With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

Sustainability has become a mainstream issue within the commercial real estate sector and will become even more fundamental in the process of delivering office space as it moves up the occupier agenda. Globally, what are the trends in valuing net-zero and ESG strategies for the office sector?

With more tenants focusing on environmental targets, the burden to reduce direct emissions will intensify, placing increased pressure on real estate investors, who are now at a pivotal moment in defining their sustainable investment strategies.

The International Energy Agency’s 2019 World Energy Statistics and Balances report shows that the built environment contributes 40% of carbon emissions worldwide. Evolving development legislation urging better sustainability and building practices for new and existing assets coupled with the rapid expansion of ESG criteria for commercial real estate investment will likely significantly impact the value of assets moving forward.

By 2030, many global corporations and ambitious governments aim to achieve their net-zero position. As for the commercial real estate sector, the vision is for all buildings (both new and existing) to be net-zero by 2050.

Investors will need to understand if a building can achieve a net-zero status, how to balance their portfolio, what the costs are to achieve this ambitious goal, and what impact it will have on their valuations. As occupational trends evolve and the future of work transforms, investors will also need to understand if their buildings are able to adapt to meet market demand.

According to a recent JLL survey of investors, sustainability and climate change are deemed to have the greatest impact on real estate performance, with two thirds stating that they would be increasing their allocations to more sustainable properties.1

HOW TO VALUE SUSTAINABLE STRATEGIES

Valuers adopting Discounted Cash Flow (DCF) methodology can adapt assumptions that relate to income, exit yields, capital expenditures, voids, financing, and discount rates for all building types. Cash flows, which reflect the net income over the hold period, can illustrate how investment in sustainable buildings makes sense both ethically and financially.

INCOME

Rental income will be influenced by a limited supply of appropriately specified buildings and increased demand from tenants with ESG requirements. JLL research indicates that there is already an impact on several office markets, where the most sustainable specifications are resulting in premium rents, or discounts to prime rents are occurring where sustainability credentials are not in line with market expectations. The most significant risks to value exist where older buildings will soon not match up to changing occupier or legislative requirements, resulting in increased obsolescence. Therefore, when using forecasts that principally follow prime rents, there will be under-performing buildings, which will not track forecasted rental growth.

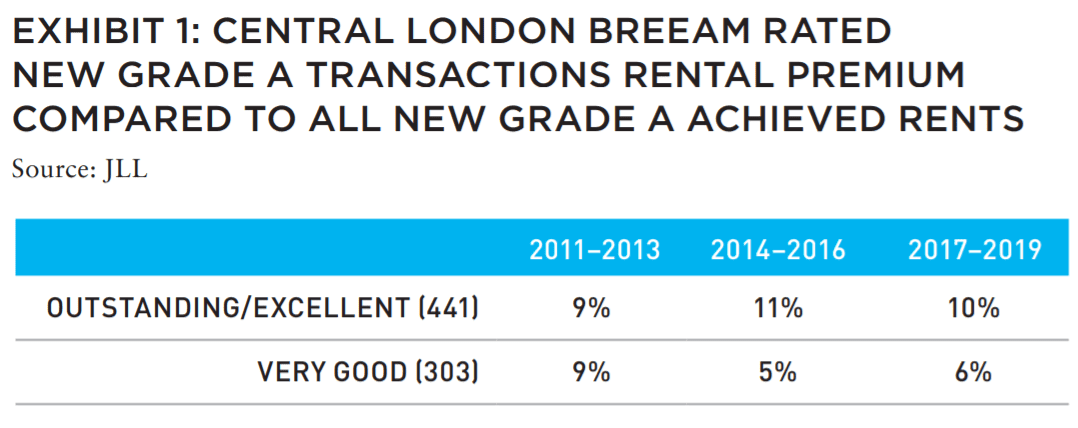

Based on JLL’s research in Central London,2 there is already a rental premium for BREEAM, a world-renowned sustainability rating scheme to assist the real estate industry to deliver sustainable buildings where the Outstanding- or Excellent-rated buildings tend to perform better than non-rated buildings. In fact, generally all buildings with a BREEAM rating of Very Good or higher achieve higher rents than those Grade-A buildings without a rating. The research shows that over the past three years, the average premium of all rated buildings above non-rated buildings is around eight percent. Similar rental premiums are also coming through internationally from the US and India (for LEED certified buildings) and Australia (for highly rated NABERS and Green Star buildings).

It is worth noting that BREEAM and other green ratings are not the sole factor for low vacancy or increased rents. Tenants consider a wide range of factors when seeking new office space, including location, access to transportation, amenities, costs, and floorplates.

CAPITAL EXPENDITURE

When considering refurbishing or retrofitting older buildings, it may be financially advantageous and carbon efficient to upgrade existing buildings, both in terms of specification and plant and machinery, to create a more efficient building.

Investors also need to consider the potential risk of future taxation penalizing excessive carbon emissions or operational inefficiency within a building. In terms of cash flow, the question is whether to commit additional costs at the start of a retrofit project, or to take advantage of the short-term dearth of supply, or lower upfront costs with the anticipation of further significant refurbishments costs within the next ten years, to stay in line with legislation and market demand.

Estimates for additional capital expenditure vary and are dependent upon building type, design, and efficiency. Delivering a more sustainable building will, in most cases, cost more to build than a less sustainable office. However, if this results in higher demand from occupiers, higher rents, lower void rates, and savings in operational expenditures, then the enhanced sustainability of the building should mitigate the initial higher capital investment.

While variations in costs over time and the pace of legislative change are somewhat unknown, delaying action will mean losing out on the short-term supply-and-demand dynamics of the current market.

VOIDS

At the end of leases, tenants either renew or the space is remarketed. According to JLL research, well-specified spaces fitted out to meet both sustainable and wellness criteria lease up quicker than standard offices.

FINANCE

Geared returns can enhance performance through using debt to either acquire or fund the retrofit of a building. An increasing number of green loans are also being made available, which results in lower finance costs where sustainability-related key performance indicators (KPIs) are achieved, resulting in a lower cost of debt and enhanced returns.

DISCOUNT RATE

The discount rate applied to the cash flow reflects the risks associated with the achievement of a business plan in relation to the building over the hold period. Less sustainable buildings will inherently have a higher discount rate, as well as potential increased capital expenditure over time, taxation, longer voids, lower rents, and higher exit yields.

The associated risks will result in a higher pricing discount. By contrast, more sustainable buildings will prove less risky and bring lower discount rates.

EXIT YIELD

The exit yield adopted in a DCF reflects the quality of the building and the estimated average weighted unexpired term remaining on the lease at the time of the exit, which relates to a hold period normally reflected in the business plan or a standard assumption of either five or ten years. It also reflects the market’s assessment of the long-term net income growth.

If a building does not track the leading market standards, then the exit yield will be higher, resulting in a lower value at the end of the hold period.

LOOKING FORWARD

As more tenants commit to environmental targets, the pressure to engage with the supply chain and reduce direct emissions will intensify, leading to increased pressure on real estate owners. This urgency to build what tenants are increasingly demanding will only accelerate.

Investor- and tenant-driven ESG requirements are expected to increase in all types of buildings, both new and refurbished. Supply and demand imbalances will potentially result in green premiums in the short-term for well-specified buildings, or brown discounts due to increased obsolescence. These fluctuations in supply, demand, cost, and legislation will occur over the next one to two hold periods for investors.

To achieve the best sustainability credentials and net-zero carbon specifications, costs are generally higher than for a standard refurbishment. However, given the speed at which legislation and ESG requirements are advancing, it is projected that within the next ten years, further capital expenditure will be required if net-zero compliance decisions are not made now.

Despite the increase in capital expenditure, the associated rental premiums, reduction in yield, and lower interest expenses should result in a more positive cash flow and an overall increase in returns for greener buildings.

As technology and construction techniques evolve, and as more sustainable buildings become less expensive to deliver, there may be a reduction in capital costs as new construction methods are adopted. Conversely, it is also likely that the costs of maintaining a less sustainable building will rise as fossil fuel prices increase, carbon taxes are introduced, and fines are levied for those not keeping up with legislative requirements.

Further, costs may be mitigated through the principle of the circular economy, with much more focus on recycling materials. Demolition costs may be significantly reduced as materials are resold for further use. In addition, building design will result in more flexible buildings so that these assets can be refurbished more economically and adapted to alternative uses.

THE CIRCULAR ECONOMY

“Put simply, the circular economy is an economy where we create more value with fewer resources. A circular economy is based on three principles, as stated by Ellen MacArthur Foundation, the global leader in circular thinking:

• Design out waste and pollution

• Keep products and materials in use

• Regenerate natural systems

As opposed to a linear economy where we extract materials, use them, then dump them, the circular economy seeks to “close the loop” by reusing, repurposing, remanufacturing, or recycling materials.

For instance, it might mean designing a building so it can be easily adapted to different uses, constructing a building in a way that it can be dismantled without damaging the materials, or fitting out a property using repurposed or recycled furniture. It also means maximising the current value of assets by using them to their full capacity, for example, by using empty office space for events outside of business hours.”

Emerging trends indicate that there may also be short-term premiums for net-zero buildings. While the low-carbon premium in rents and capital values may dissipate over time, buildings that have not had meaningful upgrades towards net-zero carbon will experience increased obsolescence.

As sustainability performance becomes clearer and more defined, it is likely that premiums will disappear. Buildings that don’t comply will underperform. Buildings that are not designed to be net-zero carbon will require costly retrofits in the future, which will likely result in the displacement of tenants and lost rent.

—

ABOUT THE AUTHOR

Lori Mabardi is Senior Director, Research, ESG for JLL. Emily Chadwick is Lead Risk Advisor, ESG for JLL Valuation Advisory EMEA. Eric Enloe is Head of Commercial Valuation of JLL Valuation and Advisory Services, US.

—

NOTES

1.JLL, “Decarbonizing the Built Environment,” June 20, 2021, us.jll.com/en/trends-and-insights/research/decarbonizing-the-built-environment.

2.JLL, “The Impact of Sustainability on Value,” May 28, 2020, us.jll.com/en/trends-and-insights/research/decarbonizing-the-built-environment.

ALSO IN THIS ISSUE (FALL 2021)

NOTE FROM THE EDITOR / GROUPTHINK VS. GROUP COLLABORATION

AFIRE | Benjamin van Loon

MID-YEAR SURVEY / CHECKING THE PULSE

No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

AFIRE | Gunnar Branson and Benjamin van Loon

CLIMATE CHANGE / REASSESSING CLIMATE RISK

The commercial real estate industry may not yet fully grasp the actual relationship between climate risk and asset pricing and value. But the knowledge is coming fast.

York University | Jim Clayton

University of Reading | Steven Devaney and Jorn Van de Wetering

Kinston University | Sarah Sayce

UNEP FI | Matthew Ulterino

NON-TRADITIONAL / THE ALLURE OF SPECIALTY SECTORS

Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

Invesco Real Estate | David Wertheim

NON-TRADITIONAL / NON-TRADITIONAL IS GOING MAINSTREAM

The mainstreaming of nontraditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

Principal Real Estate Investors | Indraneel Karlekar, PhD

DIGITAL INFRASTRUCTURE / DIVERSIFYING INTO DIGITAL

As investors look for sustainable sources of inflation-protected yield, real estate investment is increasingly blurring into a wider range of “digital” real asset investment strategies.

AECOM Capital | Warren Wachsberger, Josh Katzin, and Corbett Kruse

LIFE SCIENCES / TAPPING INTO BIOTECH

Over the past two decades, the single-family rental industry haLife sciences real estate has been a “hot” property type for the past decade—and even more since the pandemic. Will all the capital targeting the space be placed where it needs to go?

RCLCO | William Maher, Ben Maslan, and Cecilia Galliani

ESG + CLIMATE CHANGE / HIGH-WATER MARKS

Interest and excellence in ESG performance is becoming increasingly critical to portfolio strategy. So with sea levels on the rise, how can portfolios stay above water?

Barings Real Estate | Jerry Speltz

ESG + NET-ZERO / VALUING NET-ZERO

With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

JLL | Lori Mabardi, Emily Chadwick, and Eric Enloe

ESG + FAMILY OFFICE / FAMILY OFFICES AND ESG

As sustainable investing continues to grow in popularity, family offices have taken note—and understanding ESG targets and regulations will be key for longterm performance.

Squire Patton Boggs | Kate Pennartz and Rebekah Singh

DEBT / WHY DEBT, WHY NOW?

Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

USAA Real Estate | Karen Martinus, Mark Fitzgerald, CFA, and Will McIntosh, PhD

MIGRATION / MIGRATION IN REAL TIME

As the public health situation started to improve in early 2021 and the economy reopened, did migration flows change too—and what if we are able to answer this in real time?

Berkshire Residential Investments | Gleb Nechayev

StratoDem Analytics | Michael Clawar

URBANISM / DOWNTOWN DISRUPTION

The pandemic-driven changes to downtown areas and central business districts is changing the geography of institutional investment. What else changes because of this?

Drexel University | Bruce Katz

FBT Project Finance Advisors + Right2Win Cities | Frances Kern Mennone

WORK-FROM-HOME / CHOOSING FLEXIBILITY

Employees are increasingly demanding flexibility and choice for where (and when) they work. What strategies can landlords implement to adapt?

Union Investment Real Estate | Tal Peri

TALENT AND RECRUITMENT / TALENT PARITY

To be better prepared for future risks, firms need diverse talent. So is the goal of 50% female representation achievable in global real estate investment and asset management firms?

Sheffield Haworth | Isabel Ruiz

CLIMATE CHANGE / PREDICTING THE CLIMATE FUTURE

We are all invested in the cities, assets, and infrastructure of tomorrow, even if we might not live to see the ten largest cities in 2100. But understanding climate change can get us closer.

Climate Core Capital | Rajeev Ranade and Owen Woolcock