Expenses generally rose at a faster rate over the past several years than in the years prior to COVID. Above-trend increases are expected over the next year, as well. The greatest increases were experienced by industrial properties; however, this was more than compensated for by robust income growth. Multifamily, also experienced substantial expense growth, but did not achieve offsetting income increase. The increases experienced by office building were relatively minimal – likely because buildings are currently occupied to only a fraction of the level of several years ago.

Effective Gross Income (EGI) is just one of the two components of Net Operating Income (NOI).1 Although an obvious truism, expenses are often less of a focus than income. Operating expenses have surged over the past several years. According to our analysis of aggregated operating expense data on a per square foot basis for properties within the NCREIF Property Index, apartment, industrial, and office expenses rose, on average, 5.7%, 5.9%, and 5.5% annually over the past two years compared to the compound annual growth rate (CAGR) of 4.5%, 1.1%, and 3.6% over the 18-year period ending Q2 2019.2 Retail expenses were held down during the pandemic time period when non-essential retailers were closed, so it may be best to analyze the expense increases in this sector over the four-year period from Q2 2019 to Q2 2023. Retail expenses rose on average 3.8% annually over the past four years compared to the historical compound annual growth rate of 3.6% over the 18-year period ending Q2 2019.

The higher the operating expense ratio (OER), the more sensitive the property’s NOI is to declines in EGI.3 Accordingly, hotels and to a lesser extent offices are the most sensitive. Property types with low OERs such as logistics and self-storage facilities are the least sensitive. In the middle are multifamily and retail properties.

Expenses generally rose at a faster rate since Covid, relative to previous years and, except for industrial, have exceeded rent increases. As a corollary, OERs are up for all major property types except the industrial sector. For a time during the pandemic, rent increases on multifamily exceeded operating expense increases – but that is no longer true. Above-trend increases are expected over the next year as well and will likely outpace revenue growth. Ultimately – expense reimbursement clauses embedded in industrial, retail and office leases do not help because gross rent will need to adjust to maintain market levels.

The greatest expense increases over the past four years were experienced by industrial and multifamily properties. The increases experienced by office and retail facilities were lower, but consequential, considering the anemic rent growth in the sectors. Warehouse facilities exhibited significant increases, however, from a low base as logistics properties have relatively few expenses. Lodging facilities had the greatest swings in expense levels because they were shut down during COVID and the expenses increased substantially as they reopened. Wages for staff at hotels grew faster than for any other category of employment.

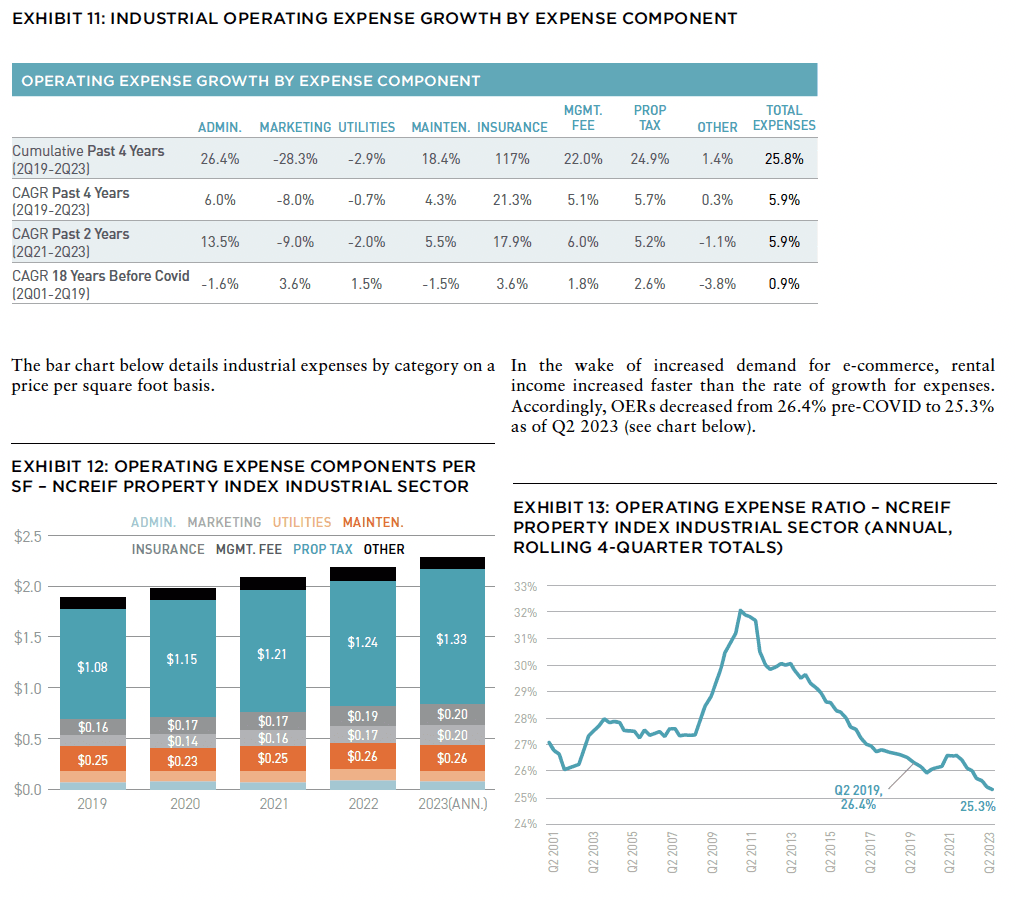

Although a relatively small portion of overall expenses, insurance has grown faster than all other expense categories.4 Other major expense growth contributors include utilities, maintenance and administrative costs. Property taxes – almost always the largest expense category – has increased the most in the industrial sector.

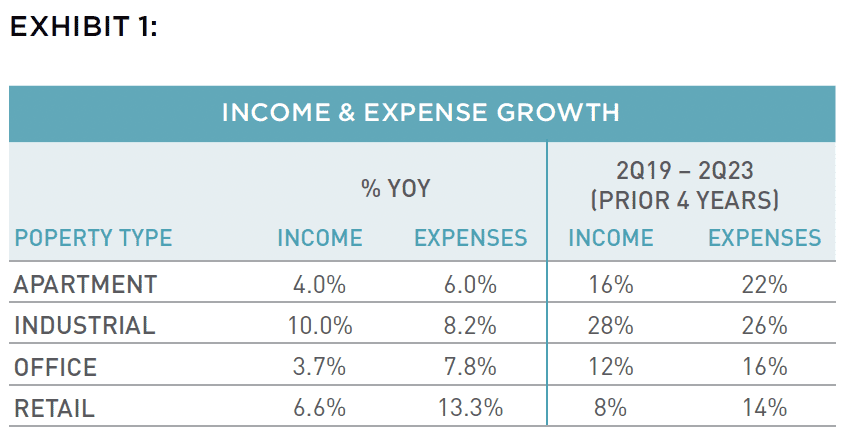

Exhibit 1 details cumulative growth of property-level income and expenses per square foot over the past one and four years. The industrial sector was the only to experience income growth in excess of expense growth over both time periods.

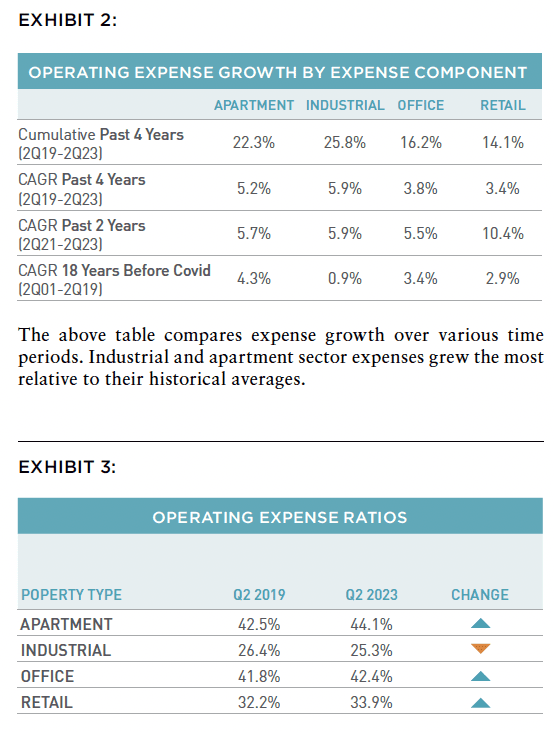

Exhibits 2 and 3 compare the change in average OERs by property type. Decrease in industrial sector OER is indicative of expense growth in excess of income growth over the past four years.

We will now further analyze expenses for each of the major property types.5

APARTMENT

We begin with the apartment sector which has been highly impacted by expense increases. During the four quarters ending 2Q 2021 multifamily rents decreased by 0.9%, while expenses grew 7.9%. However, during the four quarters ending 2Q 2022 multifamily rents increased by 14.4%, far outstripping expense increases of 5.3%. In the past year, expenses have risen 6.0% while income increased 4.0%. The apartment sector has exhibited income and expense growth since Q2 2019 growing a cumulative 16% and 22%, respectively. It is likely that expenses will continue to rise faster than trend over the next two years which could result in even higher OERs.

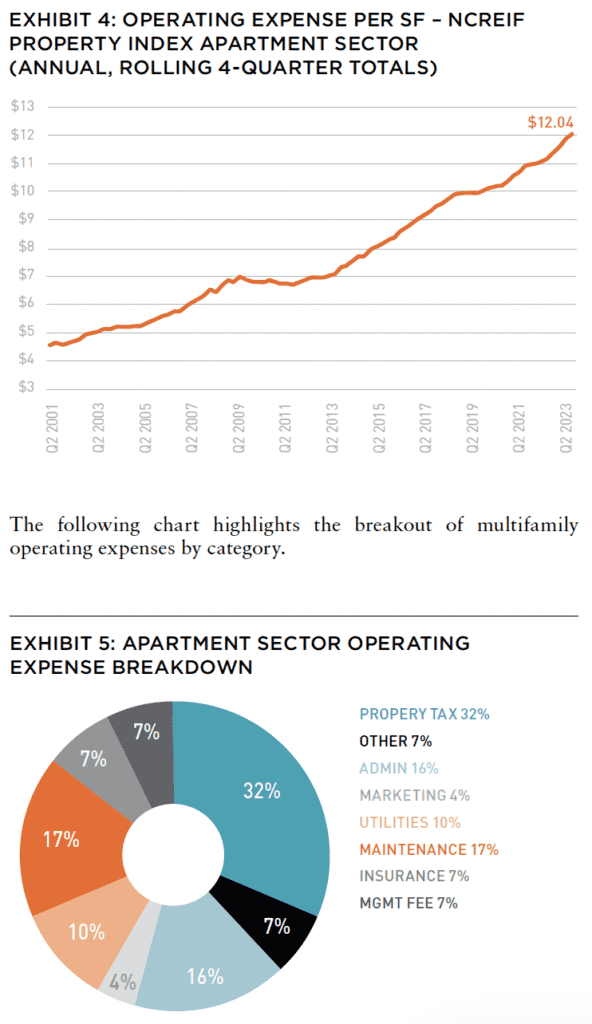

Exhibit 4 details the growth of operating expenses of multifamily properties over the past 22 years.

Since Q2 2019, apartment expenses have increased a cumulative 22%, with the greatest rise experienced by insurance at 156%. The causes of insurance increases include 1) the accelerated rate of climate events6, 2) higher replacement costs, 3) and regulatory pressure in the insurance market. Rates vary based on location and their exposure to climate events and their severity. Other increases include property taxes (13%), administrative (24%), utilities (23%), maintenance (22%). Property taxes represents the largest share of expenses, but its growth of 3.0% CAGR over the past four years is lower than the 6.5% average (CAGR) over the 18 years ending in 2019, muting its impact. The greater movement in administrative, utilities, maintenance expenses, which constitutes 45% of apartment expenses, resulted in a far greater impact.

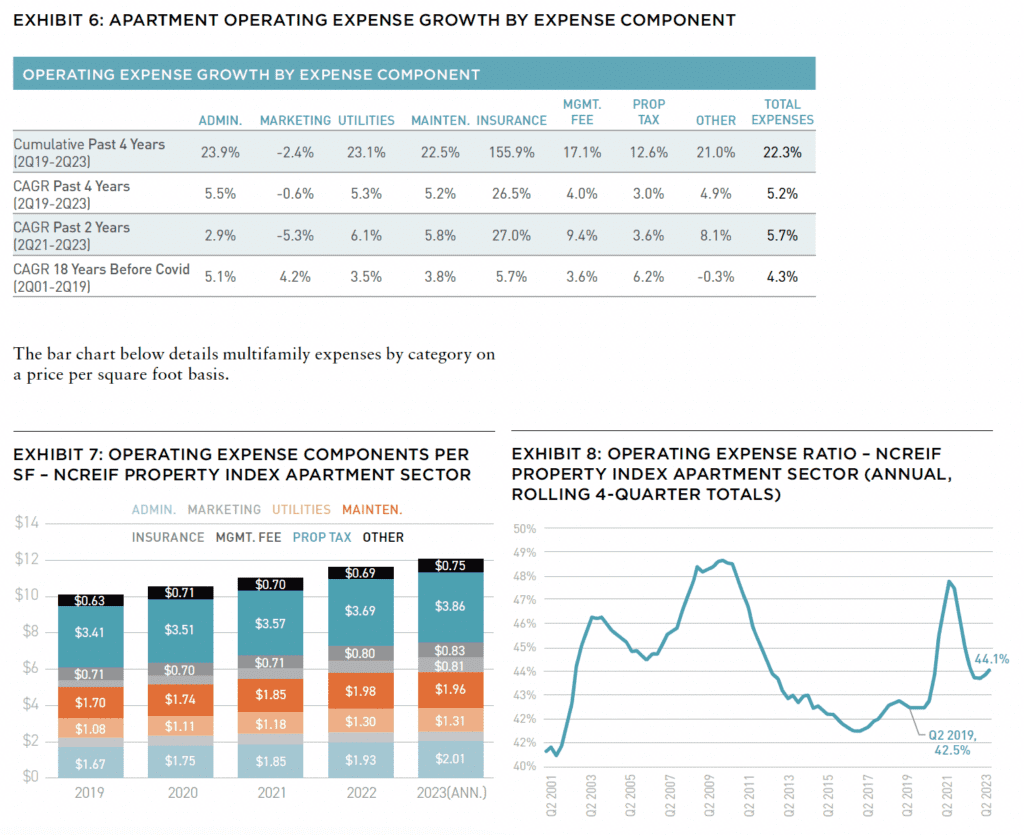

Exhibit 6 details expense increases by category during distinct time periods.

When income does not keep up with expense growth, OERs increase. This renders property cash flows more vulnerable to downturns and increases the chances of a default. The OER for the apartment sector increased from 42.5% pre-COVID to 44.1% as of Q2 2023. In the interim, the OER had increased to nearly 48% since some tenants did not pay rent and in other cases, rent had declined, while expenses increased. As the pandemic continued, migration patterns to the Sunbelt accelerated and demand outstripped supply, resulting in higher rents and lower operating expense ratios. Developers responded to this demand by adding units, which has recently put downward pressure on rents while expense growth has remained elevated.

INDUSTRIAL

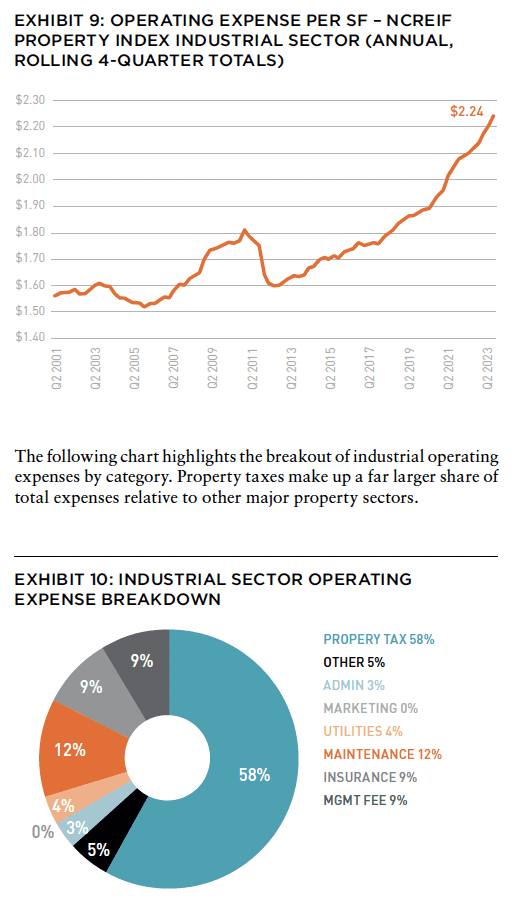

The industrial sector has exhibited the most income and expense growth of the four major sectors since Q2 2019, growing a cumulative 28% and 26%, respectively. In the past year, expenses have risen 8.2%, while income increased 10%. It is likely that expenses will continue to rise faster than trend in the next two years, resulting in higher OERs. Most industrial leases are written on a net basis and are, accordingly, reimbursed by the tenant. Nevertheless, expense increases add to the overall tenant rent burden. Should the total rent cost grow beyond market, base rents would need to be reduced to compensate.

The following chart details the growth of operating expenses of industrial properties over the past 22 years.

Since Q2 2019, industrial expenses have increased 26% with the greatest rise experienced by the insurance expense category at 117%. Other increases include property taxes (25%), administrative (+26%), maintenance (18%). Property taxes represents the largest share of expenses, and its average growth of 5.7% CAGR over the past four years is higher than the 2.6% average over the 18 years ending in 2019, which is reflective of the increase in values spawned by the growth of e-commerce.

Exhibit 11 details industrial expenses by category on a price per square foot basis.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

OFFICE

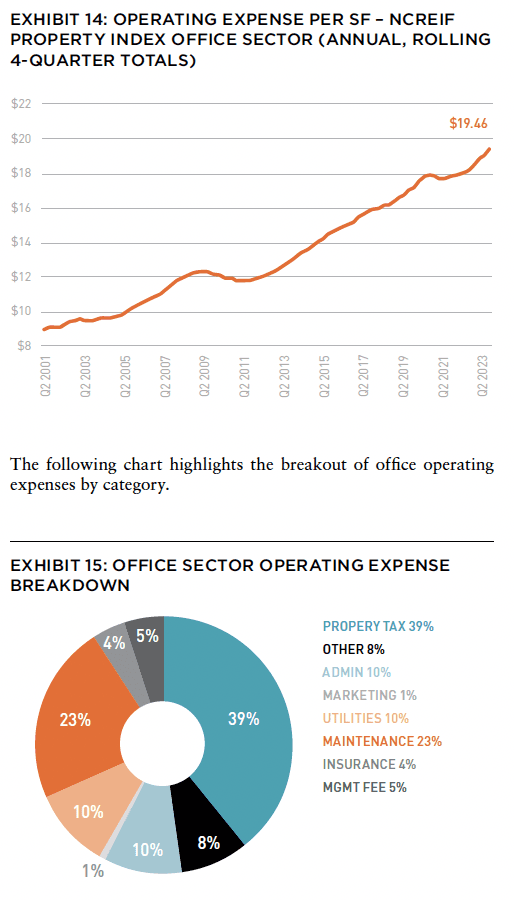

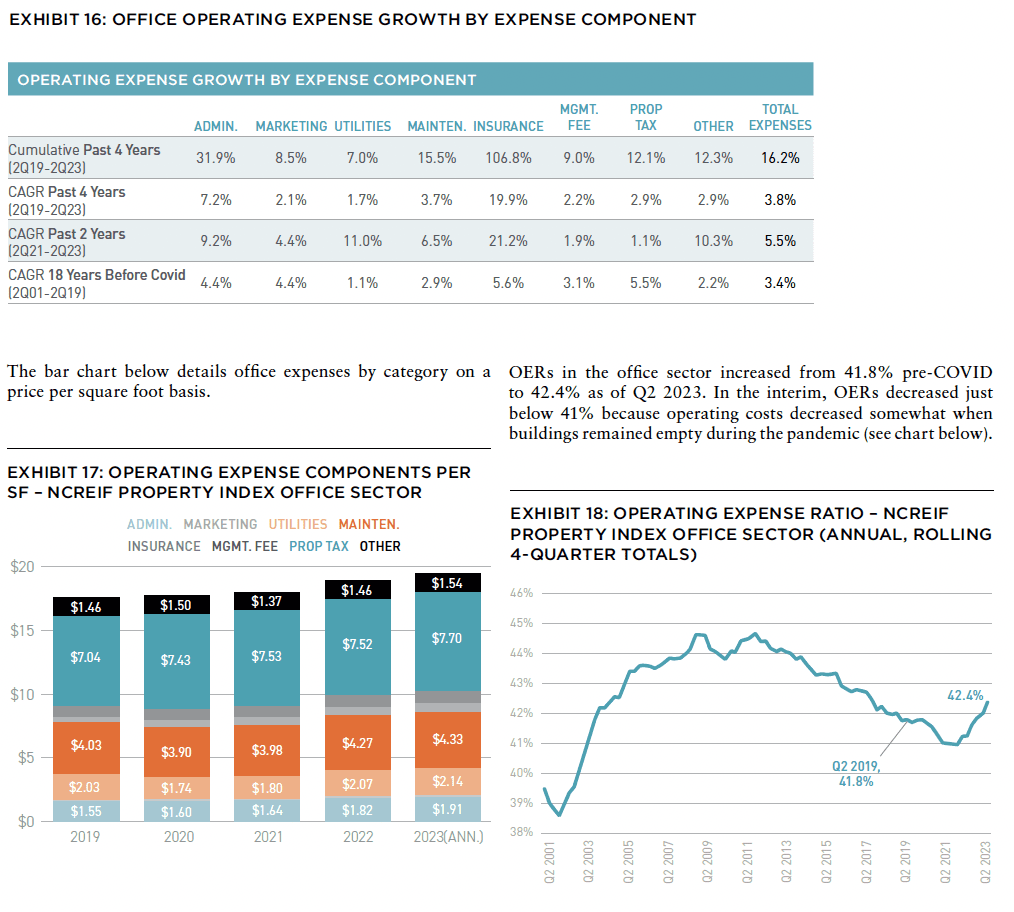

The office sector has exhibited cumulative income and expense growth since Q2 2019 of 12% and 16%, respectively. However, in the past year, expenses have risen 7.8% while income increased 3.7%. It is reasonable to assume that expenses will continue to rise faster over the next two years and result in higher OERs. Ultimately – expense reimbursement clauses included in office leases do not compensate for expense increases because base rent will have to adjust to keep it at market levels.

Exhibit 14 details the growth of operating expenses of office properties over the past 22 years.

Since Q2 2019, office expenses have increased 16% with the greatest rise experienced by insurance at +107%. Other increases include property taxes (12%), administrative (+32%), and maintenance (15%). Property taxes represents the largest share of expenses, but its average growth of 1.1% CAGR over the past four years, lower than the 5.9% average over the 18 years ending in 2019, muted its impact. The addition or upgrade of certain protective equipment and other measures during Covid may have added to expenses for certain properties. Overall, office values have been negatively impacted by elevated remote work in the wake of the pandemic.

RETAIL

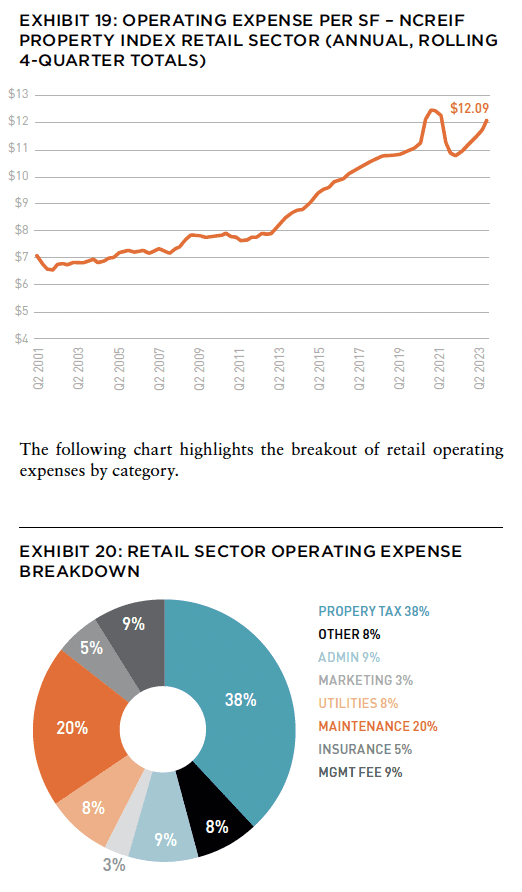

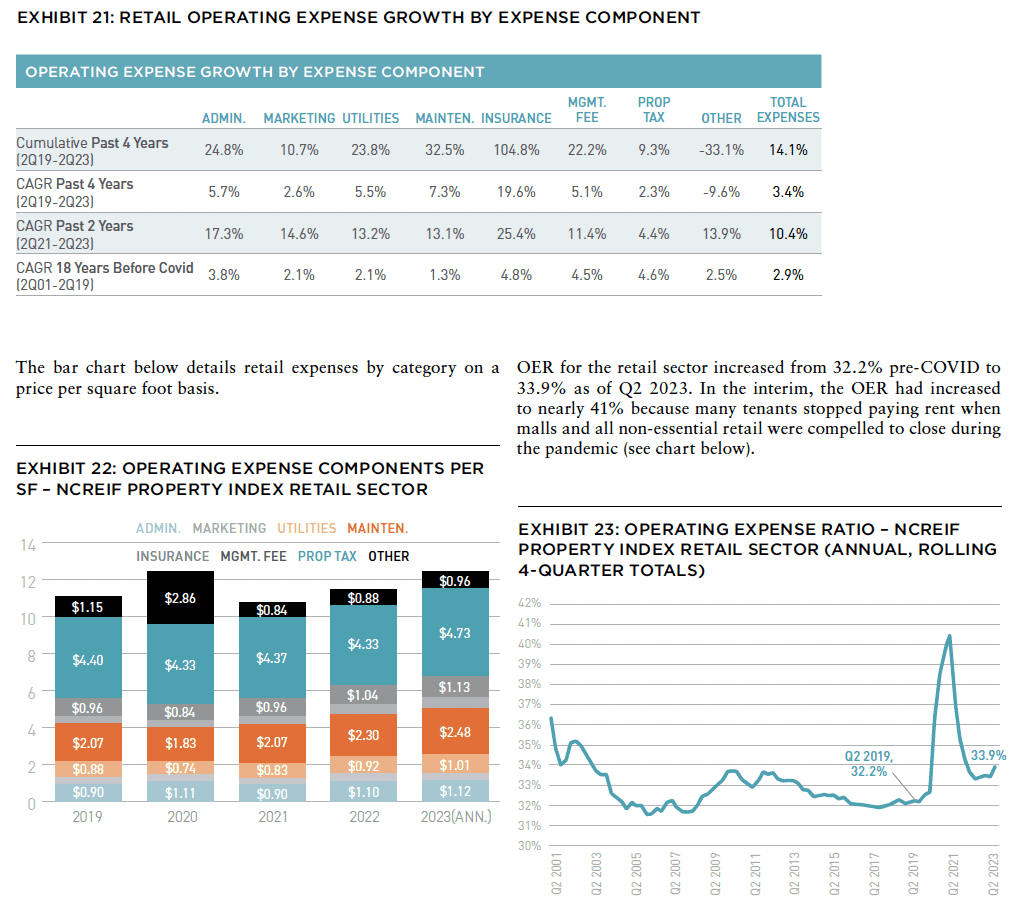

The retail sector has exhibited cumulative income and expense growth since Q2 2019 of 8.0% and 14.1%, respectively. However, in the past year expenses have risen 13.3% while income increased 6.6%. It is reasonable to assume that expenses will continue to rise faster in the next two years and result in higher OERs. Ultimately expense reimbursement clauses included in retail leases do not compensate for the increases because base rent will have to adjust to keep it at market levels.

Exhibit 19 details the growth of operating expenses of retail properties over the past 22 years.

Since Q2 2019, retail expenses have increased 14.1%, the smallest increase amongst the four major property types. In terms of individual expenses, the greatest rise was experienced by insurance at +105% followed by maintenance (32.5%), administrative (24.8%), and utilities (23.8%). Property taxes represents the largest share of expenses, but its growth at 2.3% CAGR, lower than the 4.7% average over the 18 years ending in 2019, muted its impact.

REIT EXPENSES

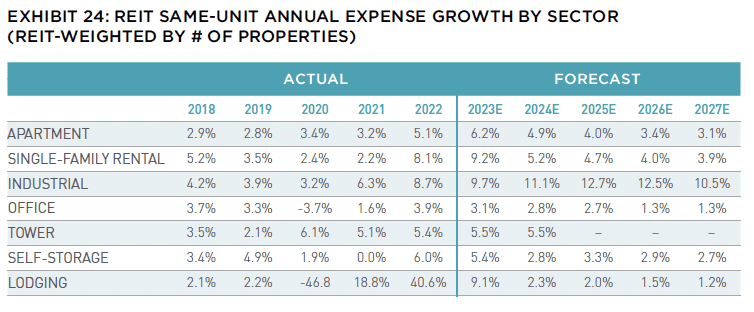

Operating expense increases for properties held in REITs reflect a similar trend. In addition, Green Street projects higher-than-trend increases for 2023 and 2024. Expenses are rising across the property type spectrum. Industrial has experienced the highest cumulative expense growth for a major property type. This is expected to continue, with the greatest increases forecast for the industrial sector through 2027.

Expenses generally rose at a faster rate over the past several years than in the years prior to COVID. Above-trend increases are expected over the next year, as well. The greatest increases were experienced by industrial properties; however, this was more than compensated for by robust income growth. Multifamily, also experienced substantial expense growth, but did not achieve offsetting income increase. The increases experienced by office building were relatively minimal – likely because buildings are currently occupied to only a fraction of the level of several years ago. Lodging facilities had the greatest swings in expense levels because they were shut down during COVID and the expenses increased substantially as they reopened. Warehouse facilities also exhibited significant increases, however, from a low base as logistics properties have relatively few expenses.

The higher the operating expense ratio (OER), the more sensitive the property’s NOI is to declines in EGI. Accordingly, hotels and to a lesser extent offices, are the most sensitive. Property types with low OERs such as logistics and self-storage facilities are the least sensitive. In the middle, are multifamily and retail properties.

—

ABOUT THE AUTHORS

Stewart Rubin is Senior Director and Head of Strategy and Research, and Dakota Firenze is a Senior Associate, for New York Life Real Estate Investors, a division of NYL Investors LLC, a wholly-owned subsidiary of New York Life Insurance Company.

—

NOTES

1. Net operating income is effective gross income less operating expenses.

2. NCREIF Property Index (NPI) is a quarterly, unleveraged composite total return for private commercial real estate properties held for investment purposes only. All properties in the NPI have been acquired, at least in part, on behalf of tax-exempt institutional investors and held in a fiduciary environment. Annual expense figures are based on compound annual rate of growth (CAGR) as of Q2 2023.

3. The operating expense ratio is the quotient of operating expenses divided by effective gross income.

4. Based on data from RealPage, U.S. apartment insurance costs went up by about 33% last year. In San Diego, for example, they only went up by about 8%. But in Jacksonville, insurance costs went up by about 65%.

5. Lodging is not included in this section because of the wild swings experienced during the pandemic.

6. See NYLREI Strategy & Research Group published articles by Stewart Rubin and Dakota Firenze, including: “Regulations and ESG: The Impact of Environmental Mandates on Commercial Real Estate”; “Rather than the Flood”; “The Midwest’s Blue Wildcard.”

—