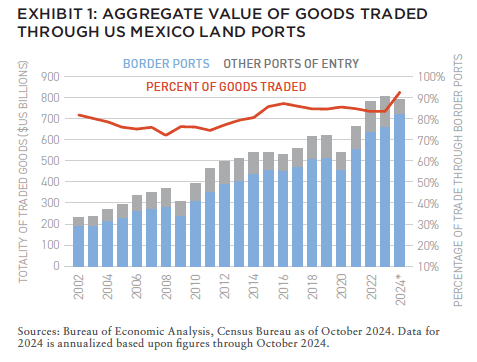

The combined value of goods traded between the US and Mexico reached $808 billion in 2023 according to the Bureau of Economic Analysis (Exhibit 1). That is 2.5 times more than the value of aggregate goods traded between the two countries in 2002.

And in 2019, Mexico surpassed both Canada and China in terms of goods traded. Even as protectionist rhetoric between the two nations has ramped up since the November 2024 elections, Mexico’s status as America’s largest and most important trading partner is unlikely to change given the mutually beneficial relationship.

However, the return of President Donald Trump to the White House and his vociferous endorsement of tariffs to correct the perceived injustices created through global trade, investors and businesses are now concerned that the incoming administration will tip the scales towards self-inflicted and self-defeating economic wounds.

The concept of “reshoring” is an extension of this same logic. Reshoring (also known as on-shoring or near-shoring) references the (re)location of manufacturing and production activities to a firm’s country of domicile. Ironically, Trump’s first presidency spurred a reshoring “renaissance” that continues to the present. In practice, reshoring can take on different manifestations.

As it concerns American industry, currency, wages, and business costs make the prospect of fully repatriating manufacturing operations for domestic firms cost prohibitive over the near-term—and aging demographics create long-term headwinds. In many instances, firms have moved higher value-add segments of their supply chains back to the US while keeping or moving other segments in foreign countries such as Vietnam, Malaysia, China, Canada, and Mexico. Trump has explicitly targeted these half-measures.

Leading up to his reinstatement as president, Trump has pledged 25% tariffs on goods from Mexico and Canada and an “additional 10%” on imports from China until issues related to drugs and illegal border crossings are resolved. The proposed Mexico and Canada tariffs would violate the terms of Trump’s USMCA trade agreement, which he authored during his first presidency, ahead of its July 2026 review. Mexican and Canadian leaders’ initial responses were mixed but generally conciliatory. Clearly, both Canada and Mexico are prepared to make concessions, but their messaging also couched the potential for retaliation.

Real estate investors are also concerned around the multifaceted implications of a more protectionist trade regime in the US. Possible impacts range from longer wait times and higher prices for construction materials and durable goods to a further cooling of demand for industrial space to higher prices leading to upward pressure on rates and borrowing costs. Property investors must make investment decisions that span multiple years, and given the uncertainty around trade policy, many would prefer to pause as they assess what the next four years could bring.

PORT MARKETS ALONG THE US MEXICO BORDER

Real estate investment along the US-Mexico border is relatively nascent. Historically, 83% of total goods trade between the US and Mexico comes through four border ports (or “districts,” as described in the parlance of the US Census Bureau). These four districts are comprised of the industrial metros of Brownsville, Laredo, McAllen, and El Paso, Texas; Nogales, Arizona; and San Diego, California. Combined, these industrial markets encompass approximately 400 million square feet of industrial space.

For comparison, Chicago has 1,400 million square feet of stock, making it the largest industrial market in the nation. Relatively, there is not a lot of warehouse space in and around ports of entry along the US and Mexican border.

Industrial markets accompanying ports of entry do not need to be sizable. Savannah, the fourth busiest coastal port in the continental US, has an industrial market of 136 million square feet, versus nearby Atlanta with nearly 900 million square feet of inventory. Traditionally, goods move through ports directly to primary warehouse markets largely by interstate and rail. But increasingly, ports are seen as an intermediate stop for goods on the way to their destination. The post-pandemic reconfiguration of supply chains has prioritized optionality and resiliency through redundancy versus simply trying to achieve the greatest cost efficiencies.

Savannah provides a helpful case study around how a port industrial market can evolve. From 2008 to 2024, Savannah’s industrial stock rose by 174% cumulatively, versus 19% for the national industrial market. While the market has experienced higher than average vacancy due to the accelerated pace of construction, warehouse rent growth in Savannah has outpaced the US even as Industrial rents nationally rose at their fastest pace ever following pandemic lockdowns.

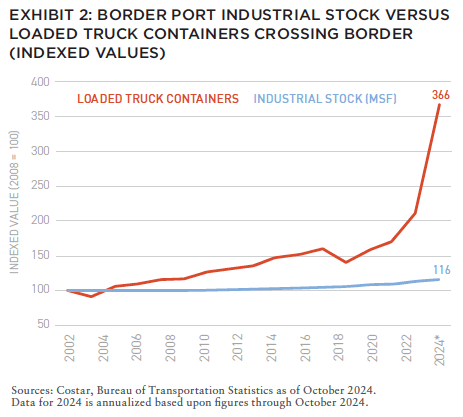

While the stock of industrial space across US Mexico border ports has been rising for years, they have lagged the national pace. From 2008 to 2024, the aggregate amount of space across border ports has increased by only 16% versus 19% nationally.

In 2008, 2.7 million loaded truck containers crossed the border; by the end of 2024, it would be close to 10 million—a 266% increase, or nearly sixteen times the pace by which industrial stock has expanded (Exhibit 2). The degree to which Southern US border port industrial markets are undersupplied versus the volume and the value of the products that pass through them has become almost comically stark. Given the uncertainty around how trade policy will change and how and when those changes will be implemented, one could easily imagine a scenario in which demand for warehouse space in border ports could dramatically increase in coming years—particularly along trade routes with goods that require assembly or other sources of value-add.

REASONS FOR UPSIDE TO THE OUTLOOK FOR US MEXICO TRADE

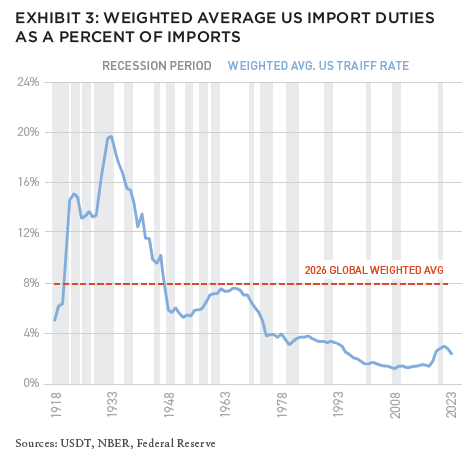

Market consensus appears to coalesce around a baseline scenario of manageably higher tariffs and the initial Trump duty announcements as a starting point for negotiations. Bloomberg forecasts overall US import taxes will increase from around 3% in 2024 to around 8% in late 2026, mainly due to China (Exhibit 3). In addition, potential tariff increases are expected to be targeted and used to extract specific concessions. A trade war between the US and it’s top three US trading partners—Mexico, Canada, and China—is unsustainable because it would severely undermine economic growth, price stability, and employment.

Among other benefits, trade with Mexico has a greater association with supporting US jobs than China through bilateral manufacturing as around 40% of the content from Mexican imports are produced or finalized in the US compared to around 4% from China, based on Wilson Center analyses. Although posturing and brinksmanship between the two nations is likely to continue, there are long-lived and entrenched factors that compel both to maintain mutually beneficial trade relations.

STRUCTURAL COST ADVANTAGE

Aging US demographics and a low unemployment rate point to lack of slack in the workforce whereas Mexico’s population growth and lower labor costs provide production capacity and price efficiency. The Mexican peso has continually weakened against the American dollar for decades. The MXN/USD exchange rate has fallen to 0.0494 in December 2024 from 0.3618 in Q1 1990. The CAD/USD exchange rate in contrast has only declined from 0.8548 to 0.7057 over that same period.

From 2006 to 2021, Mexico’s cost competitiveness has improved marginally by 2.3% while China’s cost competitiveness has declined by 12.4%, according to Boston Consulting’s Global Manufacturing Cost-Competitiveness Index. The cost advantage that Mexico possesses over both China and Canada has been built up over decades, and supply chains for American industry increasingly traverse the Mexican border. Even as the next Administration prepares to start its term, countless corporate executives are plying the Trump’s ear about the criticality of trade with Mexico.

PUBLIC/PRIVATE INVESTMENT AND BORDER SECURITY

One of the reasons behind Mexico’s favorable cost structure is due to past and future investment in transportation infrastructure. Around El Paso alone, $7.8 billion of infrastructure spending has been proposed between 2024 through 2028. US foreign direct investment into Mexico, whose GDP activity overwhelmingly is related to US export production, has also risen in the years following the pandemic. Training has also been a focus of the Mexican government and global firms to improve the productivity of the country’s domestic labor force. Additionally, despite repeated incriminations over illegal border crossings and drug trafficking, there have been marked improvements in safety and crime reduction in and around the border over the past year. With greater media focus and public sector budget allocation to monitoring crossings, border security should continue to improve.

FINANCIAL MARKETS

Despite that the “Republican sweep” in the 2024 presidential and congressional elections, financial markets will be a referendum on the unintended consequences of the Trump Administration’s policy actions. While public equity markets have moved higher on the promise of lower headwinds for corporations from taxes and regulation following the November election, the 10-year Treasury yield has moved up by around 70 basis points from its mid-September levels in part accounting for the likelihood of higher inflation and more deficit spending. Trump often associates his performance with market trends and adverse effects due to trade policy resulting in accelerating inflation and tighter financial conditions should restrain the administration from the worst excesses.

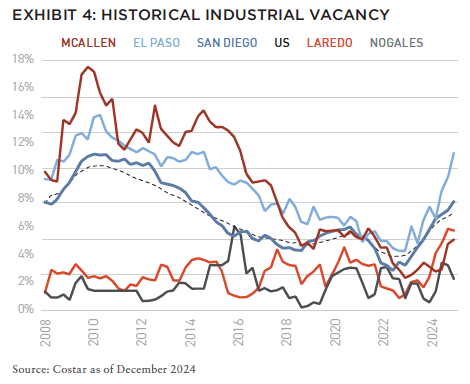

Capital flows into border port industrial markets have been subdued especially when considering how enthusiastically institutional investor appetite has grown for the industrial property sector over the past decade. It is tempting to pass on a strategy that appears right in the crosshairs of a trade policy regime change, yet the degree to which border port industrial markets have been undersupplied has been persistently dramatic and becoming more so. As critical as US-Mexico trade has become even since the last Trump Administration, there is justification to think that disruption to trade policy will be marginal coming from a “pro-business” President but represents an added source of return. Smaller markets, however, can in the near-term become overrun by development spurred by capital flows so monitoring supply cycles is critical to any longer-term investment exposure (Exhibit 4).

NEW: SUMMIT #17

+ EDITOR’S NOTE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT

+ CONTACT

WHERE ARE WE IN THE CYCLE?: OVERVIEW OF THE US ECONOMY AND REAL ESTATE SECTOR

Richard Barkham + Jacob Cottrell | CBRE

COMPELLING OPPORTUNITIES: MAKING A CASE FOR US REAL ESTATE

Karen Martinus + Mark Fitzgerald + Max von Below | Affinius Capital

OPEN WINDOW: WHY NOW IS THE TIME TO INVEST IN COMMERCIAL REAL ESTATE

Chad Tredway + Josh Myerberg + Luigi Cerreta | JPMAM

NORMALIZING MOVEMENT: POPULATION MOVEMENTS NORMALIZING AFTER COVID-19 SHOCK

Martha Peyton + Matthew Soffair | LGIM America

CHRONIC SHORTAGE: THE US HOUSING SCARCITY WILL BE LIKELY TO PERSIST FOR SEVERAL YEARS

Gleb Nechayev | Berkshire Residential Investments

FLORIDA FOCUS: PRODUCTION INDEX BELOW 50 CURIOUSLY SIGNALS OPPORTUNITY

Rafael Aregger | Empira Group

WHOLESALE CHANGE: DEMOGRAPHIC CHANGES AND STAGNANT INVENTORY CREATE NEW OPPORTUNITIES FOR RETAIL

Stewart Rubin + Dakota Firenze | New York Life Real Estate Investors

GAME CHANGE: INFRASTRUCTURE GROWTH ACCELERATING WITH AI

Jon Treitel | CBRE Investment Management

FOR THE TREES: MASS TIMBER INTEGRATION IN INDUSTRIAL REAL ESTATE

Mary Ellen Aronow + Erin Patterson + Caroline Suarez + Cassidy Toth | Manulife Investment Management

BORDER INDUSTRIAL: INVESTING IN US/MEXICO BORDER PORT INDUSTRIAL MARKETS

Dags Chen, CFA + Lincoln Janes, CFA | Barings Real Estate

RESILIENCE AMIDST UNCERTAINTY: HOW ISRAELI AND UKRAINIAN INVESTORS ARE ADAPTING REAL ESTATE STRATEGIES DURING CONFLICT

Asaf Rosenheim | Profimex

CYBER RISK VIGILANCE: HOW REAL ESTATE DIRECTORS AND BOARDS CAN GUARD AGAINST CYBER RISK

Marie-Noëlle Brisson, FRICS, MAI + Michael Savoie, PhD | CyberReady, LLC

ALTERNATE REALTY: DIGITAL RIGHTS MANAGEMENT FOR REAL ESTATE AND AUGMENTED REALITY

Neil Mandt | Digital Rights Management + Steve Weikal | MIT Center for Real Estate

DRIVING FORCE: UNDERSTANDING SYNDICATED LOANS AND MULTI-TIERED FINANCING

Gary A. Goodman + Gregory Fennell + Jon E. Linder | Dentons

HOUSING COMPLEX: CUTTING-EDGE APARTMENTS ARE A CATALYST FOR A MORE PROFITABLE FUTURE

Alejandro Dabdoub | AOG Living

NOTES

[]

ABOUT THE AUTHOR

Dags Chen, CFA is Managing Director and Head of US Real Estate Research and Strategy, and Lincoln Janes, CFA, is Director of US Real Estate Research and Strategy for Barings Real Estate, one of the world’s largest diversified real estate investment managers, with $48.18 billion AUM, offering a broad spectrum of solutions across private real estate debt and equity.

THIS ISSUE OF SUMMIT JOURNAL IS GENEROUSLY SPONSORED BY

/ EXECUTIVE SPONSOR

AOG Living is a leading fully integrated, multifamily real estate investment, construction, and property management firm headquartered in Houston, Texas. AOG Living has acquired, built, or developed more than 20,000 multifamily units with a total aggregate value of over $2.4 billion and has a growing portfolio of more than 35,000 apartment homes and 170+ properties under management throughout the nation. Learn more at aogliving.com.

/ ASSOCIATE SPONSOR

Vertically integrated owner, operator, and developer of Sunbelt multifamily. Partnering with institutions on a single-asset and programmatic basis. 28k+ units acquired and developed. 62k+ units under management. 1,500+ associates. 8 Sunbelt states. To learn more, visit hrpinvestments.com and hrpliving.com. And for more information, contact john.duckett@hrpliving.com.

/ SUPPORTING SPONSOR

Affinius Capital is an integrated institutional real estate investment firm focused on value-creation and income generation. With a 40-year track record and $64 billion in gross assets under management, Affinius has a diversified portfolio across North America and Europe providing both equity and credit to its trusted partners and on behalf of its institutional clients globally. To learn more, visit affiniuscapital.com.