An upswing in occupancies and rents has taken root, and the key age demographic is on the precipice of what is anticipated to be unprecedented growth.

After nearly three years of pandemic-induced operational challenges, a rising cost environment, and uncertainty and a general lack of conviction in debt capital markets, the senior housing sector appears to be transitioning to an expansionary cycle that could last several years due to projected tailwinds.

Expectations tilt to the upside. An upswing in occupancies and rents has taken root, and the key age demographic is on the precipice of what is anticipated to be unprecedented growth, even as construction activity has ratcheted back to a decade low.1

THE SENIOR HOUSING VALUE PROPOSITION

Before delving into the driving forces powering the sector’s recovery, let’s first explore the diverse range of housing options available to seniors.

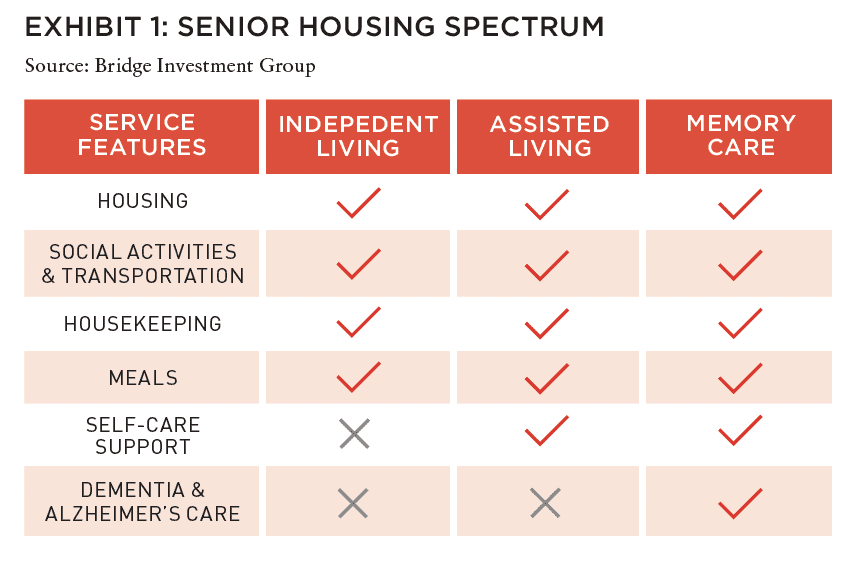

While the spectrum of long-term care options ranges from active adult communities through skilled nursing facilities, where patients require particular medical attention, senior housing—for the purposes of this article—comprises independent living, assisted living, and memory care. These communities offer service- and care-enriched housing that allows residents to age in place and are for-rent and private pay, rather than government subsidized and large upfront buy-in fees.

While senior housing offers substantial cost savings relative to in-home care,2 affordability is a crucial consideration in gauging the potential uplift to the sector overall. With monthly rents that typically range from $3,200 to $6,700,3 senior housing tends to attract what we have termed the “mass affluent demographic cohort,” with personal assets between $350,000 and $500,000. Private-pay senior housing residents typically rely on a combination of income sources such as retirement accounts, pensions, Social Security, and the liquidation of non-financial assets (i.e., financial asset spenddown) to access high-quality housing, which limits government reimbursement and rent collection risk.

Senior housing living offers residents the advantages of vibrant social engagement and round-the-clock support for self-care, medication management, wellness, meals, transportation, and housekeeping. Given that the asset class combines elements of community-based living, hospitality services, and healthcare, we see a direct link between resident satisfaction and asset performance. This means senior housing is an operationally intensive business where specialized operators who can fully meet nuanced individual resident needs are best positioned to deliver exceptional results.

SENIOR HOUSING ON THE UPSWING

Because senior housing is needs-based, it has historically served as a counter-cyclical asset class by offering resilient performance through macro-cycles. The specific challenges of the recent pandemic, however, disproportionately affected the sector in terms of both demand and operations.

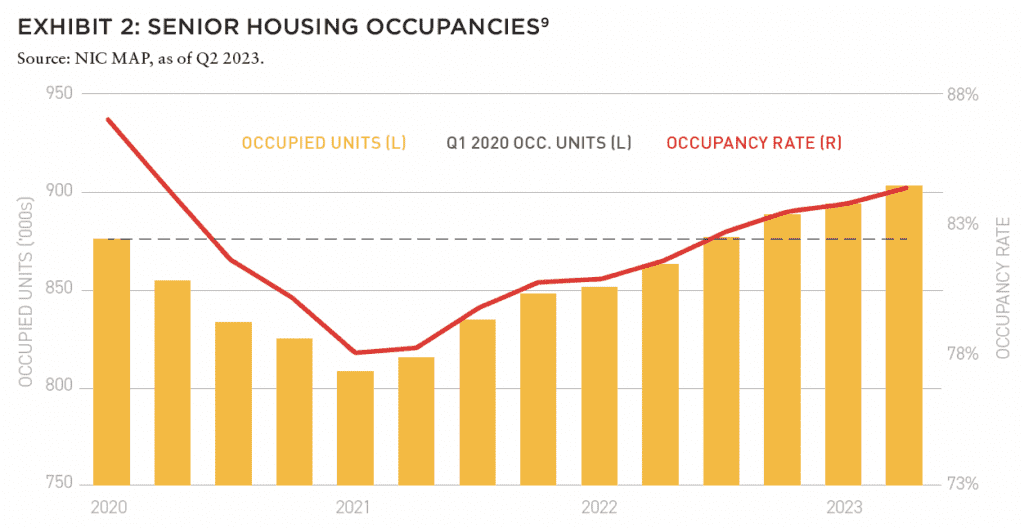

As safety concerns prompted strict regulations and moratoriums that clamped down on resident move-ins, the industry shed 9.2 percentage points in occupancies,4 undercutting financial results even as front-line employees admirably worked to protect vulnerable resident populations.

As of mid-2023, however, the sector has staged a remarkable turnaround. Market observers may look to a meaningful recovery in fundamentals that has taken root as the pace of resident move-ins has substantially stepped up compared to 2020’s subdued levels, while net absorption has carried into positive territory for eight consecutive quarters at double the pre-pandemic average.5 Occupancy rates are up 6.3 percentage points since 2021 and now stand only 2.6 percentage points short of full recovery.6 On an absolute basis, the number of occupied units has already rebounded past the previous peak and continues to climb.7

These incremental demand gains appear to be poised to accelerate revenue creation and accretive rent growth. Senior housing rents experienced challenges throughout the pandemic, but we have observed steady gains over the past several quarters, more recently establishing a new high of 5.7% YOY with regard to effective rent growth as of Q2 2023.8

ACCELERATING TAILWINDS FUELING DEMAND

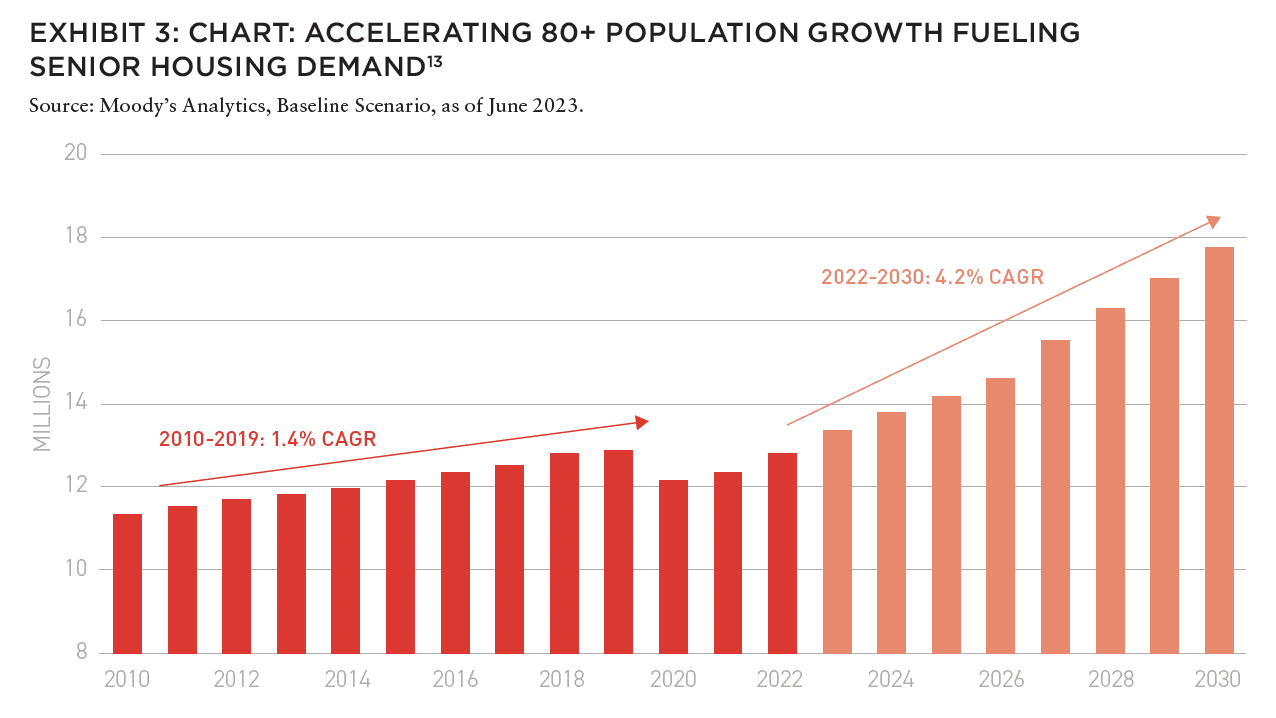

With pandemic disruptions in the rearview mirror, a leading headline in the sector’s recovery is what we have termed the “Aging Avalanche,” which is the incoming surge in the 80+ population cohort that is setting the table for what we believe will be protracted demand gains. The Aging Avalanche has been discussed at length, and as the crest of a demographic swell arrives, we see two distinct waves of population-driven demand providing meaningful tailwinds.10

The first wave of the Aging Avalanche is already in motion as the 80+ population is projected to expand by a record-breaking 561,000 people in 2023—more than double the typical annual increase compared to the past ten years and well in excess of prior population growth rates.11 A second, even larger cohort is projected to rise in 2027 when the 80+ ranks will begin to accelerate by 800,000 people per year, foreshadowing several years of pronounced demand growth potential, leading to a 39% increase in the prime senior housing demographic.12

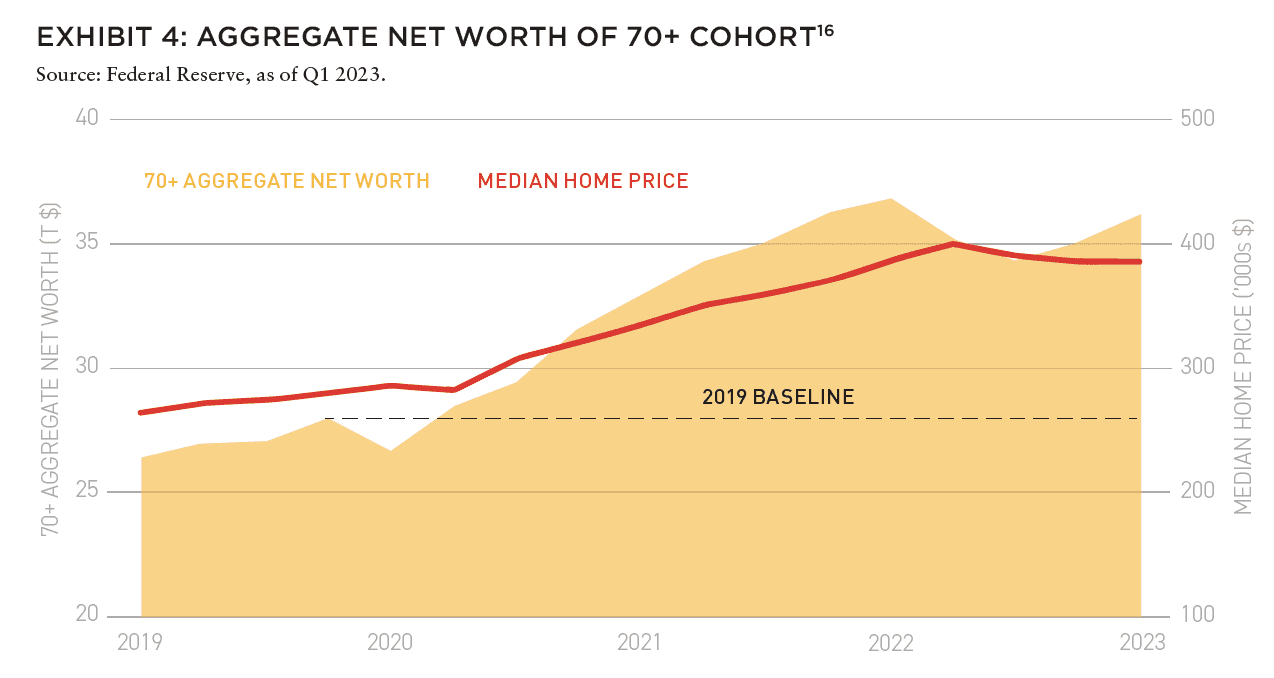

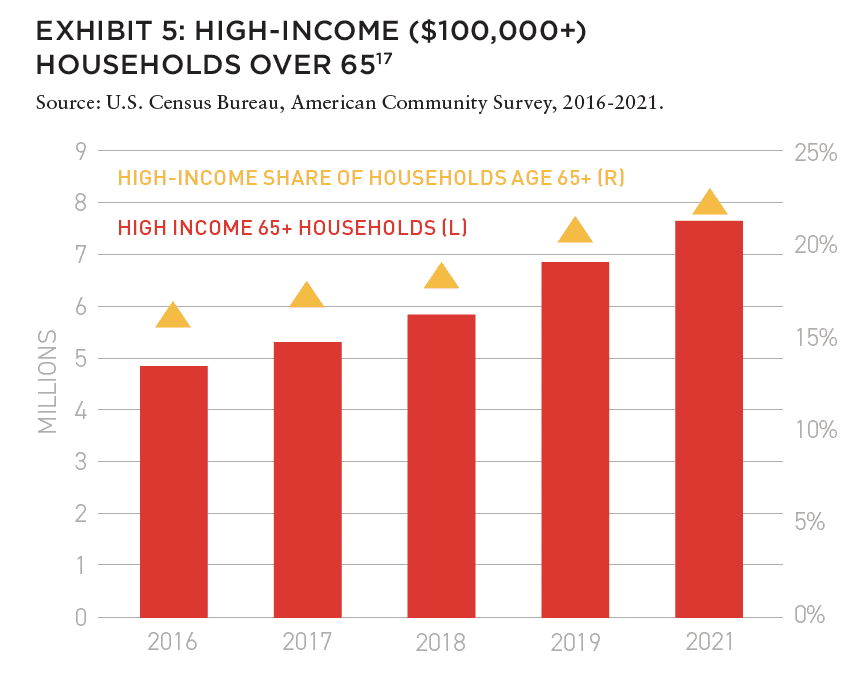

Another touchstone in the sector’s outlook is the notable increase in purchasing power among seniors, who are wealthier than ever before, creating a broader potential pool of renters. Since 2019, seniors aged 70 years and older have witnessed a remarkable 29% increase in household net worth, representing an aggregate gain of $9.1 trillion14 that was fueled in great part by a jump in home values during the pandemic. Additionally, a rise in both the number and the share of retirees with high incomes (i.e., $100,000+ annually) suggests a higher ceiling for pricing power along a longer time horizon.15

RATE HIKES LIKELY TO MUTE SUPPLY AND CATALYZE TRANSACTION ACTIVITY FOR HIGH-QUALITY ASSETS

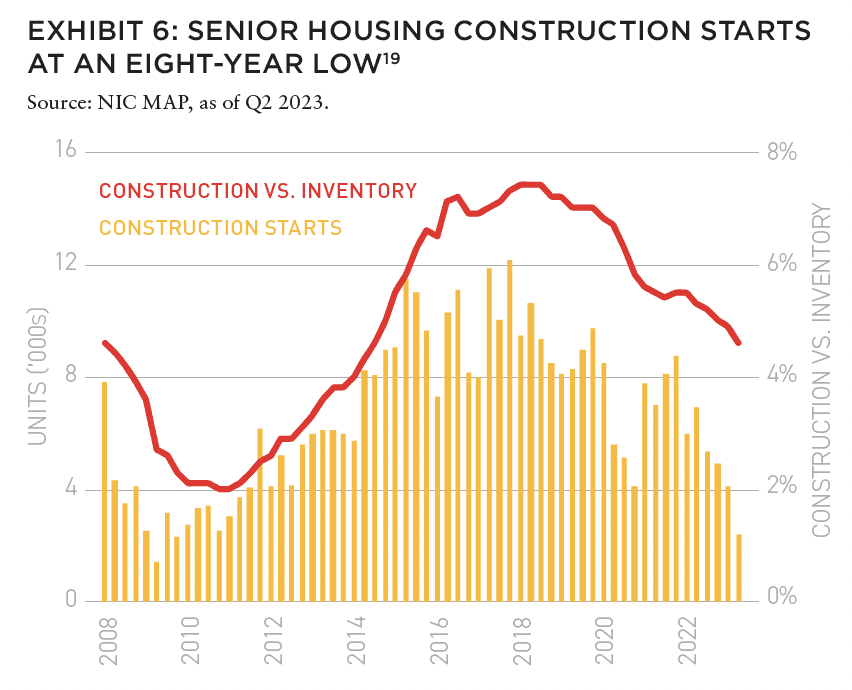

Even as demand tailwinds accelerate, hardening debt markets have forced developers to throttle back, marking a stark reversal from the runup to the pandemic when deliveries overshot the market. Senior housing construction starts are down 80% since the 2017 peak, registering at a decade low of 2,400 units nationwide, and the number of units under construction as a share of existing inventory is now at the lowest level since 2014.18 Taken together, these leading indicators are indicative of muted supply growth through at least the next 24 months, and potentially longer if conventional lenders remain largely sidelined for new construction.

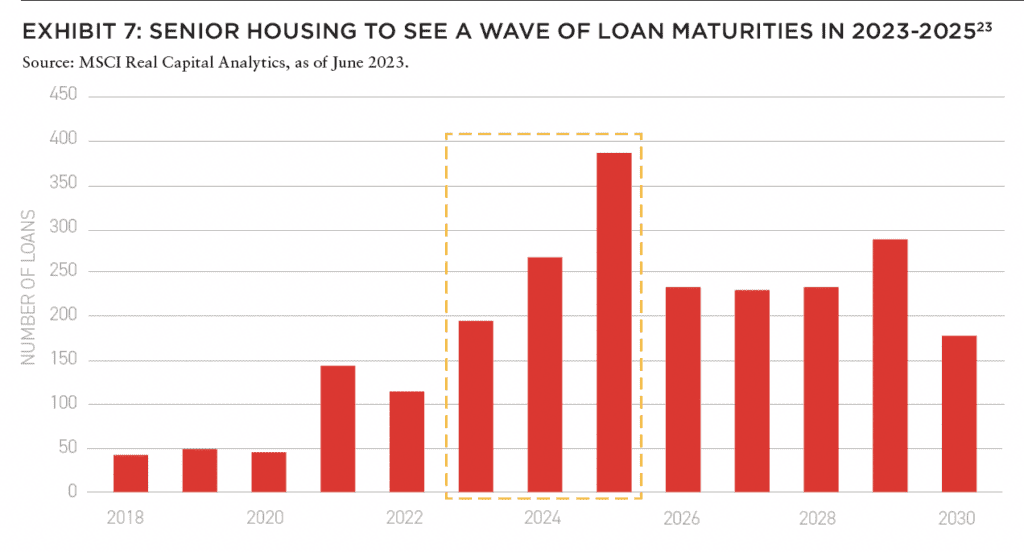

Elevated volatility in debt markets is also reshuffling the investment landscape and could open the door to forced sales of high-quality assets, potentially creating openings for opportunistic buyers with sharp pencils. Between 2023 and 2025, 860 senior housing loans will come due,20 and borrowers are likely to encounter capital stack stress amid a stricter lending environment that has seen loan-to-value (LTV) ratios retreat.

Further expanding the opportunity set of high-quality investments, private equity funds own ~$12 billion of senior housing assets that are approaching the end of typical asset hold periods, which will likely lead asset managers to consider strategic sales of such assets.21 At the other end of the investor spectrum, small-scale investors that represent 40% of sector deal flow22 are often poorly capitalized, raise equity on a deal-by-deal basis, and may also be forced to exit investments upon loan maturity as the current debt capital environment is not accretive for short-term extensions.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #13

Benjamin van Loon | AFIRE

OFFICE TROUBLES: FINANCIAL RISKS AND INVESTING OPPORTUNITIES IN US CRE

Dr Alexis Crow | PwC + Byron Carlock

THE UNDERPERFORMANCE PARADOX: WHY INDIVIDUAL INVESTORS FALL BEHIND DESPITE BUYING LOW

Ron Bekkerman | Cherre + Donal Ward | Tenney 101

CLIMATE THREAT: EXTREME WEATHER IS THE NEW NORMAL FOR REAL ESTATE

Jacques Gordon, PhD | MIT

CLIMATE OPPORTUNITY AWAITS: HOW REAL ESTATE CAN INVEST IN CLIMATE ADAPTATION

Michael Ferrari, PhD and Parag Khanna, PhD | Climate Alpha

PREMIUM PRICE TAGS: INSURABILITY THROUGH PROPERTY RESILIENCE DATA

Bob Geiger | Partner Engineering & Science

REAL ESTATE WEB3: THE EMPEROR’S NEW CLOTHES OR THE NEXT BIG THING?

Zhengzheng Tan, Alice Guo, and Naveem Arunachalam | MIT

ADAPTIVE TO REUSE: COULD BUILDING CONVERSIONS BE DIFFICULT, EXPENSIVE . . . AND STILL PROFITABLE?

Josh Benaim | Aria

RENOVATE, REBRAND, REPOSITION: ADDING VALUE TO MULTIFAMILY THROUGH REVITALIZATION

Robert Kilroy, CFA | The Dermot Company + Will McIntosh, PhD | Affinius Capital

REDEFINING THE PROGRAM: A CONVERSATION WITH ARCHITECT DAVID THEODORE

Peter Grey-Wolf | Wealthcap + David Theodore | McGill University

SENIOR HOUSING UPDATE: EMERGING OPPORTUNITIES THROUGH DEMOGRAPHIC TAILWINDS AND DIMINISHING SUPPLY OUTLOOK

Robb Chapin, Jack Robinson, Andrew Ahmadi, and Morgan Zollinger | Bridge Investment Group

SENIOR HOUSING UPDATE: UNPRECEDENTED DEMOGRAPHIC ACCELERATION MAY DRIVE STRONG OPERATING FUNDAMENTALS AMID ECONOMIC SLOWDOWN

Tom Errath | Harrison Street

HOLIDAY FROM HISTORY: REASONS FOR US OPTIMISM IN A CHANGING GLOBAL ENVIRONMENT

Charlie Smith | Newmark

CRADLE TO CRADLE: AN ALLOCATOR’S VIEW ON IMPLEMENTING ESG INITIATIVES

Christopher Muoio and Katie Cappola | Madison International Realty

FREE LUNCH: MULTI-DIMENSIONAL DIVERSIFICATION IS A FULL-COURSE FREE MEAL

Elchanan Rosenheim and Tali Hadari | Profimex

CAMPAIGN MESSAGING: CFIUS, AFIDA, AND EXPANDING FEDERAL AND STATE RESTRICTIONS ON FOREIGN INVESTMENT IN US REAL ESTATE

Caren Street, John Thoms, and Anya Ram | Squire Patton Boggs

TANGIBLE TAILWINDS

Fundamentals are creating tangible tailwinds, and projections continue to trend upward just as the Aging Avalanche begins swelling the ranks of the prime senior housing demographic cohort and boosting demand. At the same time, the recent central bank rate hike cycle is undercutting development activity to the lowest levels in years and is likely to result in an uptick in sales of assets with attractive operations but misaligned capital stacks.

With many of the challenges of the pandemic now in the rearview mirror, the senior housing sector is primed for a new phase of expanded opportunity.

—

ABOUT THE AUTHORS

Robb Chapin is CEO & Co-CIO of Bridge Senior Housing, Jack Robinson is Chief Economist & Head of Research, Andrew Ahmadi is Vice President in the Client Solutions Group, and Morgan Zollinger is Director, Head of Market Research, for Bridge Investment Group.

—

NOTES

1. NIC MAP, as of Q2 2023. Moody’s Analytics, Baseline Scenario, as of June 2023.

2. Genworth, Cost of Care Survey.

3. NIC Investment Guide: Investing in Seniors Housing & Care Properties, 6th Edition.

4. NIC MAP, as of Q2 2023.

5. NIC MAP, as of Q2 2023.

6. NIC MAP, as of Q2 2023.

7. NIC MAP, as of Q2 2023.

8. NIC MAP, as of Q2 2023.

9. NIC MAP, as of Q2 2023.

10. Moody’s Analytics, Baseline Scenario, as of June 2023.

11. Moody’s Analytics, Baseline Scenario, as of June 2023.

12. Moody’s Analytics, Baseline Scenario, as of June 2023.

13. Moody’s Analytics, Baseline Scenario, as of June 2023.

14. Board of Governors of the Federal Reserve System, Distributional Financial Accounts, as of Q1 2023.

15. U.S. Census Bureau, American Community Survey One-Year Estimates: Table B19037, 2016-2021. 2020 data unavailable due to Census survey difficulties during the pandemic.

16. Board of Governors of the Federal Reserve System, Distributional Financial Accounts, as of Q4 2022.

17. U.S. Census Bureau, American Community Survey One-Year Estimates: Table B19037, 2016-2021. 2020 data unavailable due to Census survey difficulties during the pandemic.

18. NIC MAP, as of Q2 2023.

19. NIC MAP Data and Analysis Service, as of Q2 2023.

20. MSCI Real Capital Analytics, as of June 30, 2023. Includes assets and portfolios valued at $2.5 million and greater.

21. Preqin, as of Q2 2023

22. MSCI Real Capital Analytics, as of June 30, 2023. Includes assets and portfolios valued at $2.5 million and greater.

23. MSCI Real Capital Analytics, as of June 30, 2023. Includes assets and portfolios valued at $2.5 million and greater.

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY UNDERWRITTEN BY

For more than 20 years, Yardi has developed real estate investment management software that helps managers of global assets valued at trillions of dollars make informed investment decisions. Yardi Investment Suite clients include many of the world’s premier investment management funds, start-ups and partnerships of all types and sizes.

Real estate investments grow on Yardi. That’s because the Yardi Investment Suite automates complex investment management processes and provides full transparency, from the investor to the asset. Through interactive dashboards, investors can view documents and have access to reports and metrics. Collaboration is easy when your advisor or accountant is given access to view your accounts, reducing the need for emailing sensitive information.

The Yardi Investment Suite leads the real estate industry through innovation and value with fully integrated investment management, property management and accounting functionality. Fund managers and their customers can manage assets with superior efficiency and ease. Learn more.