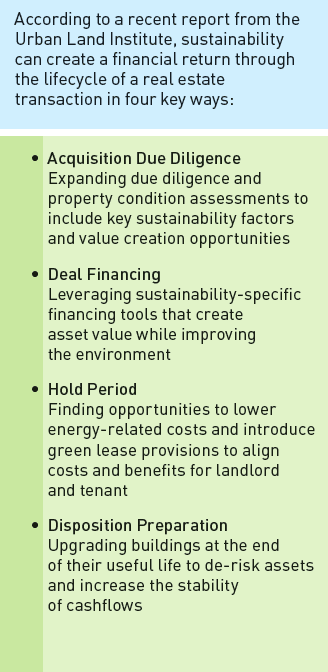

SUSTAINABILITY HAS LONG BEEN THOUGHT OF AS A COST, RATHER THAN SOMETHING THAT CAN DRIVE VALUE. BUT THAT TYPE OF NARROW THINKING IS STARTING TO CHANGE.

Global capital markets are evolving, bringing increased focus on environmental, social, and governance (ESG) criteria. Where the public sector has failed to bring about change, the private sector is moving forward with ESG at an accelerating pace. In doing so, capital markets are transforming the process by which capital is allocated, as well as the issues impacting investment decisions.

This is not a trivial matter. By 2018, 25% of all professionally managed assets, worth more than $11.6 trillion, were under ESG investment strategies. The issuance of green bonds globally represented more than $167.3 billion in 2018. Participants in GRESB, the investor-driven organization that assesses the sustainability performance of assets worldwide, have grown in number from 200 in 2010 to more than 900 in 2018 and now represent more than 79,000 assets with a gross value exceeding $3.5 trillion.

Together these trends represent a sea change in thinking about sustainability. It is longer seen as mere cost, but growing in importance as a field of strategies and KPIs that drive asset value. As an extension of the discussion held at AFIRE’s 2019 European Conference, held in Frankfurt, Germany, this article provides a deep dive into a fictional example that highlights the issues – and the benefits – of ESG investing.

CLIMATE VS. CAPITAL

As a way to understand the evolving conversation around ESG, consider this study of the fictional Alpha Fund, an amalgam that resembles a familiar case.

Dieter and Gerhard are experienced real estate professionals and key members of the Alpha Fund’s Investment Committee. In their recent review of the 2019 budgets, they learned that their flagship open-end fund, the Alpha Future Fund (AFF), had recently received €40 million in new capital. But the use of the capital didn’t seem obvious. They asked each other, what path will create the most value for Alpha, as well as our investors?

Founded in 2011 by its current CEO, Manuel, Alpha had a reputation for innovation and strong risk-adjusted returns. Prior to founding Alpha, Manuel was a partner with a leading global real estate investment firm. Alpha was owned 50% by a German insurance company and 50% by the management team, of which Manuel personally owned 20%.

In the past eight years, Alpha had raised three closed-end funds and one open-end fund – the AFF. With assets under management totaling €5.1 billion across four funds, and strong top-quartile returns, Alpha seemed to have a promising future.

But there were challenges. As CEO, Manuel was a quintessential deal person who typically saw most value being created in the “buy.” While the firm had a reputation for being a savvy buyer and for its value-add approach, Manuel did not personally have a great deal of asset management experience in his career. As a result, Alpha had earned a reputation as a very good buyer but only an average asset manager. While the firm’s returns had been strong and in the top quartile of their peer group, the capital markets team was being asked more and more frequently about the firm’s ESG policy and benchmarking strategies, such as ULI Greenprint and GRESB. Manuel was aware that some large investors, including Dutch, Scandinavian, and US pension funds, had made it clear that a strong ESG strategy would be a prerequisite for getting access to their capital.

This prerequisite represents a tension that leading global property investors face every day. But it also presents a false choice, because climate and capital are not fundamentally at odds.

DISPELLING A FALSE CHOICE

Rather than having to choose between ESG and something else, ESG can actually increase property values and fund manager returns through an incentive fee structure, thus becoming a strategic option with demonstrable financial value.

Dieter and Gerhard were well-versed in the versatility of these returns, which were further prioritized by Alpha’s expanding investor base. ESG policies were raised more frequently in meetings, and consultants were adding significant areas of inquiry to their due diligence questionnaires (DDQs). Additionally, many of the US cities with AFF assets had mandatory benchmarking requirements which exposed the energy performance of their assets to public disclosure, and AFF’s assets in the EU had energy efficiency directives with mandatory reporting. In fact, some EU members had gone one step further by benchmarking some buildings and limiting the use of those that were underperforming.

During a recent partners’ meeting at Alpha, its participants discussed the idea of ESG and its impact on Alpha. The partners agreed to investigate the potential for integrating ESG standards in its real estate transactions, and how this integration could potentially create value for Alpha across its assets and its reputation.

Dieter, Gerhard, and the entire AFF Investment Committee thus faced an interesting choice. Historically, it had used new capital to acquire real estate assets. For example, the committee was considering an investment in Paris anticipating a going-in cap rate of 5.2% with an unlevered IRR of 10.5%, and with the modest debt utilized by the open-end fund, a levered IRR of 13.4%. The acquisition of this approximately 180,000-square-foot (16,700-square-meter) office building was fully underwritten and the investment memo was ready for discussion by the committee.

At the same time, Gerhard pointed out that the recent annual budget review had identified approximately €40 million of capital and operating expense projects in the existing portfolio that were projected to have an average net payback of 4.5 years. These projects included efficiency projects, such as HVAC and lighting upgrades, as well as capital projects that would ensure continued building operation while ensuring a payback where high performance options were considered. Gerhard’s team had also taken advantage of existing rebates and incentives, mostly in the US.

Referencing the directives from Alpha’s partner meeting, Dieter noted that investing in projects with an ESG “story” would be well-received by investors driving capital inflows. In turn, this would increase fees to Alpha and everyone’s compensation – but especially Dieter, who was partly incentivized by assets raised. Importantly, it would also help Alpha address continued legislation in both the US and EU.

With both Dieter and Gerhard advocating to use the €40 million in new capital funds for ESG projects, Manuel had a choice to make. As CEO, he was the team’s primary decision-maker, but he was focused on the entire team and had a broad definition of winning.

TELLING THE ESG STORY

When this case study was shared for discussion with AFIRE’s 2019 European Conference, participants suggested that Manuel faced a false choice. An organization could commit to the ESG program, acquire a building now, and then fund it over time – but perhaps the AFF Investment Committee wasn’t the right place to house this discussion. At Alpha – and at many other real-world fi rms – ESG had only ever been seen as a cost and never considered a source of tangible financial returns. In any case, as mandatory benchmarking grows in the EU and in many US cities, owners can fully utilize the use of benchmarking data to make better decisions that drive asset values higher.

In the example of AFF, Gerhard had reviewed a list of projects (LED lighting upgrades, photovoltaic system installations, building management systems, etc.) totaling €40 million for which his asset management team was seeking approval during the 2019 budget reviews. The projects were typical of projects presented in prior years, evenly spread across the portfolio by asset type, class, and geography, but often rejected so as not to impact the cash-on-cash returns. The lease structure was such that approximately 30% of the operating cost savings would benefit the tenants. Alpha had until that point only considered but not implemented a green lease program.

The proposed project upgrade program would cost €40 million in 2019 – but it would also underscore Dieter’s note about the importance of telling an ESG story. When lease structure was taken into consideration, the payback would be 6.5 years; 2020 EBITDA impact would be €6.2 million to AFF, and with it, the fees earned by the Alpha management company would also increase. The asset management team was confident that the projects were well-scoped and that both energy savings and project costs were achievable, while enhancing income by reducing existing capital improvement program costs; lower total utilities budgets; reducing maintenance and repair costs; and increasing rent and occupancy through updated services and amenities.

Additionally, the upgrades would reduce electricity consumption across the impacted assets by 17%, and the fund overall by 8.5%, versus the ULI Greenprint median of 3.7%. Total carbon emissions reduced would be 2,295 tons – the equivalent of planting nearly 96,000 trees. The projects would also reduce water consumption across the portfolio by 5.3% – well ahead of the 2.9% median for ULI Greenprint members.

CALCULATING HARD AND SOFT ROI

While we don’t know Manuel’s final decision – it’s ultimately a decision being made every day by investors, who are facing increased pressures (and incentives) to incorporate ESG into their strategies. AFIRE members suggested that areas of financial return cross both “hard” and “soft” ROI, including reduced insurance, repairs and maintenance, and energy-related costs on one side, and optimized teams, asset occupancy, and capital market access on the other.

The example case of AFF underscores a broadened thinking about how sustainability can create value for assets and organizations. The results of the discussion at AFIRE’s 2019 European Conference are ultimately part of a growing global conversation that can potentially lead to tangible changes in how the industry and organizations think about sustainability and value creation.

—

ABOUT THE AUTHOR

Brad Dockser is the CEO of Green Generation, which transforms the world’s built environment through innovation and solutions by integrating energy, real estate, technology, and capital markets to “Operate in the Green.” He also serves on the ULI Global Advisory Board for the Center for Sustainability and Economic Performance.

NOTES

THIS ARTICLE ORIGINALLY APPEARED IN SUMMIT: ISSUE #2

—