Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

While there is no standard definition of “specialty” property sectors, they include a variety of non-traditional residential and commercial properties. With respect to residential real estate, these specialty sectors span single-family rental (SFR) homes, manufactured housing, student housing, and senior housing.

In commercial real estate, specialty includes data centers, infrastructure, self-storage, life science, and medical office, among others.

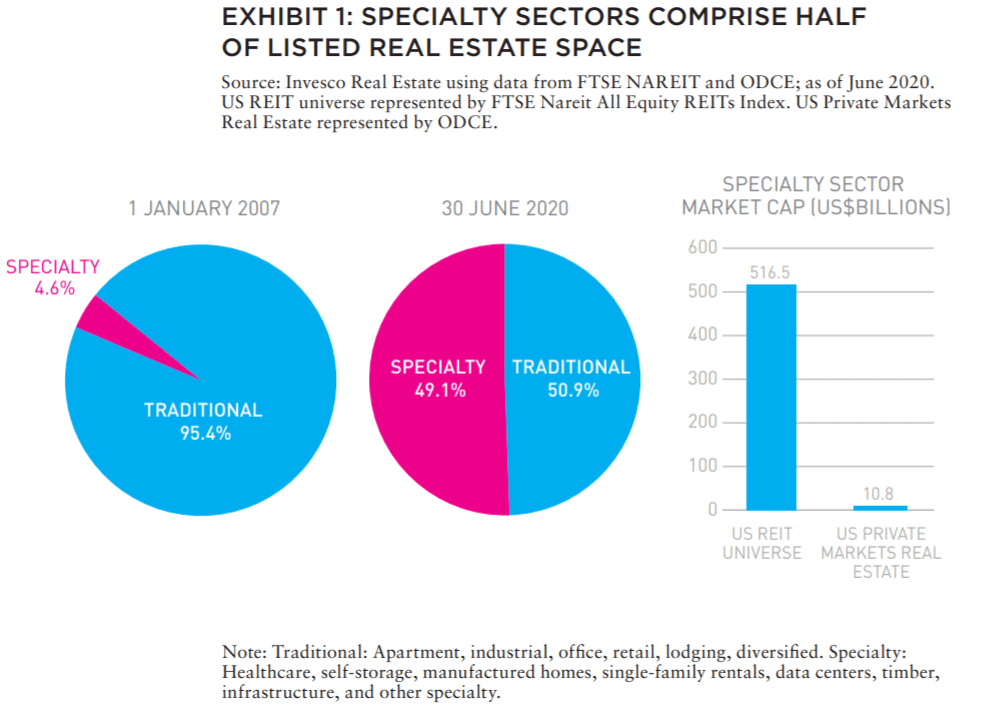

The representation of specialty sectors in real estate securities indices has grown tremendously. In June 2020, they accounted for roughly half the collective market capitalization, compared to less than 5% in early 2007. However, in many private market real estate constructs, they still play only a minor role. Whereas the total market capitalization of specialist REITs is now well above US$500 billion, private vehicles account for a mere US$10 billion (Exhibit 1).

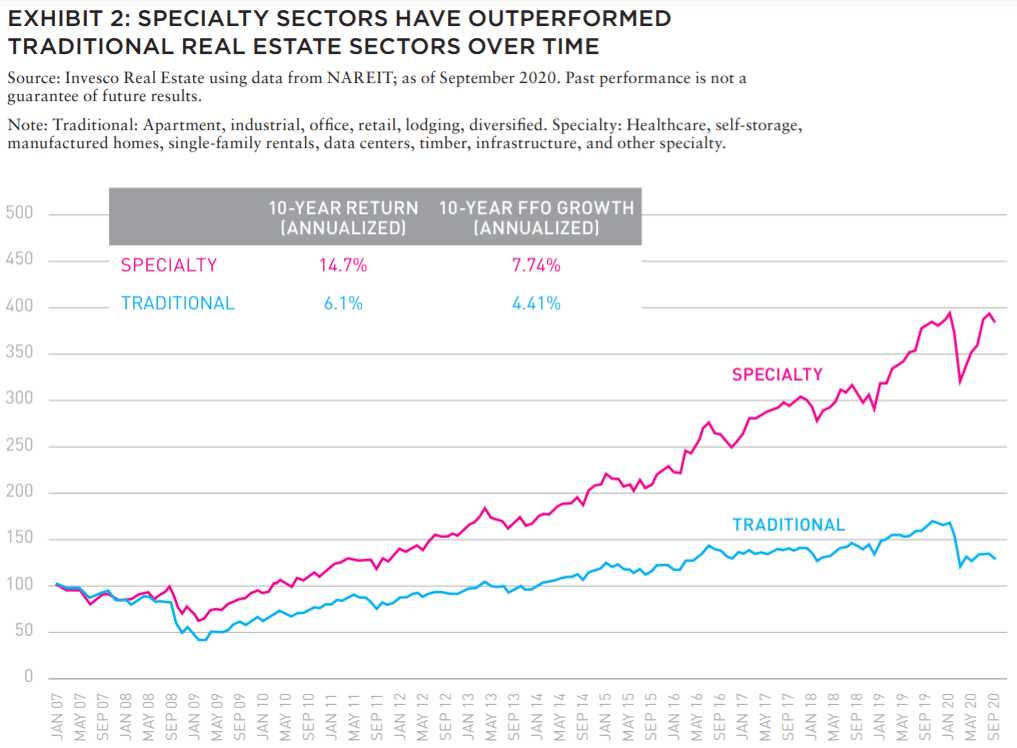

Since early 2007, cash flows in specialty sectors outpaced traditional sectors and, not surprisingly, their annualized returns were more than twice as high (Exhibit 2). This robust growth has been spurred by changes in demographics, education, preferences for renting rather than owning, and even downsizing trends. Additionally, several specialty sectors have enjoyed strong tailwinds from technological and medical advancements (Exhibit 2).

DATA CENTERS

Data centers typify a specialty sector that benefits from technological changes, including how society is increasingly consuming data. At the basic level, data centers are secured warehouses containing racks that house network equipment and servers critical for data processing and storage, as well as cloud computing. These facilities provide sophisticated amenities, such as backup generators and industrial air conditioners, to keep computer equipment cool, as well as optical connections for linking business partners and service providers.

While data center shells are relatively simple to build, the complexity of the interior infrastructure requires high upfront capital expenditures and an equally high level of operating expertise, constituting significant barriers to entry. Not surprisingly, lease terms are often 5–15 years, and data center REITs typically enjoy high customer retention rates due to the complexity and cost of moving. Tenants often form network ecosystems through colocation (in part to achieve lower latency and higher speeds), which tends to increase the value of a data center as more tenants choose that location for their operations.

Data center characteristics mean that server racks and digital content are owned and managed by tenants, while the physical warehouse is owned by the data center. The most desirable features for tenants often relate to technology ecosystems, power availability and cost, fi ber connectivity, and protection from natural disasters. Furthermore, the lease characteristics are based on the usage of power.

The fundamentals appear robust based on the rapidly increasing data needs of tenants spanning the technology, financial services, and communications industries. The secular growth story is buttressed by the rapid expansion of cloud computing, increasing demand for mobile data, and the inexorable growth of the digital economy. The impact of the pandemic has so far been minimal on data centers, which are relatively unaffected by social distancing and were among the best performing REIT sectors in 2020. The annual size of the global datasphere is expected to triple from 2020 through 2025, and demand from both consumers and enterprises should support the data center business model for years to come.

INFRASTRUCTURE

As another technology-driven and higher-growth specialty sector, infrastructure includes assets such as cell phone towers and small cell nodes. The largest tower companies are structured as REITs and play a crucial role in enabling wireless communications. Cell towers are the physical foundation of nearly all wireless connectivity. Tower companies own the vertical real estate— usually a tower or pole, often with a land parcel underneath— and the fiber cable underground. Wireless carriers, broadband providers, cable companies, and government agencies lease space on towers to mount equipment, such as cell transmitters. By leasing space on thousands of towers domestically and globally, wireless carriers have built communications networks to handle the ever-increasing volume of mobile data traffic.

Infrastructure companies have benefitted from rapid growth in mobile data consumption as well as increased traffic loads in the burgeoning work-from-home environment. The lease terms for these assets are often 5–15 years, and infrastructure providers typically enjoy high customer retention rates due to the complexity and cost of moving, as well as the lack of viable alternatives in the oligopolistic US market. Furthermore, infrastructure should be a prime beneficiary of the coming wave of 5G wireless connectivity. Initial 5G smartphones are expected to consume 270x data than 2G-era phones, and roughly 3x the data of current phone models.1

In our view, 5G will help expand the industrial and enterprise use cases for mobile connectivity by enabling a volume of simultaneous connections, data speeds, and ubiquity of coverage that were not previously available. New use cases could include self-driving vehicles, remote health care, smart manufacturing, smart cities, drones-as-a-service, and virtual reality, among others. Simply put, tower and data center REITs are uniquely positioned to benefit from the initial multi-year infrastructure buildout for 5G, and later from the potential step change increase in data transmission that will result from widescale deployments.

SINGLE-FAMILY RENTALS

The residential sector is one of the four traditional pillars of commercial real estate and encompasses several property types: apartments, SFR, manufactured housing, and student housing. The overall sector has performed well over the past several years—right up to the market downturn in February 2020. However, residential has been structurally undersupplied worldwide since the GFC. Additionally, extremely low unemployment rates in the US and other countries have helped support high residential occupancy rates. Strong growth in the young adult age cohort was also a tailwind, as this demographic has a higher propensity to rent.

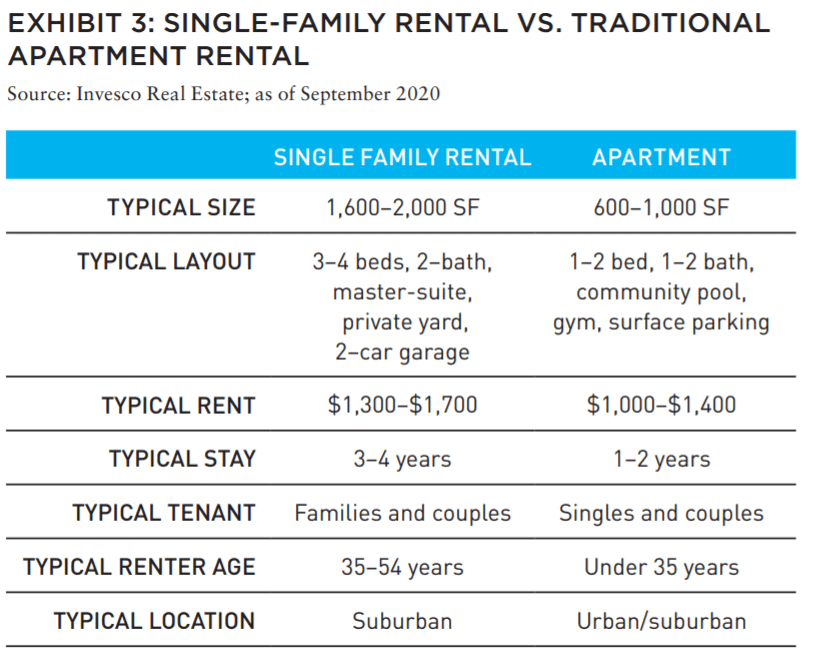

SFR homes are a specialty subsector of residential and are growing substantially faster than apartments due to their differing characteristics (Exhibit 3). The pandemic has accelerated this trend, as many renters now seek a lowerdensity living environment in a more suburban setting. SFR totals about 15 million units, similar in size to the traditional apartment market, yet SFRs have one of the most attractive multi-year demand profi les in US real estate, according to industry analysts.2 Job growth across Sun Belt-focused footprints has been solid, homeownership has been stuck in neutral, and this segment’s demographic tailwind should accelerate in the next several years as apartment renters age toward prime SFR years.3 In this regard, as millennials reach adult milestones, they typically seek more living space.

SFR has also benefitted from changing views among millennials and Gen Xers, as fewer of them own a home, want to own a home, or even live on their own, compared to prior age cohorts.4 In fact, they value the optionality provided by renting, along with the concomitant increase in mobility. Simply put, the SFR market bridges the gap between apartment living and home ownership.

Demand for SFR has been strong, in part because of increased demand for lower-density environments in suburban settings. Additionally, extreme fi nancial dislocation for many consumers, combined with stress in the banking sector, has likely reduced the number of renters who can afford the move to home ownership. This, in turn, could lead to higher retention rates for residential landlords.

Finally, a residence is need-to-have real estate, which should warrant priority in a consumer’s payment stack. Not surprisingly, the drop in occupancy rates for the residential sector has typically been lower than the drop for many other property sectors during prior economic downturns.

HEALTHCARE AND LIFE SCIENCE

Healthcare is one of the largest segments of the US economy, comprising approximately 18% of GDP. The sector continues to grow faster than the overall economy on the back of a rapidly aging population.5 There are multiple segments of the health care sector, but just two of them account for almost 75% of the listed health care REIT space: senior housing and medical office.6

However, there is another specialty subsector in health care: life science (i.e., lab space), which we believe is positioned to perform well based on strong fundamentals that remain essentially untouched by COVID-19. Life science accounts for roughly 10% of US health care REIT assets and consists primarily of specialized offices for biotech and pharmaceutical tenants, who use the space to develop new drugs.7 Lease terms are often 8–10 years, and renewal rates are typically high because of the complexity and cost required to build out sophisticated lab space. Demand for this kind of specialized real estate is only expected to grow as a result of the heightened global focus on new drug development.

ALSO IN THIS ISSUE (FALL 2021)

NOTE FROM THE EDITOR / GROUPTHINK VS. GROUP COLLABORATION

AFIRE | Benjamin van Loon

MID-YEAR SURVEY / CHECKING THE PULSE

No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

AFIRE | Gunnar Branson and Benjamin van Loon

CLIMATE CHANGE / REASSESSING CLIMATE RISK

The commercial real estate industry may not yet fully grasp the actual relationship between climate risk and asset pricing and value. But the knowledge is coming fast.

York University | Jim Clayton

University of Reading | Steven Devaney and Jorn Van de Wetering

Kinston University | Sarah Sayce

UNEP FI | Matthew Ulterino

NON-TRADITIONAL / THE ALLURE OF SPECIALTY SECTORS

Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

Invesco Real Estate | David Wertheim

NON-TRADITIONAL / NON-TRADITIONAL IS GOING MAINSTREAM

The mainstreaming of nontraditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

Principal Real Estate Investors | Indraneel Karlekar, PhD

DIGITAL INFRASTRUCTURE / DIVERSIFYING INTO DIGITAL

As investors look for sustainable sources of inflation-protected yield, real estate investment is increasingly blurring into a wider range of “digital” real asset investment strategies.

AECOM Capital | Warren Wachsberger, Josh Katzin, and Corbett Kruse

LIFE SCIENCES / TAPPING INTO BIOTECH

Over the past two decades, the single-family rental industry haLife sciences real estate has been a “hot” property type for the past decade—and even more since the pandemic. Will all the capital targeting the space be placed where it needs to go?

RCLCO | William Maher, Ben Maslan, and Cecilia Galliani

ESG + CLIMATE CHANGE / HIGH-WATER MARKS

Interest and excellence in ESG performance is becoming increasingly critical to portfolio strategy. So with sea levels on the rise, how can portfolios stay above water?

Barings Real Estate | Jerry Speltz

ESG + NET-ZERO / VALUING NET-ZERO

With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

JLL | Lori Mabardi, Emily Chadwick, and Eric Enloe

ESG + FAMILY OFFICE / FAMILY OFFICES AND ESG

As sustainable investing continues to grow in popularity, family offices have taken note—and understanding ESG targets and regulations will be key for longterm performance.

Squire Patton Boggs | Kate Pennartz and Rebekah Singh

DEBT / WHY DEBT, WHY NOW?

Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

USAA Real Estate | Karen Martinus, Mark Fitzgerald, CFA, and Will McIntosh, PhD

MIGRATION / MIGRATION IN REAL TIME

As the public health situation started to improve in early 2021 and the economy reopened, did migration flows change too—and what if we are able to answer this in real time?

Berkshire Residential Investments | Gleb Nechayev

StratoDem Analytics | Michael Clawar

URBANISM / DOWNTOWN DISRUPTION

The pandemic-driven changes to downtown areas and central business districts is changing the geography of institutional investment. What else changes because of this?

Drexel University | Bruce Katz

FBT Project Finance Advisors + Right2Win Cities | Frances Kern Mennone

WORK-FROM-HOME / CHOOSING FLEXIBILITY

Employees are increasingly demanding flexibility and choice for where (and when) they work. What strategies can landlords implement to adapt?

Union Investment Real Estate | Tal Peri

TALENT AND RECRUITMENT / TALENT PARITY

To be better prepared for future risks, firms need diverse talent. So is the goal of 50% female representation achievable in global real estate investment and asset management firms?

Sheffield Haworth | Isabel Ruiz

CLIMATE CHANGE / PREDICTING THE CLIMATE FUTURE

We are all invested in the cities, assets, and infrastructure of tomorrow, even if we might not live to see the ten largest cities in 2100. But understanding climate change can get us closer.

Climate Core Capital | Rajeev Ranade and Owen Woolcock

Historically a niche sector, life science has rapidly gone mainstream in recent years, with an impressive track record. Some real estate investment players are focused on biotech cluster markets like Boston, San Francisco, and San Diego, while others are located on university campuses or near major medical facilities. In terms of asset value, life science has fared the best in the health care sector this year, according to industry analysts, with values virtually unchanged compared to pre-pandemic levels.8

THE BRIGHT SPOTS OF TOMORROW?

Even with current dislocations in the property market, certain specialty sectors could continue to benefit from several potentially sustained tailwinds while facing limited impact from the pandemic.

Despite the many uncertainties surrounding the economy and capital markets, REITs operating in these sectors are poised to benefit from robust demand in relatively supply-constrained markets. This can translate into above-average revenue, cashflow, and earnings growth, which is why these specialty sectors present potentially attractive opportunities for investors.

—

ABOUT THE AUTHORS

David Wertheim is Senior Director, Client Portfolio Manager for Invesco Real Estate, one of the world’s largest real estate managers.

—

NOTES

1. Heidi Vella, “5G vs. 4G: What is the Difference?” Raconteur, Last modifi ed May 16, 2019. heidivella.com/2019/05/16/article-raconteur-5g-vs-4g-whatis-the-difference/

2. Green Street, s.v. “Residential Sector Update,” accessed March 3, 2020. greenstreet.com/

3. Green Street, s.v. “Residential Sector Update”

4. John Burns Real Estate Consulting, LLC, s.v. “Burns Single-Family Rental Analysis and Forecast,” accessed October 2019. realestateconsulting.com/our-company/research/single-family-rental-analysis-and-forecast/

5. Green Street, s.v. “Health Care Sector Update,” accessed December 4, 2020.

6. Green Street, s.v. “Health Care Sector Update”

7. Green Street, s.v. “Health Care Sector Update”

8. Green Street, s.v. “Health Care Sector Update”