This article appears in Summit Journal (Summer 2020) | Download PDF

The demographic data for baby boomers has long been a routine talking point for medical sector outlooks, but with COVID-19, advancements in medical science and technology, and the surprise of Generation X, where’s the sector headed next?

The convergence of demographics, constant advancements in medical science, and the distinct social attitudes of baby boomers has been forecasted to drive medical office demand for several years. Predictions and analyses for Generation X, with its lower birth rates and differing attitudes, introduces some key questions to the outlook for the overall sector, but a closer look at the data suggests that impacts of the generational transition are not as ominous as some may think.

Another look at the baby boomer generation

For the past several decades, the collective effect of baby boomers on American society has been routinely described as the “pig in the python,” a statistical bulge passing through a system that wasn’t necessarily designed for such a large meal but will nevertheless find some way to digest it.

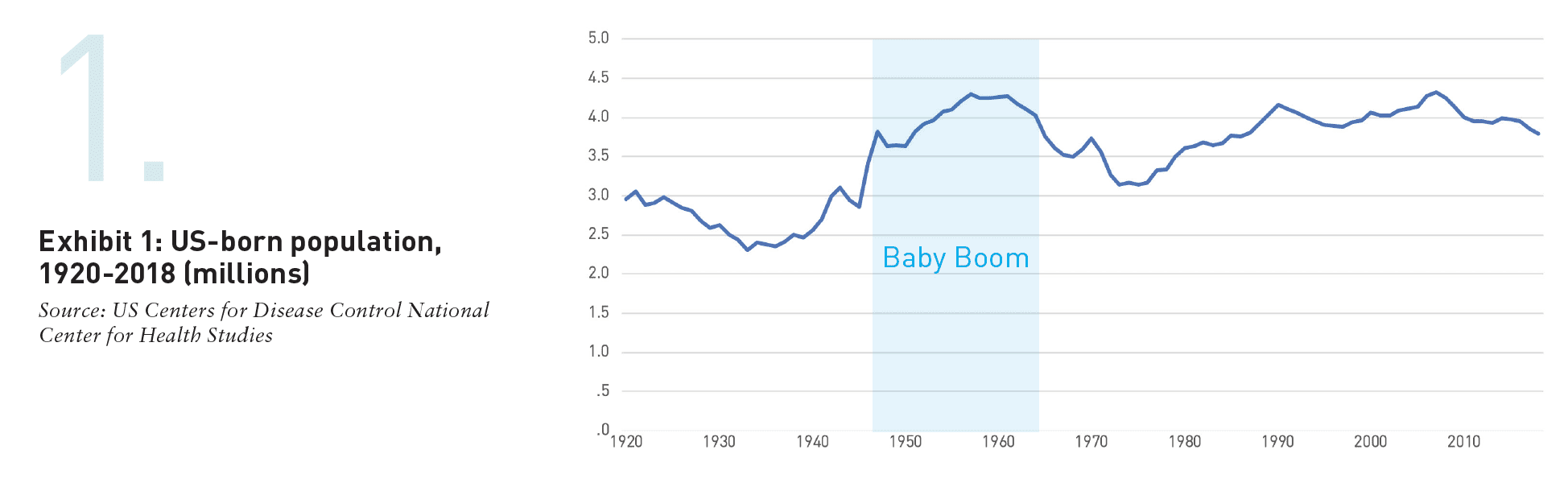

Born between 1946 and 1964, it’s estimated that the net population of baby boomers is currently 72 million (see Exhibit 1). Approximately 10,000 boomers per day are turning 65. They started crossing that threshold in 2011 and will continue doing so through 2029. According to the 2010 Census, life expectancy at age 65 was 19.1 years. That’s up from 11.9 years at the turn of the twentieth century. Assuming the average boomer lives to see their early 80s, the pig will remain in the python for at least another two decades. During that time, it’s estimated that the 65+ age group could swell to 20-25% of the national population, up from 13% in 2010.

Aging baby boomers, looking to remain active well into their golden years, will continue to benefit from advances in medical science. Recent healthcare innovations have radically improved the quality of life for many seniors. However, these innovations go hand-in-hand with need. They were developed because the human body remains vulnerable to injury and disease. One of the downsides of living a longer life is the greater likelihood of chronic conditions. In a recent report from the National Council on Aging, it’s noted that 80% of all Americans over 65 are currently managing at least one chronic condition, and many of them are managing more than one.[1]

Leading into the COVID-19 crisis, baby boomers were seeking out medical treatments that help maintain a feeling, and appearance, of youth. Their strong self-image, coupled with a healthy dose of affluence, pushes them to seek care that never would have occurred to their parents. Whether it be discussing stress with a psychologist, golf swings with a physical therapist, or “a little work” with a plastic surgeon, boomers simply have different medical needs and expectations, and more of them, than past generations. According to the Centers for Disease Control, the average American visits a physician’s office 2.8 times per year.[2] However, it increases to 4.7 times per year for those aged 65-74, and 5.5 times for those older than 75. Medical demand increases with age.

Medical office supply and demand

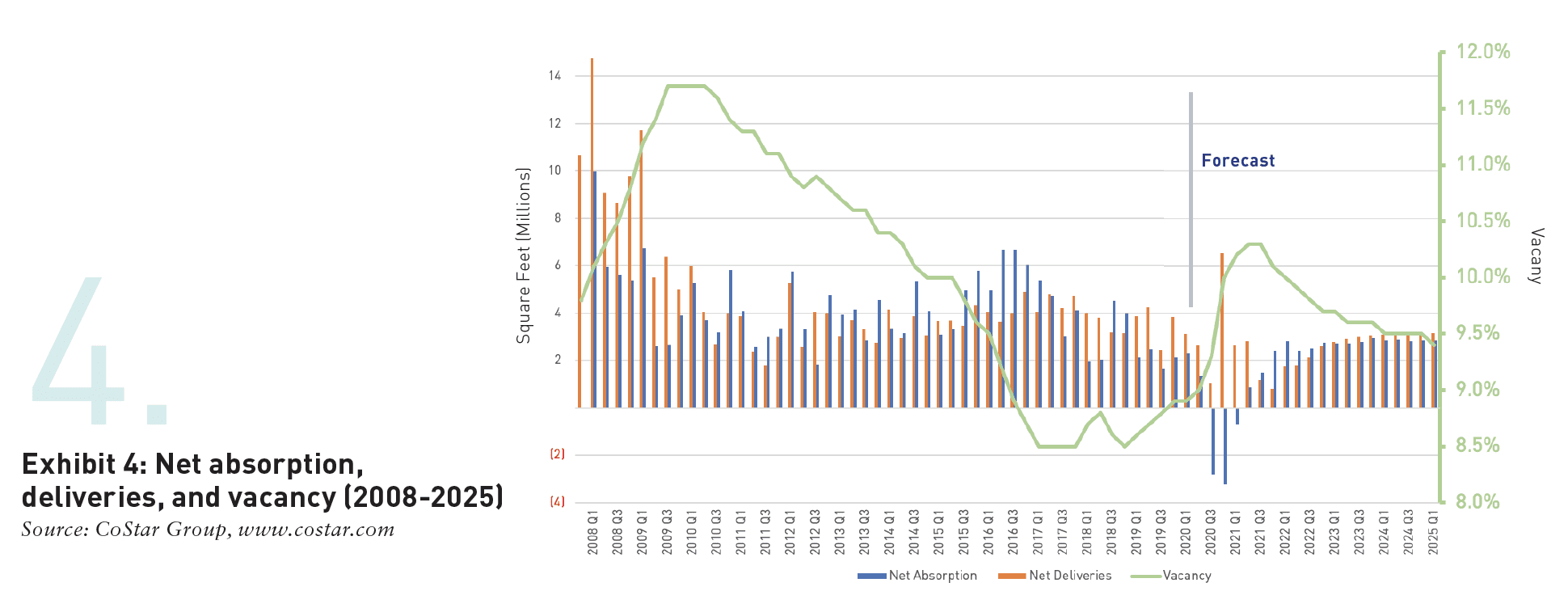

Where there’s demand, supply will follow . . . eventually. Leading up to COVID-19, new medical office construction was not keeping up with the demand. There is currently 1.2 billion SF/111.5 million SM of existing medical office inventory in the continental US, limited to Class A and B properties. Only 13.4 million SF/1.24 million SM was delivered within the past year, and 70.5% of that was pre-leased at completion of construction.

Net absorption during this same time was 8.3 million SF/772,000 SM. There is currently another 14.4 million SF/1.34 million SM under construction that will be coming online by the end on 2021, though construction starts slowed dramatically during the first half of 2020. This has kept vacancy relatively tight at 9.0%, despite the current economic slowdown. Breaking it out, Class B is currently performing better than Class A, with vacancy of 8.6% vs. 10.9%, while both continue to outperform general office (Exhibit 2).

OVERWHELMINGLY, the focus of new development has shifted to suburban locations, a decentralization of healthcare services that tends to be more conveniently located for patients and grows market share for healthcare providers, the latter starting to take on more significance due to recent high-profile mergers and acquisitions of hospital and healthcare systems. This decentralization is favoring ambulatory surgery centers and other build-to-suit facilities, due largely to the breadth of medical procedures that no longer require a hospital stay. Ever improving technology now allows for many procedures to be performed safely and more economically on an outpatient basis.

So, what about Generation X (and immigration)?

So far, all of this has seemed pretty favorable to medical office. But what happens after boomers? We’ve all heard the dire warnings about Generation X. Born between 1965 and 1980, Xers are sandwiched between two much larger demographic cohorts: baby boomers and millennials. The first of the Xers will start turning 65 in 2030, leading their generation in a march over that threshold that won’t end until the more populous millennials starts turning 65 in 2046. If the birth rate statistics suggest that 15 years of negative growth trends in the aging population are imminent, shouldn’t we be concerned about the longer-term demand for medical office? Perhaps not.

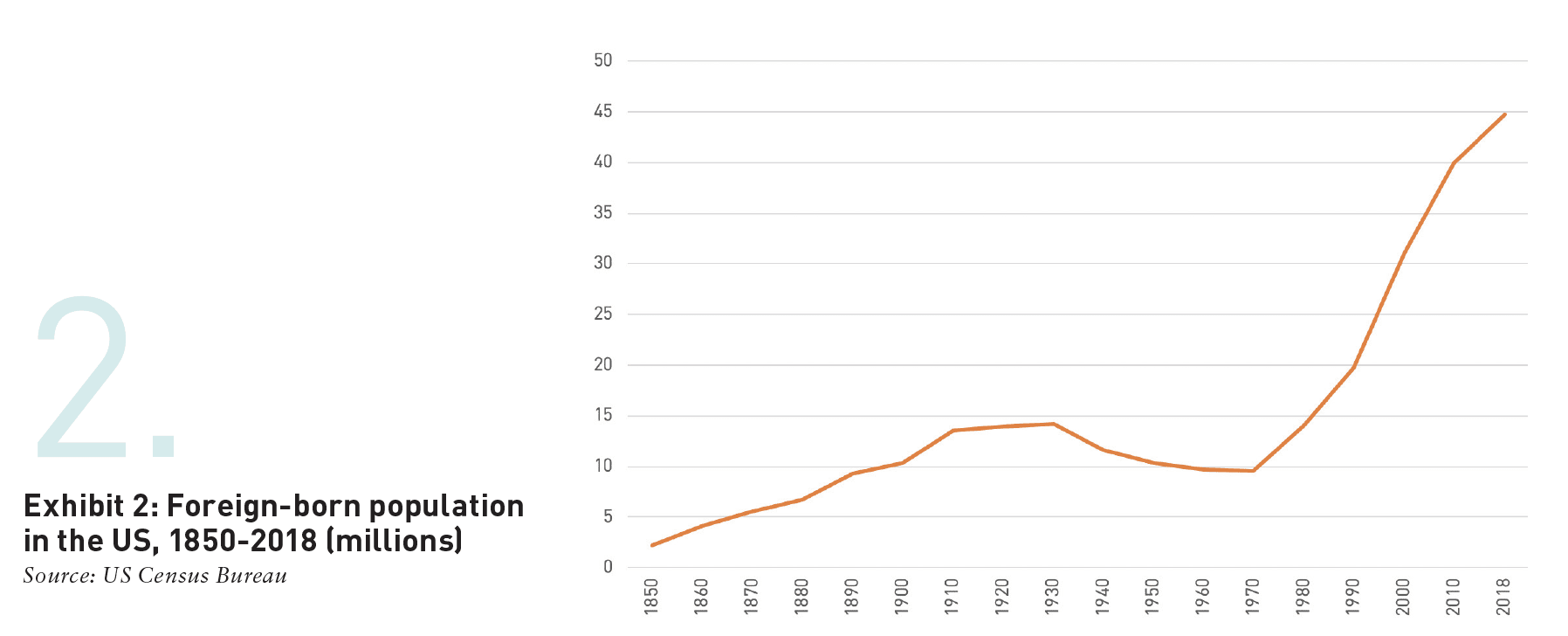

According to the most recent estimates from the US Census Bureau, there were a record-high 44.7 million immigrants living in the US in 2018, which accounted for 13.7% of the nation’s population. That’s up from only 9.6 million in 1970, when foreign-born residents represented just 4.7% of the nation’s population. The Census Bureau releases its official numbers every 10 years, with 1970 being the first decennial census taken after the generational transition from baby boomers to Generation X. Exhibit 3 represents the foreign-born population in the US over the past 150 years. As shown, all the real action began in the 1970s, coinciding with the birth of Generation X.

THE ANNUALIZED growth rate trends of foreign-born residents have a meaningful impact across generations. Between 1940 and 1970, growth rates were negative for the only time during the twentieth century. In 1980, that trend reversed and growth rates in the foreign-born population have been positive ever since, with the greatest growth occurring between 1980 and 2000. These ebbs and flows were significantly guided by the implementation of restrictive immigration policies and quotas during the first half of the twentieth century, followed by a loosening of those restrictions by a number of key pieces of legislation that started with the Immigration and Nationality Act of 1965. While it may be entirely coincidental, this makes for spot-on timing as the first Xers were born in 1965 as well.

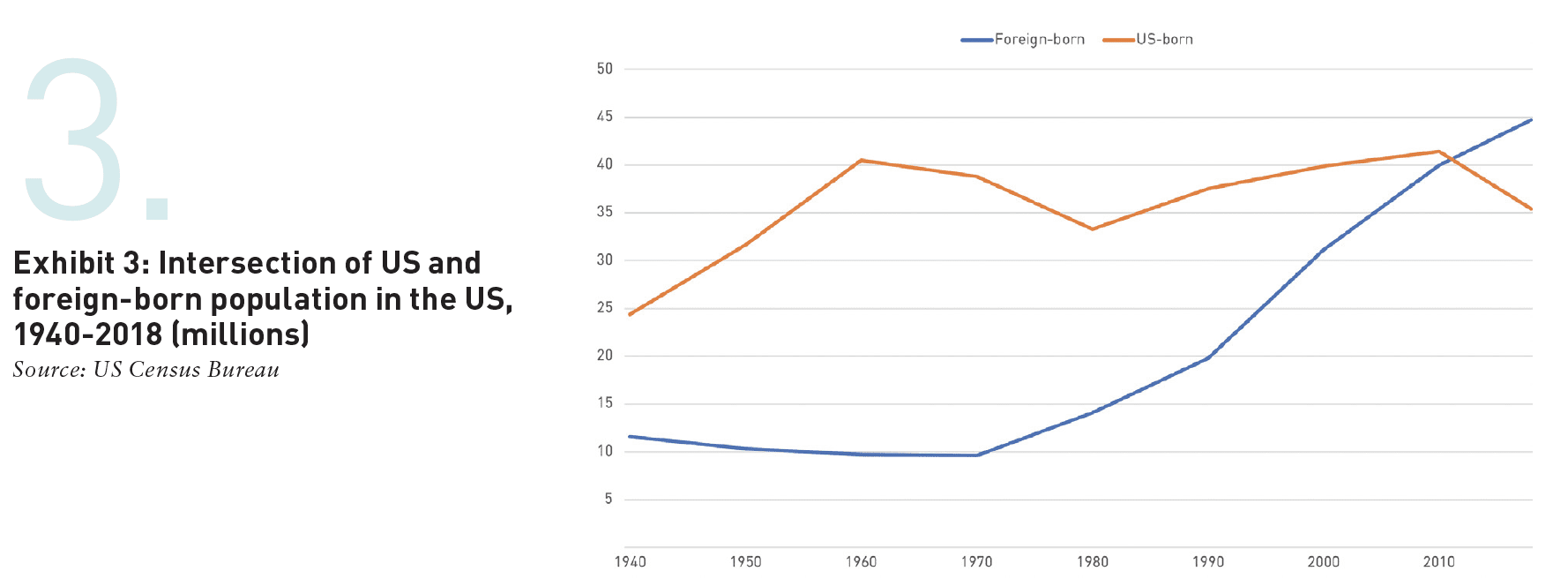

THE GROWTH in the foreign- born population goes a long way in offsetting the declines in the native-born population associated with Generation X. As of 2018, the Census Bureau estimates that approximately 18 million of the current 44.7 million foreign-born residents in the US, or approximately 40% of the total, fall between the ages of 38 and 53 (Generation X). Add that to the 55 million native-born Xers, and you end up with a sum that’s similar to the currently estimated population of baby boomers. This suggests that we’re unlikely to experience a significant reduction in the number of senior citizens in the US anytime soon.

As long as the recent immigration trends hold relatively steady through 2030, when the Xers start turning 65, any decline in demand for medical office is unlikely to be traced directly back to demographic changes.

Demographics, technology, attitudes, and COVID-19

Beyond demographics, the future of medical office is not without risk, especially when considering advancements in telehealth and medical technology—many of which are rapidly evolving throughout the COVID-19 crisis.

While telehealth has the potential to offset demand for medical office, and warrants continued monitoring, this technology is equally as likely to evolve as a compliment to in-person visits, rather than a flat-out replacement of them. Medical office users are still going to need physical space for the services that simply can’t yet be handled remotely.

A more concerning trend is the ongoing encroachment of retail properties into the medical office market. Sometimes referred to as the “consumerization of healthcare,” the benefits to patients include walk-in services, expanded days and hours of operations, and convenient locations. From the landlord’s perspective, however, consumerization presents challenges.

Traditional retailers and their customers may be averse to the close proximity of ill and potentially contagious patients. It is not always given that retail zoning will allow for all medical office uses. Most significantly, the retrofitting of a retail space to medical office use can be very elaborate, typically in direct correlation with the level of care being provided, up to and including structural and mechanical upgrades. For the foreseeable future, the variety of medical office tenants in retail properties will likely be limited to those that treat low-acuity patients and benefit from locations with good street visibility, and healthcare providers in highly competitive fields, such as chiropractors and dentists.

Although the durations of both the COVID-19 pandemic and the current economic recession remain unclear, there’s one thing we can say with absolute certainty: boomers (and Xers) aren’t getting any younger. COVID-19 has introduced many of them to the idea that they may be the “most vulnerable” members of society, an aging demographic cohort that is likely to be managing one or more chronic or “underlying” conditions. That’s powerful motivation to double down on one’s health concerns, especially for a group that identifies so strongly with an active and independent lifestyle.

There’s another truism that’s often heard these days: this too will pass. At some point, we’ll be on the other side of COVID-19 and this recession. Baby boomers will still be aging, the human body will still be frail, and there will still be a never-ending need for healthcare services. The demographic and healthcare industry trends discussed in this article point to ongoing demand for medical office across generations. While we must acknowledge the risks associated with technological advancements in healthcare delivery, and the conversion of retail space to medical office uses, well-chosen medical office investments remain poised to outperform many other property types for years to come.

—

ABOUT THE AUTHOR

G. Evan Bennett is the Founder and Managing Member of Anthology Capital, a private equity firm that invests in commercial real estate, and also serves as the Secretary General of the World Council of Experts at FIABCI, an international real estate industry group.

NOTES

1. National Council on Aging, “Healthy Aging Fact Sheet,” National Council on Aging (October 7, 2018), d2mkcg26uvg1cz.cloudfront.net/wp-content/uploads/2018-Healthy-Aging-Fact-Sheet-7.10.18-1.pdf

2. US Centers for Disease Control, “National Ambulatory Medical Care Survey: 2016 National Summary Tables,” US Centers for Disease Control (2016), cdc.gov/nchs/data/ahcd/namcs_summary/2016_namcs_web_tables.pdf?source=post_page

—