This article appears in Summit Journal (Summer 2020) | Download PDF

THE ASSET MANAGEMENT FUNCTION IS ALWAYS INTEGRAL TO LONG-TERM VALUE CREATION IN REAL ESTATE, BUT THE COVID-19 CRISIS HAS SERVED AS A FRESH REMINDER OF JUST HOW CRUCIAL THIS ROLE IS FOR NAVIGATING CHALLENGING CONDITIONS.

The spread of COVID-19 across the globe and the rippling effects across all geographies have left no segment of the economy untouched. Real estate markets are no exception. From deserted office buildings to shuttered storefronts and empty hotels, the impact has been more severe than many investors’ downside scenario analyses would have predicted. Yet, global real estate markets still offer potentially attractive returns over the long term—across a wide variety of sectors and risk types—if investors can effectively navigate the current storm. Critical to this effort are the asset managers themselves—also known as the “eyes on the asset.”

THE EYES ON THE ASSET

Even in “normal” times, the tasks performed by real estate asset managers (AMs) are broad-based. AMs develop, monitor, and drive the long-term value creation strategy for real estate properties, focusing on risk management at every stage.

Typically involved even before a property is acquired or a loan is originated, AMs are charged with understanding the latest trends across specific sectors (e.g., office, retail, logistics, etc.) as well as geographical nuances—from the country-level to the city block. They are also the driving force responsible for executing the strategic business plan for each individual property.

Depending on the nature of the asset, this may involve improving rent collection, optimizing a property’s tenant mix, implementing value-creation plans that can range from minor improvements to ground-up construction, and ultimately managing the sale process to realize the greatest potential value for investors.

ENTER COVID-19

Managing this broad set of responsibilities presents its own set of challenges day-in and day-out during normal times, from managing tenant nuisances to clearing construction delays. But adding a global pandemic to the mix changes the equation markedly, and our teams at Barings have attempted to manage this transition from “business as usual” to “crisis mode” in a strategic, timely, and decisive fashion. So how do you manage through a global pandemic?

IDENTIFY THE PROBLEM

First, you need to understand the problem, which takes coordination and communication. For example, after monitoring the development of the COVID-19 crisis in Asia in late 2019 and into early 2020, and then closely analyzing its spread to the West in February and March, our teams set out to understand just how the properties that we owned or lent to would be impacted. It quickly became clear that retailers and hotels were obvious pain points. Fortunately, the grocery-anchored nature of many of our retail assets insulated them to a degree, and our relatively low number of owned hotels would turn out to be a positive in this case. But every sector looked set to be impacted.

Stay-at-home orders across the world introduced new—and potentially longer-term—challenges for commercial office space, and the apartment/multifamily segment seemed likely to take a hit.

At this stage, our goal was to make reasonable assumptions about the short- and long-term financial impacts of the disruption: What percentage of borrowers are likely to miss interest payments? Which tenants are likely to have difficulty paying their rent? Over what time period should we expect this disruption to play out?

Of course, the problem was broader than simply modeling expected rent collections and interest payments. With dozens of value-add projects in the works across the globe, we needed to understand how or if work could continue on projects ranging from the full-scale refit of an eighteenth-century building in central Paris to the ground-up construction of an apartment building in Miami. And, if so, how could it be done in a fashion that put worker and tenant safety first, and comply with local regulations around social distancing?

MAKE A PLAN AND TAKE ACTION—ONE SIZE DOES NOT FIT ALL

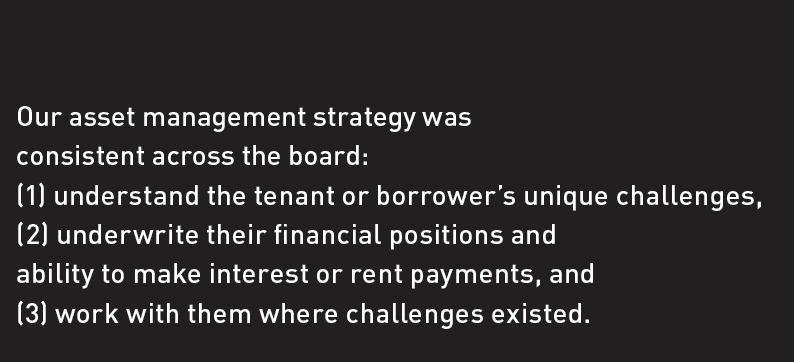

With the input of teams ranging from portfolio managers to engineers, to researchers and third parties (e.g., lenders and property managers), and tenants and borrowers, we were able to triangulate into what we believed to be reasonable assumptions as to the scope of the potential impact. We used these to set broad guidelines for our asset managers across sectors and geographies, and importantly, gave them the flexibility to work with tenants and borrowers one-on-one, especially when it came to difficult discussions around forbearances or rent relief.

The crisis had impacted our tenants and borrowers very differently, depending on their industry sector (e.g., retail, office, logistics, etc.), but geography played less of a role than expected, because similar lockdowns were in place everywhere from Berlin to Boston. For instance, in the US, as more than 500 requests for rent relief came across the desks of our asset managers’ (home) offices, it wasn’t terribly surprising to see that most (300+) came from retailers, while tenants in other sectors, such as logistics, fared much better.

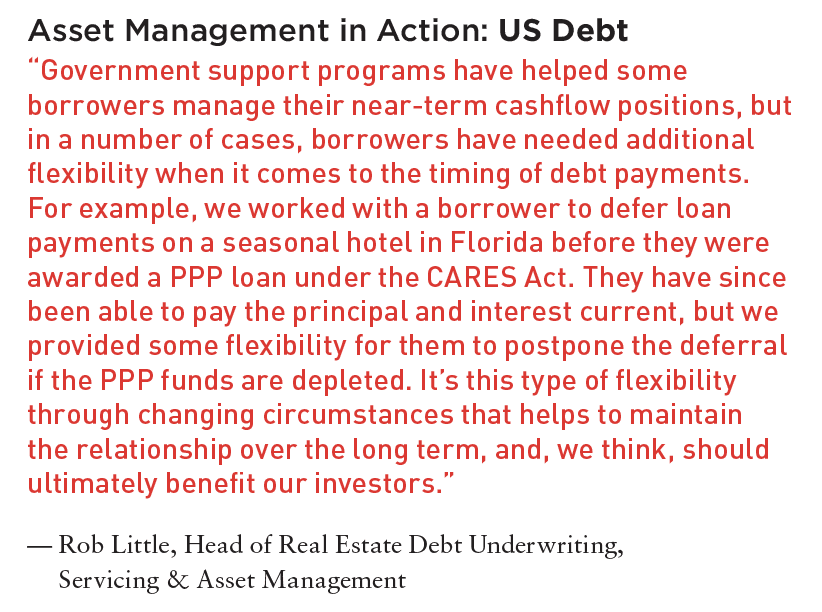

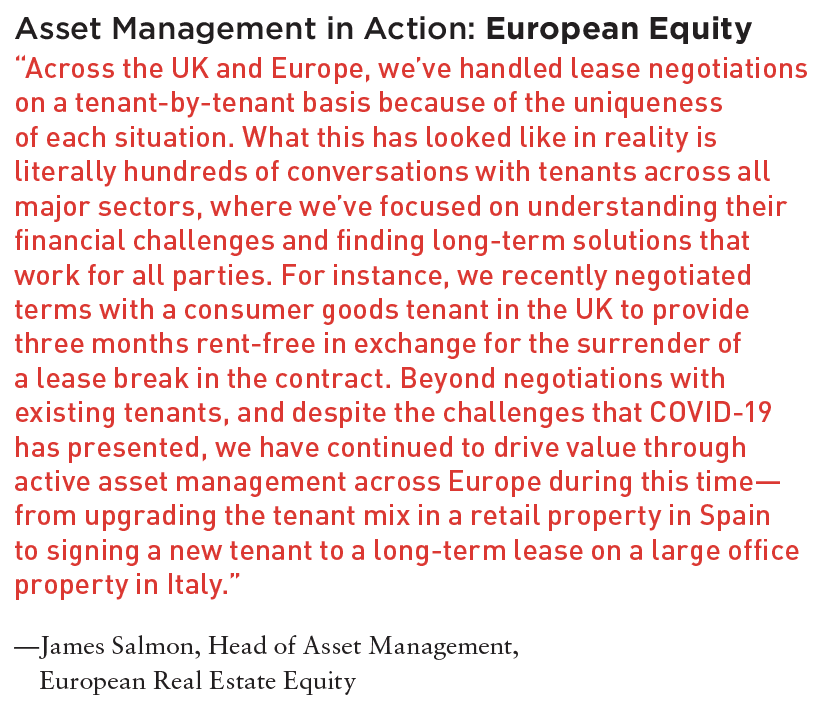

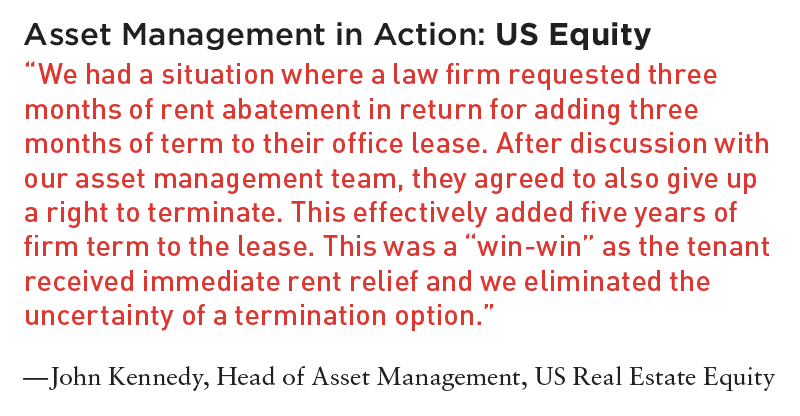

Practically, this has involved the introduction of forbearance measures for certain borrowers and tenants. For instance, a borrower may have been granted the right to defer principal and interest payments for 90 days but was then obligated to repay missed payments within 12 months. Similarly, tenants faced with short-term cash crunches may have been granted rent deferrals, but in a number of cases, they were willing to give something in exchange—for instance, removing a lease break from a contract, which effectively extends the lease years into the future.

Such a strategy of one-to-one negotiations is time- and labor-intensive and involves an incredible amount of communication—not only between the two parties, but also with banks, lawyers, and other stakeholders. The COVID-19 crisis has reinforced our philosophy that experienced, in-house asset management teams with sector-specific knowledge and local expertise are critical for real asset performance. In fact, it is the management of such complex negotiations in times of crisis where the validity of this philosophy becomes even more apparent.

ASSESS AND PIVOT ACCORDINGLY

Perhaps the most encouraging element of this crisis has been the resilience we have witnessed in the face of uncertainty—among our borrowers, tenants, service providers and our own teams.

Not only have leases and debt obligations been creatively renegotiated where needed, but construction projects have forged on—albeit with new social distancing and safety guidelines in place.

Rent collections have also generally been better than the assumptions we made in our initial stress-testing, partly helped by government support programs like the Paycheck Protection Program (PPP) in the US but also, we believe, as a direct consequence of the hands-on approach that our asset managers have taken with tenants.

THE LONG-TERM IMPACT

Challenges certainly remain. Re-opening properties safely with features such as touchless entry, social distancing in common areas, and additional cleaning measures will require much planning and coordination. The length and depth of the cyclical recession is also unknown and will almost certainly put additional pressure on tenants and borrowers. And of course, we are only beginning to scratch the surface of the impact that COVID-19 will have on long-term structural trends like urbanization, e-commerce, and the densification of office space. But this crisis has reinforced our belief in the critical role of asset management as a long-term value driver for real estate investments. Understanding tenants and borrowers and communicating effectively during times of crisis to collectively solve problems doesn’t seem like it will go out of style anytime soon.

—

ABOUT THE AUTHORS

John Kennedy is Head of US Equity Real Estate Asset Management; James Salmon is Head of European Real Asset Management; and Rob Little is Head of Real Estate Debt Underwriting, Servicing and Asset Management for Barings Real Estate.

—