Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

The share of debt funds in total capital raised globally by real estate investors has risen steadily, growing from 7% in 2016 to about 12% in 2020.1 Funds investing in North America continue to lead the pack in the real estate debt world. Capital raised for debt funds shows the depth of the market in the US as compared with Europe. For non-US-based investors looking for exposure to commercial real estate (CRE) debt, the US market offers numerous attractions.

Broadly, the COVID-19 pandemic created an economic setback that led traditional sources of debt capital to retrench during the early stages of the pandemic, and while most have returned to nearly normal activity, there remain constraints on proceeds, as compared to pre-COVID.

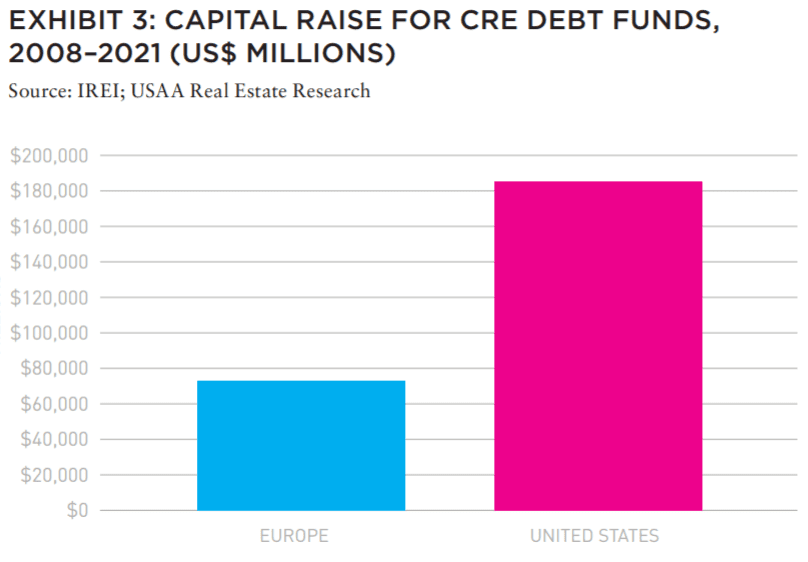

CRE debt markets are also at different levels of maturity. Since 2008 the US has raised about 2.5 times more capital for debt funds compared to Europe.2 As such, CRE debt presents an attractive proposition, at a time when returns from fixed income investments have been pushed to all-time lows. In the current low interest rate environment, the CRE lending sector should remain attractive on a relative basis given the decline in bond yields.

FUNDING GAP

CRE debt has long been considered attractive for its ability to combine stable income returns with a level of downside protection from real asset exposure. However, the lure has intensified as regulatory requirements have constrained traditional capital sources, creating opportunities for non-traditional lenders to fill the resulting gap.

• Recent economic uncertainty has exacerbated the capital gap that resulted from regulation during the last expansion, creating further opportunity for non-traditional lenders.

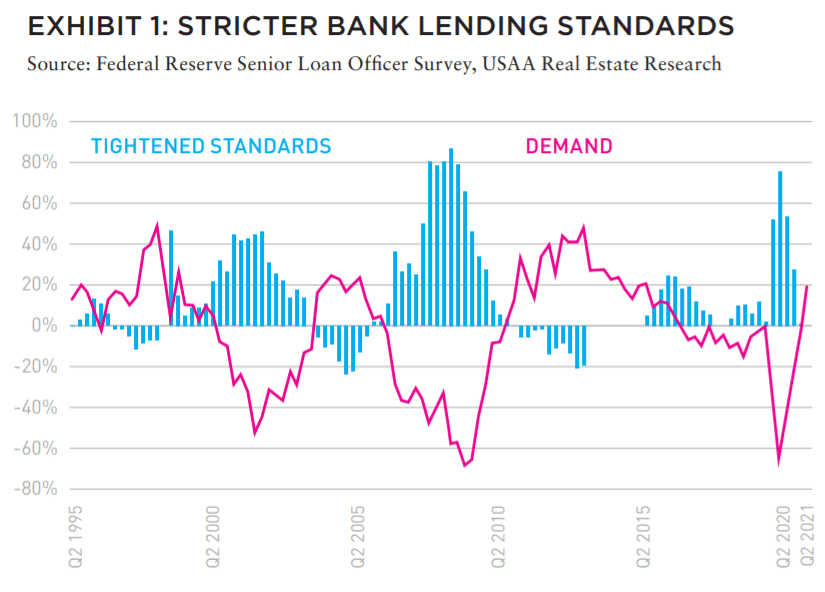

• Lending standards tightened dramatically in 2020 as banks responded to the uncertain economic outlook. As demonstrated by the Federal Reserve Senior Loan Officer Survey (Exhibit 1), the percentage of banks tightening lending standards reached levels not seen since the GFC. Lending standards have started to loosen in recent quarters but remain constrained.3

• Reduced appetite amongst traditional lenders for certain types of real estate lending—particularly transitional properties or assets which are typically higher risk—creates further opportunity for alternative lenders to respond to unmet demand.

• Nontraditional capital providers are well positioned to take advantage of this funding gap by originating and acquiring loans to produce attractive risk-adjusted returns, while potentially taking materially less risk due to having seniority in the capital stack in relation to the equity position.

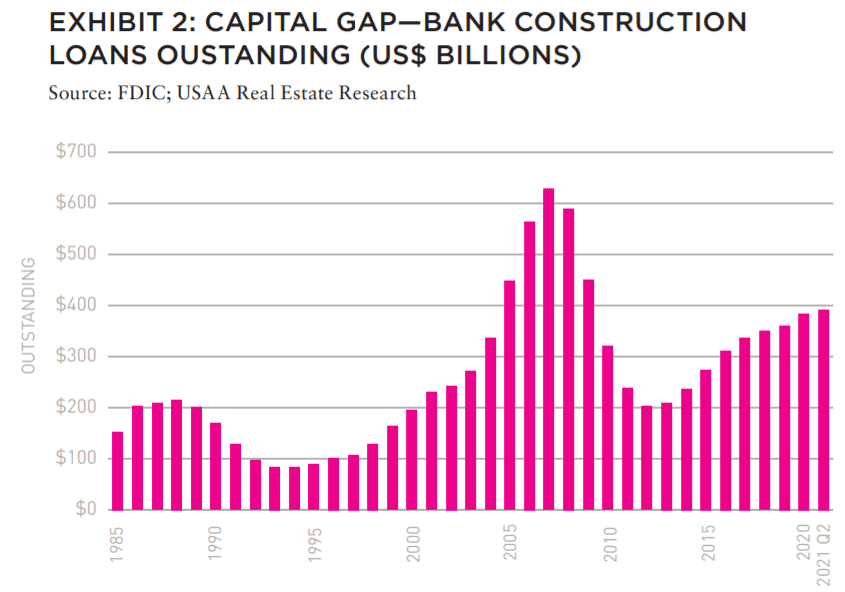

• Banks are the primary source of construction loan capital in the US, though bank construction loans outstanding remain 39% below pre-GFC levels, even though development activity is above 2007 levels (Exhibit 2).

• This demonstrates that for construction deals, the market is seeing a mix of more equity capital required and nontraditional lenders increasingly being relied upon to meet the borrowing needs of developers.

US CRE DEBT IS A SIZEABLE MARKET

These market dynamics suggest an attractive investment environment for private debt. According to the 2021 ANREV/ INREV/NCREIF Capital Raising Survey, non-listed debt products were the only type of vehicle for which the number that raised capital increased from 48 in 2019 to 76 in 2020, growing their share in the total number of vehicles from 5% to 11%.4

US CRE debt makes up a large market, with over US$5.0 trillion in US mortgage debt outstanding as of Q2 2021, via traditional sources.5 The size of the market offers institutional investors depth, liquidity as well as potentially strong risk-adjusted returns. Capital raised for debt funds shows the depth of the market in the US, especially as compared with Europe. Since 2008, the US has raised about 2.5 times more capital for debt funds as compared to Europe (Exhibit 3).

However, appetite for CRE debt vehicles amongst European-domiciled investors is growing. European investors account for 51% of the global capital raised for nonlisted debt vehicles in 2020. This is a notable change compared to 2019 when European-domiciled investors accounted for only 13% of the capital raised for non-listed debt products.6

The CRE debt market in Europe continues to lag the strong growth in investor appetite. Outside the US, real estate finance continues to primarily be a bank-led market, although European non-bank lending activity has grown in recent years. Real estate debt funds remain comparatively new in Europe as the market is evolving, but vehicles have been gaining in momentum.

STRONG RELATIVE PERFORMANCE

Institutional investors have increased their appetites for CRE debt funds in recent years. The reasons for this are familiar; the hunt for yield and diversification arguments are well-known—though low volatility and strong relative performance have also played key roles. Expectations of traditional fixed income securities have been driven extremely low. Demand for yield has become more pronounced and the relative risk-reward profile of CRE debt has become even more compelling.

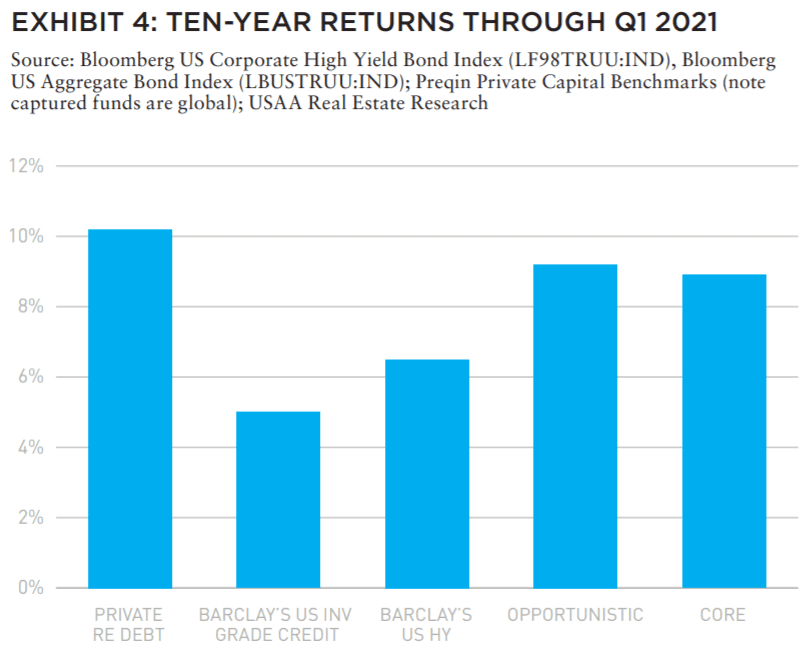

• CRE debt funds have outperformed investment-grade corporate bonds by 540 BPS annually, on average, over the past ten years, and outperformed high-yield corporate bonds by 370 BPS (Exhibit 4).7

• CRE debt fund total returns have also compared favorably to other real assets. Private equity real estate returns, as captured by Preqin. Have delivered returns of 9.3% and 8.9% for opportunistic and core strategies, compared to 10.4% for CRE debt funds over a ten-year period.8

• Looking at the available returns data for CRE debt funds across geographies, the relative outperformance of the US compared to Europe is also clear. Most vintages where we have data suggest North American debt funds have outperformed Europe across seven out of nine vintages.

BEYOND THE CURRENT ENVIRONMENT

In the current environment, investors have become very selective, choosing certain asset classes over others and focusing on quality assets in terms of location, tenant covenants, and ESG criteria. US CRE debt has been increasingly sought after by pension funds and other institutional investors, and the arguments for including real estate in private-debt allocations appear to be strong.

Currently, there is an opportunity for institutional investors to fi ll the funding gap and capitalize on the robust demand in the commercial lending sector while providing investors with strong risk-adjusted returns. CRE debt strategies are attractive because they rival core equity strategies from a total return perspective and provide substantially more return than traditional fixed income in the current environment, while potentially taking materially less risk due to seniority in the capital stack in relation to the equity position.

As with most investment opportunities, real estate lending has a certain level of embedded risk. Even with such a strong CRE debt outlook, it is important to ensure sponsor alignment. It is critical to invest with a qualified and experienced investment manager that can navigate the risks and challenges within this sector.

ALSO IN THIS ISSUE (FALL 2021)

NOTE FROM THE EDITOR / GROUPTHINK VS. GROUP COLLABORATION

AFIRE | Benjamin van Loon

MID-YEAR SURVEY / CHECKING THE PULSE

No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

AFIRE | Gunnar Branson and Benjamin van Loon

CLIMATE CHANGE / REASSESSING CLIMATE RISK

The commercial real estate industry may not yet fully grasp the actual relationship between climate risk and asset pricing and value. But the knowledge is coming fast.

York University | Jim Clayton

University of Reading | Steven Devaney and Jorn Van de Wetering

Kinston University | Sarah Sayce

UNEP FI | Matthew Ulterino

NON-TRADITIONAL / THE ALLURE OF SPECIALTY SECTORS

Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

Invesco Real Estate | David Wertheim

NON-TRADITIONAL / NON-TRADITIONAL IS GOING MAINSTREAM

The mainstreaming of nontraditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

Principal Real Estate Investors | Indraneel Karlekar, PhD

DIGITAL INFRASTRUCTURE / DIVERSIFYING INTO DIGITAL

As investors look for sustainable sources of inflation-protected yield, real estate investment is increasingly blurring into a wider range of “digital” real asset investment strategies.

AECOM Capital | Warren Wachsberger, Josh Katzin, and Corbett Kruse

LIFE SCIENCES / TAPPING INTO BIOTECH

Over the past two decades, the single-family rental industry haLife sciences real estate has been a “hot” property type for the past decade—and even more since the pandemic. Will all the capital targeting the space be placed where it needs to go?

RCLCO | William Maher, Ben Maslan, and Cecilia Galliani

ESG + CLIMATE CHANGE / HIGH-WATER MARKS

Interest and excellence in ESG performance is becoming increasingly critical to portfolio strategy. So with sea levels on the rise, how can portfolios stay above water?

Barings Real Estate | Jerry Speltz

ESG + NET-ZERO / VALUING NET-ZERO

With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

JLL | Lori Mabardi, Emily Chadwick, and Eric Enloe

ESG + FAMILY OFFICE / FAMILY OFFICES AND ESG

As sustainable investing continues to grow in popularity, family offices have taken note—and understanding ESG targets and regulations will be key for longterm performance.

Squire Patton Boggs | Kate Pennartz and Rebekah Singh

DEBT / WHY DEBT, WHY NOW?

Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

USAA Real Estate | Karen Martinus, Mark Fitzgerald, CFA, and Will McIntosh, PhD

MIGRATION / MIGRATION IN REAL TIME

As the public health situation started to improve in early 2021 and the economy reopened, did migration flows change too—and what if we are able to answer this in real time?

Berkshire Residential Investments | Gleb Nechayev

StratoDem Analytics | Michael Clawar

URBANISM / DOWNTOWN DISRUPTION

The pandemic-driven changes to downtown areas and central business districts is changing the geography of institutional investment. What else changes because of this?

Drexel University | Bruce Katz

FBT Project Finance Advisors + Right2Win Cities | Frances Kern Mennone

WORK-FROM-HOME / CHOOSING FLEXIBILITY

Employees are increasingly demanding flexibility and choice for where (and when) they work. What strategies can landlords implement to adapt?

Union Investment Real Estate | Tal Peri

TALENT AND RECRUITMENT / TALENT PARITY

To be better prepared for future risks, firms need diverse talent. So is the goal of 50% female representation achievable in global real estate investment and asset management firms?

Sheffield Haworth | Isabel Ruiz

CLIMATE CHANGE / PREDICTING THE CLIMATE FUTURE

We are all invested in the cities, assets, and infrastructure of tomorrow, even if we might not live to see the ten largest cities in 2100. But understanding climate change can get us closer.

Climate Core Capital | Rajeev Ranade and Owen Woolcock

—

ABOUT THE AUTHORS

Karen Martinus is Senior Research Associate; Mark Fitzgerald, CFA, CAIA, is Executive Director of Research; and Will McIntosh, PhD, CRE, is Global Head of Research for USAA Real Estate.

—

NOTES

This article represents the opinions and recommendations of the authors and are subject to change without notice. Past performance is no guarantee of future results.

1 Asian Association for Investors in Non-Listed Real Estate Vehicles, European Association for Investors in Non-Listed Real Estate Vehicles, and National Council of Real Estate Investment Fiduciaries, Capital Raising Survey 2021, INREV, April 13, 2021, inrev.org/research/capital-raising-survey.

2 IREI (website), Institutional Real Estate, Inc., irei.com/.

3 “Senior Loan Offi cer Opinion Survey on Bank Lending Practices,” Federal Reserve, Accessed October 25, 2021, federalreserve.gov/data/sloos/sloos202004.htm.

4 ANREV, INREV, and NCREIF, Capital Raising Survey 2021.

5 “Financial Accounts of the United States,” Federal Reserve, September 23, 2021, federalreserve.gov/releases/z1/.

6 ANREV, INREV, and NCREIF, Capital Raising Survey 2021.

7 Preqin, Private Capital Performance Data Guide, Preqin, Accessed October 25, 2021, docs.preqin.com/pro/Private-Capital-Performance-Guide.pdf; Bloomberg and Barclays Indices, US Corporate High Yield Bond Index, Accessed October 25, 2021, assets.bwbx.io/documents/users/iqjWHBFdfxIU/rSbjXhPAtPbI/v0; Bloomberg and Barclays Indices, US Aggregate Bond Index, Bloomberg, September 30, 2021, ssga.com/library-content/products/factsheets/etfs/emea/factsheetemea-en_gb-sybu-gy.pdf.

8 Preqin, Private Capital Performance Data Guide.