)

(4) societal risk (e.g., civic unrest, labor issues, etc.)

Environmental risks rank the highest almost universally across all three areas, with 83% stating that these risks will affect potential investment value and nearly 60% forecasting climate-related threats to their assets and operations. And consistent with sentiments expressed elsewhere, political issues pose similar degrees of risk, with 87% finding value affected and 75% forecasting a threat to assets and operations.

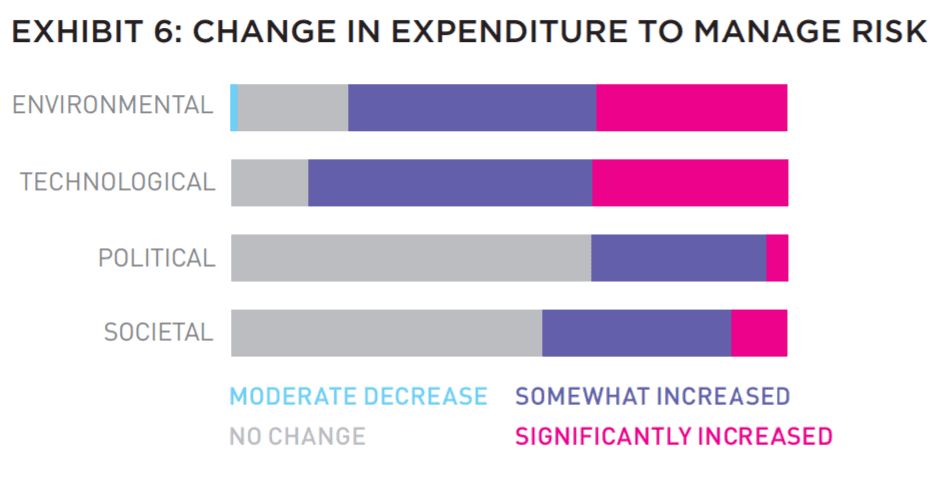

Because environmental risks rank among the highest areas of concern for investors, respondents also signaled an 78% net increase in risk management expenditures over the next decade. This is led by a forecasted 86% increase in technology and cyber-security-related spending over that same period. Alternately, anticipated extra spending for political and societal risks is more modest, perhaps reflecting their more immaterial nature.

These increased expenditures are an extension of how respondents are forecasting broader technological, cultural, and consumer changes over the next decade. For example, 85% of respondents anticipate an ever-accelerating application of technology in the industry, as well as a greater demand for technology. And no matter the nature of risk, most respondents (79%) also expect higher insurance premiums in all areas.

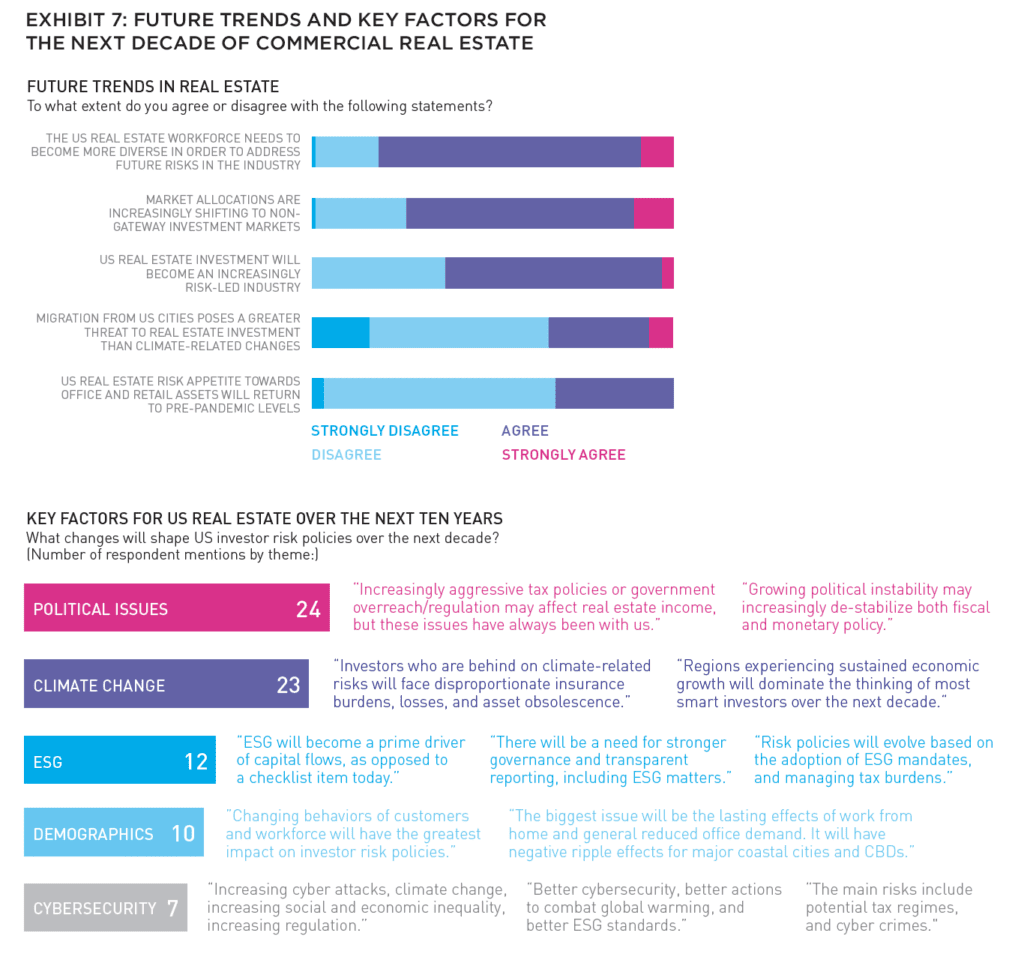

FUTURE TRENDS

AFIRE’s Future Committee is comprised of leaders within the association’s global membership and focuses on trends that will help understand the future of real estate investing beyond the visible horizon. For this section of the survey, respondents rated “future factors” likely to have the most significant impact on their investments for the next decade.

Political issues and climate change will be top-of-mind for investors in over the next decade. The connection between workforce diversity and risk management (with 81% agreed) will be critical to future performance, as will the ongoing prioritization of allocations in non-gateway investment markets (74% agreed).

In the various Venn diagrams that could be construed for many of the risk categories and future outlooks detailed in this survey, a four-dimensional model would be needed to fully articulate the interrelationship of the issues affecting long-term value commercial real estate within and beyond the US. For example, as detailed in Exhibit 7, respondents overwhelmingly agree that the US real estate workforce needs to become more diverse to address future risk—including simple reputational risk that could affect a company that lacks a diverse workforce.

But at the same time, the calculus for diverse talent development, recruitment, and retention is related to (and informed by) the same economic conditions, political attitudes, and technological trends that are otherwise fanning uncertainties at other tiers of the commercial real estate ecosystem.

Such complexities are inherent in real estate, and savvy investors are those able to find clarity amidst uncertainty. As such, this close-in look at the subtle changes in investor attitudes over the past year ultimately provides an up-to-date snapshot of how the global institutional real estate investor community is thinking about the future: still optimistic, still focused, but even more careful—a shift that is certainly warranted during these challenging times.

ALSO IN THIS ISSUE (FALL 2021)

NOTE FROM THE EDITOR / GROUPTHINK VS. GROUP COLLABORATION

AFIRE | Benjamin van Loon

MID-YEAR SURVEY / CHECKING THE PULSE

No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

AFIRE | Gunnar Branson and Benjamin van Loon

CLIMATE CHANGE / REASSESSING CLIMATE RISK

The commercial real estate industry may not yet fully grasp the actual relationship between climate risk and asset pricing and value. But the knowledge is coming fast.

York University | Jim Clayton

University of Reading | Steven Devaney and Jorn Van de Wetering

Kinston University | Sarah Sayce

UNEP FI | Matthew Ulterino

NON-TRADITIONAL / THE ALLURE OF SPECIALTY SECTORS

Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

Invesco Real Estate | David Wertheim

NON-TRADITIONAL / NON-TRADITIONAL IS GOING MAINSTREAM

The mainstreaming of nontraditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

Principal Real Estate Investors | Indraneel Karlekar, PhD

DIGITAL INFRASTRUCTURE / DIVERSIFYING INTO DIGITAL

As investors look for sustainable sources of inflation-protected yield, real estate investment is increasingly blurring into a wider range of “digital” real asset investment strategies.

AECOM Capital | Warren Wachsberger, Josh Katzin, and Corbett Kruse

LIFE SCIENCES / TAPPING INTO BIOTECH

Over the past two decades, the single-family rental industry haLife sciences real estate has been a “hot” property type for the past decade—and even more since the pandemic. Will all the capital targeting the space be placed where it needs to go?

RCLCO | William Maher, Ben Maslan, and Cecilia Galliani

ESG + CLIMATE CHANGE / HIGH-WATER MARKS

Interest and excellence in ESG performance is becoming increasingly critical to portfolio strategy. So with sea levels on the rise, how can portfolios stay above water?

Barings Real Estate | Jerry Speltz

ESG + NET-ZERO / VALUING NET-ZERO

With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

JLL | Lori Mabardi, Emily Chadwick, and Eric Enloe

ESG + FAMILY OFFICE / FAMILY OFFICES AND ESG

As sustainable investing continues to grow in popularity, family offices have taken note—and understanding ESG targets and regulations will be key for longterm performance.

Squire Patton Boggs | Kate Pennartz and Rebekah Singh

DEBT / WHY DEBT, WHY NOW?

Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

USAA Real Estate | Karen Martinus, Mark Fitzgerald, CFA, and Will McIntosh, PhD

MIGRATION / MIGRATION IN REAL TIME

As the public health situation started to improve in early 2021 and the economy reopened, did migration flows change too—and what if we are able to answer this in real time?

Berkshire Residential Investments | Gleb Nechayev

StratoDem Analytics | Michael Clawar

URBANISM / DOWNTOWN DISRUPTION

The pandemic-driven changes to downtown areas and central business districts is changing the geography of institutional investment. What else changes because of this?

Drexel University | Bruce Katz

FBT Project Finance Advisors + Right2Win Cities | Frances Kern Mennone

WORK-FROM-HOME / CHOOSING FLEXIBILITY

Employees are increasingly demanding flexibility and choice for where (and when) they work. What strategies can landlords implement to adapt?

Union Investment Real Estate | Tal Peri

TALENT AND RECRUITMENT / TALENT PARITY

To be better prepared for future risks, firms need diverse talent. So is the goal of 50% female representation achievable in global real estate investment and asset management firms?

Sheffield Haworth | Isabel Ruiz

CLIMATE CHANGE / PREDICTING THE CLIMATE FUTURE

We are all invested in the cities, assets, and infrastructure of tomorrow, even if we might not live to see the ten largest cities in 2100. But understanding climate change can get us closer.

Climate Core Capital | Rajeev Ranade and Owen Woolcock

—

ABOUT THE AUTHORS

Gunnar Branson is the CEO of AFIRE and the publisher of Summit Journal. Benjamin van Loon is Communications Director for AFIRE, and Editor-in-Chief of Summit Journal.

—

NOTES

The 2021 AFIRE International Investor Survey Report and Mid-Year Pulse Report are underwritten by Holland Partner Group.

1AFIRE. “2021 International Investor Survey Report.” AFIRE (April 2021), https://www.afire.org/of-note/2021afi resurvey/

2Members of AFIRE represent nearly 190 organizations from 23 countries, with approximately US$3 trillion in assets under management (AUM). The mid-year pulse survey collected insights from 76 executives representing unique organizations within and beyond the AFIRE membership. Regional participation in the data collection was broadly in line with AFIRE’s overall membership profile, which includes institutional investors, fund and investment managers, family offices, publicly listed companies, and related services. More than half of the respondents to the August 2021 pulse survey also participated in the annual survey, conducted in March 2021.