How are shorthand labels like the “Sun Belt” and the “Rust Belt” shaping investment decisions? Should they?

Reports of a mass exodus from northern US cities have become ubiquitous during the pandemic, while southern cities, towns, and suburbs continue to grow. Population shrinkage in northern “Rust Belt” cities has gone on for so long that it is no longer news—and many investors have simply lost interest in the region.

The “Sun Belt” investment strategy has become the standard for serious investors in the US property markets. The migration accelerated by COVID has only increased investor confidence. Yes to the Sun Belt, No to the Rust Belt—end of story.

And yet, this universal certainty is concerning. “Everyone agrees” is usually a sign that assumptions need to be examined.

Assumptions are dangerous, of course, because they determine how facts are interpreted. Assumptions like to hide. Whether cloaked in language and metaphors, or in graphs, historical spreadsheets, and pro-formas, it’s important to know that the assumptions are always there and to understand what they are doing.

SUN VS. RUST

The concept of Sun versus Rust paints a compelling picture: shrinking northern cities and expanding southern cities. This picture becomes clearer with analyses such as the 2020 Migration Report from North American Moving Services, which showed that in 2020, even more people migrated away from Rust Belt states such as Illinois, Michigan, and upstate New York for Sun Belt destinations such as Arizona, Texas, Florida, and the Carolinas.[2] In Illinois, for example, residents have moved away at a rate of one person every ten minutes—for fifteen years. As with other cultural changes during COVID, this migration from North to South has proven to be consistent and, in some cases, accelerating.

Pandemic aside, why have people been migrating? There are many reasons, of course, but according to Harvard Economist Ed Glaeser, “Since the 1970s, increases in housing supply have been as important as increases in productivity in driving the increases in Sun Belt population.”[3] Simply stated, homes cost less in the South. At the same time, taxes in those regions are minimal. Of course, warmer weather doesn’t hurt, and as baby boomers, the largest demographic cohort, transition into retirement, they also drive-up demand.

Investors assume that these migratory trends will continue. This assumption may be correct, but how much does it take into account all risks and opportunities in both regions—and for how long?

DECONSTRUCTING THE SHORTHAND

The term Sun Belt was coined in the late 1960’s, and around the same time, the Rust Belt emerged as a shorthand way to describe manufacturing centers located in a “belt” from upstate New York, to Pittsburgh, Cleveland, Detroit, Chicago, and Milwaukee. As these former industrial centers became obsolete or fell behind to new competition, companies moved, outsourced, or went out of business entirely. Towns and cities lost jobs, plants and infrastructure “rusted” and fell apart as populations moved away. (This trend was observable in other countries, as well, as older industrial towns such as Berglagen, Sweden; Saarland, Germany; Shikoku, Japan; and much of northern England have struggled through a time of changing technology and markets.)

This shorthand for geographic regions in the US has dominated industry discourse for decades, and words have power over perceptions. Rust Belt is a label that communicates loss and hopelessness, and it can color an investor’s perception of risks and opportunities. How many investment strategies and decisions are swayed by words? As residents of this region—we often witness the cognitive dissonance of friends and colleagues that are convinced that we live in the ruins of another industrial age. (We do not.)

Rust Belt was always a colorful overstatement, such that investors in the region came to be positioned as adventurous, charitable, or just plain foolhardy. Nonetheless, the benefits of the region, and the promise of their long-term potential to residents and investors alike, has been (and continues to be) well-documented. For the sake of making better assumptions, it may be time to find another way to describe this region. But what should it be called?

To help find the right descriptor, let’s review what this region is today. After fifty years, it has quietly transformed into something innovative, resilient, and in some cases, rust-free.

To start, it’s important to understand the scale of the Rust Belt—starting with the fact that, if it were counted as a country, it would be home to the third-largest economy in the world, with a GDP of US$6 trillion—just behind the US and China, and greater than Japan, Germany, or the UK.[4]

Additionally, there are 17 million people in the region,[5] as well as nearly a quarter of all US R&D, and eighteen of the top hundred universities in the world.[6]

The region also surrounds the US side of the Great Lakes, where the US annually ships more than 200 million tons of cargo and comprises over half of the US-Canada border trade. This volume represents more than all US trade with France, Germany, South Korea, or the UK.[8]

With the trade, education, and manufacturing capacity stronger than many realize, the region is delivering new technology in a way that few other regions can—including advanced R&D underway across biotech, infotech, nanotech, and polymers. For example, Pittsburgh, Pennsylvania has become a significant global center for robotics and autonomous vehicles. And Akron, Ohio used to be the tire and rubber manufacturing capital of the world. Those production lines closed down a while ago, but now that same infrastructure leads advanced polymer research and manufacturing, with 400 manufacturing and distribution companies.[9]

RESILIENCY IS THE KEY TO REGIONAL RECLAMATION

Beyond innovation, there is one important fact to consider when evaluating the future of the region—perhaps more important every year—based on the region’s proximity to the Great Lakes:

The Great Lakes hold 21% of the world’s surface fresh water and 84% of US surface water.[10]

On this fact alone, and as underscored by the dozens of new “point of no return” climate change reports released every quarter, it seems that the term Rust Belt—if once useful for making a novel observation about post-industrial cities—is no longer adequate or accurate for signaling the livability and investment potential of the region. A 2018 analysis from the Brookings Institution clearly makes the case for how the nation’s “freshwater coast” will be integral to Rust Belt revival.[11] Experts from the Nature Conservancy make a similar case, and even go so far as to suggest that “Blue Belt” might be a more relevant evolution of the regional nomenclature,[12] while IndustryWeek goes one notch up the color spectrum to suggest “Green Belt” for similar reasons.[13]

ALSO IN THIS ISSUE

SOCIAL ISSUES / The Great Real Estate Reset: A data-driven initiative to remake how and what we build.

Brookings | Christopher Coes, Jennifer S. Vey, and Tracy Hadden Loh

SOCIAL ISSUES / Confronting the Myth: The events of the past year have driven businesses to confront racial inequity, but some still shy away from the challenges needed to make real progress.

Alfred Dewitt Ard Consulting | Shumeca Pickett

INDUSTRY OUTLOOK / CRE Prospects Post-COVID-19: How is commercial real estate set to perform in the post-COVID world?

Aegon Asset Management | Martha Peyton

HOSPITALITY / Time to Check In: If history is a guide, the time to invest in hotels is when things look bleak. This appears to be one of those times.

Barings Real Estate | Jim O’Shaughnessy

HOSPITALITY / Hoteling 2.0: The pandemic has impacted the hospitality, but a growing wave of non-traditional investors has shown heightened interest in the evolving industry.

JLL Hotels & Hospitality Group | Gilda Perez-Alvarado

RESIDENTIAL / Safe as Houses?: The future of residential investments is all about demographics—and the forces behind them.

American Realty Advisors | Sabrina Unger

RESIDENTIAL / Housing for Goldilocks : The pandemic highlights the advantages of single-family and appears to have accelerated migration to less dense, more affordable areas.

GTIS | Eliot Heher and Robert Sun

DATA CENTERS / Data Centers, Stage Center: Data center investments have proven resilient in periods of volatility—and they’re only going to become more essential and important into the future.

Principal Real Estate Investors | Bob Wobschall

CLIMATE CHANGE (WHITE PAPER) / Rather Than the Flood: A comprehensive look at climate-induced water disasters and their potential impact on CRE in the US.

New York Life Real Estate Investors | Stewart Rubin and Dakota Firenze

LOGISTICS / Reforging the Supply Chain: The only way to deliver on the service promises of a booming logistics sector requires a complete reimagination of the supply chain.

Stockbridge | David Egan

DEBT AND LEVERAGE / Leveraging Control: Though leverage is an important part of capital funding, it’s important to ask LPs if (and how) they should take control of their real estate leverage.

RCLCO Fund Advisors | William Maher and Ben Maslan

DEVELOPMENT / Recasting Risk and Return: The investment community can have an active role in economic recovery—but it will require recasting the traditional risk/return framework.

Standard REI | Shubrhra Jha

CORPORATE TRANSPARENCY ACT / Transparency Rules: Non-US-based investors face the disclosure regime of the Corporate Transparency Act. What do you need to know?

Pillsbury | Andrew Weiner

PENSIONS (WHITE PAPER) / Rising Pressures: The latest joint, in-depth report from Praedium and SitusAMC looks at rising fiscal pressures on state and local governments.

Praedium Group and SitusAMC Insights | Russell Appel, Peter Muoio, and Cory Loviglio | SitusAMC Insights

TALENT AND HR / Plugging the Skills Gap: Several trends are forcing change in the global commercial real estate industry, driving demand for new skills. How is the industry responding?

Sheffield Haworth | Max Shepherd

ESG / Operationalizing the Sustainability Agenda: During a time of unprecedented disruption, how should businesses approach the “new metrics” ESG of performance?

AccountAbility | Sunil A. Misser

Researchers focused on water innovations for the region, including Rachel Havrelock, director of the Freshwater Lab at the University of Illinois at Chicago, have suggested something more intuitive: Water Belt. Referencing drought, floods, and other massive weather events impacting livelihoods and even lifespans in increasingly large swaths of the US—including the sunny southern states—Havrelock writes, “there is a need to transform our much-maligned Rust Belt into a Water Belt, a freshwater oasis for the world.”[14]

While AFIRE and Summit Journal will increasingly promote terminology along these “post-Rust Belt” lines (see editor’s note), many of the local population refer to theirs as the “Great Lakes Region.” The region has a shared culture and common history of immigrants from around the world, and for decades, linguists have studied the shared dialect of the region (what they call “the Great Lakes shift,” which stretches from New York in the East to Wisconsin in the West). Shared language, shared education, shared industries, and shared lakes.

COMPARING THE BELTS

So, how does the Water Belt measure up to the Sun Belt? By current metrics, it doesn’t.

Local taxes are higher in the Great Lakes. Many governments have underfunded their infrastructure and pension plans to the point where bankruptcy and/or even higher taxes are likely. Overall cost of living is higher in the North, and it’s colder in the winter. Not attractive. But how permanent and how much of a difference is there between the two?

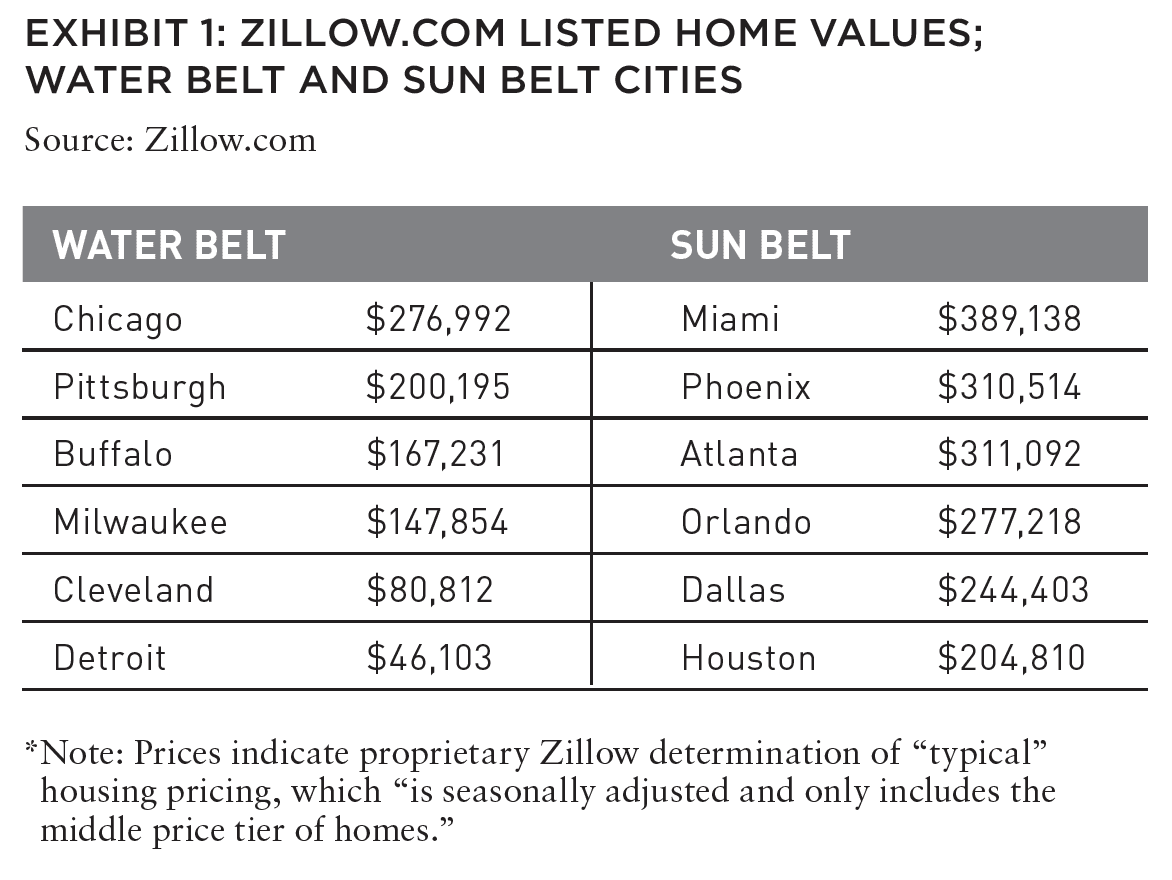

Migrants to the Sun Belt often talk about a lower cost of housing. For some time, that has been the case, but a quick look at Zillow’s listed home values tells a different story: Phoenix, Miami, and Atlanta are all higher than the most expensive Great Lakes city, Chicago, while Dallas and Houston aren’t far behind.

This is, of course, a blunt measurement of the cost of housing, but directionally it points to decreased arbitrage. The fast-growing populations are increasing the demand and cost of housing. But what about taxes? For example, many companies and individuals have relocated to Texas to take advantage of lower taxes. But population growth and climate change could put an end to that, sooner than we think.

With more than twenty years of significant growth in the Sun Belt population, the need for high-quality infrastructure has only increased, while zoning and building practices have made infrastructure such as power, roads, and sewage more expensive. Climate change makes it cost more. In February 2021, Texas was devastated by what was called a “freak winter storm” with temperatures as low as -10C (13F), 69 deaths, and US$18 billion in damages. With infrastructure and buildings designed primarily for temperate to hot weather, the Arctic temperatures were especially devastating. Millions of people were left without heat or drinkable water for days, and even weeks.[15]

Texas will likely need to improve their power grid and require more tax revenues to do so. Of course, the leadership of Texas will make every attempt to keep that increase to a minimum—but no one can get something for nothing.

And that’s not the last “freak storm” that will challenge the Sun Belt. According to the Environmental Defense Fund, “Though it can be hard to pinpoint whether climate change intensified a particular weather event, the trajectory is clear—hotter heat waves, drier droughts, bigger storm surges and greater snowfall.”[16]

CLIMATE CHANGE IS ALREADY HERE, AND MOVING FAST

Climate change has moved from something that might happen in the decades to come, to something that is happening right now: drought, fire, storms and floods.

At the end of 2020, 40% of the US was in a state of drought—most of it in the Southwest and Western regions.[18] During 2020 there were 57,000 wildfires that engulfed more than 10.3 million acres—an increase of 50% compared to 2019.[19] The smoke from these fires could be seen and smelled thousands of miles away, and even hid the sun in some places.

According to the National Oceanic and Atmospheric Administration, the Southeast saw a “[threefold] increase in flooding days” from 2019 to 2000. For example, Charleston, South Carolina, had thirteen days where flooding reached damaging levels in 2019, compared to only two days typical in 2000. And along the western side of the Gulf, in Texas, Sabine Pass and Corpus Christi had 21 and 18 flood days, respectively, in 2019.[20] Miami may not be underwater (yet), but they are experiencing record amounts of “sunny day floods,” or flooding that occurs at high tide. Between 9 and 19 of these floods occurred in the Miami area in 2019.[21]

In 2020, the US experienced a record-breaking hurricane season with thirty named storms, and floods. The last time the US had a record-breaking year was 2005. There are and will be larger storms, more often, and the records continue to be broken.

The more frequent these events, the less of an advantage the Sun Belt has, and the more the Water Belt is positioned for in-migration and growth. How long will the population of the Sun Belt continue to grow, especially in the face of these weather events and other economic pressures? And at what point does the Great Lakes Region, and its former industrial capitals grow again? The answer to these questions can be found in the facts, but depends on assumptions for context.

DOWNLOAD A PDF OF THIS ARTICLE

—

ABOUT THE AUTHORS

Gunnar Branson is the CEO of AFIRE, the association for international real estate investors focused on commercial property in the United States. Benjamin van Loon is the communications director for AFIRE and the Editor-in-Chief of Summit Journal.

—

NOTES

1. William Goldman The Princess Bride (Film) 20th Century Fox, September 25, 1987

2. North America Moving Services 2020 Migration Report avlnavlblob.blob.core.windows.net/northamerican-com/docs/default-source/ default-document-library/key-takeaways—2020-migration-report.pdf?sfvrsn=3b1554ef_0

3. Edward Glaeser and Kristina Tobio, The Rise of the Sunbelt Taubman Center Policy Briefs, May 2007 hks.harvard.edu/sites/default/files/centers/taubman/files/sunbelt.pdf

4. The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/the-greatlakes-economy-the-growth-engine-of-north-america/

5. The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/the-greatlakes- economy-the-growth-engine-of-north-america/

6. “The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/ the-great-lakes-economy-the-growth-engine-of-north-america/

7. The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/the-greatlakes- economy-the-growth-engine-of-north-america/

8. The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/the-greatlakes- economy-the-growth-engine-of-north-america/

9. akronlegalnews.com/editorial/7004

10. The Great Lakes Economy: The Growth Engine of North America Council of the Great Lakes Region (Web site) councilgreatlakesregion.org/the-great-lakes-economy-the-growth-engineof- north-america/

11. brookings.edu/blog/the-avenue/2018/05/31/the-nations-freshwater-coastis- a-key-fulcrum-for-rust-belt-revival/

12. rochesterbeacon.com/2019/06/27/its-not-the-rust-belt-its-the-blue-belt/

13. industryweek.com/operations/energy-management/article/21964224/ohioisnt-the-rust-belt-its-the-green-belt

14. chicagotribune.com/opinion/commentary/ct-perspec-water-great-lakesrust- belt-economy-0209-20180208-story.html

15. Alex Meier, 69 deaths, 44 hours of freezing, $18 Billion in damage: This week’s winter storm, by the numbers, ABC13 Eyewitness News February 21, 2021 abc13.com/2021-texas-winter-storm-weather-how-many-peoplelost- power-boil-water-advisory/10356914/

16. Environmental Defense Fund (EDF) Extreme weather gets a boost from climate change edf.org/climate/climate-change-and-extreme-weather

17. Christopher Coes, Tracy Hadden Loh, and Tola Myczkowska The Great Real Estate Reset, Brookings Institute December 16, 2020 brookings.edu/essay/distorted-and-destabilized-housing-markets-are-pushinghouseholds- into-climate-risky-low-opportunity-communities/

18. US Drought Monitor Update, National Centers for Environmental Information, December 1, 2020 ncei.noaa.gov/news/us-drought-monitorupdate- december-1-2020

19. Facts + Statistics: Wildfires Insurance Information Institute December 2020 iii.org/fact-statistic/facts-statistics-wildfires

20. US high-tide flooding continues to increase, National Oceanic and Atmospheric Administration (NOAA) July 14, 2020 noaa.gov/mediarelease/ us-high-tide-flooding-continues-to-increase

21. Alex Harris, Miami broke an all-time record for high tide floods in 2019, NOAA says Miami Herald July 14, 2020 miamiherald.com/news/local/ environment/article244217807.html