This article appears in Summit Journal (Fall 2020) | Download PDF |

Portfolio diversification is one of the most fundamental concepts in investing. Investors agree that diversification is a useful risk management tool employed to construct a portfolio in such a way that an investor is not overly exposed to any asset or risk.

But how investors define their diversification strategies varies widely with some conceptualizing it at the property level, and others, at the city level.

So, which is “right?”

©iStock.com/nadla

For a risk-averse investor, higher risk investments should come with higher expected returns. But high returns may not be so attractive after taking risks into account. A key finding of modern portfolio theory—the main theoretical work on diversification—is that a portfolio of uncorrelated assets should lead to a higher risk-adjusted return than investing everything in one asset.

Most of the work on and tools used in portfolio diversification analysis comes from liquid markets, in particular stocks. Physical real estate markets, by contrast, are relatively illiquid, carry a high degree of idiosyncratic locational risk, trade in large lot sizes, and have much less pricing transparency compared to stocks. These all make it more challenging to get broad-based exposure to physical real estate markets, especially for capital-constrained investors.

How, then, should physical real estate investors think about constructing a diversified portfolio in an efficient and cost-effective manner? What aggregates should physical real estate investors consider to maximize diversification benefits with scarce capital?

Consider two of the main categories investors use to build portfolios: property type and city. In this article, we aim to identify which of these two broad groupings offer the most diversification potential. Do investors get more diversification from investing across all real estate property types in a single city, or a single property type across several cities?

RETURN AND VOLATILITY DIFFERENTIALS

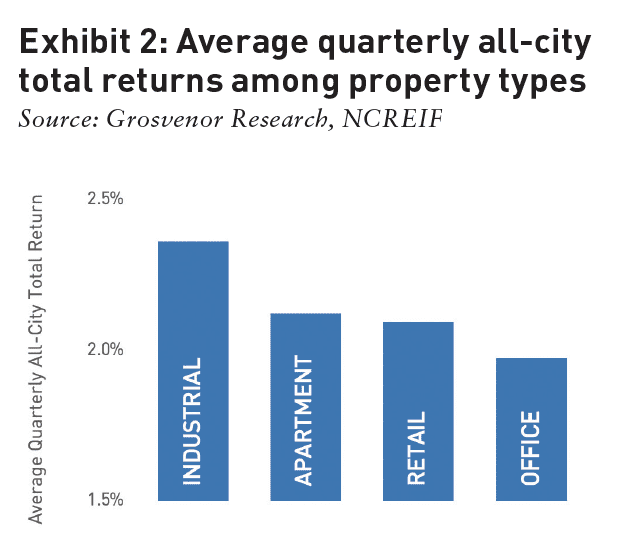

As Exhibit 1 and Exhibit 2 show, return differentials are much larger between cities than between property types. Between 2005 and 2019, NPI total returns averaged 2.1% quarter-over-quarter in our sample. There was a 1.2% differential in average quarterly returns among cities, with San Francisco registering 2.7% per quarter average return and Minneapolis seeing only 1.5% average quarterly returns.

The difference in return among cities dwarfs the difference in return among property type, where there is only 0.4% difference between the highest returning property type (industrial at 2.4%) and lowest (office at 2.0%). This is based on the 15-year historical analysis, but it is also a pattern we have observed over many different time periods.

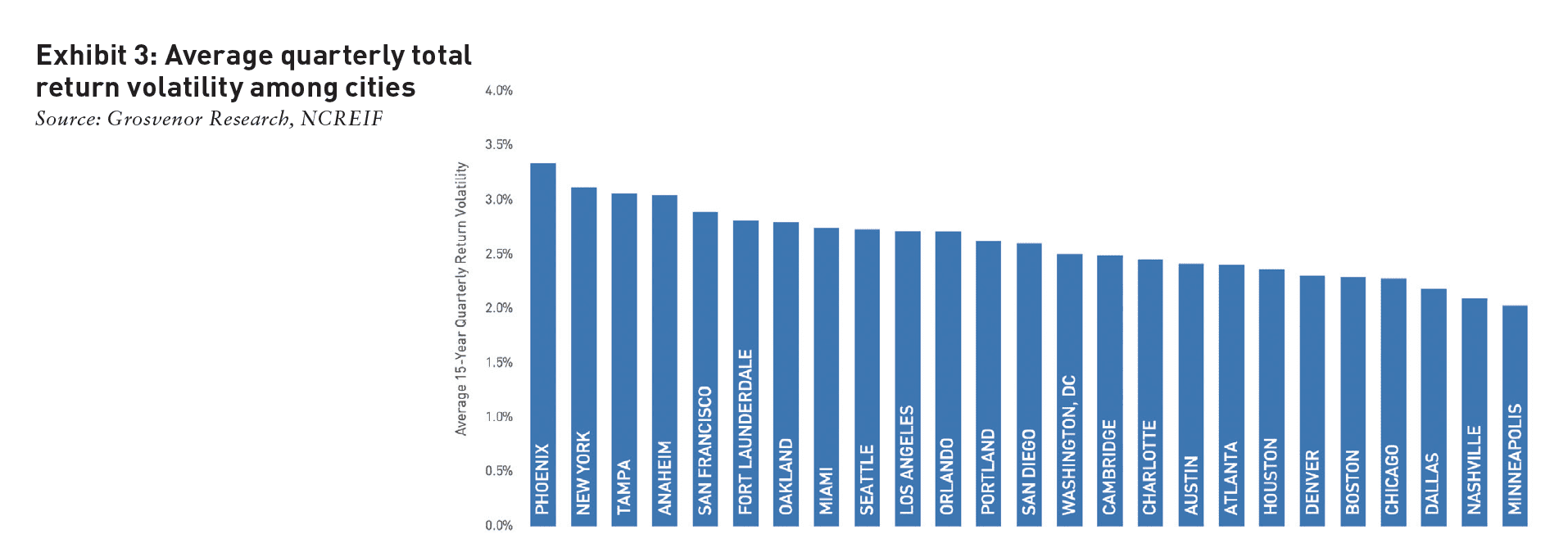

Differences in return volatility, measured by the standard deviation in returns over our sample period, are also materially larger among cities than among property types. Exhibit 3 shows that the city with the highest standard deviation in returns (Phoenix at 3.3%) was much more volatile than the city with the lowest standard deviation (Minneapolis at 2.0%).

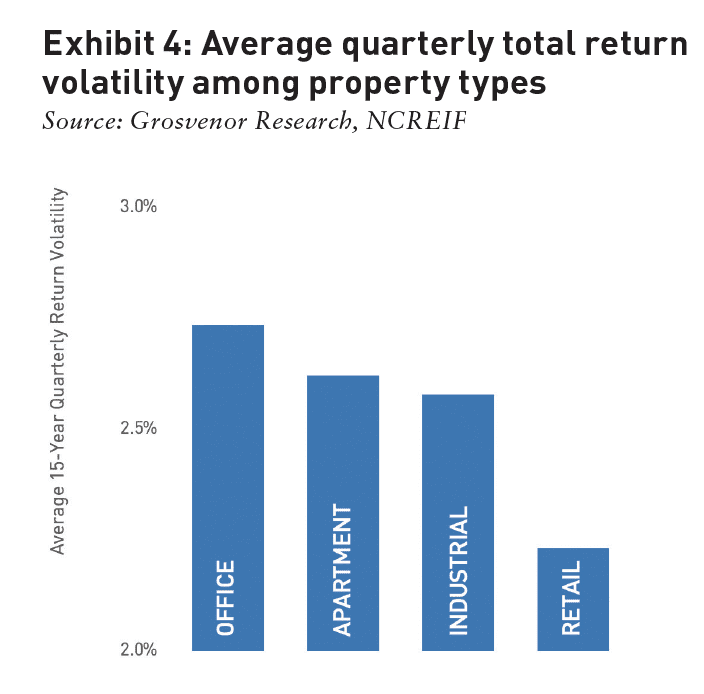

By contrast, there was only a 0.5% difference in return standard deviation between the most volatile property type (office at 2.7%) and least volatile (retail at 2.2%) property type Exhibit 4.

Correlations lie at the heart of portfolio diversification. Portfolios composed of uncorrelated assets tend to offer more diversification benefits, as seen in our analysis of correlations among cities and property types over a 15-year time horizon (consistent with our analysis of average returns above).

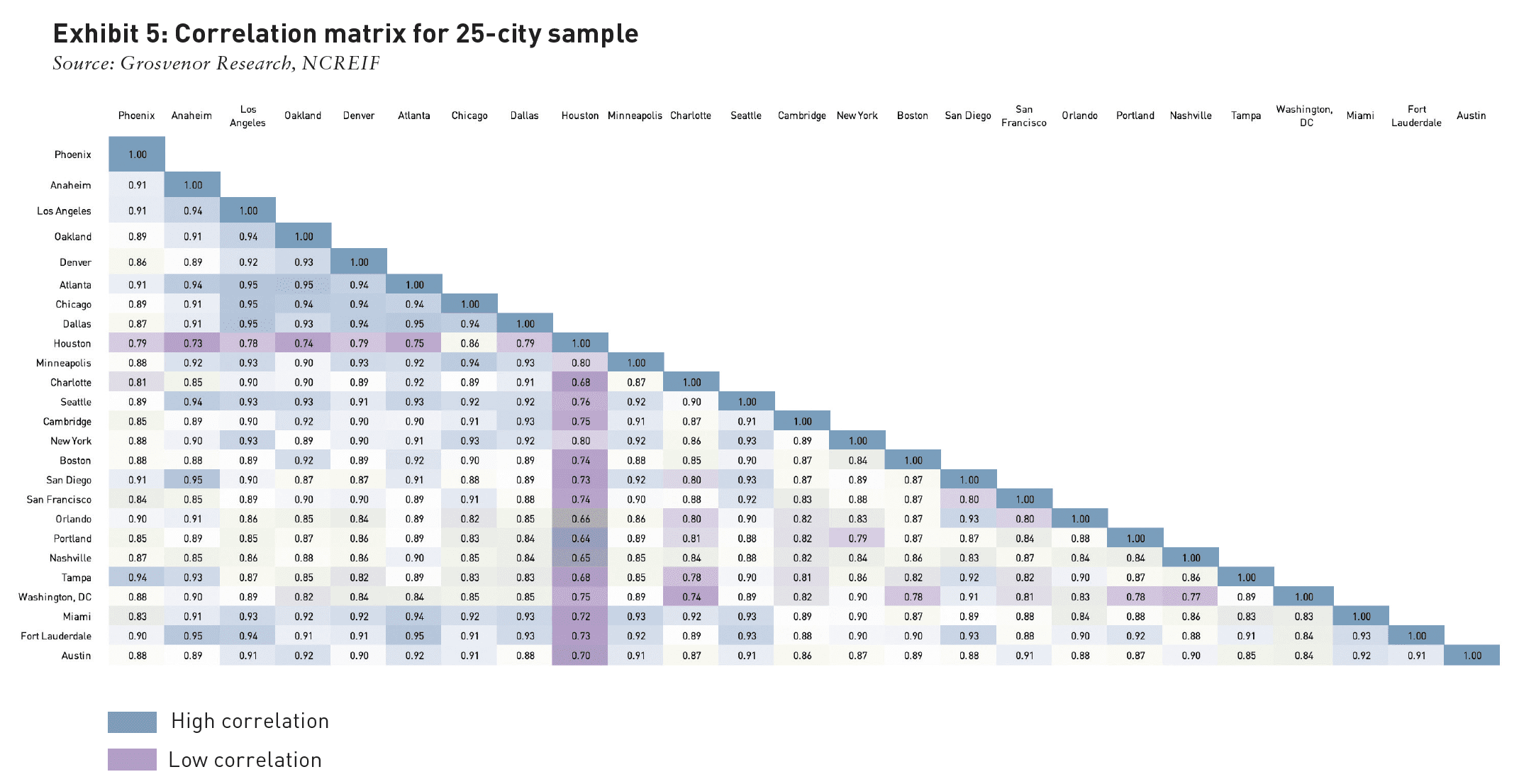

Exhibit 5 shows correlations among the 25 cities. The city of Houston, which has a property market dictated by the oil price cycle, stands out as being highly uncorrelated with any of the other cities. Washington, DC and Boston follow Houston as the second and third-least correlated to the remaining cities. Conversely, Atlanta, Seattle, and Los Angeles rank the highest in terms of their correlation to the other cities.

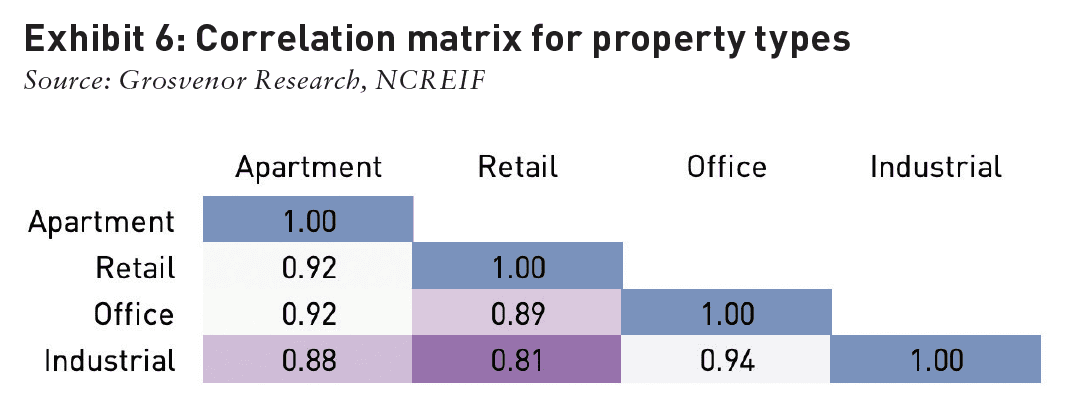

Exhibit 6 contains correlations among property types. Industrial and retail have the lowest cross-property correlations, while office and apartment exhibit higher correlations. In general, we find more pockets of low correlation among cities than property types, which suggests that the city perspective on asset allocation is likely to provide more potential for diversification.

EFFICIENT FRONTIER AND MINIMUM VARIANCE PORTFOLIOS

Considering returns and correlations, our analysis suggests that the city is the most effective lens through which to view diversification potential. How, then, should investors structure their city exposure to create a diversified portfolio?

Modern portfolio theory argues that risk-averse investors aim to maximize returns and minimize volatility in their portfolios. No single asset typically meets these criteria, so investors construct a portfolio of several assets to meet their investing goals.

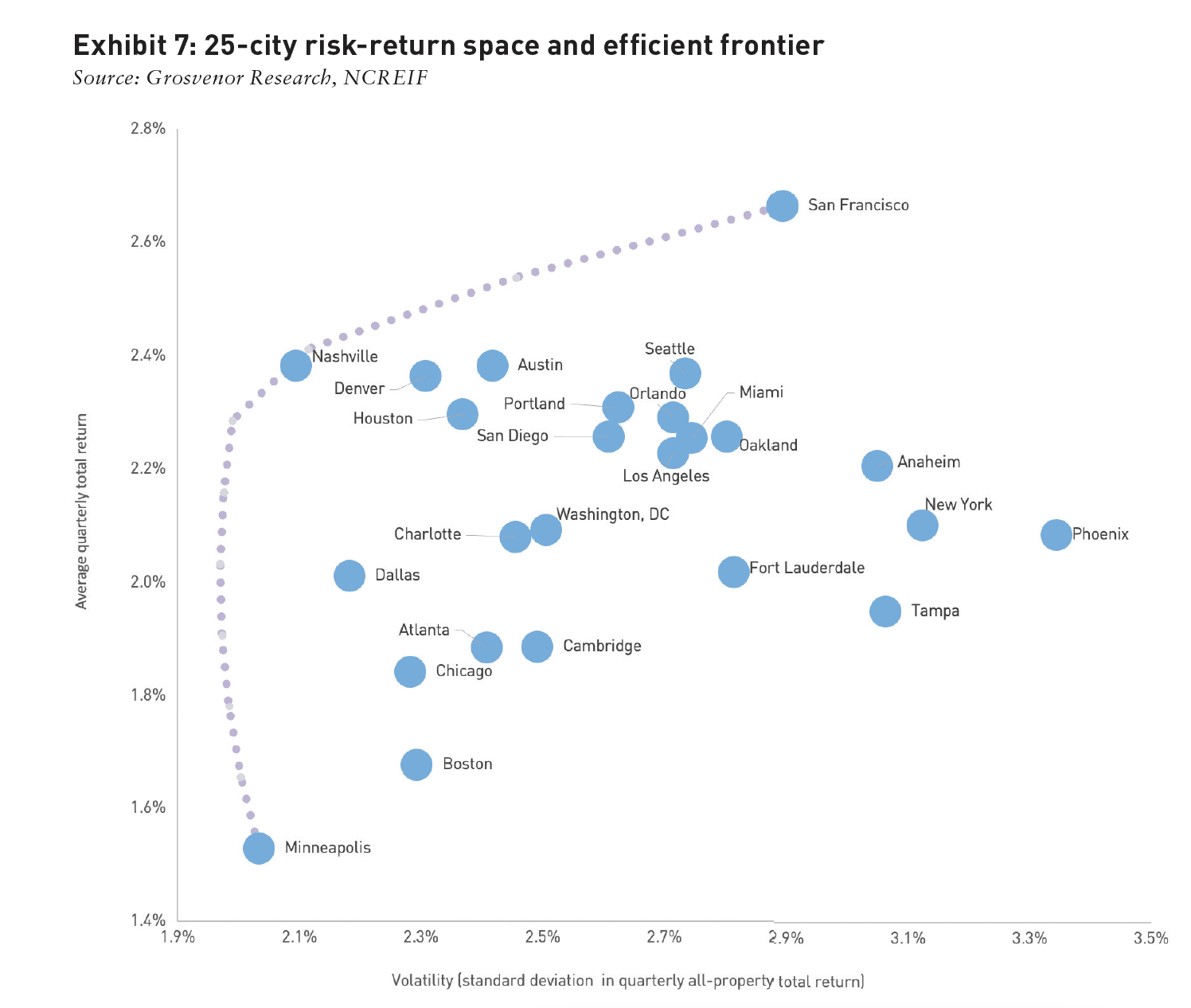

Exhibit 7 plots the 15-year average quarterly all-property return and volatility—measured by standard deviation in returns—for the 25 US cities in our sample. Using this data, we ran an algorithm that solved for the combination of cities that yielded a portfolio with the minimum volatility at various levels of target return. This set of portfolios is called the “efficient frontier” and lies to the left of most of the cities in our sample. In other words, portfolios on the efficient frontier offer better return on risk than any one asset. The only exception to this is Nashville, which lies on the efficient frontier itself.

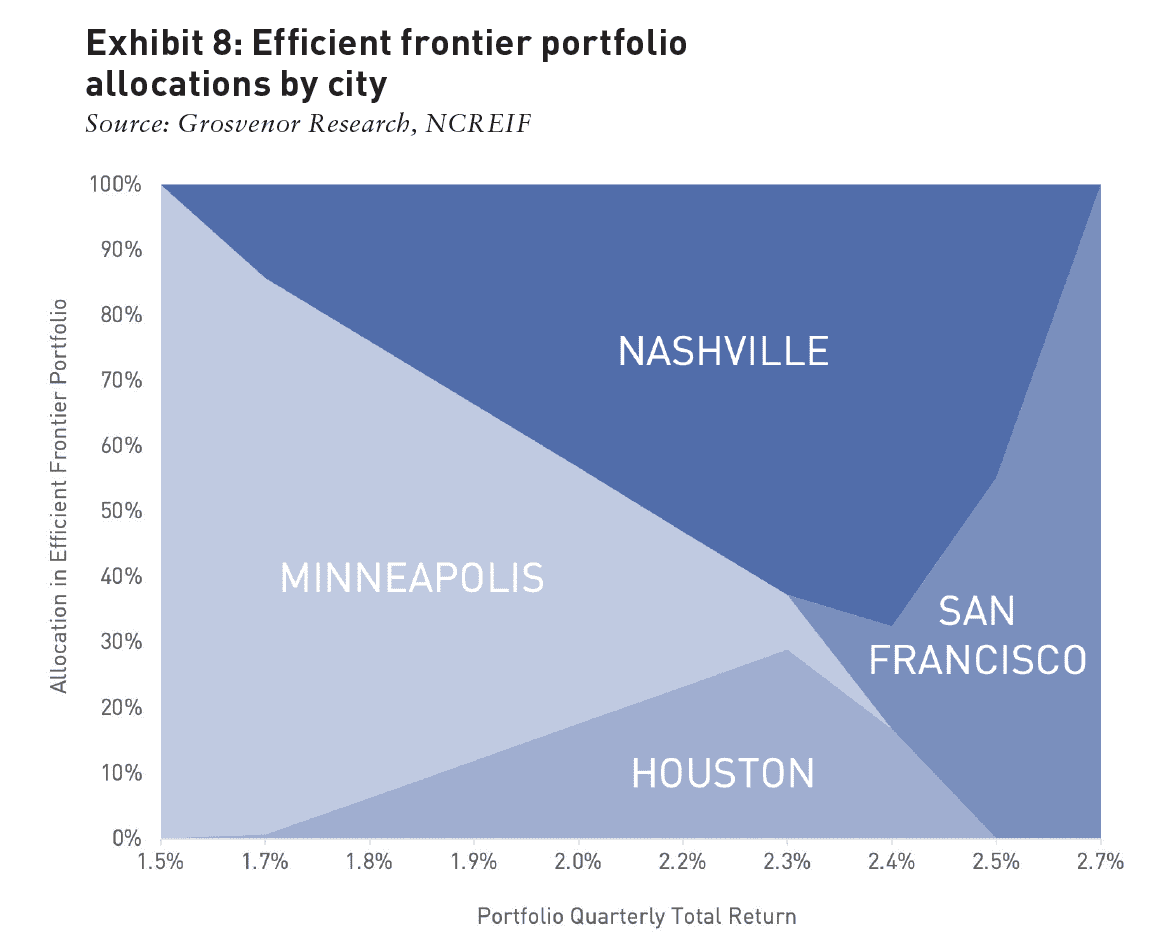

Investors do not need to invest across all 25 cities to reap the benefits of diversification. Exhibit 8 contains the cities and relative weights of the portfolios used to create the efficient frontier in Exhibit 7. At lower levels of return, a diversified portfolio would have a heavy weight towards Minneapolis with some exposure to Nashville. At higher levels of return, the portfolio tilts towards San Francisco and Houston. In any of our efficient frontier portfolios, investors only need to access four cities to reap the diversification benefits available in our sample of 25.

CONCLUSION

The COVID-19 pandemic looks like it will herald the end of a decade-long bull run in US real estate markets. In this environment, diversification and portfolio stability are front-of-mind for all investors.

Top-down portfolio construction decisions in real estate often center on geography and product type. But when allocating scarce capital, which of these two differentiators provide the most scope for diversification? Cities, rather than property types, are the more significant driver of diversification.

Not every operator or investor will have the ability to access and execute in every market. Thankfully, diversification does not mean spreading capital across all investable markets. This analysis finds that a diversified portfolio that delivers the lowest volatility at each level of return is composed of only four cities, even though our basket had 25 candidate cities. This should be welcome news for investors with limited ability to access a multitude of markets.

The city lens is a powerful tool for diversified portfolio construction. By selecting a relatively small set of cities based on their long-run total returns relationships with one another, investors can build a portfolio that offers relative stability in uncertain times.

—

ABOUT THE AUTHOR

Brian Biggs, CFA, is Research Director for Grosvenor Americas, responsible for helping set Grosvenor’s investment strategy, analyzing transactions, and advancing the firm’s thought leadership projects. Madeleine Roberts is a Research Analyst for Grosvenor America, providing economic and market analysis across Grosvenor deal functions and contributing to the organization’s thought leadership work.

—