This article appears in Summit Journal (Fall 2020) | Download PDF

The COVID-19 pandemic has wrought massive shifts in behavior, as social distancing and other public health protocols have reshaped our daily lives.

One of the first protocols implemented by many countries focused on migrating non-essential employees to remote work in an effort to cut down on contacts made commuting and among co-workers in confined offices. In the subsequent months, there have been numerous reports and declarations of companies leaning into remote work as the future of their workforce.

A wide-scale embrace of remote work and decentralized labor forces will have significant ramifications on the future demand for office space across the US. However, these narratives have been counterbalanced by companies such as Amazon and Facebook leasing additional office space in recent months, as they envision a future return to normalcy once the pandemic has subsided.

Given the potential impact remote work could have on office space demand and investments, determining its true scale is paramount. If remote work set-ups were not having negative impacts on company operations, and were viewed favorably by executives, then such impacts and views would need to be accounted for in the investment process and market selection—at least in the near- to medium-term.

DETERMINING THE SCALE

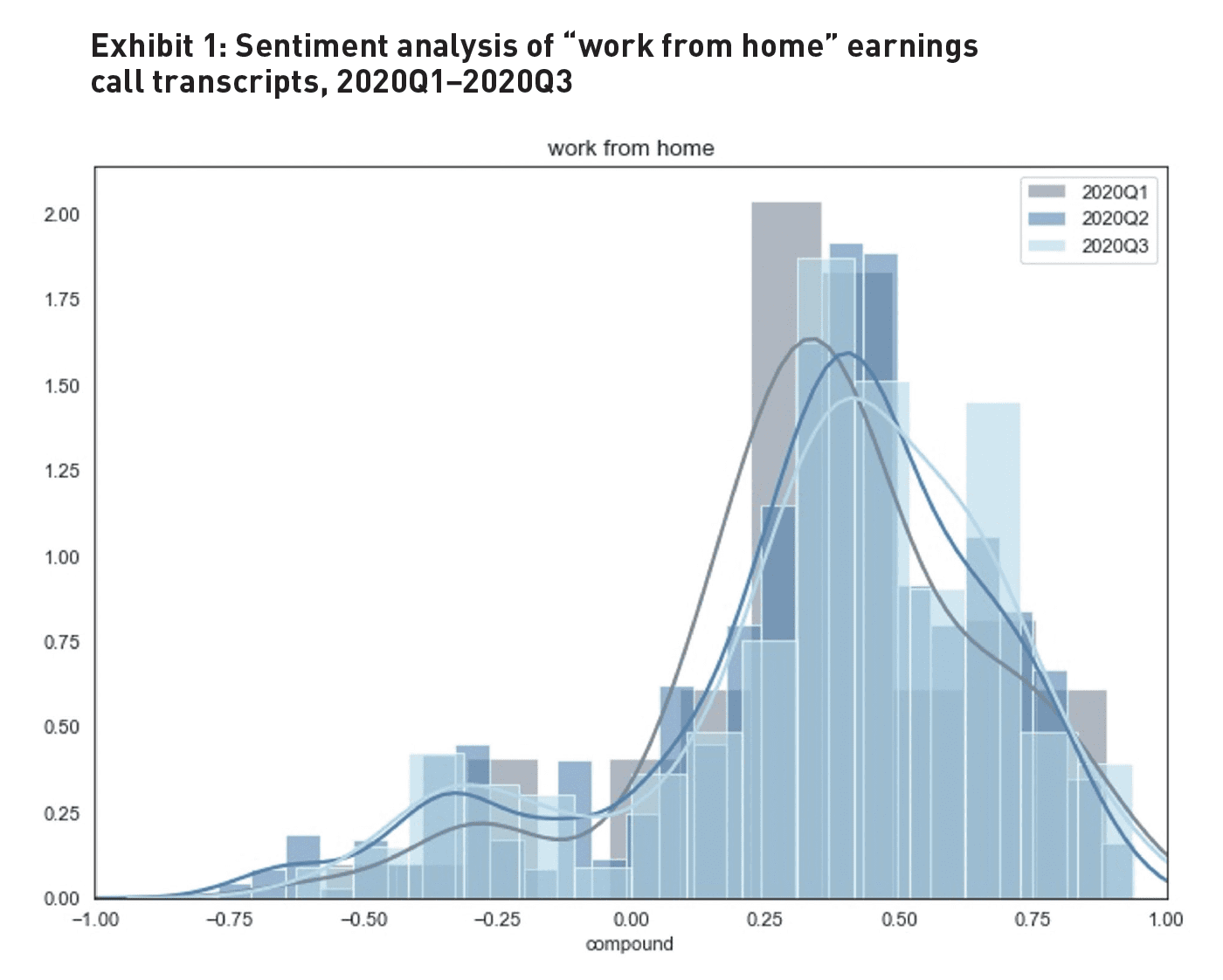

To make this determination, we reviewed more than 2,700 earnings call transcripts from US companies beginning in the first quarter of 2020 and through mid-August. The transcripts were selected for this analysis because executives would be the ones in charge of assessing and implementing remote schemes and would need to disclose material negative impacts on operations. The transcripts also give a wide exposure across industries relative to media reports, which tend to focus on higher profile companies with consumer recognition. Using transcripts does present some limitations, as public companies tend to be larger and do not always represent the experience of small and medium businesses. The calls may also have a slight inherent bias to be positive, but nonetheless serve as useful source material.

Within these transcripts, conversations that mentioned “work from home” or related phrases, such as “remote work,” were isolated and run through a Valence Aware Dictionary and Sentiment Reasoner (VADAR) algorithm that scored the sentiment of the phrase on a continuum from -1 (negative) to 1 (positive). These scores were then plotted into distributions to determine the aggregate sentiment of executives towards remote work and any potential shifts in sentiment over time (Exhibit 1).

Given the positive reception to the concept, remote work will thus remain a fixture of these labor and space markets.

UNDERSTANDING POSITIVE SENTIMENT

At the time of this analysis, the sentiment around “work from home” and related phrases was positive, and the general sentiment has shifted slightly more positive over the last few quarters. This is likely owing to increased familiarity and experience with the tools and infrastructure of remote work.

While there is a smaller consistent contingent of companies reporting negative experiences, we believe the aggregate positivity means that remote work is likely to remain a part of company operations in some capacity following the pandemic. While it is possible that, over the longer term, companies may revert towards more traditional operations, over the short- and medium-term, it is advantageous to adjust investment process tools to account for this reality and determine if there are potential disparate risks to space demand across markets.

Analyzing sentiment in this way forms a useful understanding of US office markets facing risks to demand that initially stemmed from remote work over the near- to medium-term—but not in a uniform way across markets. Our own teams took this lens and used it as a prism to approach and manipulate our more traditional datasets. First, we sought to capture the labor market dynamics that could underpin risk levels across markets.

Different industries have different capabilities for working remotely. For example, you cannot replicate a biosafety lab in your home office. As a result, the labor market composition of a metro can be a factor in the relative-risk office space demand that the market may face from an increase or permanence in remote work following the pandemic. Utilizing an analysis from the Dallas Fed that analyzed the proportion of each industry sector, we also created an index that measured the proportion of each metro’s labor market in our own target markets that could potentially work remotely. These indexes were then ranked on a relative basis to highlight the differentiation among metro economies.

We then factored in potential demand or desire employees may have for remote work in each metro. One hypothesis is that employees with longer commutes are more likely to desire working from home in some capacity, given the higher time and financial cost they face from commuting. This means that employers would ultimately need less space per employee, as only a portion of the workforce would be present in the office on any given day, resulting in diminished office space demand even as employment expands. To factor this into our analyses, we sourced commute lengths from the Census for each of our target markets and incorporated their relative rankings into our model.

One of the final factors that needed to be accounted for in the post-pandemic office sector is public health protocol and social distancing. Employees and employers are less likely to make use of or require remote work functionality if they are able to return to the office and feel safe. Even if a vaccine is developed, it appears it will significantly reduce but not eliminate the risk of contracting COVID-19, meaning that distancing and other safety measures will need to continue to be observed for some time. As a result, markets where office space per worker is lower will potentially and more rapidly embrace remote work, crimping future office space demand.

It could be argued that markets with less office space per worker means space demand will need to rise in order to accommodate employees. However, research from CBRE Americas shows that only 25% of their leasing professionals were reporting at least one tenant seeking to expand their space to accommodate social distancing. Based on this data, showing that tenants are by and large not seeking to expand space for social distancing, markets where space per employee is lower have the potential to adopt remote work at a higher rate. Given the positive reception to the concept, remote work will thus remain a fixture of these labor and space markets. Markets where there is higher space per worker to more immediately allow for a return to the office with social distancing will adopt remote work technologies at a lower rate and maintain more traditional set-ups and demand curves.

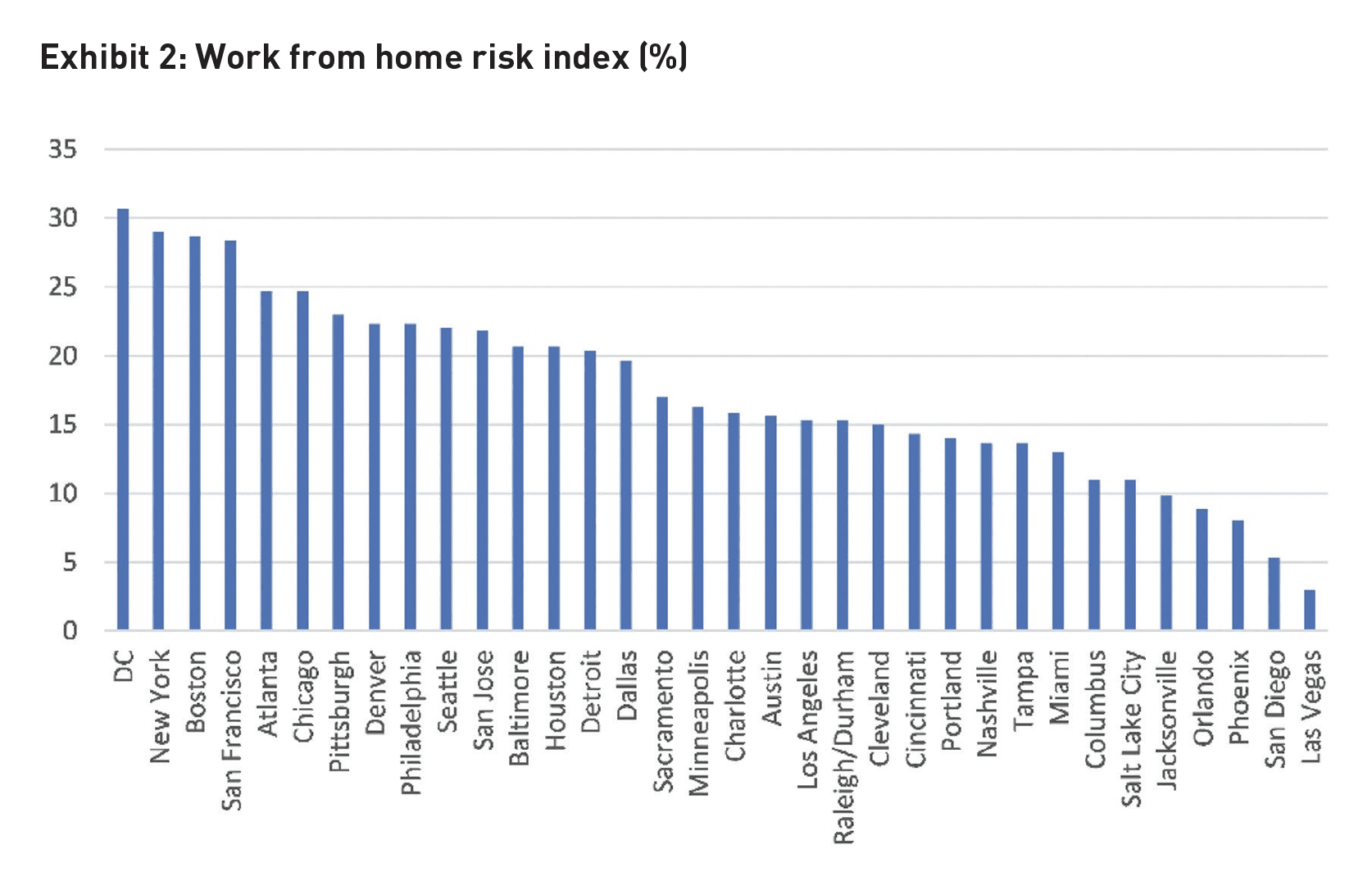

By combining the metrics outlined above, we are thus able to incorporate an aggregate remote work risk factor into our broader market rankings (Exhibit 2).

This risk index allows the investment process and market selection criteria to account for what will likely be a lasting trend of remote work, based on our own sentiment analysis of corporate earnings transcripts. On an ongoing basis, it will remain important to monitor shifts in sentiment towards remote work from the source outlined above and potentially broaden the scope of the analysis. As the sentiment towards remote work continues to evolve, we can better determine the degree to which our risk factor should be weighted in our broader market rankings, providing an insightful edge into the office investment landscape.

—

ABOUT THE AUTHORS

Christopher Muoio is Vice President, Data and Research at Madison International Realty, and Adrian Kay is Data Analyst at Madison International Realty, a real estate investment firm, is committed to excellence in providing capital, equity monetizations & recapitalizations.

—