For commercial real estate investors, inflation fears are real—but are they rational?

Investors cite inflation hedging power as one of the primary attractions of property investments.[1] This characteristic has been of limited use in recent years given the very low pace of inflation in the US and throughout most developed global markets, leaving other factors to drive the investment allure of real estate. Currently, inflation fears are emerging and raising concerns regarding potential negative effects on discount rates used to value portfolio properties, as well as potential positive effects on property cash flows.

However, inflation fears are potentially overblown, based on current macro-economic conditions. And, expectations of problematic inflation may actually have a negative impact on commercial property dynamics if they become pervasive.

INFLATION EXPECTATIONS DEMONSTRATED IN FINANCIAL MARKETS ARE MINIMAL

The best indicator of inflation expectations is the yield on Treasury Inflation-Protected Securities (TIPs). These instruments are traded continuously in deep liquid global financial markets, thereby providing a real-time window into market views of inflation prospects. Yields on TIPs are credible indicators of inflation expectations because they represent actual financial transactions rather than opinion surveys. Investors in TIPs are betting money on the path of future inflation.[2]

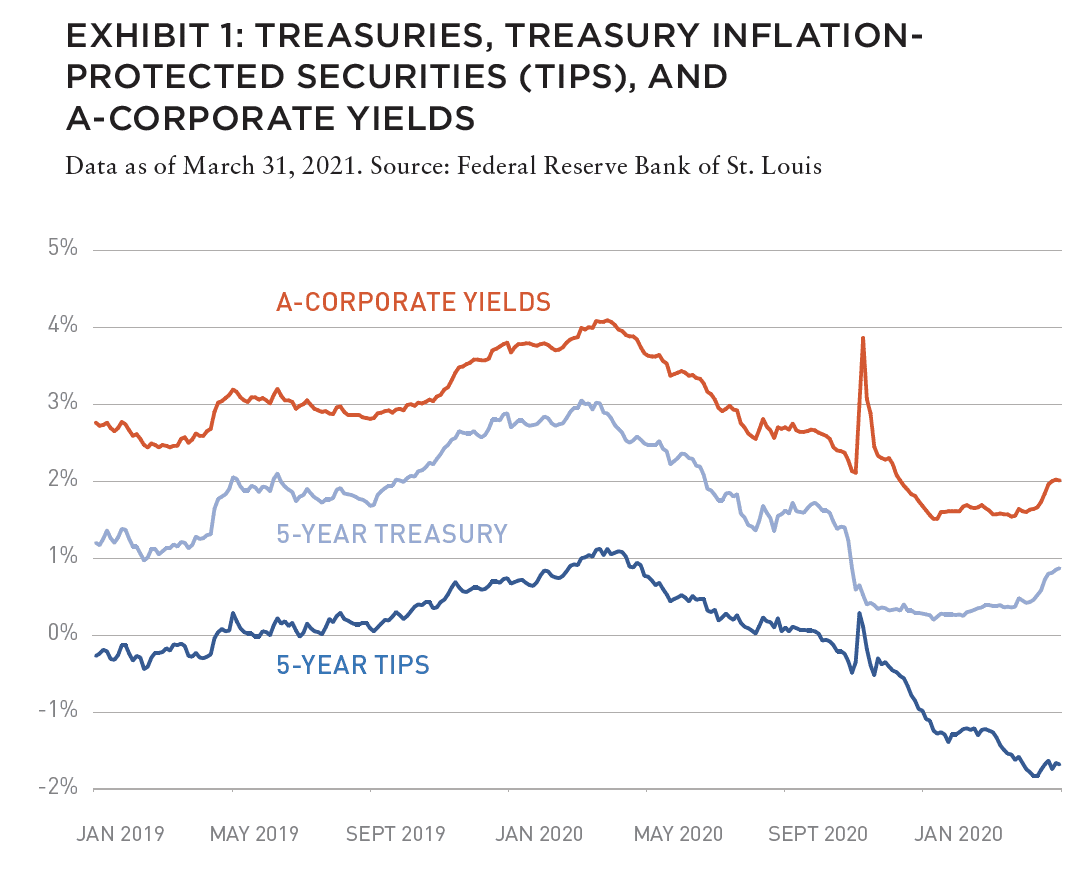

As shown in Exhibit 1, inflation expectations have been increasing—especially since mid-January 2021. The increase reflects the projected enactment of the US$1.9 trillion American Rescue Plan Act signed by President Biden on March 11. The plan is on top of the similarly-sized Coronavirus Aid, Relief, and Economic Security (CARES) Act, signed in March 2020, and the US$900 billion follow-up signed in December 2020. The combined package is directed at supporting the economy through the COVID recession that began in March 2020 with extensive shutdowns in economic activity, intended to quell contagion. The five-year US Treasury yield dropped precipitously in March 2020 along with expected inflation as the economy tanked. High quality corporate bond yields behaved in similar fashion. Yields are now picking up in response with inflation expectations of roughly 2.5%.

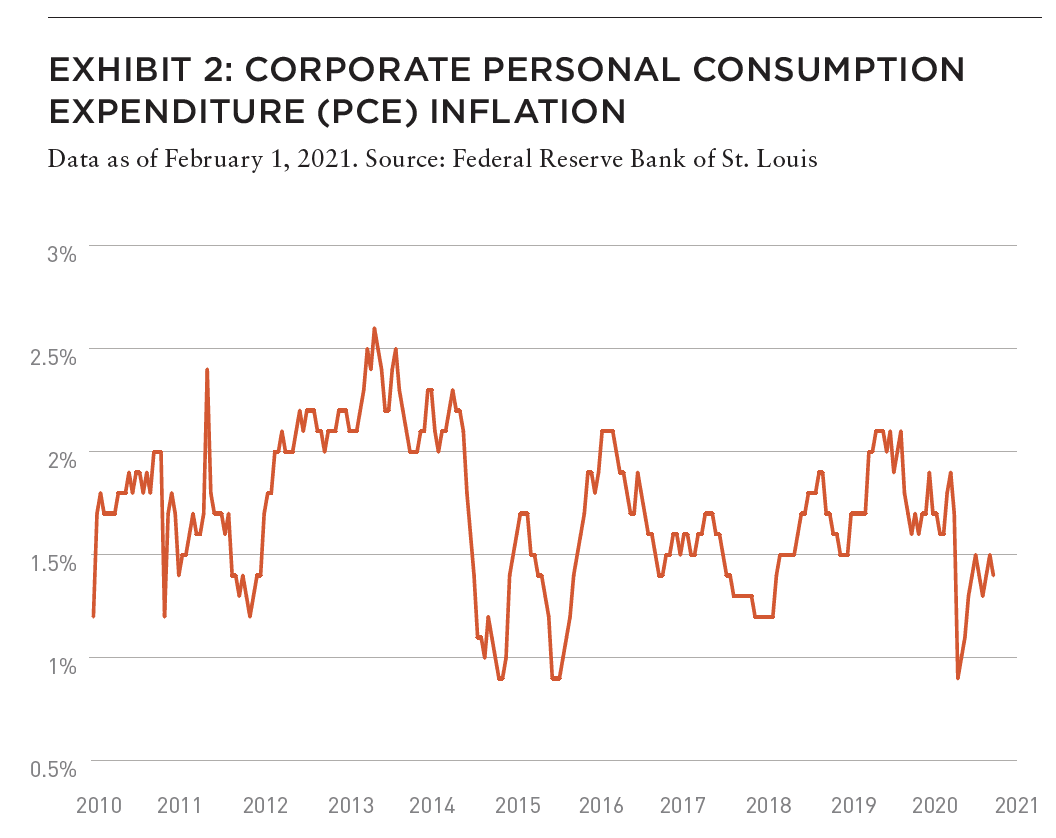

These expectations are in line with the Federal Reserve policy, which is targeting a period of above 2% inflation designed to super-charge job creation. The Fed focuses on prices of personal consumption expenditures excluding the volatile food and energy categories. Economic projections of Fed policymakers show a range up to 2.5% in 2021 and 2.3% in 2022, but averaging 2% in the long run.[3] Similarly, the forecasters polled in the monthly Blue Chip Economic Indicators Survey project steady 2.1% personal consumption expenditure (PCE) inflation throughout a long-term ten-year window, with the most bearish expecting a 2.4% PCE inflation rate in Q4 2022. As shown in Exhibit 2, inflation has rarely breached a 2% rate over the last ten years.[4] In plain words, financial markets and forecasters are expecting a very modest pickup in inflation, in line with the expectation of monetary policymakers.[5]

EFFECTS ON COMMERCIAL REAL ESTATE THROUGH BORROWING COSTS

If property cash flows and values were driven simply by yield arithmetic, the uptick in inflation and interest rates might produce negative effects similar to the negative effects on bonds. But property cash flows are not fixed; they respond to economic growth and supply-demand drivers.

The federal spending directed at COVID relief is putting upward pressure on interest rates and inflation expectations precisely because it is supporting economic recovery. Recovery will impact commercial property sectors differently: apartments are likely to benefit as job creation stimulates demand, especially by stimulating household formation; industrial should benefit from increased consumer and investment spending boosting demand for warehouse space, but will be somewhat offset by the revival of in-person shopping at stores, which is expected to benefit the retail sector; we anticipate office will benefit from returning tenants with impact of work-from-home policies highly uncertain. In addition, the hospitality sector will likely benefit mightily as travel resumes.

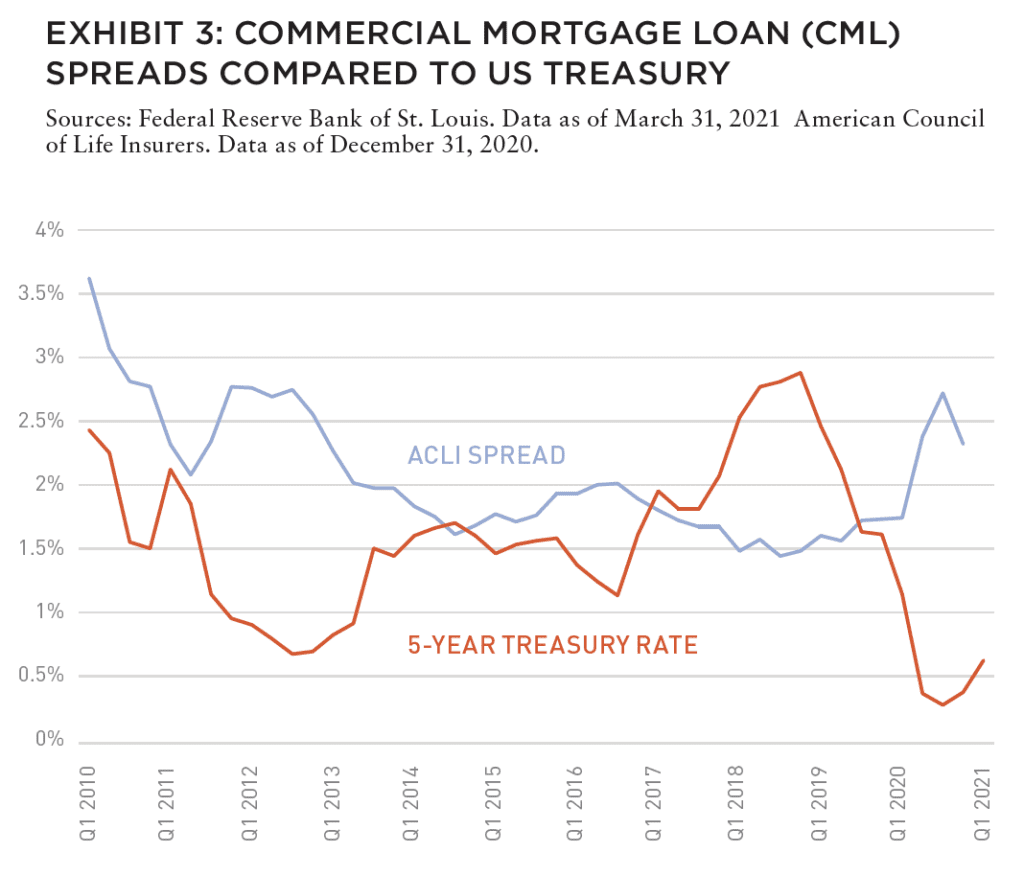

At the same time, re-pricing of commercial mortgage borrowing could have a negative effect on levered property performance but this needs to be netted against the positive impact of stronger and faster economic recovery. In addition, commercial mortgage pricing did not respond fully to the COVID-related drop in Treasury yields. According to the American Council of Life Insurers (ACLI) and shown in Exhibit 3, life company commercial mortgage spreads actually widened as the COVID recession took hold in Q3 2020. Lenders apparently viewed the drop in US Treasury yields as a transitory shock and widened spreads in response. This leaves a cushion for a return to more normal US Treasury yields as recovery ensues.

As shown in Exhibit 3, the five-year US Treasury rate peaked at 2.88% in Q4 2018, meandering downward though Q1 2020 and then plunging in the Q2 2020 as the COVID shock prompted the Fed’s rapid and strong policy response. Commercial mortgage loan (CML) spreads widened markedly at that time after holding in the 150-200 BPS range over the prior five years. Over that period, the low point in spreads hit 144 BPS in the Q3 of 2018. In the final quarter of 2020, spreads were 88 BPS wider than that low point which had a corresponding five-year Treasury rate of 2.81% versus the 0.37% US Treasury rate in the Q4 of 2020.

Arithmetically, this history implies a substantial cushion in CML spreads to absorb rising interest rates as COVID recovery progresses. But, actual spread pricing depends on more than just arithmetic; it is enormously influenced by the competition among lenders for CML origination business.

Life insurance lenders committed almost US$16 billion in Q4 2019, the highest commitment total since the beginning of the post-global financial crisis (GFC) cycle. Appetite reflected the availability of CML and pricing that remained attractive versus other fixed income assets offering comparable risk. Evidence of durable appetite for the period ahead is suggested in a strong uptick in commitments to US$10.9 billion for the Q4 2020 as COVID vaccines were approved.

Beyond life insurance lenders’ further demand for CML lending opportunities will likely come from private equity debt funds. A recent report from The Real Deal dated 30 March 2021 shows a cache of dry powder of US$250 billion that will need to be activated to generate returns. Commercial banks will also compete for CML business, but their appetite is usually focused on shorter maturities.

A final note on inflation, interest rates, and borrowing costs involves the reason for rising interest rates and inflation— which is stronger economic growth! Under the Fed’s new policy rubric, inflation above 2% will be tolerated on a temporary basis to strengthen job creation and economic growth. Stronger economic growth is the most powerful driver of commercial real estate performance. So, even if borrowing costs rise, revenues should offset some of the pain— but not all.

EFFECTS ON COMMERCIAL REAL ESTATE THROUGH LEASE STRUCTURE

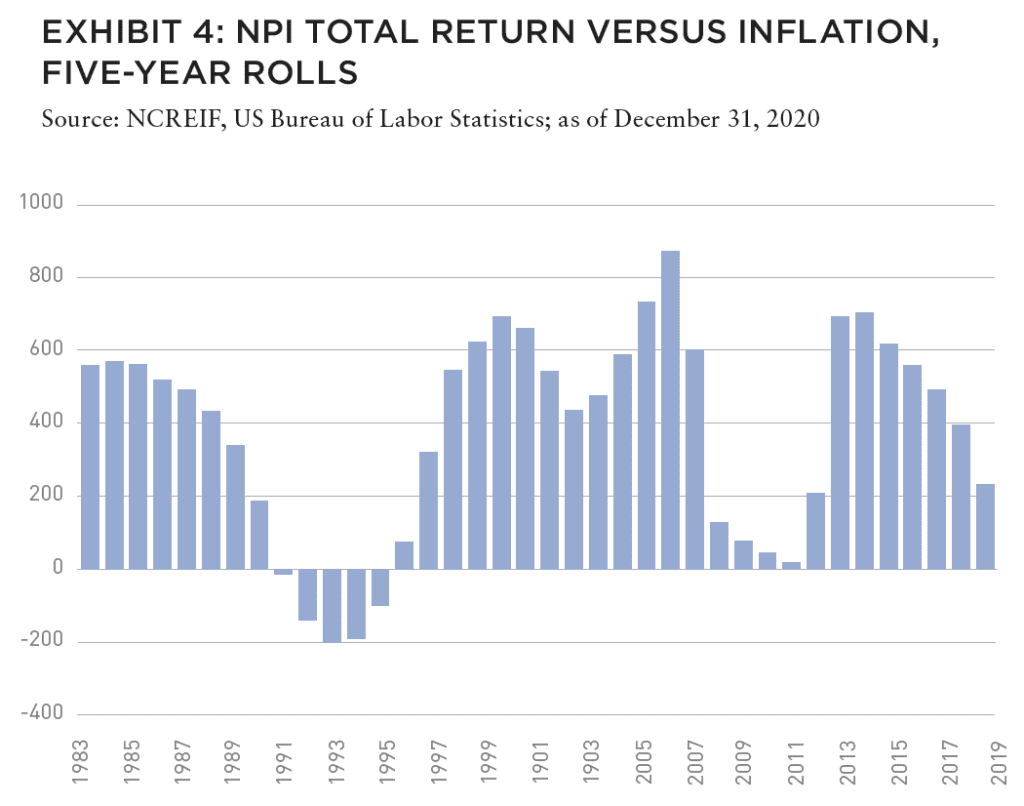

Beyond the question of borrowing costs under a regime of rising inflation, there are reasons why commercial real estate has been and will likely continue to be considered an inflation hedge. First, investment performance has beaten inflation over medium five-year holding periods for the past forty years with the exception of the 1990’s recession and its aftermath. This result is shown in Exhibit 4 using total return on the National Council of Real Estate Investment Fiduciaries (NCREIF) National Property Index (NPI) minus the Consumer Price Index (CPI) including food and energy. Similar results are obtained using the core PCE price index to measure inflation. Commercial real estate performance beat inflation even during the more severe recession associated with the GFC.

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

Recession itself does not undermine the inflation hedging power of commercial real estate which rather depends on the supply-demand balance in property markets when recession takes hold. The five-year holding period reflects the relatively long investment horizon associated with property that is necessitated by the relatively high transactions costs.

Second, commercial property returns are influenced by the structure of leases where some inflation protection can occur from triple-net leases that pass property expenses to tenants (especially for industrial property), inflation step-ups that index rents (especially for office properties), short-term leases that can be adjusted to compensate for inflation (especially for apartments), and common area maintenance (CAM) passthroughs that are prevalent for regional mall retail. It bears noting, however, that these lease structures did not prevent the shortfall in property performance versus inflation in the first half of the 1990’s because more powerful supply-demand forces were out of balance.

Third, inflation mitigation can arise from investor behavior when expectations of rising inflation encourage investment in property expecting it to hedge inflation. Rising investor demand, in turn, can generate increasing values that may indeed hedge inflation in a self-fulfilling prophecy. If rising inflation does materialize and is associated with stronger economic growth, the bet on property will be rewarded and vice versa.

Forecasters predict real GDP growth to average 6.3% in 2021 and 4.3% in 2022.8 Inflation in both years is expected to reach or slightly exceed 2% with the periods slightly above 2% within the Fed’s tolerance.

Each sector will face local market challenges as the pattern of geographic growth and postCOVID behavior emerge. The modest construction over the last few pre-COVID years will help to buoy investment performance but, as always, investors will need to select properties and manage portfolios carefully.

The outlook is complicated by the potential for a material increase in federal spending from President Biden’s infrastructure proposal now under discussion. The US$2 trillion proposal would be spent over eight years and paid for largely by raising corporate taxes. On a positive note, US infrastructure is in dire need of attention, in the American Society of Civil Engineers’ 2021 Report Card for America’s Infrastructure, a US$2.6 trillion shortfall is estimated over the next ten years unless the current pace of infrastructure spending is boosted. In addition, the need for improvements in clean energy generation, cybersecurity and public health preparedness add to the US$2.6 trillion gap. Over the long term, infrastructure investment might also improve productivity and jump start private sector innovation which are both are positive for economic growth and for real estate. The eight-year time frame for projects is important to note because it will spread out the demand for labor and materials and mitigate short-term inflation increases as pent-up demand is addressed in the aftermath of the recession.

—

ABOUT THE AUTHOR

Martha Peyton is Managing Director of Applied Research for Aegon Asset Management, the global investment management brand of Aegon Group.

—

NOTES

1. PREA. “Why Real Estate?” Accessed June 22, 2021. https://www.prea.org/research/whyrealestate/

2. Some analysts are discounting the efficacy of TIPs as indicators of market inflation expectations because the Fed has been buying them as part of the COVID quantitative easing program. These concerns are countered by the steadiness of the Fed’s purposes throughout the recent increase in inflation fears, suggesting that market participants are not fighting TIPs yields resulting from the Fed’s actions.

3. Federal Reserve Summary of Economic Projections. “Core Personal Consumption Expenditures.” March 17, 2021,. https:// www.federalreserve.gov/monetarypolicy/ files/fomcprojtabl20210317.pdf

4. Blue Chip, “Blue Chip Economic Indicators.” Accessed March 12, 2021. https://www.aeaweb.org/rfe/showRes.php?rfe_id=1922&cat_id=12

5. Aegon Asset Management expectations are similar. See Rybinski white paper April 2021

6. Blue Chip, “Blue Chip Economic Indicators.” Accessed April 9, 2021. https://www.aeaweb.org/rfe/showRes.php?rfe_id=1922&cat_id=12