The mainstreaming of non-traditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

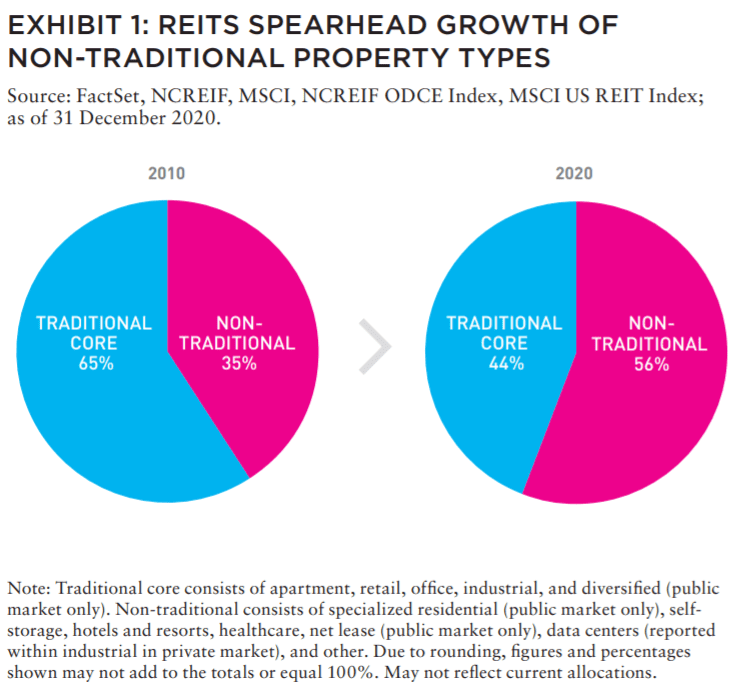

Historically, institutional real estate investors have allocated capital to five property types in the US—office, retail, multifamily, industrial, and hotel. But, in recent years, several niche and emerging property types have seen a significant increase in investor interest and capital allocated, in both the public and private real estate quadrants. According to Real Capital Analytics, as of year-end 2020, these non-traditional property types accounted for approximately 24% of all transaction volume in the US and approximately 56% of total REIT market capitalization.

The listed REIT market has spearheaded the push into nontraditional property types (Exhibit 1), greatly expanding the investment universe and improving the diversification outcome for investors. Many of the largest REIT companies by market capitalization belong to the non-traditional property type category. Their stable and steady cash flows could augment the growing case for inclusion in a real estate portfolio.

PRIVATE REAL ESTATE INVESTORS ARE RAPIDLY EMBRACING NON-TRADITIONAL PROPERTIES

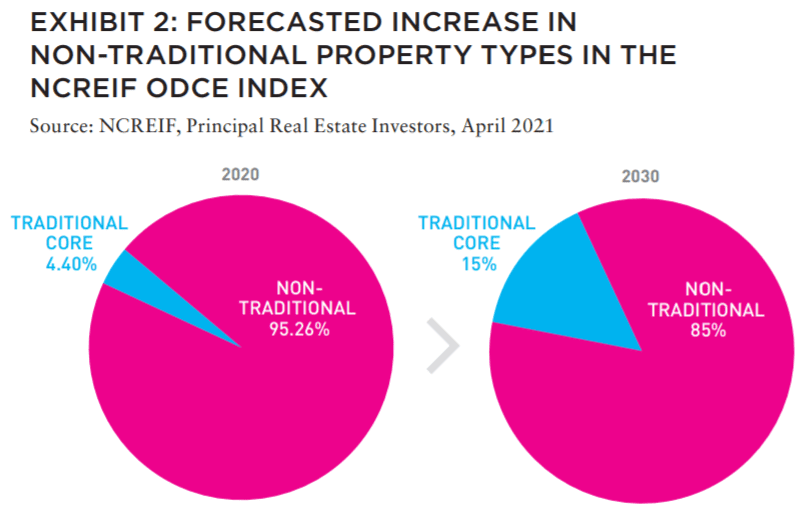

The past couple of years have seen a significant uptick in investment into non-traditional property types by private real estate investors. Currently non-traditional property types sit at 5–6% within the National Council of Real Estate Investment Fiduciaries (NCREIF) ODCE Index. One expectation is that, on a conservative basis, nontraditional property types could comprise 15% of the ODCE Index by 2030, nearly tripling from current levels. This increase would still trail the experience of listed real estate and be quite comparable, for example, to the growth in the industrial sector in the ODCE Index, which increased from approximately 14% in 2010 to around 20% in 2020 (Exhibit 2).

THE GROWTH OF NON-TRADITIONAL PROPERTIES REPRESENTS A SECULAR SHIFT IN DEMAND DRIVERS

The rapid and significant adoption of non-traditional property types in both the listed and private real estate universe is not just a cyclical rotation: it may reflect a structural shift within the economy wherein “DIGITAL” drivers of growth and demand— Demographics, Infrastructure, Globalization, Innovation, and Technology—have become more dominant in recent years.

The rapid and significant adoption of non-traditional property types in both the listed and private real estate universe is not just a cyclical rotation: it may reflect a structural shift within the economy wherein “DIGITAL” drivers of growth and demand— Demographics, Infrastructure, Globalization, Innovation, and Technology—have become more dominant in recent years.

The pandemic further accelerated these structural changes, in some cases rapidly upturning how consumers and businesses behave and occupy space. These drivers have a clear impact on the growth of both traditional and nontraditional property types— directly and indirectly—given their sheer scale. But diving a little deeper, there are specific sub-themes within the broader DIGITAL framework that tie in to the rise of non-traditional property types and their increasing importance, briefly spotlighted below.

• Demographics: senior living, medical offices and lab spaces, single-family rentals, manufactured housing, self-storage, affordable housing

• Infrastructure: data centers, logistics, warehouse

• Globalization: logistics, warehouses, last mile distribution, cold storage

• Innovation and Technology: life sciences, lab spaces, medical office buildings

LISTED REITS SHOW NON-TRADITIONAL PROPERTIES CAN BENEFIT TRADITIONAL REAL ESTATE PORTFOLIOS

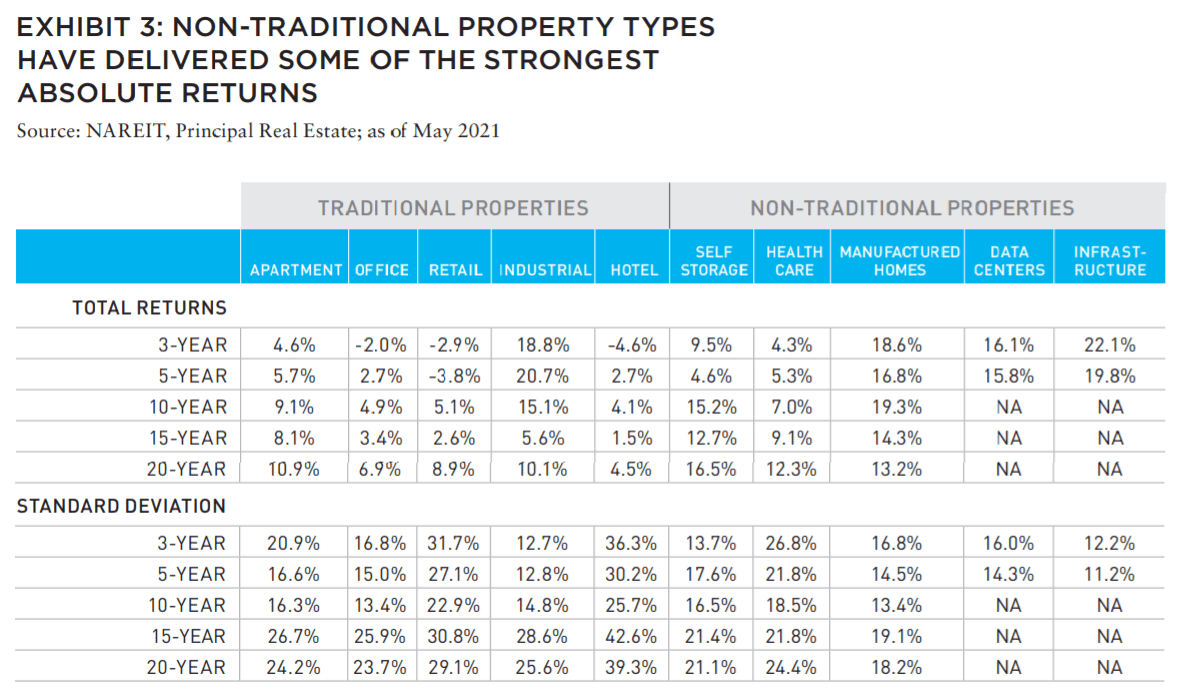

Investors need to understand the benefits to portfolio diversification that non-traditional property types may bring to an existing real estate allocation. The early and rapid adoption of non-traditional property types in listed REITs provides a robust data set of performance metrics and indicates that non-traditional property types have delivered some of the strongest absolute returns over a twenty-year history (Exhibit 3). Self-storage, healthcare, and manufactured homes are the property types that stand out for their strong absolute performance over nearly all time periods.

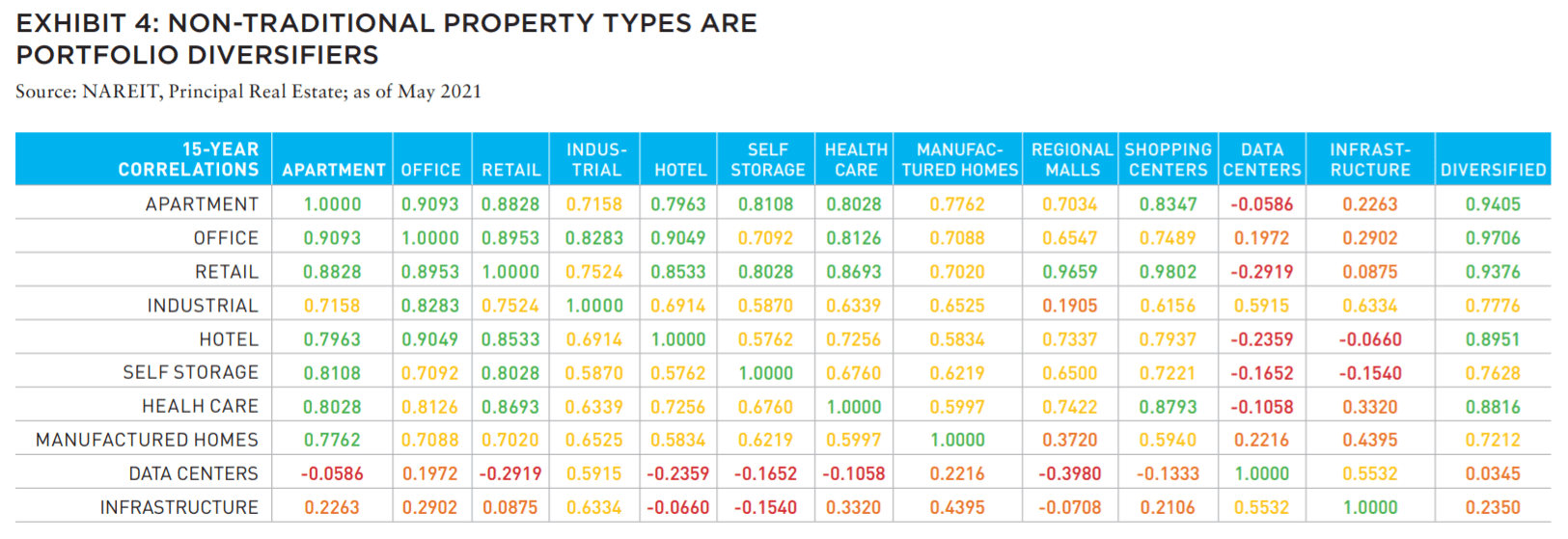

Correlation analysis further demonstrates the diversification benefit of adding non-traditional property types to a portfolio. While intuitively it would seem that return correlations between traditional and alternative property types would vary, the data does indeed confirm it (Exhibit 4).

Despite the growth and maturation of non-traditional property types, correlations have stayed low, indicating the variability of business and operating models that are brought into a portfolio with purely traditional property types. In fact, it is the operating model of many of these underlying companies that helps bring in added diversification to a more traditional portfolio comprised of income-oriented real estate.

Mirroring a similar analysis in the private real estate quadrant is hampered by lack of data but we can infer a certain degree of similarity between the performance of listed and unlisted real estate given the underlying operating and business models are the same. Data centers, self-storage facilities, or SFRs, for example, operate under similar models whether held in listed or private ownership. Most importantly, REIT historical data demonstrates that allocation towards non-traditional property types addresses two key investor requirements: performance and diversification, both of which ultimately benefit portfolio construction.

INVESTORS WILL BE WINNERS AS NON-TRADITIONAL PROPERTIES GO MAINSTREAM

In our view, the mainstreaming of non-traditional property types is well on its way within institutional investing with several positive implications. Non-traditional property types will materially broaden the real estate investment universe and in turn attract a wider array of investors.

The shift and expansion of the universe should also allow investors to generate additional alpha by making conscious investment decisions on their strategies pertaining to alternative property types. Ultimately, we believe the growth and assimilation of non-traditional property types will be a material benefit to the asset class, attracting additional capital and enhancing investment opportunities—and ensuring that investors will emerge as winners.

—

ABOUT THE AUTHORS

Indraneel Karlekar, PhD, is Global Head of Research & Strategy, Principal Real Estate Investors, the dedicated real estate investment group within Principal Global Investors, which builds on a vertically integrated platform that incorporates all disciplines of commercial real estate.

—

ALSO IN THIS ISSUE (FALL 2021)

NOTE FROM THE EDITOR / GROUPTHINK VS. GROUP COLLABORATION

AFIRE | Benjamin van Loon

MID-YEAR SURVEY / CHECKING THE PULSE

No matter your age or experience, 2021 has shaped up to be a year that no one can forget. Findings from the AFIRE 2021 Mid-Year Pulse Survey detail a cautious road ahead.

AFIRE | Gunnar Branson and Benjamin van Loon

CLIMATE CHANGE / REASSESSING CLIMATE RISK

The commercial real estate industry may not yet fully grasp the actual relationship between climate risk and asset pricing and value. But the knowledge is coming fast.

York University | Jim Clayton

University of Reading | Steven Devaney and Jorn Van de Wetering

Kinston University | Sarah Sayce

UNEP FI | Matthew Ulterino

NON-TRADITIONAL / THE ALLURE OF SPECIALTY SECTORS

Real estate investments have historically coalesced around common property types—but it may make sense for investors to reconsider specialty property sectors in the post-COVID world.

Invesco Real Estate | David Wertheim

NON-TRADITIONAL / NON-TRADITIONAL IS GOING MAINSTREAM

The mainstreaming of nontraditional property types is well on its way within institutional investing, which will materially broaden the real estate investment universe.

Principal Real Estate Investors | Indraneel Karlekar, PhD

DIGITAL INFRASTRUCTURE / DIVERSIFYING INTO DIGITAL

As investors look for sustainable sources of inflation-protected yield, real estate investment is increasingly blurring into a wider range of “digital” real asset investment strategies.

AECOM Capital | Warren Wachsberger, Josh Katzin, and Corbett Kruse

LIFE SCIENCES / TAPPING INTO BIOTECH

Over the past two decades, the single-family rental industry haLife sciences real estate has been a “hot” property type for the past decade—and even more since the pandemic. Will all the capital targeting the space be placed where it needs to go?

RCLCO | William Maher, Ben Maslan, and Cecilia Galliani

ESG + CLIMATE CHANGE / HIGH-WATER MARKS

Interest and excellence in ESG performance is becoming increasingly critical to portfolio strategy. So with sea levels on the rise, how can portfolios stay above water?

Barings Real Estate | Jerry Speltz

ESG + NET-ZERO / VALUING NET-ZERO

With more tenants focusing on environmental targets, the burden to reduce direct emissions places increased pressure on investors, who are at a pivotal moment in ESG strategy.

JLL | Lori Mabardi, Emily Chadwick, and Eric Enloe

ESG + FAMILY OFFICE / FAMILY OFFICES AND ESG

As sustainable investing continues to grow in popularity, family offices have taken note—and understanding ESG targets and regulations will be key for longterm performance.

Squire Patton Boggs | Kate Pennartz and Rebekah Singh

DEBT / WHY DEBT, WHY NOW?

Debt funds remain a comparatively small part of the real estate investment market, but they have been gaining in prominence in recent years.

USAA Real Estate | Karen Martinus, Mark Fitzgerald, CFA, and Will McIntosh, PhD

MIGRATION / MIGRATION IN REAL TIME

As the public health situation started to improve in early 2021 and the economy reopened, did migration flows change too—and what if we are able to answer this in real time?

Berkshire Residential Investments | Gleb Nechayev

StratoDem Analytics | Michael Clawar

URBANISM / DOWNTOWN DISRUPTION

The pandemic-driven changes to downtown areas and central business districts is changing the geography of institutional investment. What else changes because of this?

Drexel University | Bruce Katz

FBT Project Finance Advisors + Right2Win Cities | Frances Kern Mennone

WORK-FROM-HOME / CHOOSING FLEXIBILITY

Employees are increasingly demanding flexibility and choice for where (and when) they work. What strategies can landlords implement to adapt?

Union Investment Real Estate | Tal Peri

TALENT AND RECRUITMENT / TALENT PARITY

To be better prepared for future risks, firms need diverse talent. So is the goal of 50% female representation achievable in global real estate investment and asset management firms?

Sheffield Haworth | Isabel Ruiz

CLIMATE CHANGE / PREDICTING THE CLIMATE FUTURE

We are all invested in the cities, assets, and infrastructure of tomorrow, even if we might not live to see the ten largest cities in 2100. But understanding climate change can get us closer.

Climate Core Capital | Rajeev Ranade and Owen Woolcock