Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do to fulfill the social and governance aspects of ESG expectations.

Gone are the days when investors considered “impact investing” separate from just “investing.” In virtually every industry, environmental, social, and governance (ESG) matters have moved from a peripheral concern to a core business pillar. Real estate is no exception.

Within real estate, the conversation around the environmental component of ESG is quite advanced—and with good reason, as real estate is one of the largest domestic sources of greenhouse gas emissions1 and embodied carbon2 in the developed world. The “E” of ESG also has well-defined assessment metrics, key milestones for decarbonizing, and a robust certification marketplace for verifying a building’s green credentials.

The social and governance (S&G) components, by contrast, have received comparatively little attention, until recently. The data landscape for these criteria is less mature and performance standards and key metrics are less widespread and less consistent, partly due to lack of high-quality data.

This article introduces a “stakeholder perspective” as a tool for real estate companies to use when assessing the most material ways in which their business interacts with S&G considerations. Due to the challenge of collecting data within S&G, companies can struggle with identifying how their business activities can address social and governance needs/issues most effectively. The aim of this article is to offer a different perspective from those prevalent in S&G discourse in order to advance thinking and practice in real estate. We contend that the stakeholder perspective is a useful framing device companies can use to ensure their S&G activities are material, high impact, and consistent.

S&G: TAKING A STAKEHOLDER PERSPECTIVE

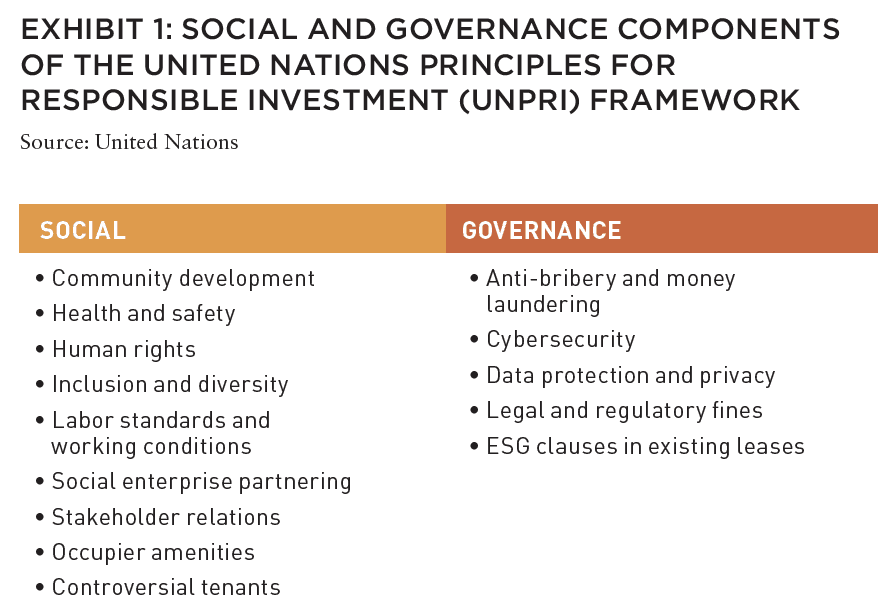

The United Nations Principles for Responsible Investing (UNPRI) in Real Estate outline the basis of S&G in ESG investing (Exhibit 1).

At a high level, the key social aspects of S&G are ethics, equity, and social cohesion, whereas governance focuses on legal matters and compliance with regulation. The UNPRI framework focuses on embedding ESG into the investment process from due diligence to acquisition, as well as holding through to disposition.3

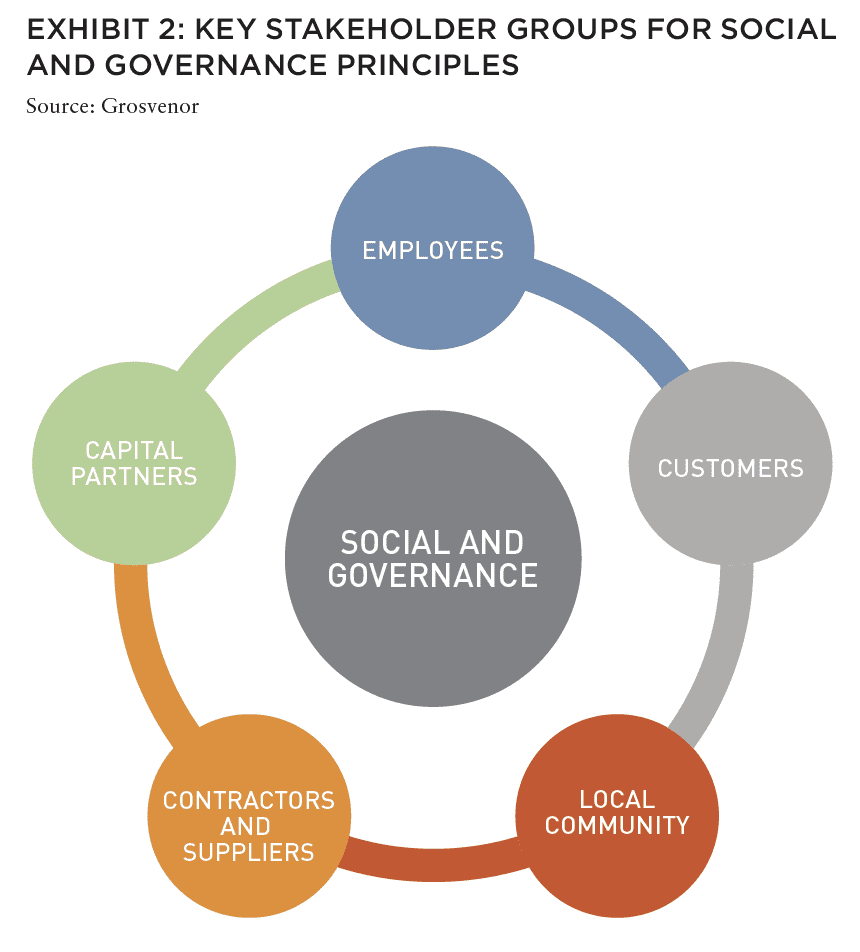

Rather than consider S&G from an operations- or initiative-based perspective, taking a stakeholder perspective highlights how broad S&G principles touch multiple stakeholders and provide a structured approach to desired impacts.

We will consider five core stake holder groups: (1) employees, (2) customers, (3) the local community, (4) contractors and suppliers, and (5) capital partners (Exhibit 2).

1. EMPLOYEES

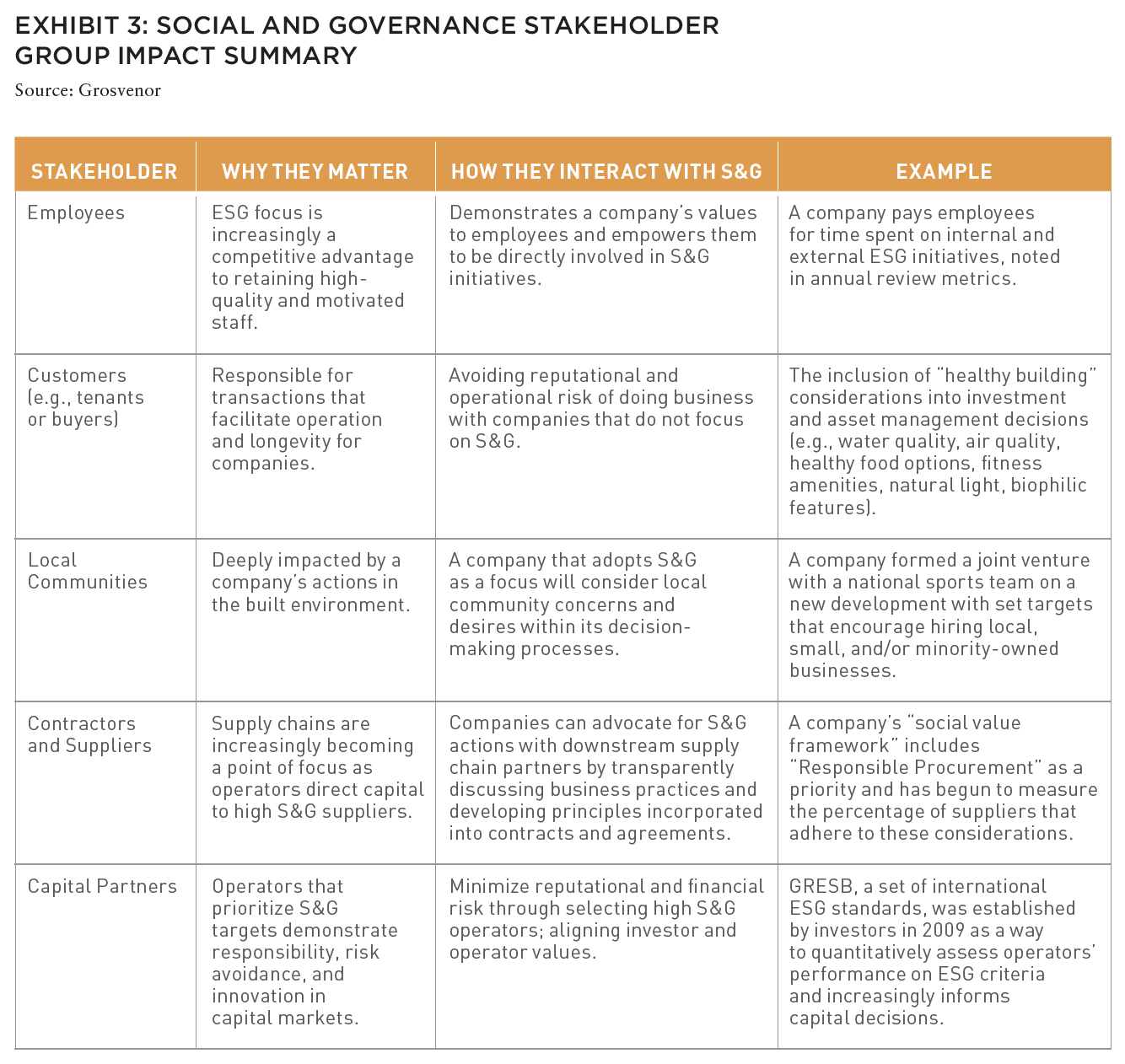

Quality employees, who demonstrate high productivity, creativity, and loyalty are a key component to a company’s success. Hiring, retaining, and growing employees can be a competitive advantage for companies that view the employee-employer relationship holistically.

A growing percentage of employees cite a company’s mission and/or values as a primary reason they choose to work or stay with a particular company.4 Encouraging employee involvement in S&G efforts not only demonstrates a company’s values to employees but empowers employees to be directly involved in S&G impacts.

For example, at Grosvenor Americas our internal voluntary ED&I groups are one of our most popular employee engagement initiatives, annually attracting more than one-third of our staff. In a recent internal survey, more staff commented on the ED&I groups’ work than sent questions relating to post- COVID working preferences. Additionally, in an effort to state clearly and focus on our values, our annual review process explicitly considers and financially rewards ESG efforts.

2. CUSTOMERS

Customers, such as tenants or homebuyers, are responsible for transactions that facilitate real estate companies’ operation and longevity. Leases incentivize repeat business and significant operating expense can be avoided by retaining tenants.

A growing body of research demonstrates the direct correlation between a building’s characteristics and tenants’ health.5 Whether considering COVID-19 safety precautions, or the impacts of physical space on mental health, health and wellness impacts tenants’ decision to occupy space. For instance, multiple high- profile tech companies have committed to only executing new leases in buildings that prioritize tenant health through certifications such as WELL and Fitwel. These market signals indicate that customers recognize the importance of occupying space that prioritizes tenant health and reduces risk by establishing standards surrounding business partners.

In response to these shifting trends, savvy real estate companies are responding by including commitments or goals surrounding S&G considerations. BentallGreenOak includes “healthy building” considerations, including water quality, air quality, healthy food options, fitness amenities, natural light, and biophilic features, in investment and asset management decision-making.6 As office occupancies continue to rise with reducing COVID cases, one can expect the focus on healthy buildings to only increase.

4. CONTRACTORS AND SUPPLIERS

Supply chains are increasingly becoming a point of focus and understanding the stability, ethics, and practices of businesses that are integral to the operation of a company is both a risk and an opportunity.

By including contractors and suppliers, a company broadens the impact of their actions. Companies can advocate for S&G actions with downstream supply chain partners by openly discussing businesses practices and developing principles or rules that are incorporated into contracts or other binding agreements.

One example of this in real estate is Revo’s Social Value Framework, where the company has included “Responsible Procurement” as a priority and has begun to measure the percentage of suppliers that adhere to specific supply chain considerations.7

5: CAPITAL PARTNERS

Capital partners are organizations that act as part of a real estate asset’s capital stack, either by owning a portion of the asset on a passive basis or as a lender. This group of S&G stakeholders is also known as “upstream” supply chain partners, in contrast to the “downstream” supplier chain partners (#4).

The process of soliciting capital partners and finding operators that align with a lender’s or manager’s goals is a two-way process. Assessing risk/return profiles, diversification strategies, and business practices is a critical part of developing a new investor/investee relationship. Operators that prioritize S&G standards demonstrate responsibility, risk avoidance, and innovation to capital markets.

Managers are tasked with growing the capital under their control in the most risk-adjusted manner possible. By understanding how an operator considers risks and opportunities surrounding S&G, managers can better assess and select operators. Additionally, some equity partners and lenders manage capital from individuals or groups who have internal ESG metrics. By aligning funds under management with an operator with similar perspectives, incentives are more likely to be similar.

In the real asset industry, GRESB was established in 2009 by a group of investors looking for a way to quantitatively assess operators’ performance on ESG factors. As capital market’s focus on ESG continues to expand, GRESB participation has increased, demonstrating the desire for quantitative ways to measure all aspects of ESG.

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

TAKING S&G TO THE NEXT LEVEL

By considering impacts on stakeholders and taking a “stakeholder perspective” in the development of its S&G goals, a company can align its actions with the areas in which it can have the greatest impact.

By focusing on who is impacted by S&G activities, as opposed to simply tracking what is being achieved, a stakeholder perspective offers several advantages to operators and investors:

- Clearer understanding of key stakeholders leads to better data collection: With a clearer and more targeted definition of stakeholder groups, a company can collect better data on how best to serve stakeholder groups. Data comprises both quantitative (as is common in the environmental component of ESG) and qualitative (reflecting the fact that some S&G actions are better defined with traits or characteristics surrounding goals).

- Addressing S&G “blind spots”: Without a structured way of thinking about stakeholder groups, even well-intended S&G activities might overlook a key stakeholder. By understanding and categorizing stakeholders in a structured manner, this perspective helps ensure that S&G impacts on all company stakeholders are considered. This includes primary impacts, targeting the stakeholder group in question, and secondary impacts, indirectly affecting stakeholder groups not targeted. In this way, the stakeholder perspective helps ensure companies have no blind spots in their S&G activities.

- Embedding S&G in day-to-day operations: Companies interact with each of the stakeholder groups during day-to-day business operations. By cenetring stakeholders in S&G thinking, companies can move from having separate, discrete S&G initiatives to embedding S&G in the course of their everyday business operations.

The stakeholder perspective is a novel approach to a long-standing challenge in the ESG fi eld: developing S&G goals that truly impact the groups a real estate company directly or indirectly influences. S&G topics are broad, and by centering stakeholders, this approach serves as a method companies may use to focus on meaningful and measurable actions.

—

ABOUT THE AUTHOR

Lauren Krause is Director of Environment, Social, and Governance for Grosvenor Americas, responsible for leading sustainability, enhancing the existing focus of delivering social benefit, and chairing Grosvenor’s Equity, Diversity, and Inclusion group. Brian Biggs, CFA, is Research Director for Grosvenor Americas, responsible for helping set Grosvenor’s investment strategy, analyzing transactions, and advancing the fi rm’s thought leadership projects.

—

NOTES

1. “Sources of Greenhouse Gas Emissions.” US Environmental Protection Agency. Accessed June 22, 2021. epa.gov/ghgemissions/sources-greenhouse-gas-emissions.

2. “Data to the rescue: Embodied carbon in buildings and the urgency of now.” McKinsey and Company. September 15, 2020. Accessed June 22, 2021. mckinsey. com/business-functions/operations/our-insights/data-to-the-rescue-embodied-carbon-inbuildings-and-the-urgency-of-now.

3. “An introduction to responsible investment: real estate.” United Nations. unpri.org/an-introduction-to-responsible-investment/an-introduction-to-responsible-investment-real-estate/5628.article.

4. Brady, Joe. “Brining sustainability home: how CSR and ESG programs can broaden impact as workplaces adapt.” February 24, 2021. Accessed June 22, 2021. forbes.com/sites/forbesrealestatecouncil/2021/02/24/bringing-sustainability-home-how-csr-and-esg- programs-can-broaden-impact-as-workplaces-adapt/.

5. Evans, Gary W. “The Built Environment and Mental Health.” J Urban Health. December 2003. 80(4): 536-555. ncbi.nlm.nih.gov/pmc/articles/PMC3456225/

6. Kalsi, Sonny. “What It Means To Be A Socially Responsible Real Estate Investment Manager.” February 8, 2021. Accessed June 22, 2021. forbes.com/sites/forbesrealestatecouncil/2021/02/08/what-it-means-to-be-a-socially-responsible-real-estate-investment-manager/?sh=255b98882247

7. Revo. revocommunity.org/document/social_value_framework