Economic state models can provide investors with empirical assumptions across different regimes. And when combined within a probabilistic framework, these models allow investors to create a set of expectations and possible forward-looking strategies.

A complex and conflicting set of macroeconomic and capital market data has complicated forecasts for the US economy. The Federal Reserve is actively slowing the economy through aggressive monetary policy tightening to offset a strong economy. The Treasury curve has been inverted for quite some time and the recent volatility in ten-year bonds has made the economic outlook murkier.

Given the heterogeneity of real estate markets, this complicated setup has made the landscape challenging to navigate, even for the most seasoned strategists. Against this backdrop, economic state models can be powerful tools for investors seeking to formulate investment strategies in periods of uncertainty by systematically grouping real estate market cycles into discernible regimes potentially identifying actionable trends.

DEFINING AN ECONOMIC STATE MODEL

There are several approaches to modeling economic cycles: structural, non-structural, and large-scale models. Structural models are mostly based on economic theory while non-structural models are statistically driven and without pre-defined relationships. Large-scale models are hybrid models that combine the benefits of underlying economic theory (structural models) and build relationships among different key indicators using empirical data (non-structural models).

Economic state models are used in identifying shifting patterns of growth or transition from one set of conditions or “state” to another. In commercial real estate, economic state models can be used as another valuable tool for investors to (a) recognize cycles given market conditions and (b) signal inflection points in demand cycles to potentially prepare for a shift from one state to another.

A NON-STRUCTURAL MODEL THAT USES EMPIRICAL OBSERVATIONS

This article aims to provide investors with a framework for navigating real estate markets through the use of non-structural economic state models. These models provide a simplified view of the economy and real estate markets that helps understand current and future market conditions and can allow investors to formulate forward looking strategies using a probabilistic transition matrix derived from empirical observations. We also limited our model to the office sector because it encompasses a large set of heterogeneous characteristics and is currently in the eye of a storm given very weak operating fundamentals.

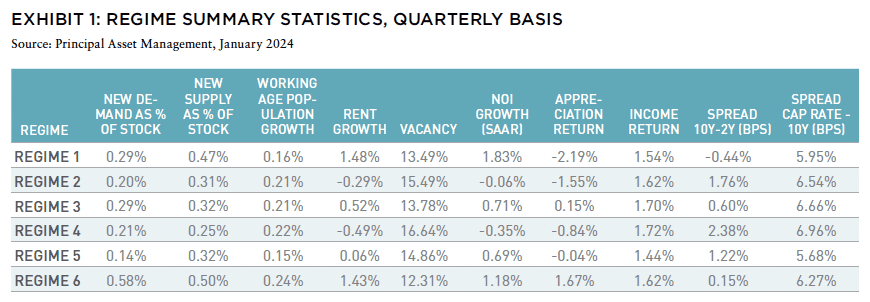

Because our economic state model focuses on commercial real estate, inputs include supply and demand fundamentals, investment performance, NOI growth, working-age population growth, and treasury spreads. Using a clustering algorithm, we identified six regimes focusing on the US office real estate market with data starting in 1990. The model relied on the following key indicators:

- Rent growth, vacancy rates, new supply as a percentage of stock, and new demand as a percentage of stock.

- NOI growth rates, appreciation, and income returns from the NCREIF National Property Index.

- Working-age population growth, the spread between the 10-year and the 2-year US bond yields, and the spread between the 10-year bond yield and office cap rates from NCREIF.

Exhibit 1 provides a breakdown of our regimes using average values from the key indicators above to describe US office real estate markets.

Each state in Exhibit 1 represents a unique combination of market conditions and associated investment performance for US national office market over the time horizon of our analysis, spanning four decades.

Under the current state (Q2 2023), our analysis indicates that the US office sector is in Regime 1, historically characterized by the worst appreciation returns, -2.19% (-8.48% on an annualized basis). This regime is more characteristic of a deep contraction, although it still has positive NOI and rent growth which is unusual for this stage in the cycle.

Conversely, Regime 6, with the lowest vacancy rate (12.19%) among all regimes, and the highest appreciation rate of 1.67% (6.86% on an annualized basis), which is characteristic of an expansion for the US national office sector in our analysis.

INSIGHTS INTO US OFFICE

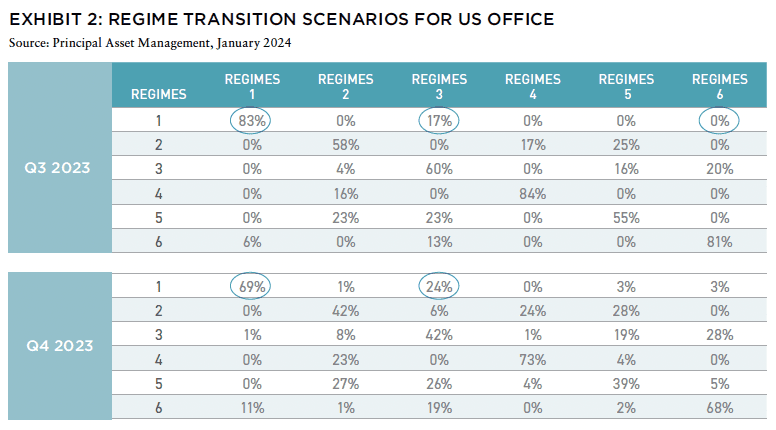

To understand how US office sector regimes may transition from one state to another, we use probability-based analysis to generate a matrix (Exhibit 2). These probabilities calculate the likelihood of transition from one state to the next within a single quarter based on the input variables described above.

Each iteration represents a quarter: Iteration 1 is the first quarter ahead, Iteration 2, the second quarter ahead, and so on. Our model suggests:

- The probability that the US office sector goes from Regime 5 to Regime 2 within the first quarter is about 17%; and

- The probability that the US office sector stays within Regime 5 during the same time (Iteration 1) is 83%.

- In the second iteration, which refers to the first quarter of 2024, the probability that the US office sector remains in Regime 5 drops to 70% while the transition to Regime 2 moves to 27%.

By repeating this process over multiple iterations, we get to a point where there is no more change in the probability distribution, indicating an equilibrium state where the odds of moving from one state to the other are stationary. In considering six regimes for our study of the US office sector, we reach equilibrium after nine quarters with the probability of remaining in Regime 1 dropping to 24%, followed by the probability to transition from Regime 1 to Regime 3 or Regime 6, indicating improved market conditions, standing respectively at 26% and 23%.

FORECASTING OFFICE PERFORMANCE

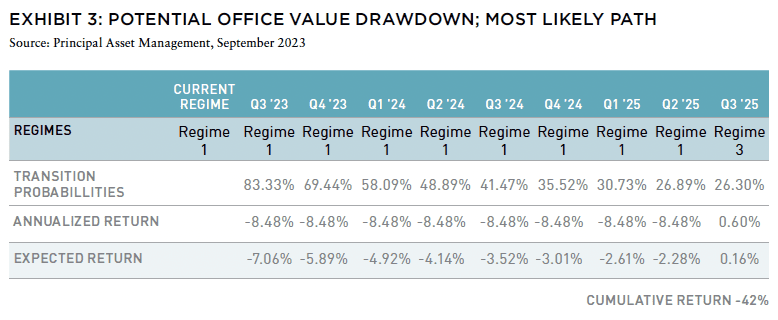

An additional benefit of economic state models is their ability to forecast expected returns for the US office sector. By employing the transition matrix in conjunction with the annual appreciation returns associated with each regime, we estimated expected annual appreciation returns for the NPI US office index using two transition paths as illustrated in Exhibit 3.

This relatively simple approach allows us to derive key takeaways for US office sector.

Following the most likely path scenario in Exhibit 3, which is based on the highest transition probability of each regime along the path, we’d expect the US office national sector to continue to face headwinds for at least the next two years and crossing positive territory only in the second quarter of 2025.

Using historical measure to and the performance associated with this scenario, the estimated cumulative value decline for US office market starting in Q2 2022 would be around 44% for the index.

It is important to recognize that the use of economic state models in forecasting forward-looking returns is limited by their heavy reliance on historical patterns. As such, caution should be exercised in times of unprecedented changes in the market like what we’ve seen in the US office sector. There is also an appreciable lag between the index and the “spot” transaction market which is already suggesting material price dislocation in the office sector. Therefore, given well documented appraisal lags in private markets, our estimate may never be realized within the index but is likely to be recognized in transaction data.

GAUGING THE STATE OF THE ECONOMY

Economic state models are valuable in providing investors with a systemic way to gauge the state of the economy, and perhaps more importantly, a path forward especially in times of uncertainty. Employing the transition matrix in conjunction with annual appreciation returns associated with each regime can help investors extrapolate expected annual returns over their forecast horizon. Economic state models are also a valuable tool for investors seeking a framework to methodically analyze dynamics between macroeconomic indicators and local market trends, as well as anticipate changes in real estate cycles and formulate better-informed strategies.

Applying our non-structural economic state model to the office sector, we conclude a difficult period lies ahead. While this will be challenging to navigate, it could also offer investors confidence, and decision-making tools as well as a potential time frame to deploy capital in the office sector with input from potential outcomes using an economic state model.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

ABOUT THE AUTHORS

Armel Traore Dit Nignan is Head of Real Estate Data and Analytics for Principal Real Estate.

—