The “great sag” in the US office market—and potential underlying financial fragilities—do not necessarily portend the calamity popularly forecasted by today’s market skeptics.

The confluence of several dynamics—some of which predated the pandemic, some of which have been exacerbated during pandemic, and some of which have emanated from recent banking wobbles—have led some market participants to portend a coming “Armageddon” in the office segment of commercial real estate.1

In the US, the secular shifts to remote and hybrid working jolted the real estate industry, as many leading investors and developers wondered whether demand would ever recover for office space (and for office-anchored retail). Looking to the supply side, the US market is particularly beleaguered by a glut in Class B office stock—that is, ossified office buildings, many of which were constructed in the aesthetically-lean 1970s. Given the datedness of these edifices, much of US Class B office stock has been historically starved of capital and is thus largely ill-equipped to cater toward changing patterns of demand for ESG and technology-driven working spaces.

On the financial side, recent bank wobbles have laid bare the exposure of some small lenders to CRE assets and debt—particularly those in the office and office retail landscape. An interest rate rise environment and concerns about the trajectory of economic growth—combined with the impacts of the structural shifts to teleworking—had already brought lending to a standstill in Q4 2022.

Thus, even prior to the bank collapses in March 2023, lenders were largely unwilling to deploy capital to a sector undergoing secular shockwaves, and potentially for overvalued assets.

Indeed, asset price inflation which predated the pandemic has continued—and is even applicable to afflicted sectors such as office buildings. Amidst an elevated price backdrop, we are currently operating in a frozen market in the US (unlike in Europe, as we explore below), with a lot of room for price discovery between buyers and sellers. As larger US lenders reduce their exposure to CRE and signal potential losses on the horizon,2 any meaningful dip in prices—combined with a cascade of delinquencies—could trigger an overt loss of confidence in the US CRE market. Hence, looking beyond the bank wobbles—which appear to be contained—the proverbial “other shoe” might well drop.

THE OPPORTUNITY: RETHINK AND REIMAGINE

Nevertheless, as these two authors maintain, the “great sag”—and potential underlying financial fragility—with US office stock does not necessarily portend the calamity that others have forecasted. In terms of the market outlook, although we are likely to witness geography and asset-specific pockets of distress, this does not appear to spell a reprise of the “all boats overboard” moments of 2008 and the GFC.3 And, at the asset level, the fact that the American office market is a laggard vis-a-vis European peers actually presents an opportunity for equity-heavy investors—especially those well-poised in the prop tech space, to equip properties for climate resilience via savvy digital adoption.

The smartest capital is likely to be deployed to the most vibrant central business districts (CBDs)—the deployment of which creates a distinct opportunity for the next cycle.

Rethinking and reimagining our business communities is not the sole preserve of real estate developers; forward-thinking municipal authorities, as well as infrastructure investors, will have a significant role to play. As we equip our cities and buildings for climate resilience and for new ways of working, prop tech investors will also be presented with significant opportunities for scaling their investments—in an age of secular shocks, this might be termed ad-venture capital! Lastly, as we conclude, reimagining our professional urban environments will require improvements in public safety—a critical and decisive factor in determining the attraction of specific markets for durable investment over a long horizon.

THE FINANCIAL PICTURE: US CRE AND POTENTIAL POCKETS OF INSTABILITY

Since the start of the COVID-19 pandemic and the rapid adoption of remote working by many tenants of CBD office space, many of the world’s most prominent investors have voiced their concerns about steep losses in the office sector. In spring 2020, our forecast was that many white-collar services jobs would converge toward a three-day office work week, which might result in about a 10% decline in footprint—and hence a meaningful drop in prices. Over three years later—and amidst a widespread adoption of hybrid working for many CBD office tenants—we’ve not yet witnessed a significant plunge in asset prices in the US market, where prices remain elevated.4

By contrast, looking across the Atlantic, transaction volumes in the European CRE market have held relatively steady throughout the pandemic economy years,5 and some investors have already taken their mark to market losses. Unlike in the US, assets are still trading, and notwithstanding potential pockets of overvaluation in some key cities, the office building stock is arguably markedly better in European markets, as many structures were built to stand the test of time.

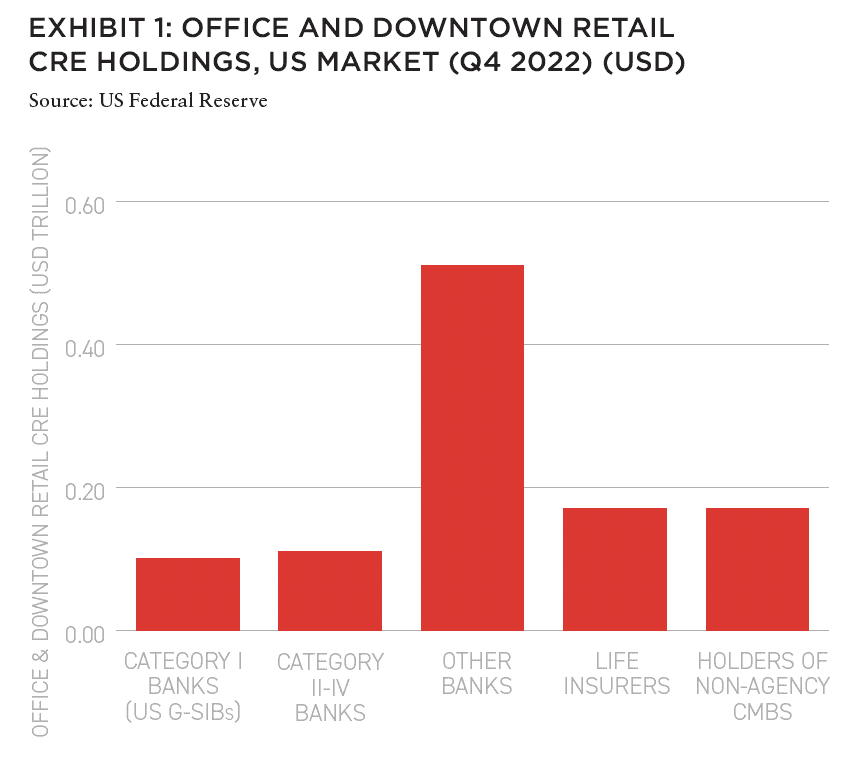

The onset of the recent bank wobbles in the US—reverberating through portfolios in recent months—have cast a shadow of doubt of whether such a moratorium on price discovery can continue, at best—or indeed whether the US CRE market might be the locus of the next wave of financial distress. Many have pointed to the linkages between the smaller banks in the US and the CRE landscape. As we can see in Exhibit 1, the country’s smaller lenders have deep exposure to office and office-adjacent retail, in contrast with America’s larger banks, where such assets make up a more modest component of total portfolios.

Our base case is that the wave of consolidation amongst the smaller banks in the US remains contained. However, some of these lenders have already commenced offloading loans at a loss, signaling the potential for writedowns and hence a softening of prices across the office landscape.6

Also, in contrast with the European market, a potentially worrisome development—and a feature of the unique hyper-financialization of the US market—is that of securitization and US CRE.7 Although CMBS’s are not as dominant in the pre-GFC heyday, non-agency holders of CMBS still comprise 15% of outstanding CRE loans to office and office-anchored retail in the US, and hold about half a trillion dollars’ worth of assets in the space.8 These are not insignificant numbers. The problem with securitization is that it implies liquidity—and in the event of defaults or delinquencies as some office-related loans reach maturity—the CMBS market is prey to redemption risk,9 and hence may spur bouts of financial instability. Although ripple effects in the market may not become a torrent or a cascade—or a proverbial bubble bursting—a loss of confidence—precipitated by softening prices, or a rush to the exit of office-related CMBS—may be enough to create distress (and hence opportunities for alternative forms of credit, thus prolonging the trend of financialization!).

THE ASSET PRICE LANDSCAPE: MARKET-TO-MARKET LOSSES?

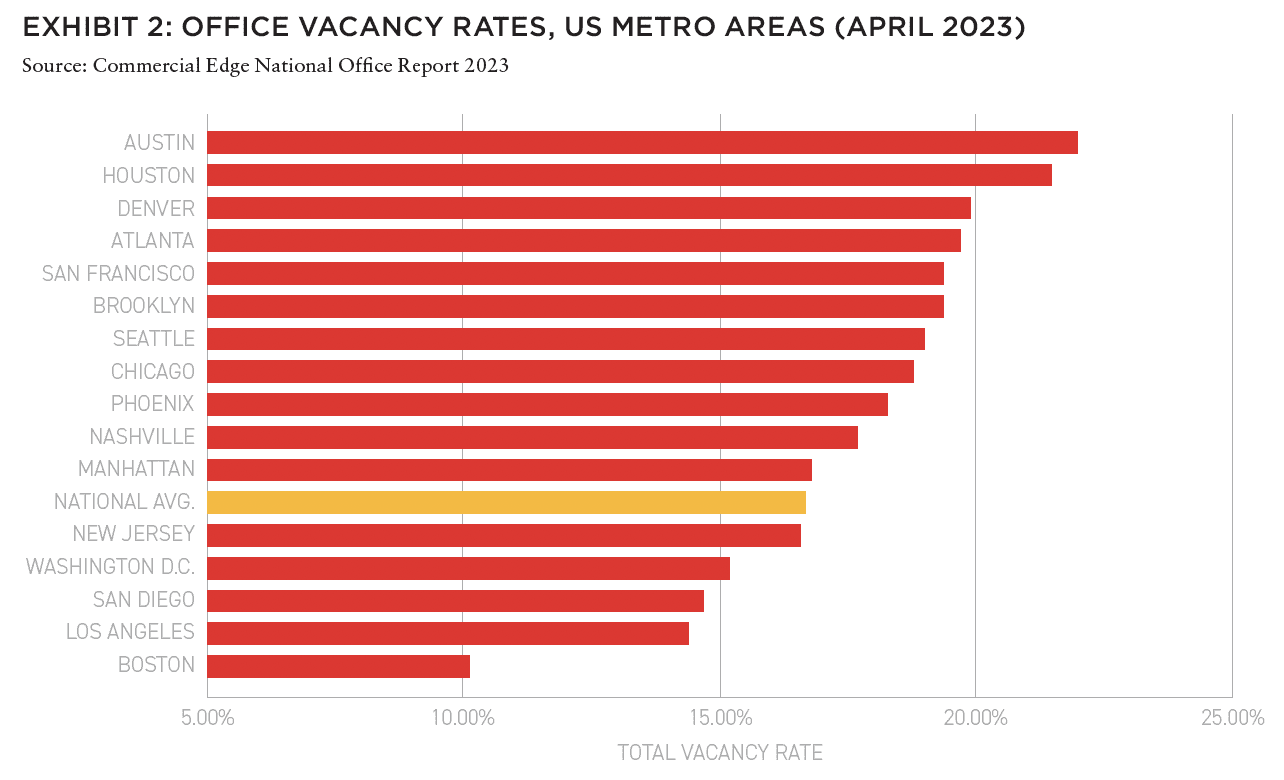

The potential for such distress to emerge in the US CRE landscape is likely to differ from market to market, with the potential for sharp divisions even within specific markets. For example, much Sturm und Drang has been made about the fate of office space in downtown Los Angeles (DTLA),10 but Century City remains a “shining star” as professional and legal services firms flock to the submarket’s Class A buildings.11 As we can see in Exhibit 2, vacancy rates remain high in tech-heavy CBDs, including San Francisco and Austin. Vacancy rates are also elevated in cities which continue to confront public safety issues, such as Chicago.

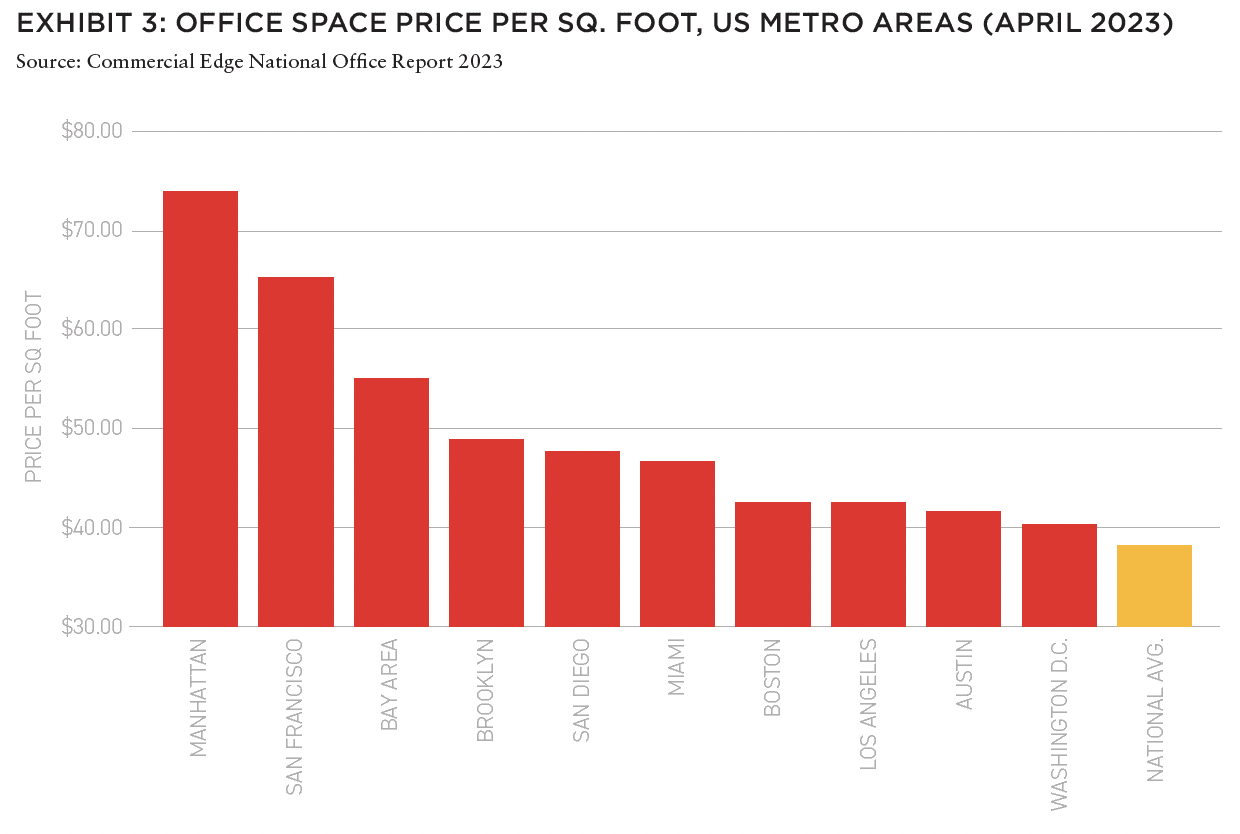

However, on the valuation front, asset prices remain significantly elevated—even in some of the hardest-hit CBDs, such as San Francisco. Office buildings in the Golden Gate city still command some of the highest prices in the US, usually standing neck and neck with Manhattan (Exhibit 3).

The spread between prices and vacancy rates in secularly hard-hit CBDs such as San Francisco means that the other shoe may eventually drop. The trigger might be a wave of defaults on one CBD, which might then have a domino effect on markets which are overpriced, over-crimed, and under-leased.

AT THE ASSET LEVEL: FLIGHT TO QUALITY

As indicated above, America has a Class B problem related to its existing office stock. A refusal to acknowledge obsolescence predated the COVID-19 pandemic—has continued, even during the secular shocks from WFH, amidst an elevated price environment, and a frozen trading landscape.

Although some optimists have pointed to the potential for such ossified office buildings to be turned into residential units (thus also alleviating the issue of a chronic shortage of affordable housing in the US), the top affordable housing developers have cited the structural challenges of such conversions. What this means is that a significant portion of US Class B office buildings will be rendered obsolete: for these reasons, one prominent executive points to pockets of purgatory in the US office landscape, and estimates that as much of 20% of the market will “have the keys handed in.”12

By contrast, European office stock seems to be standing the test of time, as it increasingly caters toward investor preferences for environmental protocols and the “E” in ESG. This might be a function of the assets themselves (as buildings were constructed for la longue durée); the lending profile to these assets (given the fact European banks bear the lion’s share of exposure to commercial real estate assets,13 their portfolios are subject to mounting climate regulations and stress testing); investor preferences (such as mandates from pension funds); or a combination of the three.

Thus, European office stock is arguably better positioned to weather the climate storm—emanating from regulation and/or investor preferences—which stands in contrast with the overhang of class B office stock.

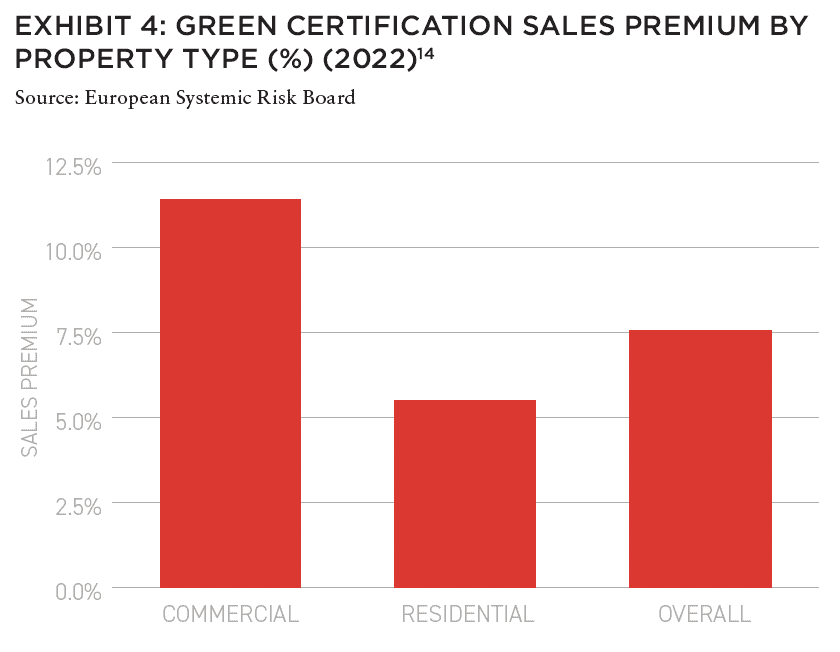

In fact, as we can see in Exhibit 4, an examination of sales data from markets across the globe (including the US) reveals that investors in commercial real estate are willing to pay a “green premium” for high quality assets which can fulfill certain environmental qualifications.

This suggests that an immense opportunity might unfold to rethink, reimagine, and potentially to future-proof America’s office stock for enhanced climate resilience, and to cater toward shifting winds of investor preferences.

DEMAND SHOCKS

In sum, in considering the demand shocks rendered to the US CRE market by the pandemic-induced shifts to telework, the verdict is still out on just how much space will be required by tenants in America’s CBDs.

As some prominent companies increase their requirements for return-to-office, others are actually increasing childcare offered on-site—with the belief that the ability for working parents to come to the office has a positive impact on productivity and well-being.15 Indeed, a close reading of data on productivity levels during the pandemic economy years evidences that the gains experienced in the early waves of COVID-19—when many white collar workers could work from home and thus save on commuting time—actually erodes over time, in part due to a lack of in-person collaboration.16

People need offices—in order to bind together as a professional and organizational culture—and need spaces to convene for whiteboarding, brainstorming, mentoring, and apprenticeship, as well as product education and socialization. Recognizing this need, and the continuing relationship between office space, professional culture, and productivity, we are hopeful that America’s current Class B problem—and pockets of potential financial instability—will actually open up an opportunity for the convergence between thoughtful city planning, cooperation between public, private and philanthropic interests, evidence of which we have witnessed in thriving urban centers including Dallas,17 Nashville, Salt Lake City, and Indianapolis.

Lastly, any bouts of financial distress—or severe losses in the office and office-anchored retail space—set against the backdrop of a higher rate environment—might just yield the advent of opportunistic funds, and alternative forms of credit, to step in where the markets have retracted.18 This might be termed ad-venture capital, for those courageous enough to take advantage of a potential reversal in the market—for future cycles in the built environment.

REVIEWER RESPONSE

More than three years after the pandemic upended our collective relationship to the built environment, the debate over the future of the office sector continues unabated. As vacancy rates have climbed and many sources of financing have retrenched, popular assessments of the office outlook have turned increasingly grim. Well-worded estimates of value declines are assured their readership, but often with little attention to the reasonableness of their underlying assumptions or thought to solutions. Similarly, a recent spate of highly visible investments in Manhattan and other legacy markets have been styled in contrarian terms, ignoring the bifurcation of competitive and uncompetitive assets.

In this careworn environment, Crow and Carlock offer welcome perspective, summarizing the facts on the ground but also turning the focus to how investors and operators can navigate the reality of offices’ changed position in our economy’s post-pandemic production function.

Among their most salient arguments, successfully rethinking offices will require alignment across a broad range of stakeholders than just real estate. Apart from property owners and developers, local governments must adopt bolder, more creative, and more flexible approaches to the design of the built environment and policies—in areas ranging from taxes to infrastructure—that have the potential to undermine or enhance the strength of urban agglomeration.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #13

Benjamin van Loon | AFIRE

OFFICE TROUBLES: FINANCIAL RISKS AND INVESTING OPPORTUNITIES IN US CRE

Dr Alexis Crow | PwC + Byron Carlock

THE UNDERPERFORMANCE PARADOX: WHY INDIVIDUAL INVESTORS FALL BEHIND DESPITE BUYING LOW

Ron Bekkerman | Cherre + Donal Ward | Tenney 101

CLIMATE THREAT: EXTREME WEATHER IS THE NEW NORMAL FOR REAL ESTATE

Jacques Gordon, PhD | MIT

CLIMATE OPPORTUNITY AWAITS: HOW REAL ESTATE CAN INVEST IN CLIMATE ADAPTATION

Michael Ferrari, PhD and Parag Khanna, PhD | Climate Alpha

PREMIUM PRICE TAGS: INSURABILITY THROUGH PROPERTY RESILIENCE DATA

Bob Geiger | Partner Engineering & Science

REAL ESTATE WEB3: THE EMPEROR’S NEW CLOTHES OR THE NEXT BIG THING?

Zhengzheng Tan, Alice Guo, and Naveem Arunachalam | MIT

ADAPTIVE TO REUSE: COULD BUILDING CONVERSIONS BE DIFFICULT, EXPENSIVE . . . AND STILL PROFITABLE?

Josh Benaim | Aria

RENOVATE, REBRAND, REPOSITION: ADDING VALUE TO MULTIFAMILY THROUGH REVITALIZATION

Robert Kilroy, CFA | The Dermot Company + Will McIntosh, PhD | Affinius Capital

REDEFINING THE PROGRAM: A CONVERSATION WITH ARCHITECT DAVID THEODORE

Peter Grey-Wolf | Wealthcap + David Theodore | McGill University

SENIOR HOUSING UPDATE: EMERGING OPPORTUNITIES THROUGH DEMOGRAPHIC TAILWINDS AND DIMINISHING SUPPLY OUTLOOK

Robb Chapin, Jack Robinson, Andrew Ahmadi, and Morgan Zollinger | Bridge Investment Group

SENIOR HOUSING UPDATE: UNPRECEDENTED DEMOGRAPHIC ACCELERATION MAY DRIVE STRONG OPERATING FUNDAMENTALS AMID ECONOMIC SLOWDOWN

Tom Errath | Harrison Street

HOLIDAY FROM HISTORY: REASONS FOR US OPTIMISM IN A CHANGING GLOBAL ENVIRONMENT

Charlie Smith | Newmark

CRADLE TO CRADLE: AN ALLOCATOR’S VIEW ON IMPLEMENTING ESG INITIATIVES

Christopher Muoio and Katie Cappola | Madison International Realty

FREE LUNCH: MULTI-DIMENSIONAL DIVERSIFICATION IS A FULL-COURSE FREE MEAL

Elchanan Rosenheim and Tali Hadari | Profimex

CAMPAIGN MESSAGING: CFIUS, AFIDA, AND EXPANDING FEDERAL AND STATE RESTRICTIONS ON FOREIGN INVESTMENT IN US REAL ESTATE

Caren Street, John Thoms, and Anya Ram | Squire Patton Boggs

—

ABOUT THE AUTHORS

Dr. Alexis Crow is Head of Geopolitical Investing for PwC. and Byron Carlock is a Board Member with Accordant Investments and Demetree Global.

—

NOTES

1 For soothsaying from one of the world’s most prominent investors, see https://www.ft.com/content/da9f8230-2eb1-49c5-b63a-f1507936d01b

2 https://www.ft.com/content/3e905e3c-697c-4109-bd9a-605e75a0cfa4

3 In part due to regulation implemented in the wake of the last crisis, the US GSIBs are in much better standing, and CRE holders and lenders have healthier LTV ratios.

4 The US Federal Reserve continues to point to elevated prices across the RE landscape in the US, including office and office-anchored retail. See, for example, https://www.federalreserve.gov/publications/files/financial-stability-report-20230508.pdf

5 See chart 2, page 11. https://www.esrb.europa.eu/pub/pdf/reports/esrb.report.vulnerabilitiesEEAcommercialrealestatesector202301~e028a13cd9.en.pdf

6 https://www.ft.com/content/3e905e3c-697c-4109-bd9a-605e75a0cfa4 ; See also: https://www.reuters.com/business/finance/overexposed-us-regional-banks-could-sell-commercial-property-loans-2023-05-17/

7 It should be noted that although CMBS is not a feature of the European office debt landscape, the potential for liquidity mismatches in open-ended CRE funds does raise concerns for financial stability. See: https://www.esrb.europa.eu/pub/pdf/reports/esrb.report.vulnerabilitiesEEAcommercialrealestatesector202301~e028a13cd9.en.pdf Pg. 34.

8 https://www.federalreserve.gov/publications/files/financial-stability-report-20230508.pdf

9 https://www.bloomberg.com/news/articles/2023-06-08/delinquent-office-loans-at-five-year-high-trouble-cmbs-market

10 See, for example, https://www.wsj.com/articles/brookfields-los-angeles-office-company-is-roiled-by-defaults-37ac5751?mod=Searchresults_pos6&page=1 ; https://www.ft.com/content/ecb9201a-b0ed-4ea2-9268-188705abb7ea#post-bd74773d-e5e0-484d-8cdd-07d109fa1b73

11 https://labusinessjournal.com/real-estate/the-real-estate-quarterly-difficulty-leasing/

12 https://www.bloomberg.com/news/articles/2023-06-07/pgim-ceo-sees-60-of-office-real-estate-market-in-purgatory

13 In terms of lending as well as asset exposure. See, for example, chart 4, https://www.esrb.europa.eu/pub/pdf/reports/esrb.report.vulnerabilitiesEEAcommercialrealestatesector202301~e028a13cd9.en.pdf

14 Original meta-analysis examines sales in the US, UK, Japan, Sweden, Australia, Singapore, Spain, Canada, China, France, Germany, Hong Kong, Netherlands, and Switzerland by Dalton and Fuerst (2018)

15 See, for example, https://www.wsj.com/articles/more-companies-start-to-offer-daycare-at-work-95d267bb

16 Gordon and Sayed, “A New Interpretation of Productivity Growth Dynamics in the Pre-Pandemic and Pandemic Era U.S. Economy, 1950-2022”

17 For one imaginative conversion of Class B office, see One Main Place in Dallas: https://www.dallasnews.com/business/real-estate/2015/01/13/downtown-dallas-one-main-place-tower-will-house-new-westin-hotel/

18 See, for example, https://www.bloomberg.com/news/articles/2023-05-01/apollo-s-rowan-says-next-stress-wave-is-commercial-real-estate; https://www.bloomberg.com/news/articles/2023-01-23/europe-is-bracing-for-a-sharp-and-abrupt-real-estate-reversal

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY UNDERWRITTEN BY

For more than 20 years, Yardi has developed real estate investment management software that helps managers of global assets valued at trillions of dollars make informed investment decisions. Yardi Investment Suite clients include many of the world’s premier investment management funds, start-ups and partnerships of all types and sizes.

Real estate investments grow on Yardi. That’s because the Yardi Investment Suite automates complex investment management processes and provides full transparency, from the investor to the asset. Through interactive dashboards, investors can view documents and have access to reports and metrics. Collaboration is easy when your advisor or accountant is given access to view your accounts, reducing the need for emailing sensitive information.

The Yardi Investment Suite leads the real estate industry through innovation and value with fully integrated investment management, property management and accounting functionality. Fund managers and their customers can manage assets with superior efficiency and ease. Learn more.