Translating rising climate risks over the next decades requires a cash flow model that starts today—and should be a necessary exercise for all investors.

Atmospheric heat hit daily, weekly, and monthly records on three continents in 2023.1 The top layer of all the major oceans also reached record high temperatures in 2023. Volatile weather has caused drought, floods, heat stress, wildfires, and wind damage at unprecedented rates across earth’s human settlements in recent years. Higher temperatures also mean that the atmosphere can hold more water vapor, which creates more precipitation, even though drought conditions in isolated areas also increase due to the heat.

Climate-induced threats to human life and to property are rising and no clear end is in sight.

So, what should real estate investors do about climate change? The top priority of the real estate industry has rightly been to focus on de-carbonization. This is a far-sighted and appropriate response, given that the energy used to operate and construct buildings accounts for two-fifths of global emissions, and in urban areas, this contribution spikes to over two-thirds of urban greenhouse gas (GHG) emissions.2 Unfortunately, reducing carbon emissions is not likely to reverse the warming of the planet that has already occurred.

Even if the entire world manages to reduce harmful emissions over the coming decades, weather volatility will continue to persist, so long as C02 levels in the atmosphere are 60% higher than what they were in the pre-industrial era.3

In other words, there is no guarantee that GHG levels in the Earth’s atmosphere will be reduced, despite all the “net zero” pledges that have been made by countries, municipalities, corporations, and asset owners.

The go-forward increases in GHG could moderate, but climate scientists are not sure how quickly CO2 parts per million would fall from current levels (in the 420 range), given all the deforestation, desertification, and shrinkage of ice sheets that has occurred over the past 50 years.4 All this environmental damage reduces the atmosphere’s ability to repair itself and it raises sea levels, which adds considerable risk to coastal communities. So, even if humankind figures out how to stop putting GHG in the atmosphere, we are likely to be living with more volatile weather for the rest of this century.5

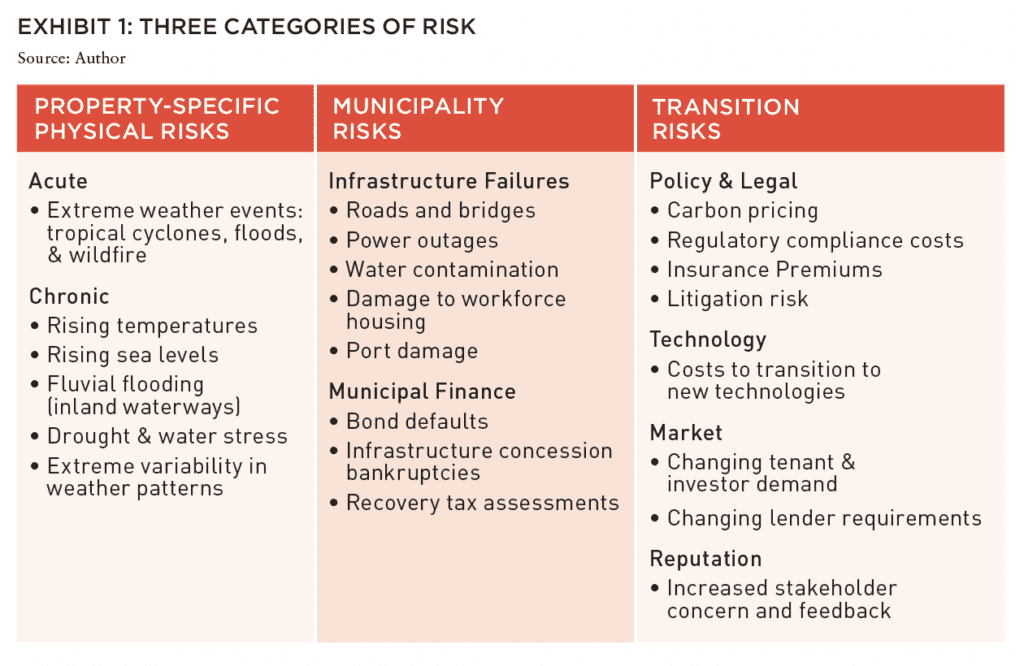

ASSET-LEVEL, MUNICIPAL, AND TRANSITION RISKS

For real estate investors, climate risks can be understood across three dimensions. The first is the property level and includes the site-specific risks of a precise location and the building that sits at that location. In the industry these are usually referred to as a property’s “physical climate risks.” The second level are the ways that physical risks threaten supporting infrastructure and the financial health of a community. Sometimes called market-level or “dependency risks,” Exhibit 1 labels them as “Municipality Risks.” Finally, there are “transition risks” that relate to changes in regulatory regimes (such as carbon pricing, or incentives to avoid the emission of GHG) or changes in the insurance market over time.

WHAT PRECAUTIONS CAN INVESTORS TAKE?

This article suggests several steps real estate owners can take to reduce and mitigate climate risks. These risks cannot be eliminated, but they can be managed. A dual course of action—focused on reducing carbon emissions and preparing for climate change is a prudent one for real estate investors.

As owners submit data to GRESB and make disclosures toward achieving a net-zero pledge, more sources of information and tools for measuring and making progress toward de-carbonization have become available.

By contrast, preparation for climate change is not as far along in getting traction in many industries, including real estate. This lag exists even though peta-bytes of climate data have been collected and thousands of scientific papers have been published describing the likely scenarios that global warming and higher atmospheric humidity are likely to cause. What are the main reasons for this lag effect?

- Insurance is still widely available to hedge the short-term effects of physical climate risk.

- Government subsidies can create moral hazard situations, which may incentivize some asset owners to avoid taking necessary precautions.

- Climate risk data can be confusing and sometimes contradictory.

- Links between climate risk and value/rent are not well-understood; climate change has not yet been built into investors’ thinking.

Let’s look at each of these four factors in greater depth.

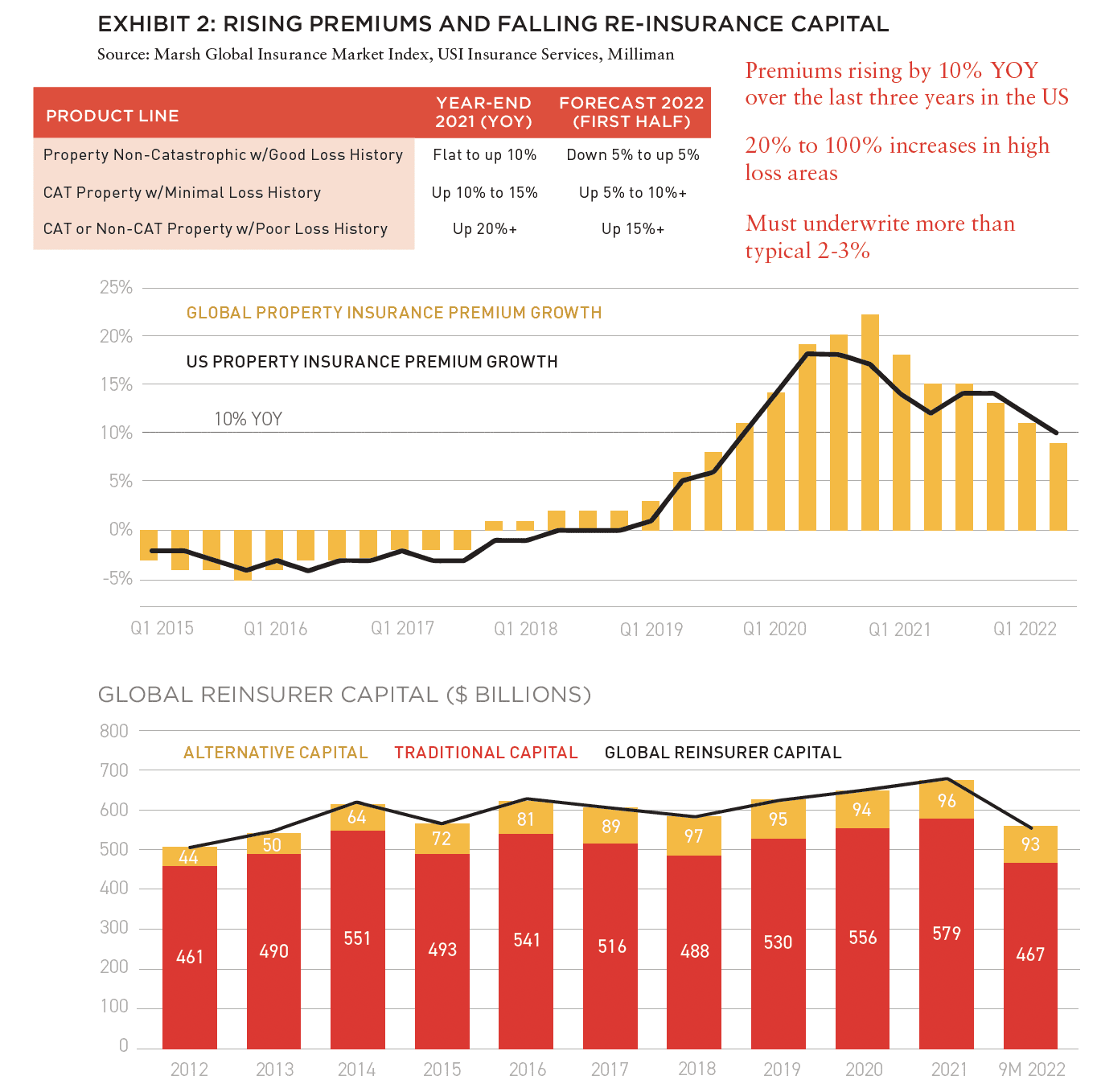

1) INSURANCE GIVES A FALSE SENSE OF SECURITY. The biggest issue with reliance on insurance is that this protection is purchased one year at a time. In the years ahead, just when property insurance will most be needed, it will become most expensive and, in some cases, unattainable. Insurance costs in the US have been rising between 15% and 20% per year in the last five years.6

In higher-risk areas, such as coastal Florida, insurance costs increased between 50% and 100% in 2023. Real estate investors’ time horizon is measured in years and decades. Insurance coverage is locked in just one year at a time. This temporal mismatch will create long-term issues for investors unless they anticipate how insurance markets are likely to react to weather volatility and rising sea levels. A lessening of capital available in the re-insurance market is a clear warning signal that catastrophic insurance is going to be more difficult to obtain in the future than it has been in the past. The re-insurance market plays an important role in allowing insurers to spread the risks in their insured portfolios over a wider pool of assets.

So, what can be done? There are a number of steps investors can take to prepare for changes in the property insurance market. Risk managers can pay close attention to how insurers are pricing climate risk. They can find out what climate risk data and forecasting models insurers are using and which physical risks they are most sensitive to.

When insurers pull out of markets, as recently happened in California and Florida, risk managers can find out why. Importantly, risk managers can find out if geographic diversification will allow higher-risk properties to get insured alongside lower-risk properties, or if insurers will simply stop writing coverage at certain locations. Finally, they can find out what asset hardening strategies, especially for flood and wind damage, insurers like to see.

The insurance industry—through tens of thousands of underwriters and claims adjusters—have more data on damage estimates than any other source. In other words, investors: Learn how your insurer is pricing climate risk. Anticipate that insurance may no longer be available in the highest risk locations within the next ten years.

2) GOVERNMENT ACTIONS CREATE MORAL HAZARD. Millions of property owners believe that the government will be there to pay claims and to rebuild infrastructure when disaster hits.7 Research done by Rebuild by Design found that 90% of all counties in the US have been eligible for federal disaster assistance at least once between 2011 and 2021.8

The US government is truly the insurer of last resort for the entire country. The Federal Emergency Management Agency administers a national flood insurance program and oversees the payout of hundreds of millions of dollars each year in disaster relief, along with a complex web of other state and local sources.9 Although many of FEMA’s programs are designed to benefit households, rather than commercial property owners, Rebuild by Design found that most disaster relief is paid out to coastal cities where the most valuable commercial and residential real estate is located.10 The difficulties of this system are well-known. It leads to rebuilding in high-risk areas and it also creates a growing and unbudgeted liability for all levels of government at a time when Federal budget deficits are hitting record levels and political opposition to these huge deficits is growing. Finally, studies show it is highly regressive with taxpayers paying for more assistance to wealthy property owners than to lower-income owners.11

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #13

Benjamin van Loon | AFIRE

OFFICE TROUBLES: FINANCIAL RISKS AND INVESTING OPPORTUNITIES IN US CRE

Dr Alexis Crow | PwC + Byron Carlock

THE UNDERPERFORMANCE PARADOX: WHY INDIVIDUAL INVESTORS FALL BEHIND DESPITE BUYING LOW

Ron Bekkerman | Cherre + Donal Ward | Tenney 101

CLIMATE THREAT: EXTREME WEATHER IS THE NEW NORMAL FOR REAL ESTATE

Jacques Gordon, PhD | MIT

CLIMATE OPPORTUNITY AWAITS: HOW REAL ESTATE CAN INVEST IN CLIMATE ADAPTATION

Michael Ferrari, PhD and Parag Khanna, PhD | Climate Alpha

PREMIUM PRICE TAGS: INSURABILITY THROUGH PROPERTY RESILIENCE DATA

Bob Geiger | Partner Engineering & Science

REAL ESTATE WEB3: THE EMPEROR’S NEW CLOTHES OR THE NEXT BIG THING?

Zhengzheng Tan, Alice Guo, and Naveem Arunachalam | MIT

ADAPTIVE TO REUSE: COULD BUILDING CONVERSIONS BE DIFFICULT, EXPENSIVE . . . AND STILL PROFITABLE?

Josh Benaim | Aria

RENOVATE, REBRAND, REPOSITION: ADDING VALUE TO MULTIFAMILY THROUGH REVITALIZATION

Robert Kilroy, CFA | The Dermot Company + Will McIntosh, PhD | Affinius Capital

REDEFINING THE PROGRAM: A CONVERSATION WITH ARCHITECT DAVID THEODORE

Peter Grey-Wolf | Wealthcap + David Theodore | McGill University

SENIOR HOUSING UPDATE: EMERGING OPPORTUNITIES THROUGH DEMOGRAPHIC TAILWINDS AND DIMINISHING SUPPLY OUTLOOK

Robb Chapin, Jack Robinson, Andrew Ahmadi, and Morgan Zollinger | Bridge Investment Group

SENIOR HOUSING UPDATE: UNPRECEDENTED DEMOGRAPHIC ACCELERATION MAY DRIVE STRONG OPERATING FUNDAMENTALS AMID ECONOMIC SLOWDOWN

Tom Errath | Harrison Street

HOLIDAY FROM HISTORY: REASONS FOR US OPTIMISM IN A CHANGING GLOBAL ENVIRONMENT

Charlie Smith | Newmark

CRADLE TO CRADLE: AN ALLOCATOR’S VIEW ON IMPLEMENTING ESG INITIATIVES

Christopher Muoio and Katie Cappola | Madison International Realty

FREE LUNCH: MULTI-DIMENSIONAL DIVERSIFICATION IS A FULL-COURSE FREE MEAL

Elchanan Rosenheim and Tali Hadari | Profimex

CAMPAIGN MESSAGING: CFIUS, AFIDA, AND EXPANDING FEDERAL AND STATE RESTRICTIONS ON FOREIGN INVESTMENT IN US REAL ESTATE

Caren Street, John Thoms, and Anya Ram | Squire Patton Boggs

What can be done? Government support for disaster relief is a cornerstone of the US democratic system, even though the “right” to disaster assistance is not mentioned in the Constitution. A series of Disaster Relief Acts passed in the 1950s, 70s, and 80s will not be repealed, because they created politically popular programs that elected officials often use to gain favor with their electorates. However, FEMA and other federal agencies, including the Army Corps of Engineers, are studying the resiliency practices of other countries and finding much room for improvement.12

Requirements are coming to rebuild in a way that takes into account the high and growing likelihood of recurrence of floods, hurricanes, and storm surge damage. Local communities will be incentivized to stop mindlessly replacing roadways and other infrastructure damaged by floods with the exact same design. Investors can track these changes and participate in them by using their insurance claim settlements to “build back better.”

Another strategy that is being pursued by Boston, Miami and New York City is to fund the building of enormous sea walls paid in part by assessments levied on real estate owners as well as potentially receiving state and federal assistance. This strategy is impractical for the entire hurricane-prone parts of the eastern seaboard, but in the final analysis it may prove to be less expensive than funding enormous disaster relief requests from state governors when cataclysmic damage occurs.

3) CLIMATE RISK DATA IS CONFUSING. In the last five years, dozens of privately funded climate risk data providers have sprung up to meet the rising demand from commercial property owners and insurance companies for granular climate risk data that can be used to assess future risk at specific addresses.

A 2022 review of these data options by ULI and two academics13 found that risk ratings by different firms were not consistent with each other. Moreover, the approach to measuring risk is not standardized and included highly diverse metrics over different time horizons and for different categories of physical and transition risks. Since this report was published, more firms have emerged with new tools including Value-at-Risk, average annual loss, number of days of business interruption, and 0-100 scores that rate risk on proprietary “black box” scales.

Investment managers are struggling to figure out what they should do with all this new information and how to reconcile inconsistencies among the various providers.

What can be done? As with other new data markets, users should expect constant change and refinement as vendors and users interact with the data and each other.

The rapid growth of new firms has already led to a shakeout as some have been bought by larger companies and others have folded their operations. More importantly, investors need to understand that climate risk analysis at the property level is a relatively new approach—most of the government and academic-sponsored models are calibrated to measure climate risk across counties or regions.

Investors also need to understand that although vendors are providing specific point estimates, they are doing so because they perceive that is what building owners want. The most sophisticated climate risk models produced by universities and meteorological institutes are probabilistic, not deterministic. They produce a range of probable outcomes that can show “direction of travel,”, but not precise probabilities or specific loss estimates at the building level. Much is “lost in translation” when downscaling from these probabilistic sources of future climate conditions to specific point estimates, which are then put into new metrics like dollar value of losses or the percentage of a building’s value that is at risk.

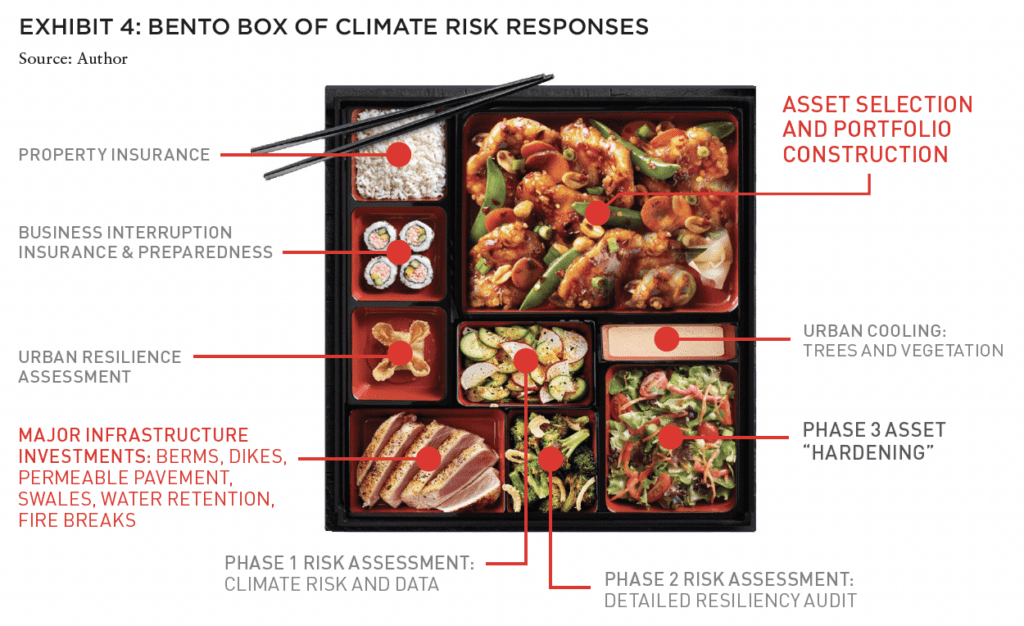

Similar to property owners’ experiences with environmental and engineering risks, broad-brush climate risk data should be treated as a Phase I filter that identifies when a more detailed Phase II or Phase III assessment of the specific risks of a micro-location and whether a specific property has been built to withstand the type of physical risks that are most likely.

In short, a whole “Bento Box” of approaches may be required by investors to prepare themselves and their portfolios for a future world where volatile weather becomes routine.

4) CLIMATE RISK HAS NOT YET BEEN FULLY PRICED. The links between climate risk, rents and values are not well-established. Investors and their investment committees do not yet have any “shortcut” methods for understanding what the risk premium should be for locations that are at higher risk for weather-related damage.

In the US, like most countries, the most desirable locations for real estate are precisely those places that are most at risk. Water views have a clear and measurable premium in most residential markets, but does the risk of coastal flooding? The uptick in the decades-long migration to the sunbelt during and after the COVID pandemic illustrates how markets may discount future climate risk costs at a higher rate – which more than offset the perceived flow of benefits of warmer weather, low taxes, and affordable cost of living that come along with life in Arizona, Florida, or Texas. This lack of a clear linkage between real estate with higher levels of climate risk and market metrics may still be the case in 2023, but this situation is likely to change over time as more volatile weather damage occurs and as insurance firms continue to raise premiums faster in at-risk zones.

What can be done? Efficient markets are amazingly good at taking an incredible amount of heterogeneous demand-side and supply-side data into account when determining prices. For all the reasons cited above, there are rational explanations why the present and future risks of climate risk are not yet fully priced. Over time, these inefficiencies in the real estate market will likely be overcome as evidence accumulates to show that climate risks are taken into account in pricing behavior.

A far-sighted investor should not take current pricing—either rents or values—as the future state of the market. By the year 2033, insurance markets are likely to be charging much higher premiums. Government assistance for disaster relief may be capped or eliminated for the highest-risk locations. Ten more years of volatile weather data combined with the concomitant property loss data will be hard to ignore. A prudent approach would be to pay close attention to research that sheds light on the circumstances where the linkages are already discernible.

Studies of the Miami office market conducted at the MIT Center for Real Estate found no rent discount for buildings with the highest risks of coastal flooding and wind damage. In fact, there was a slight premium because of the fantastic water views. Nevertheless, the analysis of comparable sales across 57 buildings showed that investors did put a slightly higher cap rate on waterfront Miami office towers.13 An analysis by CoreLogic of Miami home prices found significant discounting of homes in flood zones.14 A growing list of similar studies from around the world, show the pathways whereby markets start to price climate risks in real estate. The process is not instantaneous, and it may not adhere to the time horizon of short-term investors.

THE TRAGEDY OF THE HORIZON

One of the biggest challenges of climate risk is what Mark Carney, former Chairman of the Bank of England, called “tragedy of the horizon.” Climate change is measured in decades, well beyond the discounted cash flow modeling of most real estate valuations. Nobel-prize winning economist William Nordhaus wrote about the mismatch between the time horizons of markets, politicians, and popular opinion on the one hand, and the decadal trajectory of global warming and rising climate risk on the other.15

This mismatch can be bridged by raising the awareness of investment teams of what the future holds. This means doing the homework of studying what your property insurance teams are saying, paying close attention to changes in government policy, and finally paying close attention to market signals that look out beyond just the next five years.

Climate science is probabilistic, not point-specific. In the words of Martin and Weizmann, the authors of Climate Shock: “Climate change belongs to the rare category of situations where it is extraordinarily difficult to put meaningful bounds on the extent of planetary damage.” This difficulty should not prevent investors from educating themselves on the tools that are available now for assessing climate risk and for mitigating it through asset hardening or emergency preparedness planning.

Investing, like economics, is based on the principle that there are trade-offs in every decision. A decision to invest in a waterfront asset that appeals to tenants has validity. A complimentary decision to set aside capital expenses to cope with rising insurance costs, business interruption, and asset resilience is also a rational decision. Putting these two approaches side-by-side in a financial model is not impossible—in fact, it is likely to be the right approach. Translating future rising climate risks in 2040 into financial metrics in a ten-year cash flow model that starts in 2023 is a do-able and prudent exercise for an investor to undertake. Doing so, may mean that there does not have to be a “tragedy of the horizon” in a real estate portfolio.

—

ABOUT THE AUTHORS

Jacques Gordon is the retired Global Head of Research and Strategy for LaSalle Investment Management and remains a senior advisor to the firm. He is currently a lecturer and executive-in-residence at MIT.

The author would like to acknowledge the assistance of Yichun Fan, a doctoral student in urban economics at MIT, for providing several of the citations in this article

—

REVIEWER RESPONSE

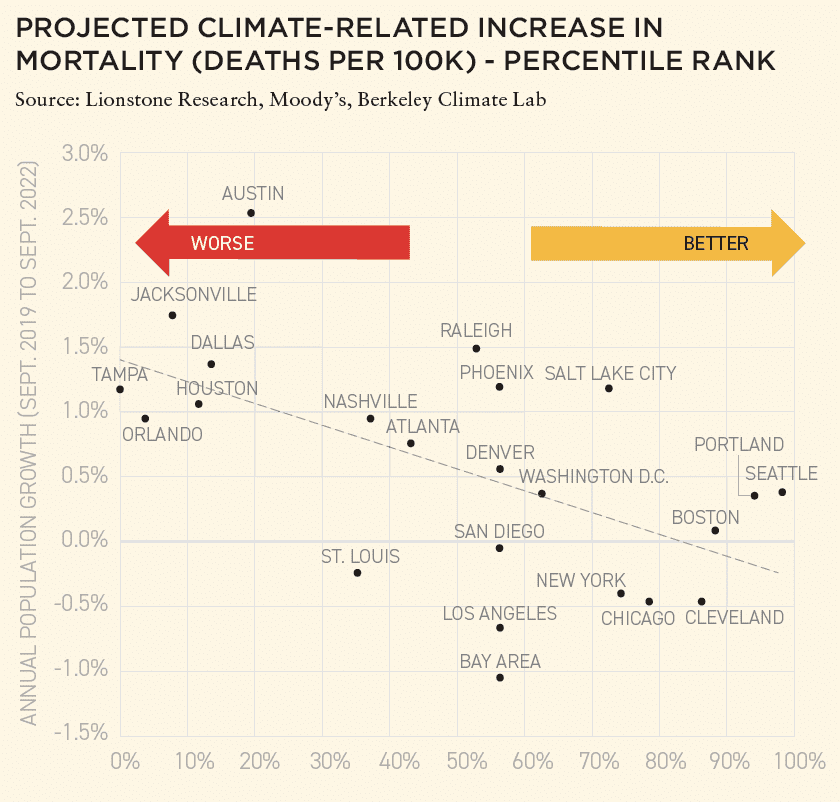

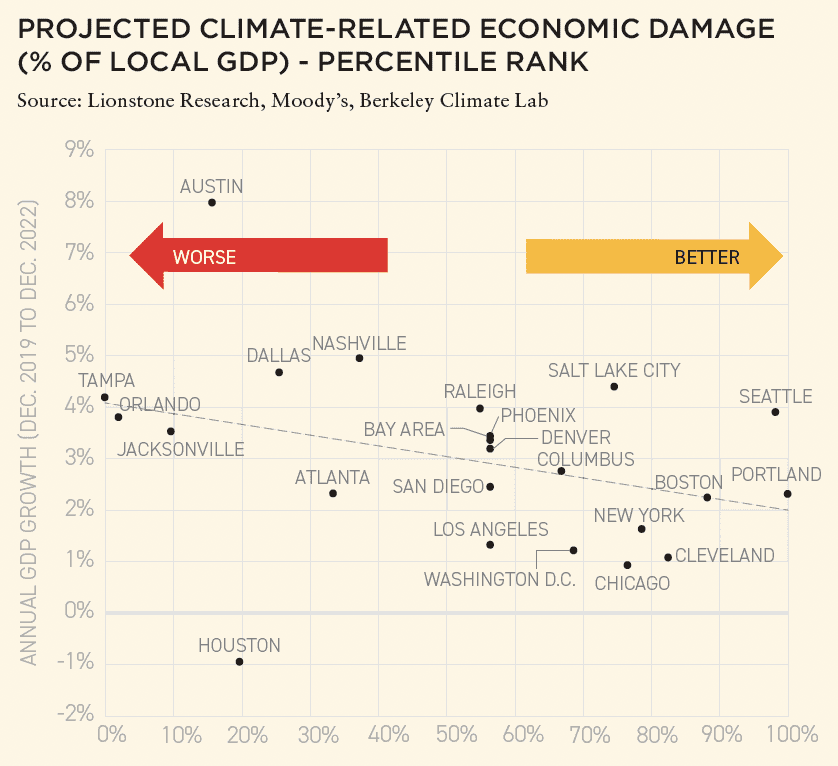

Americans can be puzzling people. Based on analytics from the Berkely Climate Lab, they appear to be moving to cities that present the highest risk of mortality from environmental change. Therefore, for real asset investment strategies dependent on population growth (which may be most real asset investment strategies), Jacques Gordon’s recommendation that investors manage environmental risk to support investment in poorly scoring geographies, rather than only investing in only well-scoring geographies, appears to be very good advice. Austin, Jacksonville, and Dallas posted solid population growth yet score near the bottom (further to the left) in terms of mortality risk over the long term. There are a few cities, such as Raleigh and Salt Lake City, which present less mortality risk with similarly solid population growth. However, the cities shown here with the lowest mortality risk, such as New York, Cleveland, and Chicago, show lower population growth as well.

In terms of a actual GDP growth versus estimates of climate risk to that GDP, tradeoffs may be similarly difficult. The metropolitan areas shown with the highest annual GDP growth, Austin, Dallas, and Nashville, all score below-average in projected climate-related economic damage risk.

Of course, future economic and population growth may be different than that experienced since the end of 2019 and well-scoring cities such as New York, Cleveland and Chicago may become growth leaders as well. Barring that outcome, Jacques’ bento box may be a fitting way for real assets investors to help balance near term investment and environmental goals.

– Hans Nordby

Head of Analytics and Research, Lionstone Investments

Member, Summit Journal Editorial Board

The views expressed are of the date given, may change as market or other conditions c hange, and may differ from views expressed by other Lionstone associates or affiliates. Actual investments or investment decisions made by Lionstone and its affiliates, whether for its own account on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Information provided by third parties is deemed to be reliable but may be derived using methodologies or techniques that are proprietary or specific to the third-party source. Lionstone is not affiliated with MIT.

NOTES

1. Climate scientists believe these are all “modern-era” records. Earth’s hottest periods occurred hundreds of millions of years before humans existed. NOAA estimates that the last time earth was as hot as now was 125,000 years ago. https://www.noaa.gov

2. JLL Global Research 2022, GHG emissions from property users in urban areas range from 60% to 80% of urban emissions. https://www.us.jll.com/en/trends-and-insights/research/decarbonizing-cities-and-real-estate

3. See Chaper 1, Climate Shock, Gernot Wagner and Martin Weitzman, Princeton University Press, 2015. Pre- and early industrial era CO2 concentrations were in the 260 to 280 ppm range.

4. https://www.climate.gov/news-features/understanding-climate/climate-change-atmospheric-carbon-dioxide

5. Ibid. Chapter 3.

6. Source: Marsh McClennan 2023.

7. A recent poll by the Robert Wood Foundation and the Chan School of Public Health at Harvard found that after a weather disaster hits, attitudes toward government regulation of carbon emissions changes significantly. https://www.hsph.harvard.edu/news/press-releases/poll-facing-extreme-weather-is-changing-americans-views-about-need-for-climate-change-action/ (In a twist on Ronald Reagan’s famous quip about the terrifying words: “I’m from the government, I am here to help”, it seems that most Americans are counting on weather disaster assistance from the government and from NGOs.)

8. https://rebuildbydesign.org

9. https://www.pewtrusts.org/en/research-and-analysis/articles/2021/08/27/how-government-can-address-growing-disaster-costs

10. https://rebuildbydesign.org/atlas-of-disaster/

11. Through supranational organizations like the Resilient Cities Network founded by the Rockefeller Foundation. https://resilientcitiesnetwork.org/

12. “How to Choose, Use, and Better Understand Climate Risk Analytics” ULI Research Report September 2022

13. Paper presented at the MIT CRE Climate Change and Real Estate conference December 2022 by Prof. William Wheaton.

14. https://www.corelogic.com/intelligence/the-impact-of-flood-risk-on-property-values-a-case-study-in-miami/

15. William Nordhaus, The Climate Casino: Risk, Uncertainty, and Economics for a Warming World, 2013. Yale University Press.

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY UNDERWRITTEN BY

For more than 20 years, Yardi has developed real estate investment management software that helps managers of global assets valued at trillions of dollars make informed investment decisions. Yardi Investment Suite clients include many of the world’s premier investment management funds, start-ups and partnerships of all types and sizes.

Real estate investments grow on Yardi. That’s because the Yardi Investment Suite automates complex investment management processes and provides full transparency, from the investor to the asset. Through interactive dashboards, investors can view documents and have access to reports and metrics. Collaboration is easy when your advisor or accountant is given access to view your accounts, reducing the need for emailing sensitive information.

The Yardi Investment Suite leads the real estate industry through innovation and value with fully integrated investment management, property management and accounting functionality. Fund managers and their customers can manage assets with superior efficiency and ease. Learn more.