As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

In a year of poor performance in some commercial real estate sectors, investors and developers are eyeing up a move into life sciences, but do the risks outweigh the potential benefits?

The life sciences industry consists of companies operating in pharmaceuticals, biotechnology, medical devices, biomedical technologies, nutraceuticals, cosmeceuticals, and food processing. Recent growth, partially driven by the pandemic, has centered on the health and medical side of the industry, including businesses dedicated to developing, producing, and commercializing innovative treatments, diagnostic tools, equipment, and software to improve and prolong lives.

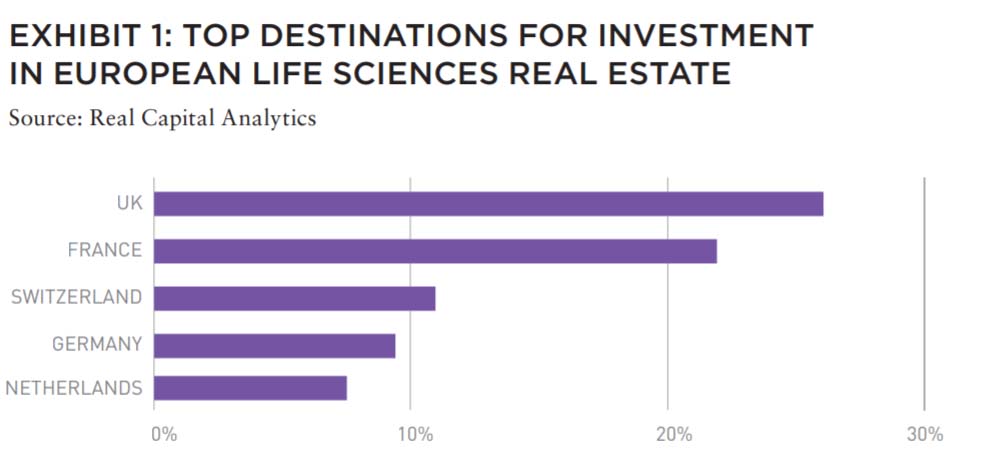

The pandemic highlighted the resilience of life sciences compared with other commercial real estate sectors, especially because much of the activity in the industry, including lab work, cannot be done from home. At the same time, the pandemic and the rush for vaccines highlighted the benefits of self-sufficiency for localized medical manufacturing and distribution. This has led to changes in government policy and increases in public and private funding for the sector (see Exhibit 1).

However, the sector has proven resilient also based on other underlying trends not related to the pandemic, including aging populations, the increased volume of lifestyle diseases, such as diabetes, and rapid technological innovation. In that sense, the pandemic has ultimately acted as a catalyst for growth in the sector, rather than a cause.

As a result, investors and developers beginning to move into life sciences must exercise caution, because real estate in the space requires highly specialized skills that don’t always come from traditional real estate talent pipelines.

We spoke to several life sciences real estate veterans in the US and Europe to get their views on the skills needed to lead real estate in this sector.

INTEREST IN LIFE SCIENCES REAL ESTATE IS AT AN ALL-TIME HIGH

Life sciences deals reached a record 16.4% of total office and flex transactions, according to a January 2021 report from New York-based advisory firm Newmark.1 In the largest life science hubs in the US, the amount of real estate dedicated to the sector has grown to around 40 million SF in the Greater Boston area, some 30 million SF in San Francisco, and around 20 million SF in San Diego.2

Based on the scale of the sector, Ronan Furlong, Head of the DCU Alpha innovation campus in Dublin, Ireland, and private consultant for scitech and life science real estate investors and developers, says “investors should be careful deploying capital through ‘vanilla developers’ who lack life sciences specialism.

To begin with, life sciences firms need more than just office space. They need wet and dry labs—dedicated research space and manufacturing facilities that are mission-critical to the development and production of new therapies and technologies.” Andrew Blevins from Liberty Property Trust, a Prologis company, says that the key considerations for building a life sciences ecosystem include “amenities, lease flexibility, specification, and research support infrastructure.”

Furlong adds that buildings in life sciences “need to be constructed very differently. Building services, engineering, floor loading, circulation, deliveries, floor to ceiling heights—all of these are different and more costly than for office space.”

Further, life sciences businesses thrive on collaboration and access to top talent. “There is absolutely a unique skill in building a successful ecosystem, so you can’t apply standard development models to life sciences,” Furlong says. “A standard developer or private equity investor will not understand how to create an ecosystem. This is important because, to make the product attractive, you need to create a community with the right people. The upshot is that the landlord or developer needs to bolt on universities, research centers, hospital trusts, and to be in tune with the commercial participants. Then they need to package all of that into an environment with lots of attractive amenities and service provision.”

In other words, beyond building specs and amenities, firms look for locations where they can cluster together in proximity to world-class research universities and medical institutions, highly educated talent, and venturebacked startups. Hence the popularity of well-known life sciences hubs in Cambridge, Massachusetts; Research Triangle Park in North Carolina; or Cambridge and Oxford, England.

As well as requiring unique facilities, support services, and locations, investments in life science assets have a much longer timeline than other assets, and therefore require more patience from the investor.

“In the UK, a lot of the opportunities to own or develop life science assets are owned by the universities, who are also a key player in the life science ecosystem, as many of the start-ups in this sector emanate from these same world-class medical universities. As such, developing relationships that focus on a long-term alignment of interest is important to unlocking these opportunities,” says Abby Shapiro, Head of Offices, Retail and Life Sciences, Europe, at Oxford Properties. “We are a long-term investor who understands the value of creating sustainable communities through its real estate, which we believe will align well with the university’s ambitions for this sector.”

Investors also need to commit a lot of capital because they need a portfolio to cater for different sizes of businesses, some of which may be lossmaking for years before they experience growth.

THE EARLY MOVERS HAVE A COMPETITIVE ADVANTAGE

Several of our US-based contacts told us that industry connectivity is crucial for success in the sector. Due to the highly technical nature of the design and development process for life science properties, landlords need to know the right architects, contractors, engineers, property managers, and service providers.

Real estate firms and their talent must demonstrate an ability to deliver infrastructure and services to the highly specialized technical specification their prospective tenants expect. The fact that life sciences used to be more of a niche sector within alternative real estate before becoming the recognized stand-alone asset class it is today means that the larger players and early movers such as Alexandria, BioMed, and Healthpeak have had a significant competitive advantage.

These firms have already spent lots of time or money—or both— building up the networks, talent, and skills to lead in the sector. For example, Alexandria entered the market as a specialist in 1994 and now owns more than 40 million SF of life sciences real estate, making it the largest company in the sector. The company also secured a twelve-year lease with COVID vaccine maker Moderna. This kind of size, track record, and credibility are hard to replicate. As the market continues to grow, new entrants will need to bring in specialists or develop expertise in order to become and remain competitive.

LANDLORDS ALSO NEED TO UNDERSTAND THE LIFE SCIENCES MARKET

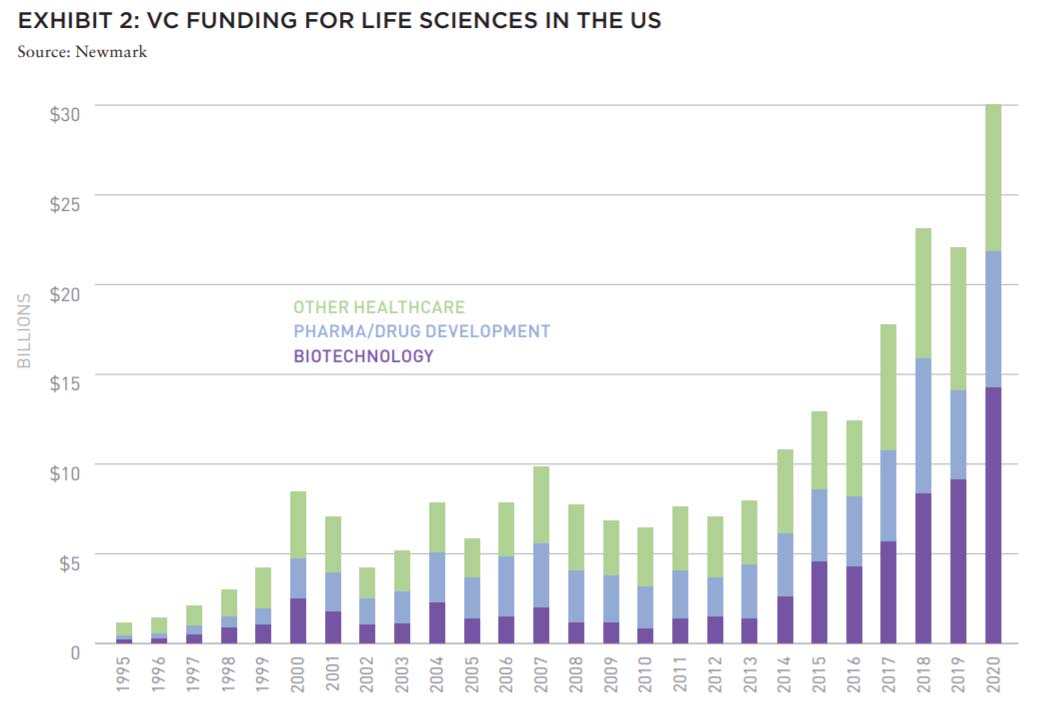

Although record amounts of venture capital (VC) funding have been pouring into life sciences in recent years (Exhibit 2) this is no guarantee of success for landlords or developers in the space. The majority of firms are small, and they represent wildly varying levels of credit risk. As in the VC space, the failure rate is high.

“You need to really understand the products they are developing to be successful,” says Thomas Renn, Managing Director at Bruntwood SciTech, which is based in the UK.

Several of our US contacts agreed, saying that understanding the science and technology helps to assess its market viability and potentially mitigate any concerns about credit quality.

Ronan Furlong adds: “You need to treat this like any early-stage investment and offer flexibility—perhaps even long rent-free periods. It’s worth it in the long run, because those tenants who do scale significantly could end up being a one-million-square-foot tenant very quickly.”

While some developers and landlords talk about the need to act like VC investors, Alexandria Real Estate Equities (ARE) actually is one such investor. As well as being the largest owneroperator of life sciences real estate in the US, Alexandria runs its own specialist strategic VC platform that invests in promising innovative companies across a wide range of technologies and sciences. According to Crunchbase, Alexandria’s notable VC investments include Moderna and Vera Therapeutics. The firm was also an early investor in Corixa Corp, a biopharma firm based in Seattle that was later acquired by GlaxoSmithKline. As of June 30, 2020, ARE had a carrying value of more than US$1.3 billion in their venture portfolio, across companies in the fields of immunology, neuroscience, gene therapy, drug discovery, and synthetic biology.3

PRIME ECOSYSTEM LOCATIONS ARE RUNNING OUT OF SPACE

A major challenge now for life sciences developers is that purpose-built supply is limited, even in top markets such as Cambridge and San Francisco, leading to more redevelopment and conversion activity, which is more expensive. Although US developers such as Breakthrough Properties and IQHQ are now expanding into Europe, markets there face a similar challenge of reaching capacity in hotspots such as Oxford, Cambridge, London, Zurich, Amsterdam, and others.

“Because there are very limited greenfield sites available in projected key life science locations in London, we also expect the focus to shift to conversions of existing properties to meet future needs,” confirms Abby Shapiro. Furthermore, “with an increased focus on ESG requirements of both investors and tenants, there is a strong argument for focusing on repurposing existing buildings to reduce the higher carbon footprint associated with demolition and rebuilding.”

While Cambridge, San Francisco, and San Diego remain the dominant life sciences ecosystems, other areas such as Seattle, Research Triangle, Maryland, and Philadelphia are growing. There are also a handful of emerging markets that are experiencing strong tailwinds and have potential for significant growth.

These markets have similar attributes to the dominant ecosystems. They have access to STEM talent, good universities, and hospitals. They’re also experiencing job and wage growth. According to JLL, cities such as Charlotte, Seattle, Denver, Austin, and Nashville could be poised to become significant life science ecosystems in the years ahead.4

SPECIALIST KNOWLEDGE AND TALENT ARE VITAL FOR SUCCESS IN LIFE SCIENCES REAL ESTATE

In summary, a strong case exists for investment in life sciences real estate, but success in this space will require specialist knowledge and technical skills. These include the ability to develop technical facilities such as laboratories, an understanding of the life sciences sector itself, experience with the unique needs of life sciences tenants, and the need to develop extensive networks across universities and healthcare organizations.

The property advisory industry, particularly in Europe, needs to recruit more specialist knowledge to be able to effectively support the growth in the sector. Given the immaturity of the market in Europe, there is reportedly a lack of specialist knowledge and experience in the mainstream advisory firms. In a highly competitive market, recruitment is one of the biggest challenges for both the advisors and client-side organizations.

Although the US life sciences sector is far more mature than Europe, many of the same constraints exist on both sides of the Atlantic—principally, the need for deep sector experience and knowledge. At a time when many office developers and landlords are looking to enter the market, attracting the right talent will be crucial to success.

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

—

ABOUT THE AUTHOR

Max Shepherd is Director Global Real Assets for Sheffield Haworth, London, and Jannah Babasa is Senior Associate Global Real Assets, Sheffield Haworth, New York. Sheffield Haworth provides highly tailored executive search and talent advisory services to help financial services companies find, attract, and retain talent.

—

NOTES

1. “2020 Year-End: Life Science National Overview & Top Market Clusters.” January 2021. Newmark. Accessed June 24, 2021. ngkf.com/storage-nmrk/uploads/fields/1-column-with-sidebar-links/Newmark_LifeSciences-YearEnd2020_FINAL-2.pdf

2. “2020 Life Sciences.”Newmark Knight Frank. Accessed June 22, 2021. ngkf.com/storage/uploads/documents/NKFResearch_LifeSciences_June2020.pdf)

3. “Biopharma Investor for Third Consecutive Year.” September 4, 2020. Biospace. Accessed June 22, 2021. biospace.com/article/releases/alexandria-ventureinvestments-recognized-as-1-most-active-biopharma-investor-for-third-consecutive-year/

4. “Life Sciences Emerging Markets Index.” JLL. Accessed June 22, 2021.us.jll.com/en/trends-and-insights/research/life-sciences-emerging-markets-index