The current state of the market suggests calls for modest growth and retreating inflation 2024, with risks focused on the downside and spread across geopolitics, monetary policy, and climate change.

As we enter into 2024, we’re seeing a consensus emerge for modest growth and retreating inflation throughout the year.

As this article discusses, drivers of growth include: (1) the expectation that interest rate tightening is done, alongside a concomitant decline in long-term yields; (2) capacity for a tech sector rebound fueled by record-level dry powder from private equity; (3) continuing stimulus from Federal industrial policies and private sector appetite for advances in electric vehicles, renewable energy, battery storage, AI, and domestic chip manufacturing; (3) preparation for revival in residential construction as financial markets pull in interest rates in expectation 2024 Fed rate cuts.

With these drivers as a backdrop, commercial real estate investment opportunities will be most attractive in metro areas that have been experiencing relatively strong employment growth along with property sectors in metros enjoying a “sweet spot”—cyclically elevated cap rates in metros with moderate vacancy rates and sparse new supply pipelines.

Risks are clustered on the downside and focused on: (1) geopolitical shocks and negative impact on trade, commodity prices, interest rates, and the value of the dollar; (2) monetary policy risk if the Fed misjudges interest rate moves; (3) timing risk if investors wait for distress bargains that are unlikely to materialize; and (4) the ongoing threat of extreme weather/climate events and their repercussions.

POSITIVE ECONOMIC OUTLOOK FOR US ECONOMY BODES WELL FOR PROPERTY

In the waning months of 2023, economic forecasters coalesced around expectations for solid growth in 2024, validating a “soft landing” victory for the Federal Reserve. This conclusion was sharply different from the negativity that was prominent at the beginning of 2023.

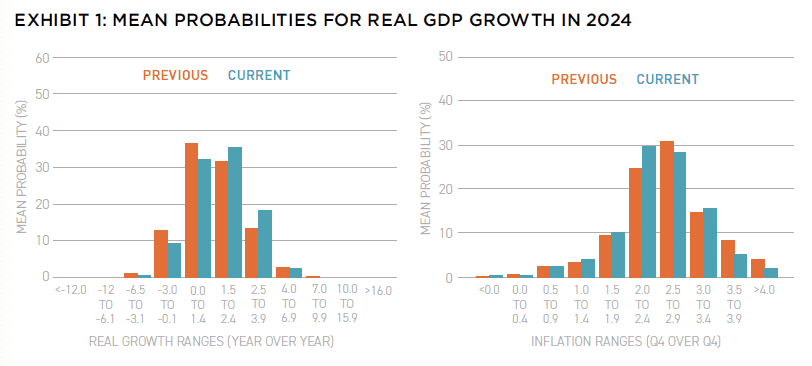

The Federal Reserve Bank of Philadelphia, Survey of Professional Forecasters, reported a 1.7% consensus forecast for real GDP growth in 2024, while assigning a less than 10% probability to a negative outcome for the year.

That optimism is mirrored in the most recent projections released by the Federal Reserve in December 2023. The projections are drawn from Federal Reserve Board members and the individual Federal Reserve Bank district presidents. Their median forecast for 2024 calls for 1.4% real GDP growth with most responses in the 1.2–1.7% range along with interest rate cuts of 50–100BPS over the year.

The drivers of growth in 2024 are focused on the assumed completion of the Fed’s interest rate tightening cycle that produced a 525BPS increase in the Federal Funds rate between March 2022 and July 2023. The tightening reversed the monetary easing enacted to cushion the negative effects of the covid recession.

When inflation popped in 2021, the need for tightening became evident. The tightening appears to have worked as shown in the return of inflation to near the Fed’s 2% target. Forecasters are assigning a 40% probability to inflation of 2.4% or less over the four quarters of 2024. Further easing in inflation through the year is expected reflecting the lag in the impact of higher interest rates on the economy.

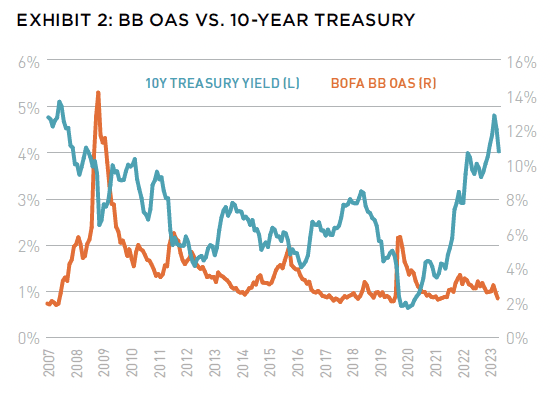

While Federal Reserve policymakers are offering assurances that they are closely monitoring the need for more tightening, financial markets are expecting none but rather see a beginning of easing before the end of 2024. This hope is embedded in the decline in the 10-year Treasury from its 4.98% cycle high posted in mid-October to 3.84% on January 2 as shown in Exhibit 2.

Residential mortgage borrowing rates have moved lower similarly since October and home building and home buying are expected to respond positively as 2024 progresses. The potential for recovery in the housing sector is supported by ongoing job creation and a recovering labor force participation rate which has not yet reached its pre-covid level. Monthly employment growth has been moderating and wage gains year-over-year were a modest 3.7% in November.

At the same time, investors’ risk appetite is reviving as shown in the shrinking of spreads on high-yield BB rated bonds back to pre-covid readings as shown in the chart above along with the 10-year Treasury yield. Beyond traditional corporate business, investors are also focusing on emerging growth engines including renewable energy, artificial intelligence, electric vehicles, and domestic chip manufacturing. Additionally, these innovating industries will get a share of the accumulated venture capital dry powder which is at a record level.

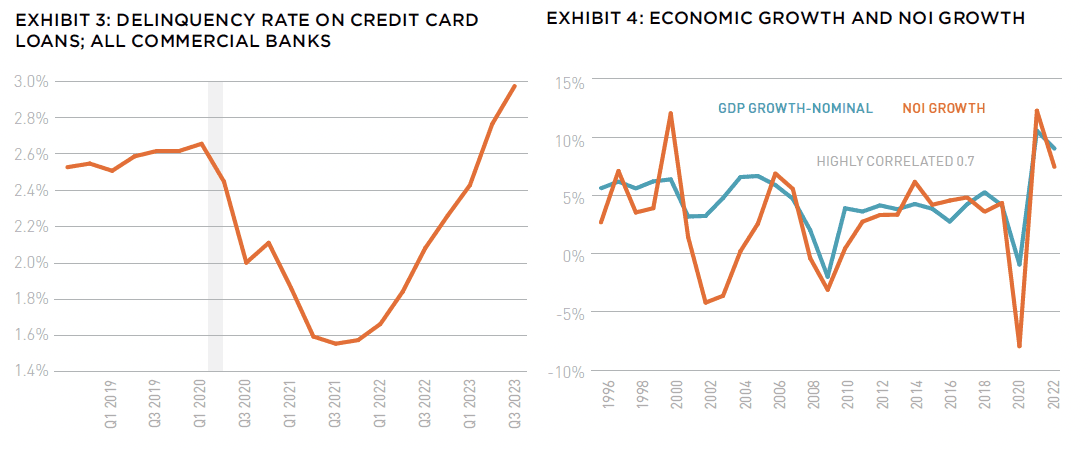

While all these factors support the soft-landing consensus forecast, it is important to note that expected growth is weak albeit positive. It depends on consumer spending holding up in the face of savings depleted of the covid build-up, weakening job growth, leveling wage gains, and elevated costs for rent and groceries. The weight of these stresses is illustrated in the rise in credit card delinquencies shown in Exhibit 3.

With the assumption that consumer spending is sustained, the modest US economic growth expected for the year ahead will produce benefits for the nation’s commercial real estate sector. Notice the strong correlation between real GDP growth and net operating income growth in the NCREIF index. That link is why monitoring the macro-economy is so important.

US REAL ESTATE OFFERING OPPORTUNITY FOCUSED IN SELECT SECTORS AND SELECT METROS

Prospects for US commercial real estate investing in 2024 are dependent on a variety of cyclical and structural forces. The cyclical forces are embedded in the macro-economic prospects already discussed. That outlook for the real economy bodes well for commercial real estate. Ongoing modest growth in jobs, income, and the pace of economic activity feed the demand for space across the four primary property sectors. The degree of benefit depends on the size of the excess space overhang in each market and sector. If the overhang is sizable, potential for rent growth will be compromised.

Cyclical forces also operate through interest rates. The shift in monetary policy that boosted US interest rates has had a huge impact on commercial real estate. Part of that impact is channeled through the restraining effect of higher interest rates on the real economy. Another part is the effect on the cost and availability of debt financing along with its disruption of refinancing maturing debt. In addition, higher interest rates impact investors’ return requirements. When riskless Treasury yields rise, return requirements for all investments must be reset. That process has been driving down property values and elevating cap rates.

A prominent real estate research firm estimates that by year-end 2023 property values had essentially reached fair value in the current interest rate environment.1 Their calculations show that by year-end 2023 core property values were down 25% from peak cycle high values. At the same time, actual property transactions are sparse suggesting that buyers and sellers are still far apart and implying that transactions prices may fall further in 2024. Real Capital Analytics reports an 11.5% value decline based on transactions.2

The path ahead for property values will the refinancing opportunities available for the huge pipeline of property debt that matures during the year ahead. Real Capital Analytics reviewed current leverage metrics for outstanding property debt and concluded that only 6.6% of properties have lost 20% or more of value since origination leaving them vulnerable to refinancing difficulty.3 As a result, opportunity to purchase property at bargain prices because of debt distress is and will continue to be very limited.

Structural forces differ by property sector and metro market. Most prominent are the shift in population growth across metro areas and the ongoing uncertainty in office-space use. Other forces were important factors during the last few years but only temporarily. These include the upsurge in online shopping during the covid shutdown which stimulated demand for warehouse space and exploded warehouse rent growth. That surge is over; both online shopping and warehouse demand are normalizing. Another temporary factor was the covid cash grants which, along with the pause in student debt repayment and the need for work-from-home space, stimulated household formation in 2020. The upsurge in demand for apartments exploded rent growth and promoted new construction with the latter helped by historically low borrowing costs. That surge is over; the household formation rate has retreated.

When combined, these cyclical and structural factors support the following expectations for 2024:

- Non-mall retail sustained as the best performing of the four primary sectors.

- Industrial sector performance returning to positive total return as excess supply is absorbed and the new construction pipeline empties. At the same time, NOI growth benefits from expiring long-term leases turning to higher rents.

- Apartment sector performance will find its floor this year as rents on new supply drop to accommodate absorption and future construction plans are delayed. As supply pressures dissipate investors will have a clearer view of underwriting assumptions facilitating dealmaking.

- Office remains the most uncertain of the four primary sectors. Work-from-home protocols are taking root but remain uncertain. New super-high-quality buildings are leasing up even at super-high rents and higher quality space in general is pulling tenants from lower quality space. As vacancy becomes concentrated in the least attractive buildings, they will slowly be weeded out of the stock . . . slowly!

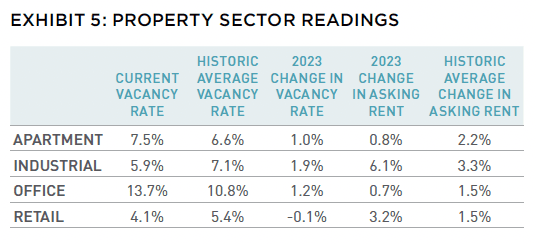

These sector level recommendations are supported by the data shown in Exhibit 5.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

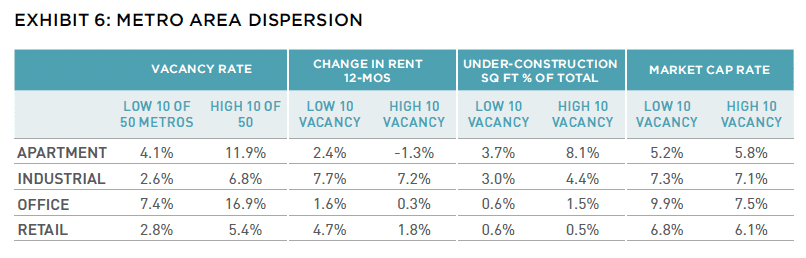

Construction activity is generally stronger in the high vacancy metros except for retail where there is weak construction uniformly. It is especially noteworthy that the pace of construction in the high vacancy apartment metros is very strong suggesting that rent growth will remain challenged in the year ahead. Cap rates are reflecting this expectation but only modestly suggesting that the excess supply is viewed as transitory.

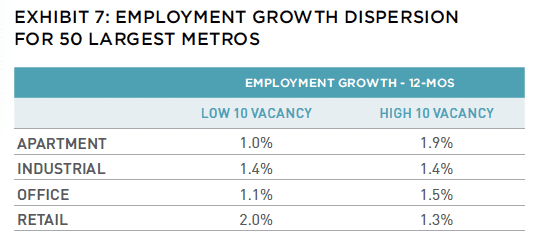

Market cap rates are lower and pointing to the higher vacancy metros as more desirable for industrial, office and retail sectors. This observation is hugely important. It shows that investors are viewing metros with excess supply as more attractive than those with tighter supply. This suggests a confidence that developers have been deeming these metros as having superior economic growth prospects and superior absorption capacity versus metros with low vacancy rates. Only apartments are pricing in some caution regarding high vacancy metros implying that investors are indeed evaluating supply carefully rather than dismissing it. Exhibit 7 shows that the high vacancy metros did indeed produce superior or equivalent employment growth in 2023 versus the low vacancy metros. Retail is the exception.

LOOKING FOR OPPORTUNITY

For investors, there is no simple conclusion other than “metro matters”. Investment selection requires analysis of top-down macro-economic factors, property sector evaluation, and metro area analysis of both property market fundamentals and of the economic and demographic drivers that influence property performance. For the year ahead, the data provided here do not identify clear sweet spots but rather illustrate the uncertainties that investors must confront. Current market cap rates point to confidence that high vacancy rates in some metros are the result of the surge in construction prompted by historically low borrowing rates. With higher interest rates curtailing construction and ongoing economic growth, property buyers will need to assume how quickly the excess space will be absorbed. That assumption will determine the price an investor will be willing to pay. If economic growth falters, absorption will be delayed. Investors are advised to consider this eventuality.

With all this said, the final word is a reminder that no investor can see the future. The potential for shocks is always at hand. But fixation on risk can be paralyzing and paralysis is a risk in itself as it creates no investment return.

The shifts in population growth across metro areas have longer-lasting implications. First, relatively faster population growth may be associated with job opportunities. Second, the relatively faster population growth will in turn create more jobs related to serving that population. Third, demand for space of all types is enhanced in locations where population growth is relatively stronger. In the chart below, population growth for the largest fifty US metros areas is divided into the top ten, bottom ten and middle thirty. (We focus on metro areas because they are comprised of contiguous counties which are deemed to be economically and socially integrated.) Vacancy rates for the four primary property sectors are shown adjacent to the chart.

—

ABOUT THE AUTHOR

Martha Peyton, PhD, CRE, is a research consultant for LGIM America, the global asset management business of Legal & General Group.

—

NOTES

1. Green Street Real Estate, Commercial Property Outlook, December 5, 2023

2. MSCI-RCA, CPPI, December 2023

3. MSCI-RCA “Assessing the Health of US Real Estate’s Loan Collateral”, November 8, 2023

—