This article appears in Summit Journal (Summer 2020) | Download PDF

While COVID-19 has conjured visions of “the end” for some, history shows that catastrophes in the human story always lead to reinvention in culture and the built environment.

On December 12, 1287, the Netherlands were forever changed because of the St. Lucia Flood. It was one of the deadliest floods in history, destroying all the villages between the sea and Amsterdam.

When the water retreated and the community rebuilt itself, Amsterdam began its transformation into the great coastal city we know today.

Source: City of Toronto Archives

There is no question that catastrophic events, such as floods, fires, and pandemics, create a real danger for humanity and impact how people live. Catastrophic events always have an economic impact, and the impact on commercial retail real estate during the current pandemic is unprecedented. It is hard to imagine what elements of our collective behaviors will permanently change after a catastrophic event. However, as humans adapt, so does real estate.

History points towards patterns of how retail adapts to crisis. Retail fulfills the primary roles of providing a foundation to rebuild communities, as well as providing long-term value appreciation to institutional investors—not to mention the benefit of its low correlation to equities.

In retail, catastrophe accelerates pre-existing consumer trends and stimulates higher long-term valuation as rebuilding efforts unlock trapped value.

PAST PANDEMIC FEARS AND RETAIL TRENDS

When the SARS pandemic hit Toronto and Hong Kong, hospitality, tourism, and retail industries were impacted severely in the near term. A study by the Chinese University of Hong Kong indicated that after SARS, consumer attitudes in Hong Kong accelerated industry wellness and social bonding trends. By June 2003 at the early ending phase of the pandemic, researchers noted, “SARS has brought some positive impacts on social/family support, mental health awareness, and lifestyle changes.”[1]

H1N1, another viral pandemic, also known as the Swine Flu, was estimated to be associated with 151,700 to 575,400 deaths worldwide during the first year it circulated in 2009, according to the US Centers for Disease Control.[2] This H1N1 virus impact was pre-empted earlier than COVID-19, but H1N1 has continued to circulate seasonally to this day, more than 10 years later.

One of the key attributes that separates viral pandemics from other natural disasters, such as floods and fires, is that they create a fear of being around other people. The invisibility of a virus also adds to alternating feelings of “fear, anxiety, and calm,” according to University of Massachusetts brain sciences professor Susan Krauss Whitbourne.[3]

Events such H1N1 and SARS have also shown that pandemics accelerated consumer awareness and priorities towards health, wellness, and family bonding. Retail adapted to meet our psychological needs and desires. Toronto and Hong Kong have since economically rebounded from both pandemics, and still have world-class shopping centers serving their communities.

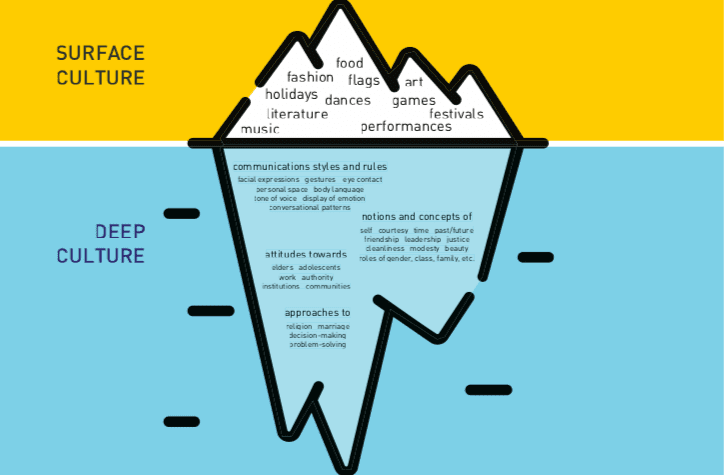

If we step back from the purely transactional focus of retail, the sector by its nature is highly valued because it serves our intersectional cultural identities. Using Gary Weaver’s Cultural Iceberg metaphor, retail speaks to more than just our surface level “fashion and food” needs and wants.

Retail is constantly reshaped by our deep cultural beliefs, based on our attitudes towards elders, adolescents, authority, and status. Retail responds to concepts of beauty, family ties, and friendship.

Consider the Envision 2020 plan presented by the International Council of Shopping Centers (ICSC). At the time it was introduced around 2015, Envision 2020 highlighted key trends shaping the retail industry (Exhibit 2).

Ultimately, consumers desired more intimacy with lifestyle brands and experiential environments, requiring accelerated developer-retailer collaboration, which we witnessed in multiple ways from 2015 to 2020.

So does COVID-19 permanently change any of these trends?

IMAGINING RETAIL AFTER CATASTROPHE

In the 1900’s, before the Great Toronto Fire, the Eaton Company, an iconic Canadian retailer based in Toronto, connected their main store and off- price retail stores through a small underground path. Four years after that connection was built, on a night of freezing temperatures in Toronto, a police constable saw flames coming from a downtown Toronto building. By the time the fire spread and was eventually extinguished nine hours later, more than a hundred buildings in the city’s core were ashes.

(ICSC Envision 2020)

Believing fire might have been associated with faulty wiring, the city pushed more infrastructure (electricity, telephone, water pipes) underground, taking a cue from the Eaton Company. However, unlike most cities, this infrastructure relocation continued for decades. Initially the underground path connected north/ south retail buildings to transit in the late 1920’s, then grew east/west in the 1970’s. Today, more than 120 years later, Toronto’s Underground PATH holds a Guinness World Record for being the largest underground shopping complex in the world. The 18.6-mile/30-kilometer maze of underground paths, with more than 3.9 million SF/371,000 SM of retail space, generates CA$1.7 billion (US$1.25 billion) in sales and more than 4,600 jobs, according to the City of Toronto.[4]

The success of the PATH system illustrates how adversity plants a seed to adapt vastly underutilized spaces. It also demonstrates how new building codes and safety requirements create an ecosystem for building more resilient, flexible, and durable spaces, which appreciate considerably for owners over the long term.

Over time, there is an opportunity for retail to be better built to meet those deep cultural needs that consumers are seeking. Forced by crisis to make more technological investments, retailers will seek to expand their margins by not having to stock excess or undesired inventories at their stores. This will force companies to find innovative ways to harvest the mountains of big data that they sit on, allowing them to be more responsive to their customers.

Where does online retailing fit into this picture? Online retailing strategically focuses more on lower-value or basic consumable products, which create frequent repurchase or refill behavior. This leaves significant room for high-margin, experiential, high-value purchases of greater quality and durability from physical store locations. Not to mention added convenience for personal service, upselling, and returns. Retailers are cautious about accelerating fulfillment costs created by online sales and the potential negative impact they have on profitability.

Over time, there is an opportunity for retail to be better built to meet those deep cultural needs that consumers are seeking.

Retailers who built productive omnichannel businesses (interconnected productive online and productive in- store platforms) are continuing to be in high demand with retail investors and developers. More variable rent structure leases are increasingly aligning landlords with tenant success, which is heightening retailer and developer collaborations.

Retail’s Resilient, Long-Term Valuation

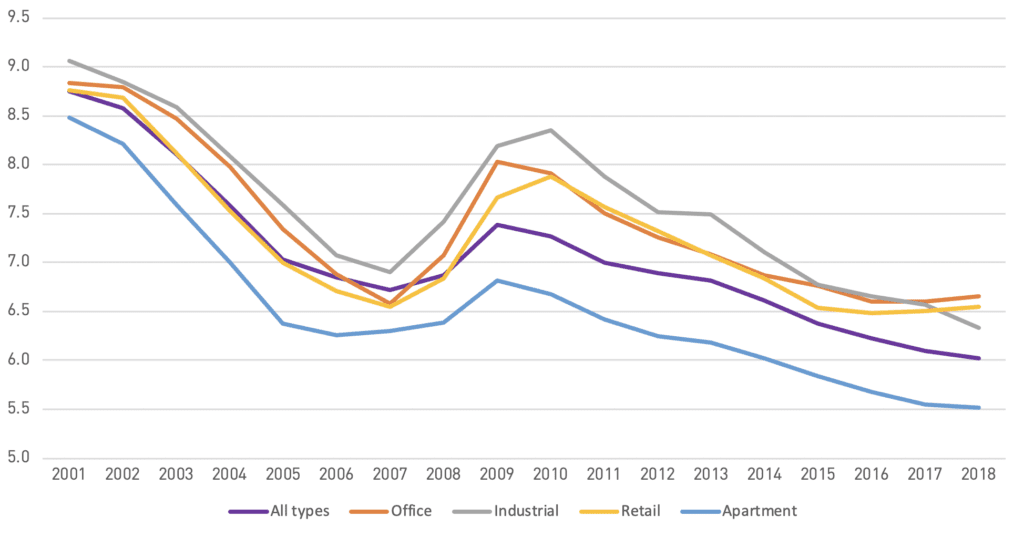

It would be fair to say that US retail been out of favor with many institutional investors the last several years. The US is also the most over-supplied country in the world, with more than 23 million SF/2.1 million SM of retail per capita in 2018.

Source: Real Capital Analytics

However, despite those headwinds, US core retail property returns have remained resilient post-dot-com bubble, 9/11 attacks, H1N1 pandemic, and increasing retailer bankruptcies. Global valuations support a similar trend of resilience historically. Investors with long-term horizons, historically have managed strong, risk-adjusted returns in retail real estate with less than 30% correlation to overall S&P 500 after major market declines.

Retailers who built productive omnichannel businesses (interconnected productive online and productive in-store platforms) are continuing to be in high demand with retail investors and developers.

These valuations often exclude the benefit captured by owners who have backfilled closing tenants and centers with non- retail uses. Abandoned retail spaces can be reborn as places of worship, apartments, hotels, car showrooms, coworking, and much more, due to their high visibility and flexible zoning designations.

As Vista Equity Partners CEO, Robert Smith has often said, “The fourth industrial revolution is real, and it is global. It relies on the ability to harness the data that is captured from real-time interactions that are taking place within the networks of their customers.”[5]

Retail transformation is aligned with this revolution, with consumers desiring more intimacy with lifestyle brands, experiential environments, and health and wellness attributes. Throughout modern history, floods, fires, and pandemics have forced the evolution of retail real estate. However, the arc of retail transformation still bends towards the technological imperative of a robust omnichannel connection with consumers. After COVID-19, owners and developers, in collaboration with retailers, will transform retail as much as nature’s fury has transformed Amsterdam.

—

ABOUT THE AUTHOR

Andrew Garrett is Executive Director, Real Estate, for the Investment Management Corporation of Ontario (IMCO), which manages more than CA$70 billion of assets with a focus on providing comprehensive and value-added investment management and advisory solutions to public-sector clients in Ontario.

NOTES

1. Joseph T.F. Laua, Xilin Yanga, H.Y. Tsuia, Ellie Panga, and Yun Kwok Wing, “Positive Mental Health-Related Impacts of the SARS Epidemic on the General Public in Hong Kong and their Associations with other Negative Impacts,” Journal of Infection 53:2 (August 2006): 114-214.

2. US Centers for Disease Control, “2009 H1N1 Pandemic (H1N1pdm09 virus),” US Centers for Disease Control (June 11, 2019), cdc.gov/flu/pandemic-resources/2009-h1n1-pandemic.html

3. Carolyn Abraham, “Your Brain on COVID-19,” The Walrus (June 18, 2020), thewalrus.ca/your-brain-on-covid-19/

4. City of Toronto, “PATH – Toronto’s Downtown Pedestrian Walkway,” City of Toronto (2020), toronto.ca/explore-enjoy/visitor-services/path-torontos-downtown-pedestrian-walkway

5. Forbes, “Money Masters 2019,” Forbes (2016), forbes.com/pictures/gkkh45imj/37-robert-smith-vista/#4d29c9a16aaf

—