While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

The US office market has been in a state of suspended animation since COVID-19 sent most office workers home more than a year ago. As one indicator of this, utilization rates for office buildings in Barings’ portfolio and across most major US cities, as of June 2021, have started to creep higher from the sub-20% levels where they have been for most of the past year, but limited office leasing and sale transaction activity has deprived the market of meaningful price discovery for assessing the pandemic’s impact on rents and prices.

Unsurprisingly, while few doubt the office sector faces a difficult near-term road ahead, there is far less consensus among real estate lenders and investors about future demand for office than any other property type.

Broader adoption of remote work will likely be a net negative for office demand going forward, but the uncertainty and differentiated landscape will create opportunity for discerning investors. The forced work-from-home (WFH) experiment during the pandemic has effectively compressed years of obsolescence into a span of about eighteen months, and both companies and workers will increasingly have the ability to substitute technology for physical office settings. However, the top strategic priorities for most companies post-pandemic will not be terribly different from those before the pandemic—namely, growing earnings and attracting and retaining the best talent. So, while earnings objectives increase the likelihood that companies will find a way to leverage technology to reduce their real estate costs, the intensifying war for talent will continue to make the office important—perhaps even more important—as a place for collaboration, cultivating corporate culture, training, mentoring, socialization, and productivity.

For investors with or seeking office exposure, three drivers— (1) the transition to a hybrid workplace, (2) employment growth in science, technology, engineering, and mathematics (STEM), and creative industries, (3) and the escalating war for talent—will shape office demand in the recovery ahead and ultimately determine which assets and markets will be winners and which will be losers.

ASSESSING THE DAMAGE

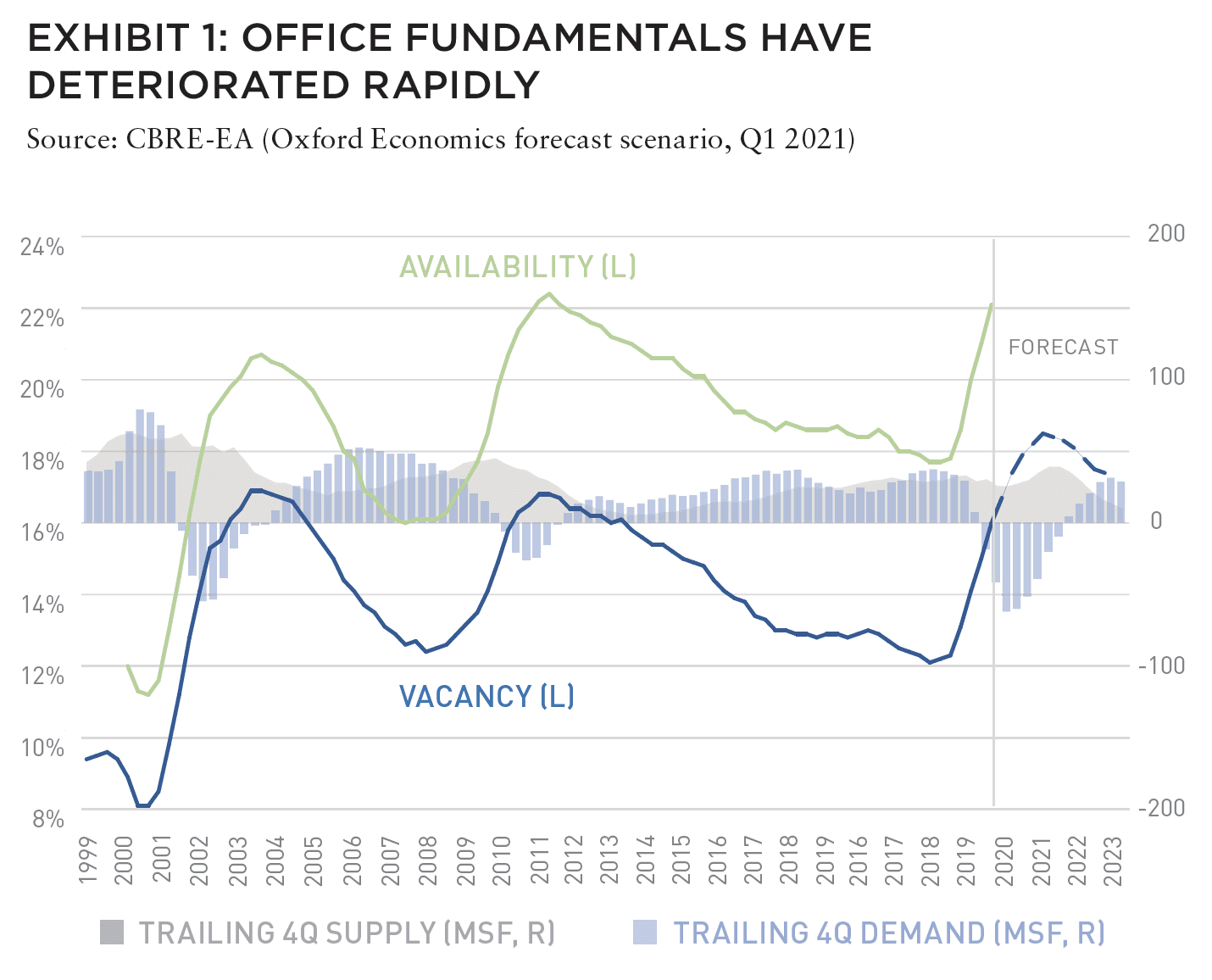

The pandemic and lockdown measures meant to contain its spread have taken a serious toll on US office market fundamentals, and conditions in most markets will likely get worse before improving. The combined effects of a year with little or no new leasing, givebacks of space (including sublease offerings), and a cyclical peak in new construction have created a perfect storm, driving vacancy rates to the highest levels in more than a decade.

Office demand, as measured by net absorption, turned negative in the first quarter last year, and according to CBRE Econometric Advisors (CBRE-EA), has since grown to nearly -110 million SF/-10.2 million SM, or more than twice the total during the GFC. With supply continuing to deliver and not expected to peak until next year, the overall US office availability rate, which includes occupied space available for sublease, has increased 440 BPS since year-end 2019 to 22.1%.

While the severe hit to office market fundamentals makes sense in the context of the nearly three million office jobs lost in March and April 2020, the weak office demand forecasts are difficult to reconcile with the strong rebound in office-using employment since May 2020 and the positive outlook for office job gains going forward. CBRE-EA’s forecasts anticipate another -36 million SF/-3.34 million SM of negative net absorption over the remainder of 2021 against a forecast 1.1 million increase (per Moody’s Analytics) in office-using jobs that will leave office employment slightly ahead of the pre-pandemic level. Viewed simply on the basis of occupied office stock, and after factoring in expected absorption and completions, the forecasts point to a 4.2% decline in occupied space at essentially the same (i.e., pre-pandemic) level of employment.

The COVID recession is fundamentally different from the early 2000’s “tech wreck” and the “Great Recession” a decade later. However, a continuation of negative net absorption would be a departure from the two previous cycles, when absorption and office job growth turned positive around the same time. Office-using employment during the pandemic and GFC suffered a similar decline in absolute levels and as a share of total employment, but both the fall and the recovery in jobs from the pandemic shock have progressed much faster. Office-using employment during the GFC declined for 32 months before hitting bottom, then took another 44 months to regain the pre-GFC level. In the COVID downturn, office jobs reached a five-year low just two months into the pandemic, but have already recovered about 1.9 million (65%) of the jobs lost and, per Moody’s Analytics, will recover to pre-pandemic levels by year-end 2021—just 22 months from the previous peak.

A BIFURCATED RECOVERY

Whether or not the office recovery can advance at an accelerated pace, the bigger questions for office investors clearly revolve around the potential longer-term impacts on office demand and use from the pandemic experience. Despite conflicting headlines of companies’ intentions—which range from re-affirming commitments to an office-centric future to transitions to fully remote corporate structures with little or no office space—survey data and anecdotal evidence increasingly point to a hybrid model where workers have greater flexibility in where and how much time they spend in the office.

The design and use of the hybrid office will vary widely by company, but most likely will include some combination of traditional workspace for workers who are either unable or unwilling to work remotely, and space that serves a more specialized purpose—collaboration, training, socialization—that is difficult to replicate through technology alone.

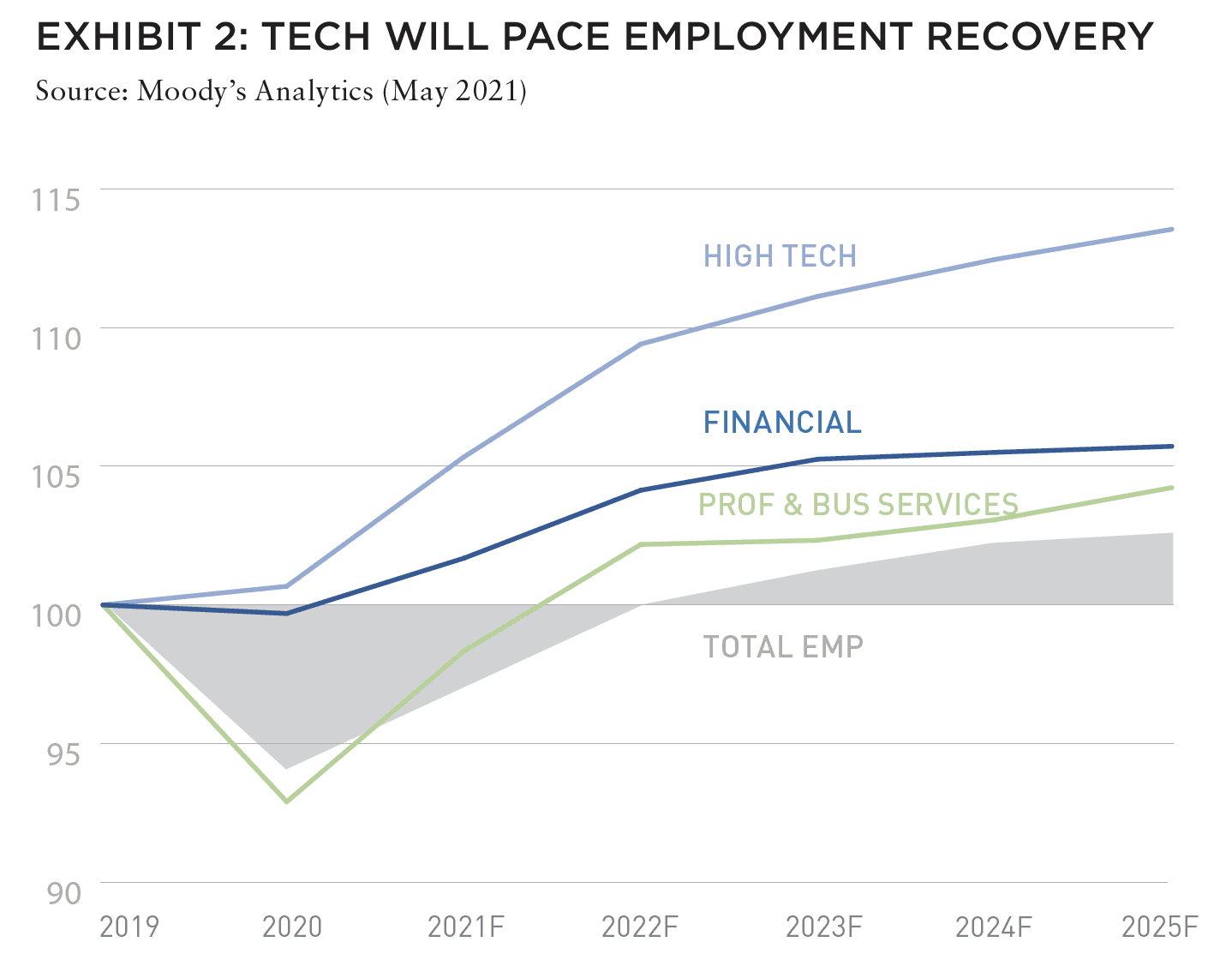

From a pure demand perspective, while broader adoption of remote work will enable companies to shrink their office footprints, office-using employment growth should provide a structural tailwind to office demand as the economy continues to evolve to a knowledge-based structure and office-using employment continues to capture a growing share of total job growth. As part of that process, with the ongoing digitization of the economy, the most dynamic growth will continue to be in high-tech and, more broadly, STEM sectors. From 2010 to 2019, high-tech employment expanded by about 3.5% per year, more than double the 1.4% growth rate for the labor market overall, and STEM sectors continued to add jobs in 2020. That outperformance is expected to continue over the next several years at least. Moody’s Analytics forecasts high-tech employment will expand at a 1.5% annual rate over the next five years versus 1.2% for total employment.

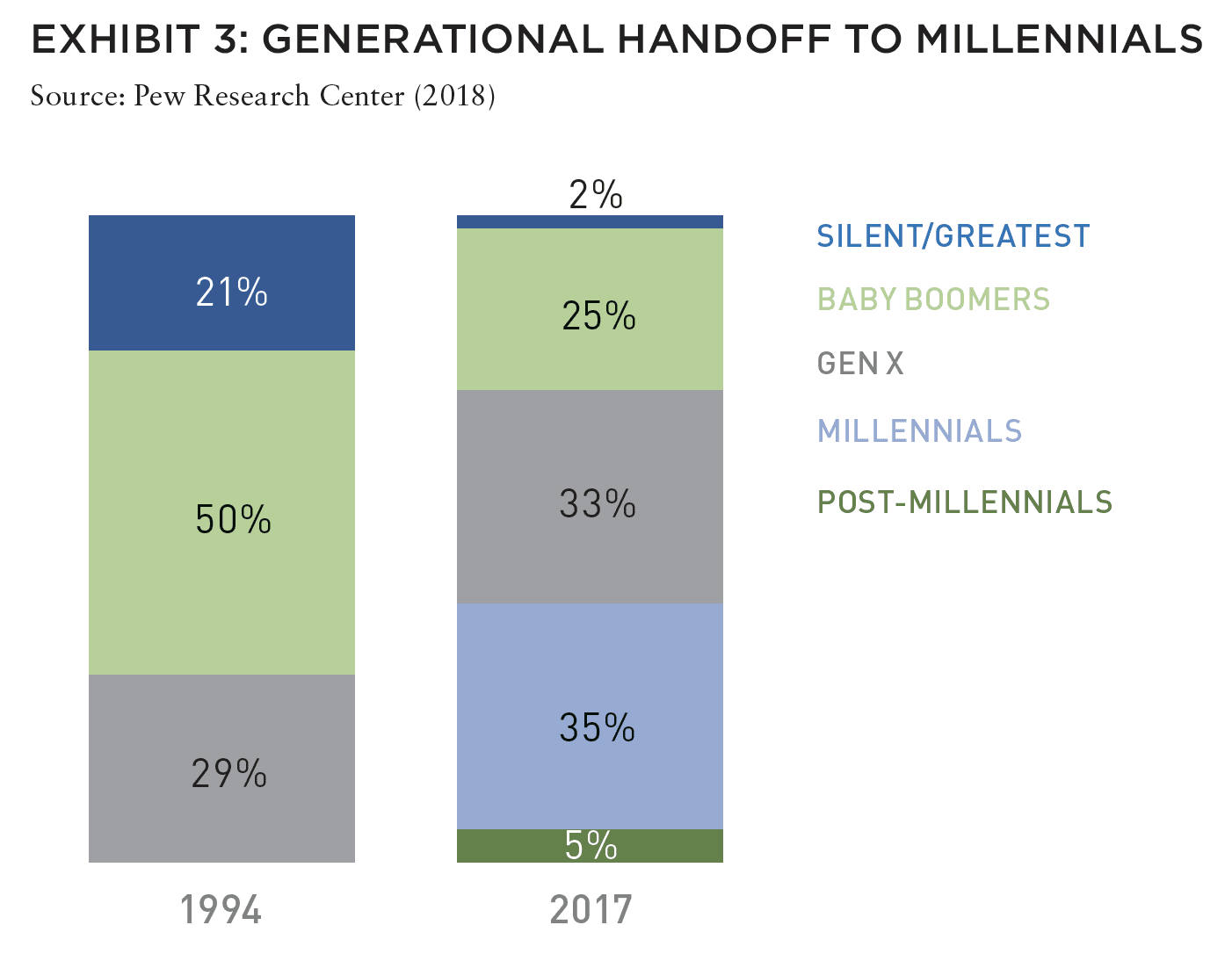

The strong growth forecast should provide a solid foundation for the office demand recovery, but it will also contribute to the escalating war for talent, which will only intensify as working-age population growth slows and innovation becomes the key driver of the US economy. The US population is undergoing a generational handoff from the baby boomers (those born from 1946–1964), who for decades have dictated all things in the economy, culture, and public policy, to millennials (1981–1996), who now comprise the largest share of the US labor force. For employers in knowledge-based sectors, especially highly competitive STEM fields, the ability to attract and retain well-educated millennials will be paramount. The physical workplace and remote work policies will be important weapons in that effort.

Taken together, the transition to a hybrid workplace, growth in office-using employment, and the escalating war for talent point to a bifurcated office recovery and future state that widens the gap between “space with a purpose” and generic, “commodity” space that faces increased competitive pressures from remote work.

In the near term, we expect the pandemic will increase demand for modern, “healthy” office buildings as companies seek to provide a safe environment for workers to return to the office. Longer term, the most competitive space will be in office buildings designed for a more agile workforce and the next generation(s) of knowledge workers who we believe will demand highly amenitized workplaces with best-in-class ESG credentials.

PREDICTING DEMAND

Changes in office demand, use, and design will take time to manifest, and aggregate demand will expand as office employment outpaces overall job growth. While this will help mitigate the immediate impact of the trends accelerated by more than a year of working remotely for most office workers, we believe the pandemic will have a lasting impact on office occupier and worker behavior going forward.

The WFH experiment has let the remote work genie out of the bottle, mostly by proving out technology that was widely available but woefully underutilized before the pandemic. While the wider adoption of remote work will render large segments of existing office stock less competitive, not unlike what has transpired in the retail sector over the past twenty years, office assets that meet the new standards should attract robust demand (and command premium rents) as companies seek to leverage the office to cultivate corporate culture, enhance innovation and productivity, and compete for talent.

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

—

ABOUT THE AUTHOR

Philip Conner is Head of US Real Estate Research and Strategy and Ryan Ma is Managing Director of Real Estate Research for Barings Real Estate, a US$354+ billion global financial services fi rm dedicated to meeting the evolving investment and capital needs of our clients and customers.

—