With solid rental growth and a shift in pricing, investor appetite for the logistics sector remains relatively strong—and with these trends intact, the logistics sector is positioned to continue its outperformance.

Occupier demand for logistics space has fallen from the exceptional-yet-unsustainable levels seen during the height of the coronavirus pandemic. However, several structural drivers are in place that should provide tailwinds for demand.

For example, vacancy rates are likely to rise in the short term, but are largely expected to remain contained, and a pull back on construction is likely to result in the return of very tight supply conditions. In combination with high development costs and higher yields, this is projected to result in further, above-inflation, prime rental growth. Much of the outward shift in logistics yields has likely already occurred and, having repriced faster and earlier than other sectors in many markets, logistics yields will likely recover first. Unsurprisingly, investor appetite for logistics remains strong and, with trends intact, we expect the logistics sector to continue to outperform.

THINKING OF THE SLOWDOWN

Over the past few quarters, there has been a slowdown in the drivers of demand for logistics space, including the volumes of both global trade and retail trade. While the slowdown in demand has been partly related to increased occupier pessimism, because of continued geopolitical and economic uncertainty, in some markets it also reflects very tight availability, which means some occupiers are unable to secure the right space in the right locations. In combination with significant rental increases, this has resulted in more occupiers opting to renew or extend their existing tenancies.

However, lower levels of net absorption must be put in context: year-to-date net absorption as of Q3 2023 is still above the year-to-date ten-year average in many countries across the globe (for example in France, Italy, and the Netherlands).1

STRUCTURAL DRIVERS FOR OCCUPIER DEMAND

While occupier demand will continue to fluctuate with cyclical factors, several structural drivers remain in place, including growth in e-commerce and supply chain reconfiguration, both of which should provide tailwinds for demand.

The slowdown in occupier demand is partly due to lower demand for dedicated e-commerce fulfilment space. However, while e-commerce sales initially slowed from the heights achieved during the pandemic as consumers started to shop more in person and spend more on services and less on goods, they have been recovering in recent quarters.

Consumers are forecast to continue to increase the share of their shopping they do online over the next several years, with especially strong growth expected in countries where penetration rates are still relatively low, such as Italy, Spain, Malaysia, and Hong Kong.2 This should continue to be a tailwind for demand for logistics space, as e-commerce tends to require more warehouse space than store-based retail for the same volume of sales, reflecting factors such as higher labor intensity, higher volumes of returns, and increasing pressure to deliver goods in shorter time frames.

While the disruption seen during the pandemic has eased significantly, both occupiers and governments remain concerned about the resilience of supply chains. Hence, logistics occupiers are adopting strategies to minimize disruption and improve their overall supply chain sustainability, such as holding more inventory nearer to consumers or end users, diversifying suppliers, and reshoring and nearshoring production and suppliers. Several markets are experiencing an increase in the proportion of take-up related to manufacturing and automotive-related occupiers. In the US, for example, particularly strong demand has been reported recently in markets such as Dallas-Fort Worth, Austin, Nashville, and Phoenix —all of which also function as superior access routes to Mexico, which has recently overtaken China to become the US’ top trading partner. And while they are long-term changes that will take time to play out, reshoring and nearshoring are anticipated to continue to be a tailwind for the logistics sector, especially increasing demand near large population concentrations, manufacturing corridors, ports, and major air hubs

REGULATION, CONSTRUCTION, AND DEMAND

In some markets, regulatory pressure and company commitments are shifting logistics demand towards more sustainable locations and buildings.

Occupiers of logistics space are placing a greater emphasis on quality, with environmental factors increasingly important as businesses look to measure their Scope 3 emissions. Strong ESG practices and modern, well-specified logistics buildings have reportedly helped occupiers attract and retain staff, improve employee motivation, win new business, and reduce costs.

There is early evidence that energy efficient buildings can experience stronger occupier demand, spend less time on the market and achieve rental premiums. Conversely, not complying with counterparties’ ESG practices can result in contractual penalties, and occupiers may seek a discount for facilities that fail to meet their ESG requirements.

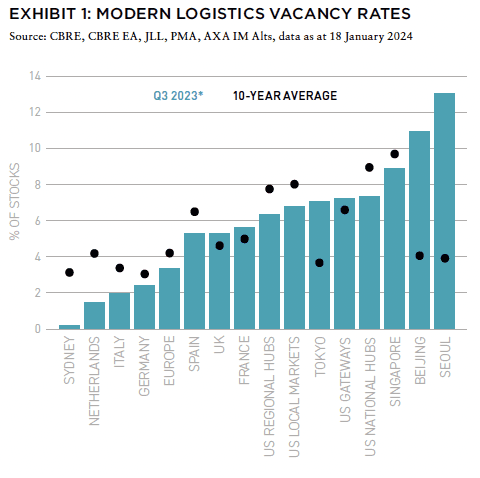

Unsurprisingly, given high levels of demand, low vacancy rates and low development financing costs, the volume of logistics space under construction increased in many global markets from 2020 to 2022. In combination with the recent slowdown in occupier demand, and some release of space for sub-lease, this has put upward upwards pressure on vacancy rates. However, this is typically from a very low base and vacancy rates are still below or near their ten-year average in most markets (Exhibit 1).

Additionally, the volume of space under construction has been falling for several quarters, reflecting lower confidence, still high construction costs, the more limited availability and higher cost of debt, and lower exit value assumptions. Construction starts also continue to fall. For example, starts in the US were at their lowest level for over two years in Q3 2023, having fallen over 64% year-on-year.3 While vacancy rates are likely to rise in the short term, availability is expected to remain contained. The pull back on new construction activity is likely to result in very tight supply conditions returning to some markets in the future. Some markets suffer from zoning and planning challenges that have kept development low for years – these challenges are largely unlikely to improve. For example, the European Union has set an objective of no net land take by 2050, which will potentially further reduce the logistics development pipeline and increase competition for already existing space. Buildings that cannot be retrofitted to meet minimum energy performance ratings and occupiers market standards face becoming stranded assets, putting further downward pressure on availability.

DELINEATING OCCUPIER DEMAND, RENT, AND DEBT

Despite higher availability, solid occupier demand for high-quality space resulted in continued prime rental growth across most major global logistics markets in 2023.

While growth has typically slowed from the double-digit levels seen in recent years, some markets have still experienced more than 10% rental growth since the end of 2022, including Los Angeles, Philadelphia, Minneapolis, Paris, Dusseldorf, Dublin, Manchester, Melbourne, and Sydney.4 The combination of a still tight demand-supply balance, lower development, high development costs and higher yields are projected to result in further, above-inflation, prime rental growth in many markets.

While the high levels of growth seen in recent years mean there are some concerns about affordability, rent is a relatively small proportion of total supply chain costs for many occupiers. For example, CBRE recently estimated fixed facility costs (including rent) typically account for 3–6% of total costs, whereas transportation costs represent 45–70%.5 It can be worthwhile occupiers paying a higher rent for an asset in a location that enables other supply chain costs to be reduced. Improvements to supply chain strategy can also increase revenue generation. For example, Amazon’s move from a national to a regional distribution network in the US has cut delivery times and shipping costs, increasing sales, and fueling higher third-quarter profits.6

Debt costs increased dramatically during 2022, largely reflecting rising swap rates rather than higher margins. In combination with geopolitical headwinds and a worsening economic outlook, this led prime logistics yields to rise sharply in most global markets. Nonetheless, there are differences between markets, with European cities typically seeing sharper outward yield shifts than those experienced in the US or Asia Pacific.7 While logistics yields are expected to increase further in some markets in the short term, much of the outward shift has likely already occurred. Indeed, logistics yields appear to be at or near stabilization point in many global markets, helped by a view that interest rates have peaked, some stabilization or even improvement in debt costs, and stronger investor demand. Having repriced earlier than other sectors in many markets, we project that logistics yields will recover first.

DEALING WITH HEADWINDS

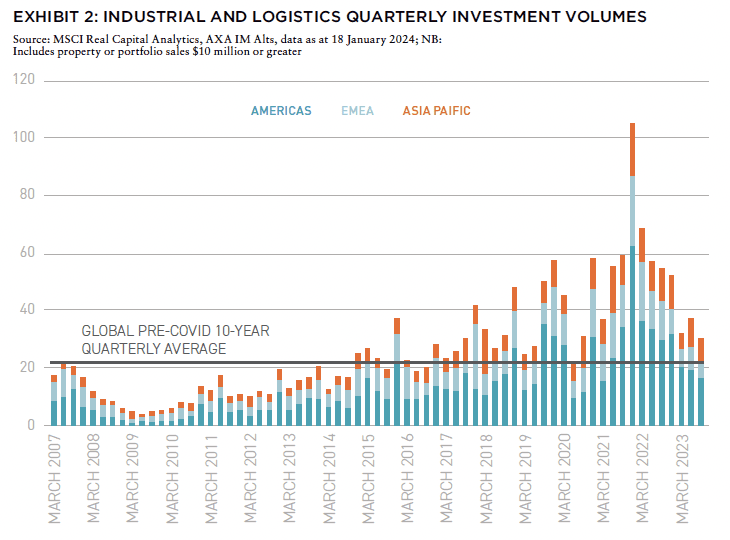

The combination of economic and geopolitical headwinds, rising logistics yields, and a turbulent lending market have resulted in investors taking a more cautious approach, pulling down industrial and logistics investment volumes since their peak in 2021. With less capital available, banks have been focusing on key relationships, core assets, and smaller deals, with funding for speculative development difficult. Transactions are taking longer to complete and there has been only a limited number of portfolio deals. Nonetheless, global industrial and logistics investment volumes remained well above their pre-COVID average throughout 2023, especially in the US and Asia Pacific (Exhibit 2).

In many global markets, logistics capital values repriced more quickly than in previous downturns or in other real estate sectors.8 These value declines reflect only outward yield shifts, as rental growth has remained strong. Unsurprisingly, investor appetite for the logistics sector remains relatively strong, underpinned by the combination of solid rental growth potential and the shift in asset prices, which is tempting back buyers, some of whom had previously been priced out of the market. With trends intact, we expect the logistics sector to continue to outperform.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

ABOUT THE AUTHORS

Kerrie Shaw is a Senior Research Analyst for AXA IM Alts.

—

NOTES

1. Referencing data from JLL; AXA IM Alts; data as of Q3 2023

2. Referencing data from PMA; forecasts as of Q3 2023

3. CBRE. “U.S. Quarterly Figures, Q3 2023.” CBRE Insights. https://www.cbre.com/insights/us-quarterly-figures. Accessed January 30, 2024.

4. Referencing data from JLL; CBRE; CBRE EA; PMA; AXA IM Alts; data as of 18 January 2024

5. CBRE. “U.S. Real Estate Market Outlook 2023.” CBRE Insights Books. https://www.cbre.com/insights/books/us-real-estate-market-outlook-2023. Accessed January 30, 2024.

6. CoStar. “Amazon Cites Warehouse Changes in Tripling Profit, Slashing Shipping Costs.” CoStar. https://www.costar.com/article/316365876/amazon-cites-warehouse-changes-in-tripling-profit-slashing-shipping-costs. Accessed January 30, 2024.

7. Referencing data from JLL; CBRE; CBRE EA; PMA; AXA IM Alts; data as of 18 January 2024

8. Referencing data from JLL; CBRE; CBRE EA; PMA; MSCI; AXA IM Alts; data as of 18 January 2024

—