This article appears in Summit Journal (Fall 2020) | Download PDF

Gone are the days when industrial was a niche sector not worth most institutional investors’ attention. But over the last five years, what is now called “logistics” in Europe has firmly established itself as one of the key sectors on par with office, retail, and residential.

While people’s lives are growing increasingly virtual, which is causing havoc for retail real estate—and now also challenging offices with more home working—the world of physical goods appears to be thriving across all global markets. The key to that counterintuitive development lies in the ever-more comfortable lifestyles consumers enjoy in ever-more urban cities. Over the last decade, successful cities have seen real estate values, especially sought-after central districts, increase enormously on the back of office, hospitality, and residential uses vying for the same locations.

On a square foot/meter basis, historically lower-value assets such as logistics, data storage, or parking garages have been pushed out of these centralized locations, while the demand for such services has increased. Shopping in cyberspace still results in a physical good being delivered, and streaming video requires data infrastructure instead of a nearby movie theater. In the competition for space, land values and consequently rents, for industrial-type properties have increased.

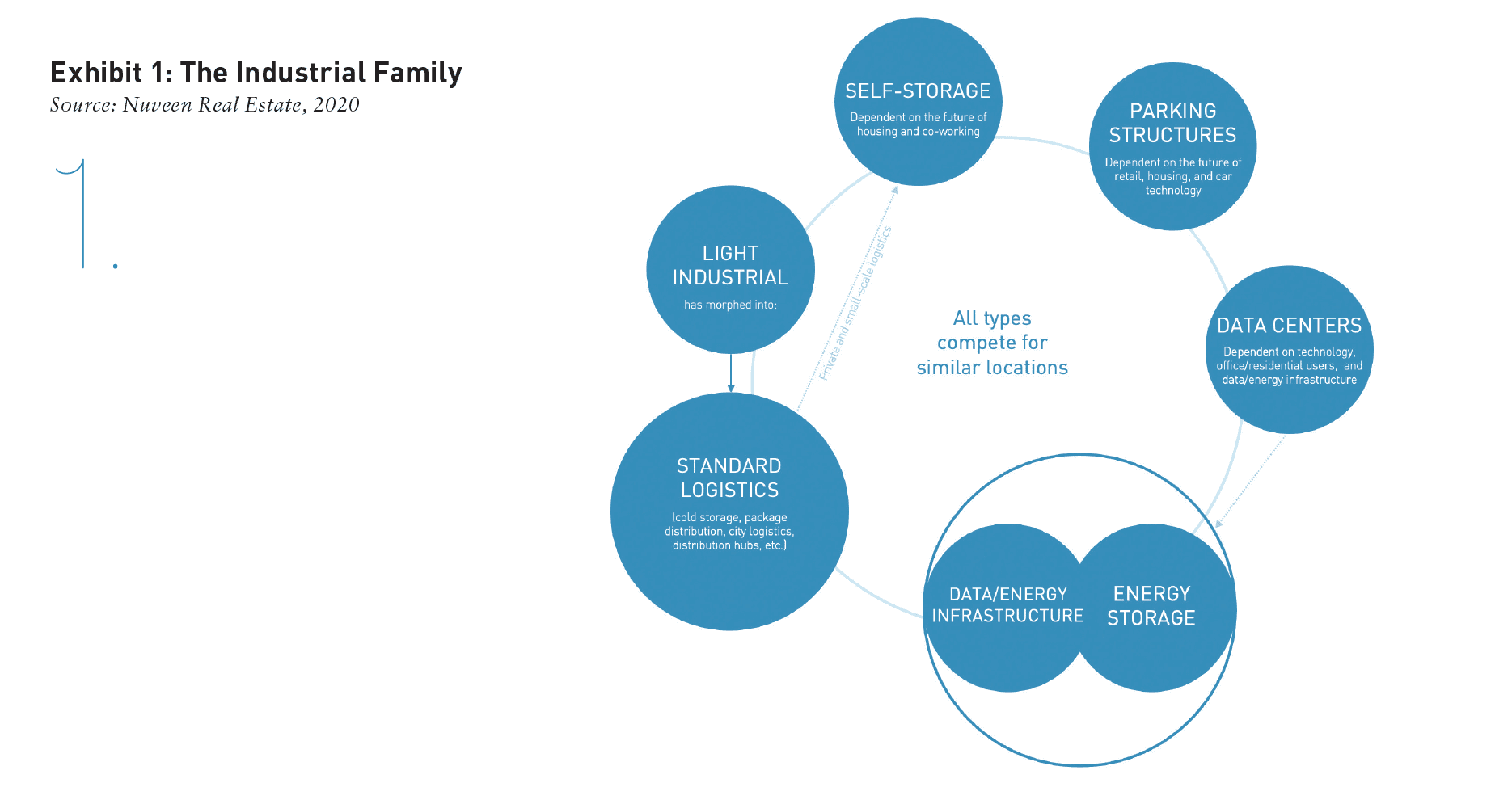

THE INDUSTRIAL FAMILY IS EXPANDING

Within the umbrella term of industrial property, logistics as a sub-type has grown into a sector on its own, driven by the rise of e-commerce. Other segments of the industrial family are on the verge of becoming sectors in their own right, too. With the development of the digital economy, data centers are the next frontier, where a mixture of REITs (mainly in the US) and private market capital (mainly in Europe) are shaping a new distinct asset class with huge growth potential. Data centers must be near their customers, which are consumers as well as businesses. Additionally, the extensive power and security requirements mean they are usually located in urban areas, competing for sites with other industrial use types, such as self-storage, parking garages, and in the near future, energy storage facilities.

Apart from the fact that these facilities need similar types of locations, they are all driven by technology trends and changes in other parts of the economy that transcend real estate. The rise of co-working has led to more business demand for self-storage, while the growing trend of micro-apartments has done the same for household self-storage requirements. More people working from home due to the COVID-19 pandemic generated a new market for cold storage and dark kitchens to satisfy the need of more meals being delivered to and consumed at people’s homes. The future of parking facilities depends on the development of driverless cars as well as households’ location decisions, which in turn are driven by the future shape of office work.

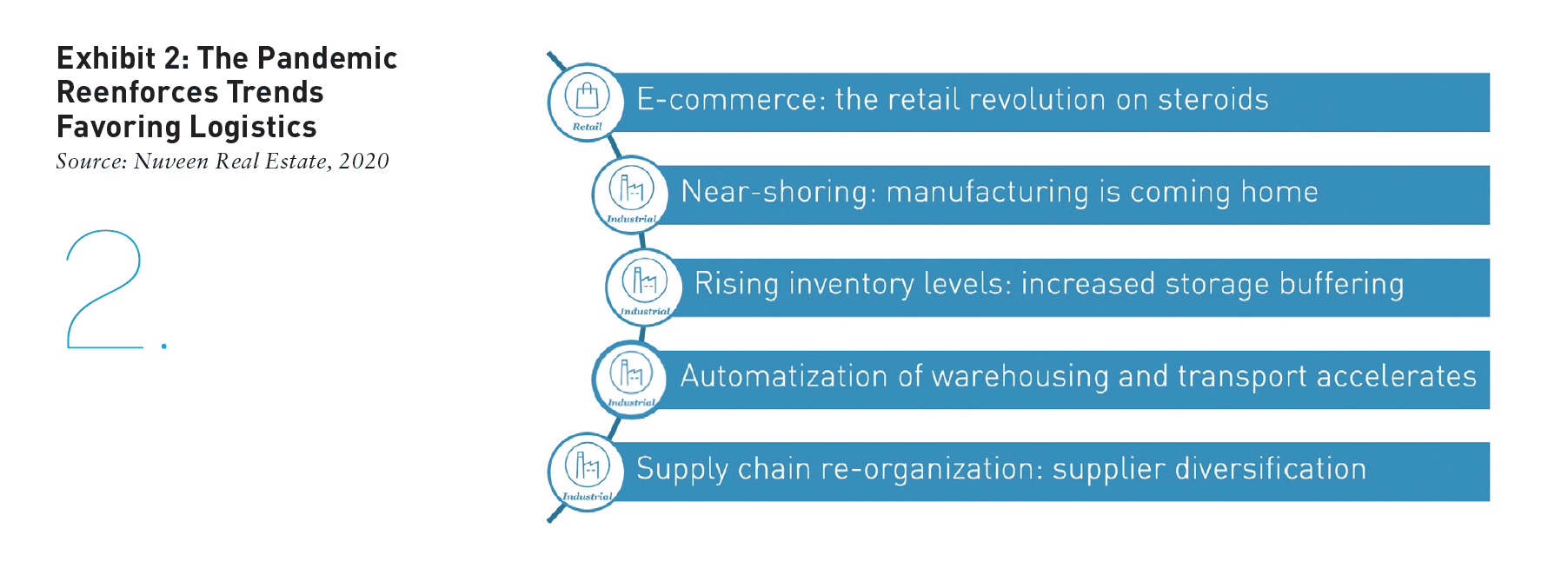

HOW THE PANDEMIC FUELS THE RISE OF LOGISTICS

The pandemic and subsequent severe recession has caused friction in many parts of the real estate market, especially in retail, hospitality, and office. In contrast, many parts of the industrial market are set to benefit, most obviously, the logistics sector. Lockdowns, fear of infection, and other restrictions have encouraged more consumers to shop online, even for products like groceries that have previously seen lower online adoption rates. Several years of online sales growth have been condensed into 2020 alone, and many consumers have tried online shopping for the first time. This means that countries lagging behind (i.e., Japan, Australia, Spain, Poland, etc.) are seeing faster growth, while cities with previously lower e-commerce penetration are set to catch up.

Logistics is also boosted by shifts on the production side. The trend of nearshoring is expected to accelerate demand for logistics closer to European production sites and consumers, while concerns about future supply chain disruptions are already leading to higher levels of inventory. Social distancing rules have spurred automation efforts in a bid to increase efficiency, address labor shortages, and create breathing space. Yet none of these trends are new—they are simply re-enforced and accelerated by the global pandemic.

INDUSTRIAL REAL ESTATE IS SET TO OUTPERFORM

Logistics and other emerging subtypes of industrial are structurally well placed to deliver performance for investors, with social, demographic, and technological changes providing strong tailwinds. Industrial used to deliver strong income returns but did little for capital growth. This has been turned on its head, and now, value increases are the main motivation to invest into the sector, with investors benefiting from both rental growth and cap rate compression.

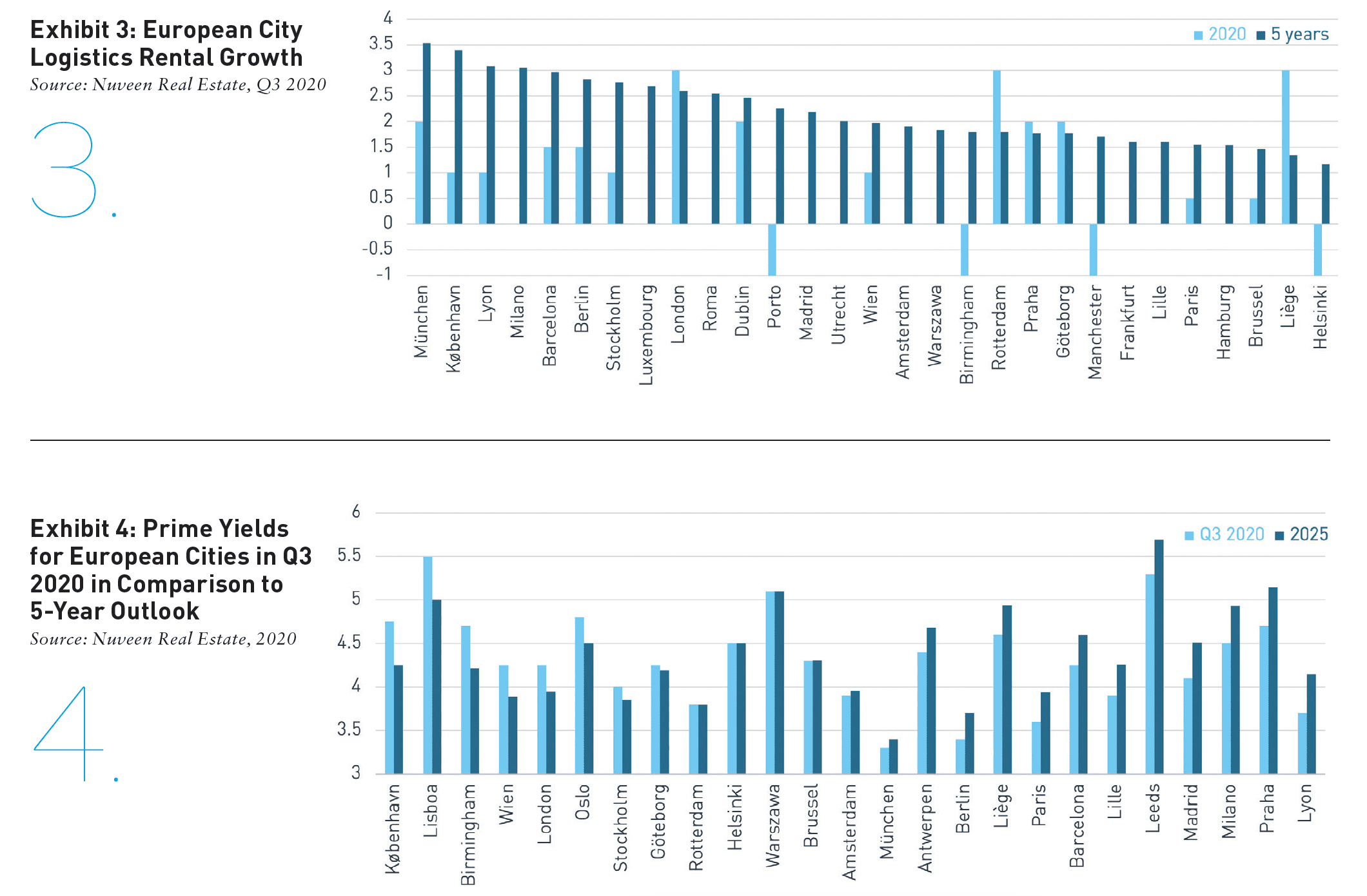

It is therefore not surprising that despite the deep recession, Nuveen projections indicate robust rental growth for the majority of European cities over the next five years (Exhibit 3).

It is also not surprising that investors are prepared to pay a high price to get exposure to this growth. For example, the prime net yield for the very best logistics in Europe is 3.3%, only 40bps higher than the prime office yield of 2.9%. However, these price levels do not indicate the existence of a bubble, with interest rates forecasted to remain ultra-low, and fundamental demand from occupiers expected to stay strong for years to come. Nuveen’s projections suggest that yields may be even lower in future (five years) in markets such London, Copenhagen, Vienna, Lisbon, or Stockholm. Some markets look relatively pricey in comparison, but generally the gap to future expected yields is less than 5bps. But even if yield shifts of that magnitude were to occur, capital growth would remain positive due to rental growth. Additionally, assuming that buyers in Madrid or Milan benchmark their investment with the Eurozone risk-free rate, instead of the higher bond yield of their home market, this outward yield shift pressure would be cancelled completely. Other key regions around the world look pretty similar, fundamentally. The prime market yield is currently around 4% in Tokyo, which we expect to harden towards 3.5%, while Singapore, with its leasehold structure limiting rental growth, is forecast to see yields fall from 6.9% to 6.7%.

It is somewhat ironic that the rise of the digital economy is leading to the rise of industrial—long-considered to be the most generic property type. However, it’s not popularity or elegance which makes industrial so successful; it is inescapable necessity as substantiated by consumer behavioral trends. No video streams without data centers; no package deliveries without distribution hubs; no goods are even produced without light industrial; and no cooked meal is delivered without a dark kitchen. Therefore, we can argue that while very few industrial buildings would be considered to have the beauty and stature of a swan, the sector has found a permanent and ever-more welcome home in real estate investment portfolios.

—

ABOUT THE AUTHORS

Stefan Wundrak is Head of Research, Europe for Nuveen Real Estate. The latest insights from Nuveen Real Estate’s market-leading global research team can be found at nuveen.com/global/thinking/real-estate.

—