The leading political and economic position of the US is currently under threat by global competition, but key trends in demography and innovation could change the equation.

The US has held a favored global political and economic position for the past 30 years—but international competition is getting tougher and threatening this status. Changing political and economic expectations can provoke uncertainties about a path forward and how the US can thrive.

Yet, if we take a moment to step back and examine long-term trends, there is cause for optimism around the US economy and its place in the world. This article looks at three key areas that underline US economic optimism: (1) demographics, (2) innovation trends, and (3) the relative position of the US and global competition.

DEMOGRAPHICS

Unlike most other advanced economies, the US population will continue to grow for years to come. The US government projects that today’s population of 336 million will increase by 11% in the next 30 years, reaching 373 million people.1 In contrast to past decades, this growth will largely come from immigration rather than domestic birth rates, especially as millennials age out of their peak child-bearing years in the 2030s.

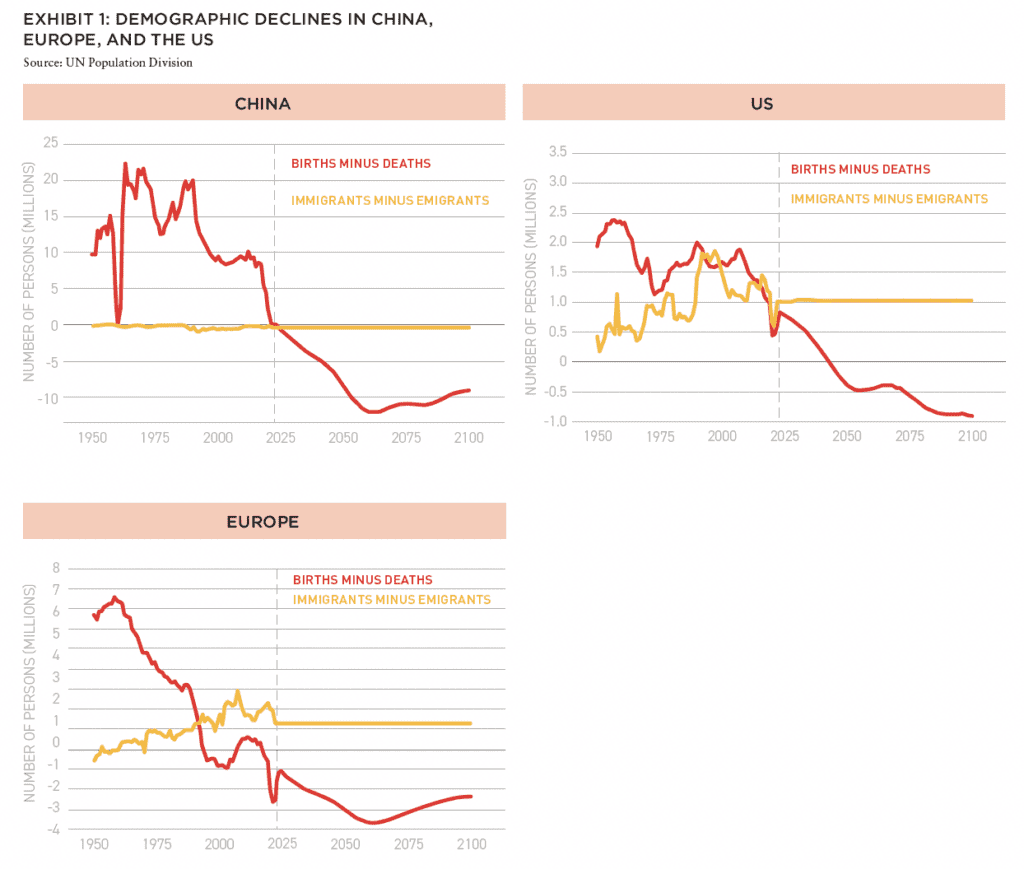

The US has continued to accept a steady stream of new residents in recent years which, in turn, has added economic benefits. Immigrant populations are more likely to start new businesses than native-born Americans.2 They are more mobile, providing the ability to move where labor is most needed. They also have a higher rate of labor force participation, amplified by the fact that nearly 80% of the foreign-born population is of working age.3 The US’ projected population growth is even more pronounced when compared to other developed economies or geopolitical competitors. China possesses a larger outright population at over one billion people, but this size is reaching a plateau and likely decreasing.4 Other G7 and EU economies are facing more dramatic population declines, especially against US growth, as detailed in Exhibit 1.

US labor participation is also recovering from the pandemic, as the prime-age labor force (ages 25-54) is back at pre-pandemic levels.5 The speed of the recovery by the prime-age labor force is remarkable, as it happened within three years of the pandemic shock. In contrast, it took over ten years after the Great Recession for a similar recovery. And while the overall labor pool size is reduced from its 2020 size, largely driven by older workers not returning to the workforce post-pandemic, other bright spots for potential growth include historically high labor participation rates by women and African Americans, an encouraging trend that should be monitored.6

INNOVATION TRENDS

Innovation is a major contributor to economic growth and development.7 As the world increasingly leans into the fourth industrial revolution, innovation will continue to be a driver of economic growth and investment attraction. Global competition around innovation is high, as both economic and security reasons compel countries to deliver new platforms and solutions.

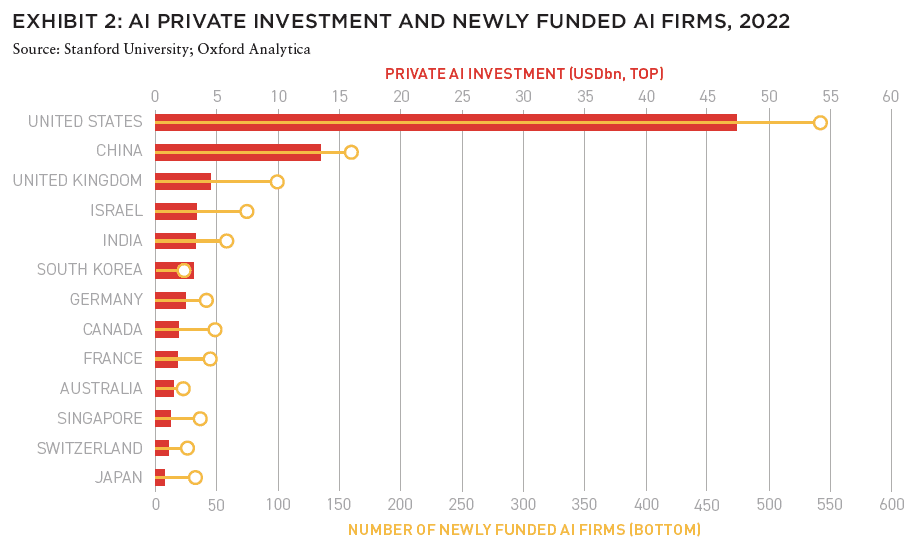

Currently, AI is leading the contest for innovation, and the early indications support a positive view for the US. Rather than being led by government policy, AI innovation is particularly driven by the private sector. Recent private investment placed into US-based AI firms far outweighs those placed in China or elsewhere, as do the total number of AI-focused companies founded (Exhibit 2). Given China’s state-led approach to economic growth, it may be difficult for China to boost innovation as it requires relinquishing a level of state control.8

That is not to say that government assistance is not worthwhile. China’s policy actions have, after all, helped the country lead in electric vehicle manufacturing. Yet, even here the recent US policymaking response shows promise. The Inflation Reduction Act, Build Back Better Act, CHIPS and Science Act all explicitly target innovation and economic competitiveness and have led to billions of dollars in new investment.9

A more active industrial policy from the US government is putting significant financial resources towards boosting innovation. Rising domestic manufacturing numbers and investment flows may prove durable and popular enough to form a long-term trend that can outlive partisan rivalries. Indeed, greater government financial support for scientific R&D is a bipartisan concern, providing additional momentum.10

Taken together, significant private and public investment into innovation support continued strength for the next wave of industrial growth. The US already enjoys advantages as the home of many world-leading technology companies. With high barriers to entry for digital platforms and data-driven segments at this stage, these leading firms may add to long-term advantages for the US.11

RELATIVE GLOBAL POSITION

International competition is rising. China’s impressive growth continues to pace several sectors. Other countries, be they traditional powers or what some are labeling as “swing states,” use their financial influence, commodity exports, geopolitical positioning, or other strengths to dictate terms more robustly than in the past.12 Yet, despite the recent rise of various powers, the US retains advantages for this age of competitiveness.

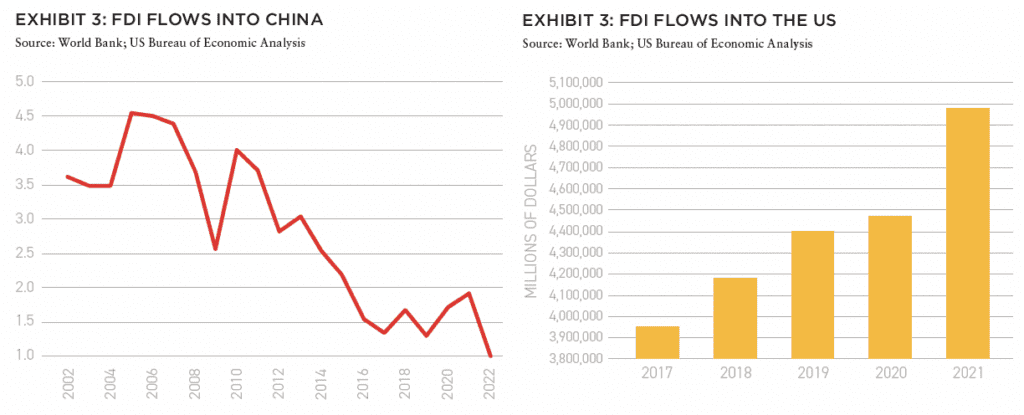

While China’s economic strengths are many, concerns remain with the business environment. Rising state interference with foreign businesses, opaque policymaking and a non-convertible currency all present challenges. A recent EU report highlights the outflow of foreign investment precisely because of the current political environment in China.13 While Hong Kong offers exceptions to some of these issues, the Chinese mainland faces structural difficulties as a course correct appears unlikely in the near term. The US, on the other hand, has a more open business environment, with a relatively transparent policymaking process and a highly convertible currency. Foreign direct investment (FDI) numbers reflect the success of this model. As Exhibit 3 shows, foreign investment into China, as a percentage of GDP, is slowing to levels not seen for years.14 Meanwhile, in 2021 the International Monetary Fund showed inward FDI to the US reaching over $500 billion, placing it in first place, and higher than China’s $360 billion.15 As Newmark’s research highlights, this is a trend that pre-dates the industrial policy legislation of 2022.16

Looking beyond China, other powers bring unique value-adds to today’s competitive environment. The EU, for example, has significant financial influence and a powerful single market with more consumers than the US. Ambitious “swing states” also carry their own points of leverage. For example, Turkey is an active geopolitical player with geographic importance, Indonesia has a large population and large rare earth deposits, and Brazil is both South America’s largest power and a major commodity supplier.

And yet, the total advantages that the US brings to bear is singular in a way that none of these locales can match across the board. The United States is a key player in every aspect where swing states are active, be it as a buyer or supplier of goods, or a leader in the geopolitical space. The combination of these positions maintains the country’s considerable influence, provided the US unites them with defined focus (as we see now with strategic supply chains around battery materials). Even when comparing against the EU, which shares similarities in economic scale and makeup, US industrial policy actions provide added incentive in an area where the EU historically had more institutional focus.

While the EU has had stricter environmental policies than the US for some time, recent US policy moves are proving competitive. The CHIPS and Science Act, for example, is more lucrative and reduces more bureaucratic hurdles when compared to the EU’s incentives. It is worth noting that even where the US is individually at a disadvantage, it can marshal consensus from a range of both allies and more transaction-based states. The US’ financial, political, military and cultural significance lend it a unique weight that, while not the unipolar power it was 20 years ago, still gives it a preeminent position.

GOING ON HOLIDAY

HR McMaster, a former US lieutenant general and national security advisor, describes the post-Cold War years as a “holiday from history.”17 While those in the US may perceive a comparative decline over the past 30 years, the country is only reverting to the historical norm of heightened competition rather than experiencing fundamental decline. And it is in this environment that US advantages in demographics, innovation and relative global position provide optimism for success.

These three factors are not the full, complex picture, but they remain core trends that favor growth and investment, particularly as they interplay among each other. For example, nearly two-thirds of AI companies in the US are founded or co-founded by immigrants.18 This advantage can boost US attractiveness as it looks to lead the next wave in technological growth – and resulting investment.

While the make-up of the coming economy may look different from the past, investors would be wise to consider the underlying, competitive advantages presented by US in this age of rising competition.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #13

Benjamin van Loon | AFIRE

OFFICE TROUBLES: FINANCIAL RISKS AND INVESTING OPPORTUNITIES IN US CRE

Dr Alexis Crow | PwC + Byron Carlock

THE UNDERPERFORMANCE PARADOX: WHY INDIVIDUAL INVESTORS FALL BEHIND DESPITE BUYING LOW

Ron Bekkerman | Cherre + Donal Ward | Tenney 101

CLIMATE THREAT: EXTREME WEATHER IS THE NEW NORMAL FOR REAL ESTATE

Jacques Gordon, PhD | MIT

CLIMATE OPPORTUNITY AWAITS: HOW REAL ESTATE CAN INVEST IN CLIMATE ADAPTATION

Michael Ferrari, PhD and Parag Khanna, PhD | Climate Alpha

PREMIUM PRICE TAGS: INSURABILITY THROUGH PROPERTY RESILIENCE DATA

Bob Geiger | Partner Engineering & Science

REAL ESTATE WEB3: THE EMPEROR’S NEW CLOTHES OR THE NEXT BIG THING?

Zhengzheng Tan, Alice Guo, and Naveem Arunachalam | MIT

ADAPTIVE TO REUSE: COULD BUILDING CONVERSIONS BE DIFFICULT, EXPENSIVE . . . AND STILL PROFITABLE?

Josh Benaim | Aria

RENOVATE, REBRAND, REPOSITION: ADDING VALUE TO MULTIFAMILY THROUGH REVITALIZATION

Robert Kilroy, CFA | The Dermot Company + Will McIntosh, PhD | Affinius Capital

REDEFINING THE PROGRAM: A CONVERSATION WITH ARCHITECT DAVID THEODORE

Peter Grey-Wolf | Wealthcap + David Theodore | McGill University

SENIOR HOUSING UPDATE: EMERGING OPPORTUNITIES THROUGH DEMOGRAPHIC TAILWINDS AND DIMINISHING SUPPLY OUTLOOK

Robb Chapin, Jack Robinson, Andrew Ahmadi, and Morgan Zollinger | Bridge Investment Group

SENIOR HOUSING UPDATE: UNPRECEDENTED DEMOGRAPHIC ACCELERATION MAY DRIVE STRONG OPERATING FUNDAMENTALS AMID ECONOMIC SLOWDOWN

Tom Errath | Harrison Street

HOLIDAY FROM HISTORY: REASONS FOR US OPTIMISM IN A CHANGING GLOBAL ENVIRONMENT

Charlie Smith | Newmark

CRADLE TO CRADLE: AN ALLOCATOR’S VIEW ON IMPLEMENTING ESG INITIATIVES

Christopher Muoio and Katie Cappola | Madison International Realty

FREE LUNCH: MULTI-DIMENSIONAL DIVERSIFICATION IS A FULL-COURSE FREE MEAL

Elchanan Rosenheim and Tali Hadari | Profimex

CAMPAIGN MESSAGING: CFIUS, AFIDA, AND EXPANDING FEDERAL AND STATE RESTRICTIONS ON FOREIGN INVESTMENT IN US REAL ESTATE

Caren Street, John Thoms, and Anya Ram | Squire Patton Boggs

—

REVIEWER RESPONSE

While I do not disagree with the author’s conclusions, I would quibble with the opening premise that international competition is getting tougher and threatening the US’ favored global political and economic position. My personal view is that there are larger forces at work, impacting the globalization and integration that we’ve enjoyed the last 30 years. Today there is a new world of economic nationalism and competition for resources that is shifting the geo-political and investment landscape. The author’s conclusions nonetheless hold true – that the US is indeed well positioned, especially vis a vis demographics and innovation. The last point is particularly important as innovation fosters growth and investment across sectors, which we are seeing now with the impact of AI. Overall, the article is well written and provides a nice investment case for the US versus other geographies / countries.

– Tommy Brown

Partner, LGT Capital Partners

Member, Summit Journal Editorial Board

—

ABOUT THE AUTHOR

Charlie Smith serves as a Managing Director, Geopolitical Strategy in Newmark Global Consulting.

—

NOTES

1. Congressional Budget Office. (2023, January 26). The Demographic Outlook: 2023 to 2053. Retrieved from https://www.cbo.gov/publication/58912

2. Pierre Azoulay, B. F. (2020, October 5). KelloggInsight. Retrieved from Kellogg School of Management at Northwestern University: https://insight.kellogg.northwestern.edu/article/immigrants-to-the-u-s-create-more-jobs-than-they-take

3. Arloc Sherman, D. T. (2019, August 15). Immigrants Contribute Greatly to U.S. Economy, Despite Administration’s “Public Charge” Rule Rationale. Retrieved from Center on Budget and Policy Priorities: https://www.cbpp.org/research/poverty-and-inequality/immigrants-contribute-greatly-to-us-economy-despite-administrations

4. Peng, X. (2022, July 26). China’s population is about to shrink for the first time since the great famine struck 60 years ago. Here’s what that means for the world. Retrieved from World Economic Forum: https://www.weforum.org/agenda/2022/07/china-population-shrink-60-years-world/

5. The White House. (2023, April 17). The Labor Supply Rebound from the Pandemic. Retrieved from https://www.whitehouse.gov/cea/written-materials/2023/04/17/the-labor-supply-rebound-from-the-pandemic

6. Lauren Bauer, W. E. (2023, April 4). Who’s missing from the post-pandemic labor force? Retrieved from Brookings Institution: https://www.brookings.edu/articles/whos-missing-from-the-post-pandemic-labor-force/

7. Maradana, R. P. (2017). Does innovation promote economic growth? Evidence from European countries. Journal of Innovation and Entrepreneurship.

8. Leonard, M. (2023, June 20). China Is Ready for a World of Disorder. Retrieved from Foreign Affairs: https://www.foreignaffairs.com/united-states/china-ready-world-disorder

9. Roeder, A. C. (2023, April 17). ‘Transformational change’: Biden’s industrial policy begins to bear fruit. Retrieved from Financial Times: https://www.ft.com/content/b6cd46de-52d6-4641-860b-5f2c1b0c5622

10. House Committee on Science, Space and Technology. (2023, April 17). Science Committee Members Introduce Two Bipartisan DOE Partnership Bills. Retrieved from House Committee on Science, Space and Technology: https://science.house.gov/2023/4/science-committee-members-introduce-two-bipartisan-doe-partnership-bills

11. Gray, J. E. (2021, May 11). The geopolitics of ‘platforms’: the TikTok challenge. Retrieved from Internet Policy Review: https://policyreview.info/articles/analysis/geopolitics-platforms-tiktok-challenge

12. Cohen, J. (2023, May 15). The rise of geopolitical swing states. Retrieved from Goldman Sachs Intelligence: https://www.goldmansachs.com/intelligence/pages/the-rise-of-geopolitical-swing-states.html

13. McDonald, J. (2023, June 20). Foreign companies are shifting investment out of China as confidence wanes, business group says. Retrieved from Associated Press: https://apnews.com/article/china-foreign-companies-investment-trade-a47887e2c89050d291ebd169b0989cc4

14. Kawate, I. (2023, February 28). Foreign investment in China slumps to 18-year low. Retrieved from Nikkei Asia: https://asia.nikkei.com/Economy/Foreign-investment-in-China-slumps-to-18-year-low

15. Sanchez-Munoz, J. D. (2022, December 7). United States Is World’s Top Destination for Foreign Direct Investment. Retrieved from International Monetary Fund Blog: https://www.imf.org/en/Blogs/Articles/2022/12/07/united-states-is-worlds-top-destination-for-foreign-direct-investment

16. DeNight, R. L. (2021, October). Make Yourself At Home: U.S. Manufacturing Reshoring And Foreign Direct Investment Accelerates. Retrieved from Newmark: https://www.nmrk.com/insights/thought-leadership/us-manufacturing-reshoring-and-foreign-direct-investment-accelerates

17. Ewing, P. (2017, February 22). McMaster, An Iconoclast, Confronts A Job Bound By Political Realities. Retrieved from National Public Radio: https://www.npr.org/2017/02/22/516631589/mcmaster-an-iconoclast-confronts-a-job-bound-by-political-realities

18. Gold, A. (2023, June 27). Exclusive: Immigrants play outsize role in the AI game. Retrieved from Axios: https://www.axios.com/2023/06/27/immigrants-us-ai-development

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY UNDERWRITTEN BY

For more than 20 years, Yardi has developed real estate investment management software that helps managers of global assets valued at trillions of dollars make informed investment decisions. Yardi Investment Suite clients include many of the world’s premier investment management funds, start-ups and partnerships of all types and sizes.

Real estate investments grow on Yardi. That’s because the Yardi Investment Suite automates complex investment management processes and provides full transparency, from the investor to the asset. Through interactive dashboards, investors can view documents and have access to reports and metrics. Collaboration is easy when your advisor or accountant is given access to view your accounts, reducing the need for emailing sensitive information.

The Yardi Investment Suite leads the real estate industry through innovation and value with fully integrated investment management, property management and accounting functionality. Fund managers and their customers can manage assets with superior efficiency and ease. Learn more.