Delivering on the service promises of the on-demand economy requires the kind of reimagined supply chain that will support industrial real estate growth for years to come.

In the aftermath of iconic toy retailer Toys “R” Us’ 2017 bankruptcy filing, the toy suppliers that had previously distributed heavily through the now-shuttered retailer were faced with new distribution complexities. Previously, these suppliers relied on a relatively small footprint of stocked warehouse buildings to replenish merchandise that would ultimately populate Toys “R” Us shelves in fairly predictable volumes. Now they would have to rely on new distribution channels to fill the Toys “R” Us void, largely turning to Amazon and other “e-tailers” that depended on fast, on-demand service in just about every location with virtually unlimited choices (including the choice to return orders with few exceptions). The net effect required a reimagination of the toy companies’ supply chains. Inevitably, they would need to ensure merchandise was stocked amply in more warehouse locations, closer to end consumers and often strategically positioned near the distributors’ own supply chain networks.

As the COVID-19 pandemic continues to support major e-commerce growth acceleration, this type of restructuring is now reverberating to just about any business that relies on the supply chain to operate: retail, logistics, manufacturing, trucking and transportation, grocery, and on and on. The only way to deliver on ambitious service promises of the on-demand economy is through a complete reconfiguration of the supply chain, much like the foundation of the industrial boom of the past decade. As we see it, the net effect will be not only major ongoing demand for industrial real estate, but also far more breadth of demand across industrial property types and locations.

Among the wide-ranging supply chain changes are three notable trends impacting real estate demand:

• The growing importance of industrial real estate proximity to the end consumer

• The changing point of production and increase of inventories in the system

• The pressures of growing returns and need for better reverse logistics

CERTAIN SMALLER MARKETS BECOME JUST AS STRATEGIC AS LARGE

The revenues of online retailers are highly dependent on their ability to deliver, far more so than their ability to sell. Nearly all US consumers have the ability to shop online, but if an item cannot be delivered quickly, a consumer is more likely to buy from a competitor or a physical store. As service requirements have dropped from weeks to days, the need to position inventory in a much wider set of markets proximate to end consumers has also increased. This has had a measurable impact on leasing activity in secondary markets.

All markets feature population clusters that need to be serviced, but the focus throughout this cycle has been disproportionately aimed at the largest markets. More recently, logistics users of all types have broadened their focus to a network design that aggressively expands into a wider configuration of strategic markets with the goal of reaching as many consumers in as short a period as possible.

Typically, these markets such as Pittsburgh, Detroit, and others have been designated as secondary or even tertiary and have been viewed by investors as somewhat risky. However, many of these markets have characteristics that make them important in the modern supply chain dynamics:

• Large industrial labor pools at relatively low cost

• Access to key transportation infrastructure

• Populations of more than 1 million people

• Growth in key demographics; young and affluent populations

Over the past decade, industrial space demand in these markets has outpaced completions by more than 35 million SF/3.25 million SM and rents have increased by 40%, according to CoStar. Due the steady leasing that has persistently outpaced construction in these markets, vacancy rates have declined to about 5%, which slightly outpaces the overall industrial national average.

These strategic industrial markets are also offering investors compelling opportunities, as the ten-year US economic expansion has lowered yields and reduced available supply and land sites for new development in primary industrial hubs.

DEMAND BROADENS ACROSS SMALLER AND DENSER BUILDING FOOTPRINTS

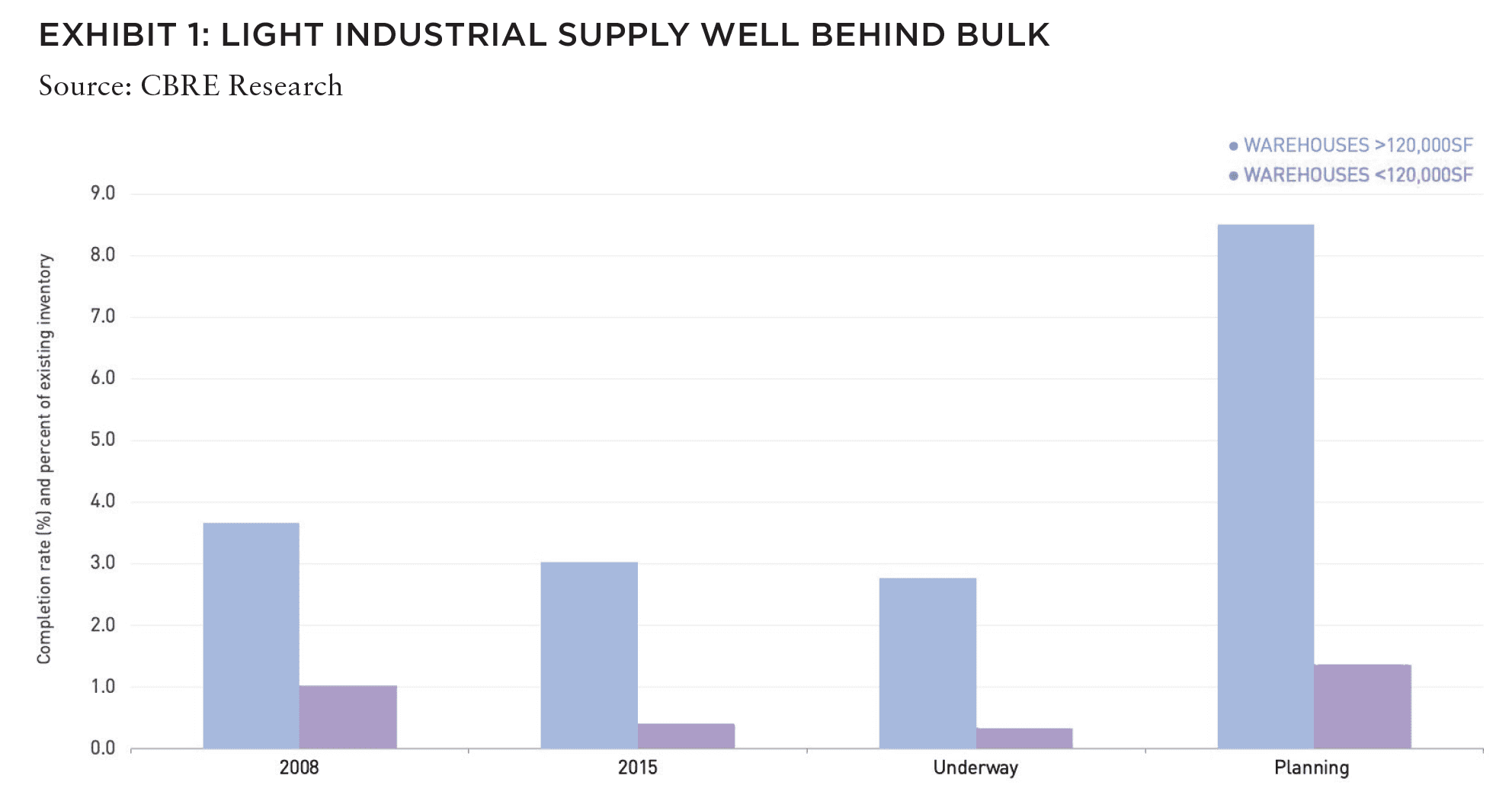

According to CoStar, light-industrial properties account for 9 billion SF/836 million SM—or roughly half of the total US industrial stock. The vacancy rate for this segment has declined by 50% over the past decade to its present rate of 4.5%. Consequently, their rents have climbed at the same rate to an average of US$8.24 per SF..

Despite the strong demand fundamentals, new development in this segment has been extremely limited, with completions accounting for just 1% of total light-industrial warehouse inventory since 1990.[1] This dearth is attributable to challenges in developing smaller parcels in densely populated areas, including competition with other uses and high land values.

Apart from demand for light industrial, demand for proximity to population-dense locations has supported a new wave of industrial building types and functions—from multistory warehouses to robotics solutions for order fulfillment— all of which are likely to see increased investment should they continue proving their ability to increase throughput and efficiencies.

ALSO IN SUMMIT (SPRING 2021)

GREAT LAKES / Tightening the Belts: How are shorthand labels like the “Sun Belt” and the “Rust Belt” shaping investment decisions? Should they?

AFIRE | Gunnar Branson and Benjamin van Loon

SOCIAL ISSUES / The Great Real Estate Reset: A data-driven initiative to remake how and what we build.

Brookings | Christopher Coes, Jennifer S. Vey, and Tracy Hadden Loh

SOCIAL ISSUES / Confronting the Myth: The events of the past year have driven businesses to confront racial inequity, but some still shy away from the challenges needed to make real progress.

Alfred Dewitt Ard Consulting | Shumeca Pickett

INDUSTRY OUTLOOK / CRE Prospects Post-COVID-19: How is commercial real estate set to perform in the post-COVID world?

Aegon Asset Management | Martha Peyton

HOSPITALITY / Time to Check In: If history is a guide, the time to invest in hotels is when things look bleak. This appears to be one of those times.

Barings Real Estate | Jim O’Shaughnessy

HOSPITALITY / Hoteling 2.0: The pandemic has impacted the hospitality, but a growing wave of non-traditional investors has shown heightened interest in the evolving industry.

JLL Hotels & Hospitality Group | Gilda Perez-Alvarado

RESIDENTIAL / Safe as Houses?: The future of residential investments is all about demographics—and the forces behind them.

American Realty Advisors | Sabrina Unger

RESIDENTIAL / Housing for Goldilocks : The pandemic highlights the advantages of single-family and appears to have accelerated migration to less dense, more affordable areas.

GTIS | Eliot Heher and Robert Sun

DATA CENTERS / Data Centers, Stage Center: Data center investments have proven resilient in periods of volatility—and they’re only going to become more essential and important into the future.

Principal Real Estate Investors | Bob Wobschall

CLIMATE CHANGE (WHITE PAPER) / Rather Than the Flood: A comprehensive look at climate-induced water disasters and their potential impact on CRE in the US.

New York Life Real Estate Investors | Stewart Rubin and Dakota Firenze

LOGISTICS / Reforging the Supply Chain: The only way to deliver on the service promises of a booming logistics sector requires a complete reimagination of the supply chain.

Stockbridge | David Egan

DEBT AND LEVERAGE / Leveraging Control: Though leverage is an important part of capital funding, it’s important to ask LPs if (and how) they should take control of their real estate leverage.

RCLCO Fund Advisors | William Maher and Ben Maslan

DEVELOPMENT / Recasting Risk and Return: The investment community can have an active role in economic recovery—but it will require recasting the traditional risk/return framework.

Standard REI | Shubrhra Jha

CORPORATE TRANSPARENCY ACT / Transparency Rules: Non-US-based investors face the disclosure regime of the Corporate Transparency Act. What do you need to know?

Pillsbury | Andrew Weiner

PENSIONS (WHITE PAPER) / Rising Pressures: The latest joint, in-depth report from Praedium and SitusAMC looks at rising fiscal pressures on state and local governments.

Praedium Group and SitusAMC Insights | Russell Appel, Peter Muoio, and Cory Loviglio | SitusAMC Insights

TALENT AND HR / Plugging the Skills Gap: Several trends are forcing change in the global commercial real estate industry, driving demand for new skills. How is the industry responding?

Sheffield Haworth | Max Shepherd

ESG / Operationalizing the Sustainability Agenda: During a time of unprecedented disruption, how should businesses approach the “new metrics” ESG of performance?

AccountAbility | Sunil A. Misser

RISING INVENTORIES INCREASE SPACE DEMANDS

One of the less reported impacts of the pandemic has been the need for businesses around the world to quickly assess and adjust the amount and source of inventory in their systems. The crisis has underscored the fragility of just-in-time (JIT) production networks, which historically have involved very intricate global supply chains in which goods often go back and forth across international borders many times using many different transportation modes.

These JIT systems were stressed to the breaking point in the early days of the pandemic, which led to disruptions ranging from household staples to critical medical supplies. A 2020 survey by the Institute for Supply Management found that nearly 75% of business respondents have experienced supply chain disruptions and more than 80% believe they will in the future.[2] As a result, many businesses are planning major restructuring of their supply chain processes.

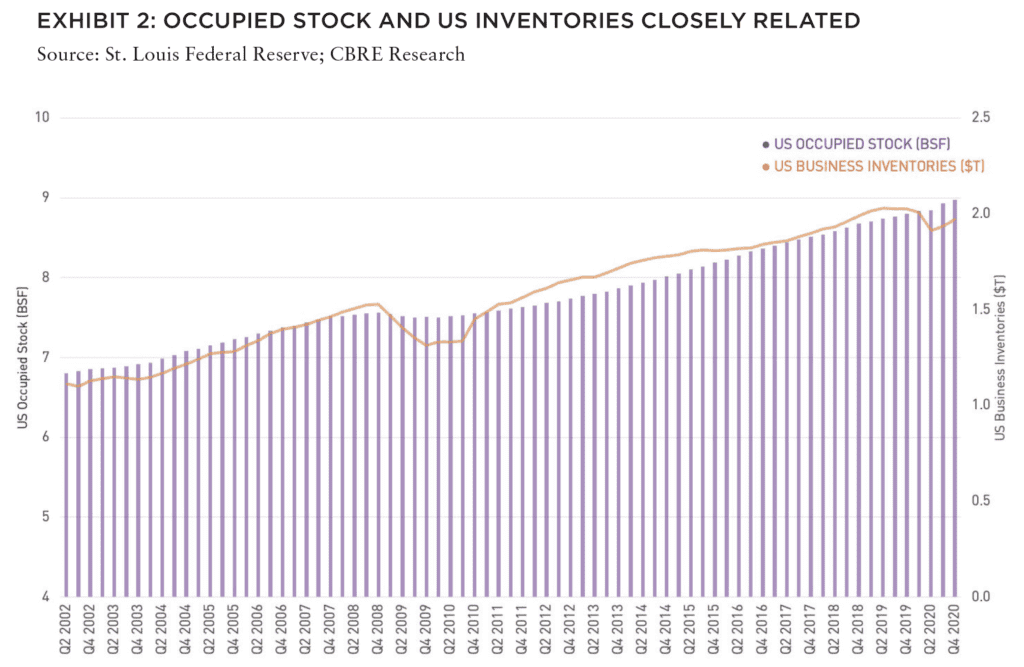

These adjustments to business supply chains will increase the demand for warehouse space in all markets. After a slight blip in early 2020, the growth of US business inventories has resumed as economic activity has picked up, fueled partly by wholesalers and retailers adding stock to store materials and products closer to manufacturing centers and consumers. The need for additional “safety stock” has grown over the past year as suppliers and retailers protect against the unknown future of the pandemic.

This extra inventory inevitably sits in warehouses waiting to be pulled into retail or business supply chains. The impact of this additional inventory is massive. According to CBRE Research, a 5% increase in business inventories requires an additional 400 million to 500 million SF of warehouse space. To put this in perspective, the US market is currently 5.5% vacant, which equates to 800 million SF/74.3 million SM, so the increase in space required would cut the overall vacancy rate in half.

The demand generated by the rise of inventories has the potential to reach all markets. Most likely, users will seek options on the coasts near seaports, but with vacancies at historical lows in all seaport locations, the demand will likely flow inland to a wide variety of locations connected to ports by rail or road.

HOW TO HANDLE RETURNS? REVERSE LOGISTICS.

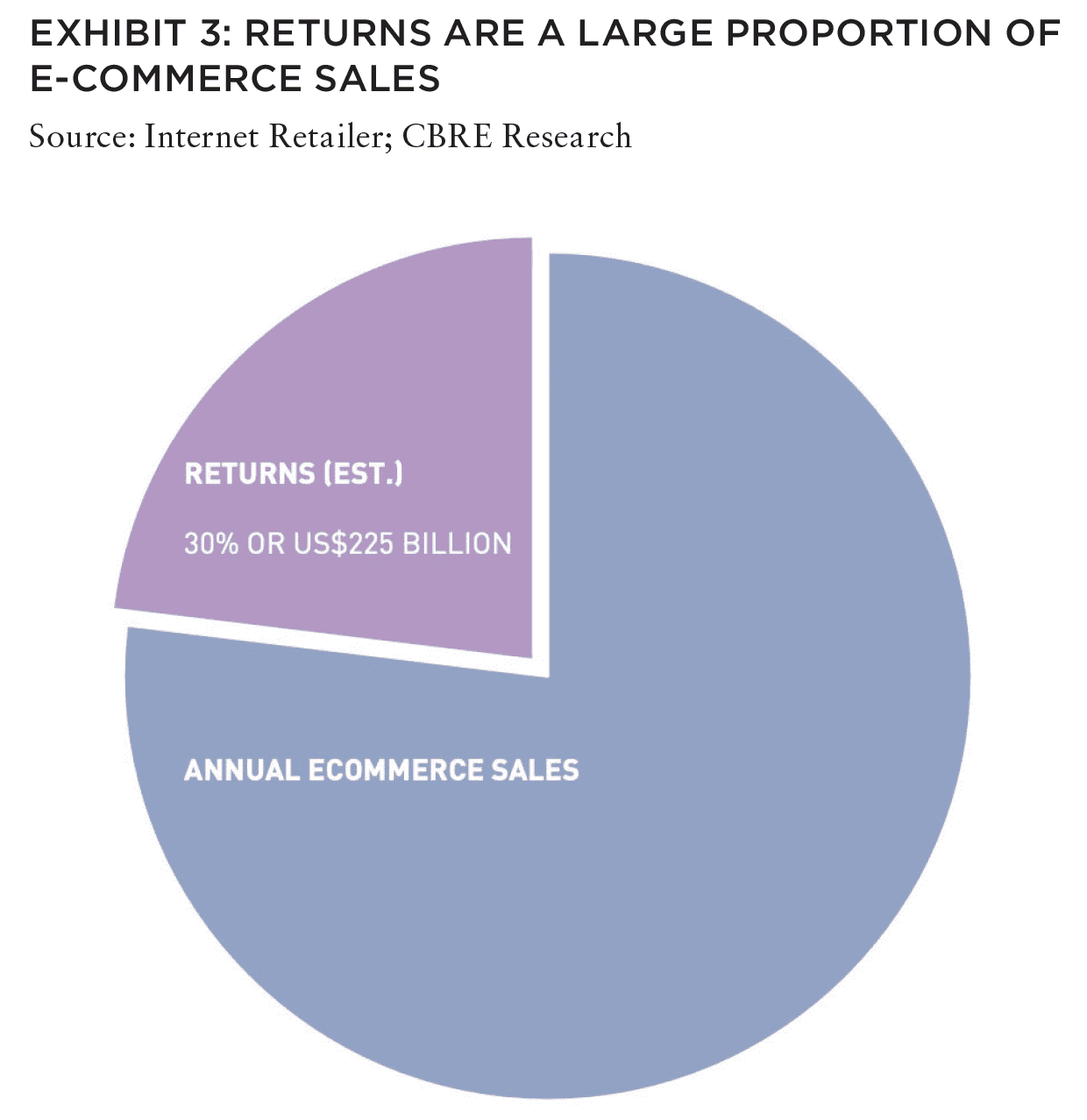

Along with the exponential growth of e-commerce, to remain competitive, online retailers must meet consumer demand for free returns, along with a simple return process. Demand for returns can reach as high as 30% of total e-commerce sales—a massive amount in a rapidly growing sector.

Efficient return strategies are increasingly important for retailers, and the tried-and-true model of in-store returns remains the best, most cost-effective way to handle returned merchandise. This creates an obvious challenge for online retailers because an online order can rarely be returned in a brick-and-mortar environment. As such, shipped returns include significant shipping and handling costs, along with challenges in processing times, liquidation recovery, and manual processes that can result in more than US$50 billion in profit loss and more than 10 billion needless shipments and touches.

While the measurable costs to a liberal returns policy are significant, the major challenge that can make or break an effective reverse logistics strategy is controlling for time and product value depreciation. By some estimates, fashion apparel depreciates by 20% to 50% of its value within three months[3], creating urgency to get inventory back into circulation and ready for resale. Depreciation levels vary by product type, with electronics losing between 4% and 8% of their value per month.

An effective reverse logistics supply chain requires approximately 15% to 20% more space than a traditional outbound supply chain.[4] However, in many cases, returns are handled on an ad-hoc basis when time permits, and often literally in the corner of an outbound fulfillment center. This type of disorganized approach only adds time and cost to the process and increases the risk of product depreciation.

Given both the urgent need for a better returns network, and the insufficient in-house process employed, many retailers outsource their returns management to third-party logistics (3PL) providers in order to free up space for forward logistics. This has created a significant amount of opportunity for the 3PL industry, which, according to CBRE, has grown in terms of square footage by approximately 31% since 2015. Large 3PLs that offer reverse logistics services include XPO Logistics, Ryder, and NFI. The types of products being returned drive specific real estate requirements and space criteria. Typically, second-generation space is preferred over modern, Class A space. Lower ceiling heights are more appropriate, because the activities within the space are high-touch with slower processing, and the odd configuration of pallet loads makes them difficult to safely stack or store in high racks. But, given the time-sensitive nature of processing returns, quality locations both in high density markets and submarkets proximate to major highways (returns are almost exclusively moved by trucks) is paramount.

—

ABOUT THE AUTHOR

David Egan is Senior Vice President at Stockbridge, a real estate investment management firm with approximately US$20 billion of real estate assets under management across the risk spectrum on behalf of US and non-US institutional investors.

—

NOTES

1. CBRE Research, Q4 2020, cbre.us

2. Institute for Supply Chain Management Coronavirus Impact on Supply Chain,

March 2020, ismworld.org

3. Kirstin Linnenkoper, “Saving billions by making smart re-commerce decisions,”

Recycling International, 19 May 2020, recyclinginternational.com/business/savingbillions-by-making-smart-re-commerce-decisions/30460/

4. optoro.com