Some investors tend to think that diversification comes down to merely investing in different asset classes, but an effectively diverse portfolio will include assets with low and preferably negative correlation—not always easy to find in today’s global economy.

Harry Markowitz, Nobel Prize laureate and creator of the efficient frontier theory, changed the fundamental view of portfolio allocation. The theories of the recently deceased Markowitz are being practiced by leading institutional and other professional investment portfolios, positing diversification as a fundamental risk management strategy.

The novelty in Markowitz’s dissertation was that the risk of a portfolio was found to depend more on component stocks’ correlation, rather than the prospects of those individual stocks.1 The dissertation originally examined the stock market, but its principals apply to asset allocation in general and the allocation within each asset class—a concept otherwise known as the modern portfolio theory.2

Although there is no argument that diversification is a recommended risk mitigation strategy, some investors tend to think that this strategy comes down to merely investing in different asset classes. While any diversification practice is more recommended than none, some ways to implement this strategy are more efficient than others. An effectively diverse portfolio will include assets with low and preferably negative correlation, which is not always easy to find in today’s global economy.

Due to high correlation between publicly traded assets, the diversification effect of an investment portfolio holding these assets is greatly reduced and even eliminated. Therefore, an investor should strive to have an investment portfolio with as many diversification parameters as possible. A properly diversified portfolio should include diversification between different asset classes, and optimal diversification within each of the asset classes.

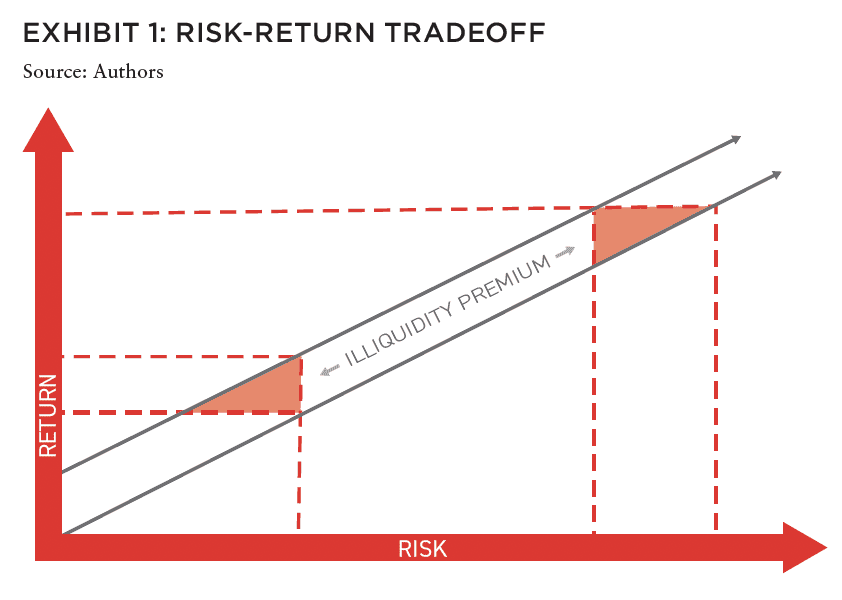

PATIENT CAPITAL IS TRADING SOME OF THE RISK WITH ILLIQUIDITY

Risk is created by market uncertainty and is calculated by the potential negative influence of unknown factors on an investment, multiplied by its probability. The return investors expect to receive from an investment opportunity is a direct expression of the degree of risk attributed to the investment. In private equity investments, one of the main risk factors is illiquidity and its 100% probability is known in advance, thus turning it into a characteristic of an investment, rather than a risk.

An investor with the privilege to forgo liquidity for a limited period of time (as underwritten but may change with the market circumstances) is therefore rewarded with the illiquidity premium, enabling investments to achieve higher returns at similar risk levels, or similar returns at lower risk levels.

A main component of the illiquidity premium is that due to its nature as patient capital (compared to publicly traded assets), it is not as affected by market sentiment, allowing managers to practice their skills in order to add value to the asset and determine the optimal timing to sell it. In real estate, the value of an asset is represented in the actual price it is sold for, not market predictions or analysts’ speculations.

When it comes to liquidity, Warren Buffet, one of the most successful investors of all times has said: “If you are not willing to own a stock for ten years, don’t even think about owning it for ten minutes,” advising investors “not to watch the market too closely,” or in other words: even when you have liquidity, use it wisely.

BARRIERS TO PROPER DIVERSIFICATION

Markowitz said: “Diversification is the only free lunch in finance.”

In other words, diversification is known to be an effective risk management strategy, requiring access to diverse markets and the ability to fund and oversee a variety of portfolio investments.

One barrier to proper diversification is the home bias syndrome: investors tend to concentrate most of their investments in their country of origin. A survey conducted by the International Monetary Fund about this widespread phenomenon3 found quite predictable reasons for it: distance and information gaps; loyalty to the local market; exchange rates and regulatory and bureaucratic limitations.

Another barrier to proper diversification is the high financial bar to participate in some investments, which requires investors to invest substantial funds in order to practice an effective diversification strategy.

The way to overcome these two barriers and maintain a professionally diverse portfolio is investing through a global fund alongside leading managers, providing broad effective diversification.

EFFECTIVE DIVERSIFICATION

The level of diversification of investment portfolios is determined by the number of parameters that differ from one portfolio investment to another. The more parameters defer, the larger the diversification is: buying two assets of the same sector, geography and management shall decrease asset-specific risks, but not sectorial, managerial or geographic-related risks. Practicing real estate for almost three decades, we find that we are more in the people business than in the real estate business, and that investing with trustworthy investment managers is just as important as the asset itself.

Since most real estate professionals have a specific expertise, sectorial strategic and geographic focus, diversification between global real estate managers, also has inherent geographic, strategic, and sectorial diversification, as well as currency diversification at times.

Low correlation between assets is amplified with the number of factors not shared by them. Investments underlined by a logistics-focused manager in the UK shall have very little in common with a Connecticut-based multifamily manager. The amplification is exponential rather than linear, or in other words: multi-dimensional.

Investing in a global managerial-diversified portfolio is likely to achieve multi-dimensional diversification, and with the proper due diligence process assuring top-quartile quality managers, it serves as the private equity real estate equivalent to investing in the tradable market using skillful experienced stock pickers, with the ability to mitigate risk even better than index funds.

Despite uncertainty, the forthcoming years (2023-2024) are expected to be interesting and provide extraordinary opportunities for patient capital, professionally managed by trustworthy managers.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #13

Benjamin van Loon | AFIRE

OFFICE TROUBLES: FINANCIAL RISKS AND INVESTING OPPORTUNITIES IN US CRE

Dr Alexis Crow | PwC + Byron Carlock

THE UNDERPERFORMANCE PARADOX: WHY INDIVIDUAL INVESTORS FALL BEHIND DESPITE BUYING LOW

Ron Bekkerman | Cherre + Donal Ward | Tenney 101

CLIMATE THREAT: EXTREME WEATHER IS THE NEW NORMAL FOR REAL ESTATE

Jacques Gordon, PhD | MIT

CLIMATE OPPORTUNITY AWAITS: HOW REAL ESTATE CAN INVEST IN CLIMATE ADAPTATION

Michael Ferrari, PhD and Parag Khanna, PhD | Climate Alpha

PREMIUM PRICE TAGS: INSURABILITY THROUGH PROPERTY RESILIENCE DATA

Bob Geiger | Partner Engineering & Science

REAL ESTATE WEB3: THE EMPEROR’S NEW CLOTHES OR THE NEXT BIG THING?

Zhengzheng Tan, Alice Guo, and Naveem Arunachalam | MIT

ADAPTIVE TO REUSE: COULD BUILDING CONVERSIONS BE DIFFICULT, EXPENSIVE . . . AND STILL PROFITABLE?

Josh Benaim | Aria

RENOVATE, REBRAND, REPOSITION: ADDING VALUE TO MULTIFAMILY THROUGH REVITALIZATION

Robert Kilroy, CFA | The Dermot Company + Will McIntosh, PhD | Affinius Capital

REDEFINING THE PROGRAM: A CONVERSATION WITH ARCHITECT DAVID THEODORE

Peter Grey-Wolf | Wealthcap + David Theodore | McGill University

SENIOR HOUSING UPDATE: EMERGING OPPORTUNITIES THROUGH DEMOGRAPHIC TAILWINDS AND DIMINISHING SUPPLY OUTLOOK

Robb Chapin, Jack Robinson, Andrew Ahmadi, and Morgan Zollinger | Bridge Investment Group

SENIOR HOUSING UPDATE: UNPRECEDENTED DEMOGRAPHIC ACCELERATION MAY DRIVE STRONG OPERATING FUNDAMENTALS AMID ECONOMIC SLOWDOWN

Tom Errath | Harrison Street

HOLIDAY FROM HISTORY: REASONS FOR US OPTIMISM IN A CHANGING GLOBAL ENVIRONMENT

Charlie Smith | Newmark

CRADLE TO CRADLE: AN ALLOCATOR’S VIEW ON IMPLEMENTING ESG INITIATIVES

Christopher Muoio and Katie Cappola | Madison International Realty

FREE LUNCH: MULTI-DIMENSIONAL DIVERSIFICATION IS A FULL-COURSE FREE MEAL

Elchanan Rosenheim and Tali Hadari | Profimex

CAMPAIGN MESSAGING: CFIUS, AFIDA, AND EXPANDING FEDERAL AND STATE RESTRICTIONS ON FOREIGN INVESTMENT IN US REAL ESTATE

Caren Street, John Thoms, and Anya Ram | Squire Patton Boggs

—

ABOUT THE AUTHORS

Elchanan (El) Rosenheim is Founder and CEO of Profimex and Tali Hadari is Head of Legal Department and Manager of Profimex’ in-house funds. Profimex makes global equity investments alongside local strategic partners.

—

NOTES

1. Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77–91.

2. Keith Ambachtsheer. (2005). Beyond Portfolio Theory: The Next Frontier. Financial Analysts Journal, 61(1), 29–33.

3. Sie Ting Lau, Lilian Ng, Bohui Zhang, The world price of home bias, Journal of Financial Economics, Volume 97, Issue 2, 2010, Pages 191-217.

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY UNDERWRITTEN BY

For more than 20 years, Yardi has developed real estate investment management software that helps managers of global assets valued at trillions of dollars make informed investment decisions. Yardi Investment Suite clients include many of the world’s premier investment management funds, start-ups and partnerships of all types and sizes.

Real estate investments grow on Yardi. That’s because the Yardi Investment Suite automates complex investment management processes and provides full transparency, from the investor to the asset. Through interactive dashboards, investors can view documents and have access to reports and metrics. Collaboration is easy when your advisor or accountant is given access to view your accounts, reducing the need for emailing sensitive information.

The Yardi Investment Suite leads the real estate industry through innovation and value with fully integrated investment management, property management and accounting functionality. Fund managers and their customers can manage assets with superior efficiency and ease. Learn more.