As an increasingly popular asset class for institutional investors, single-family rentals are supported by strong future demand drivers to propel sector outperformance.

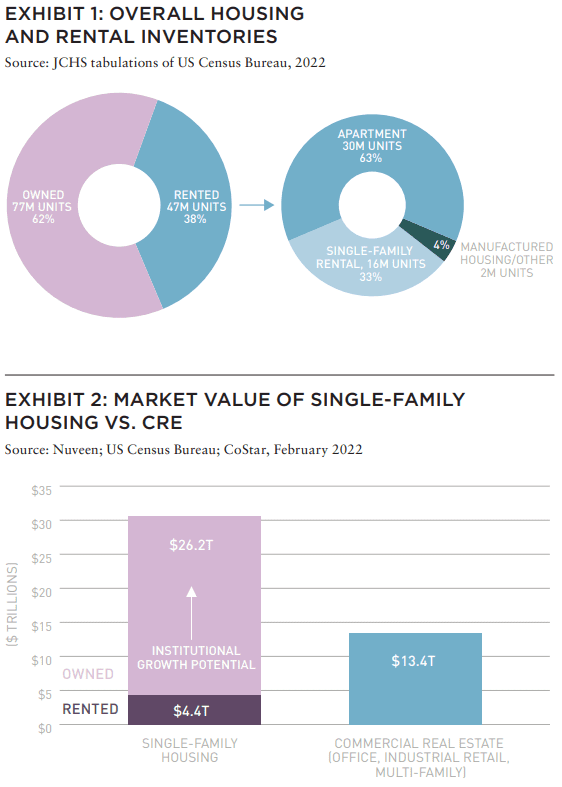

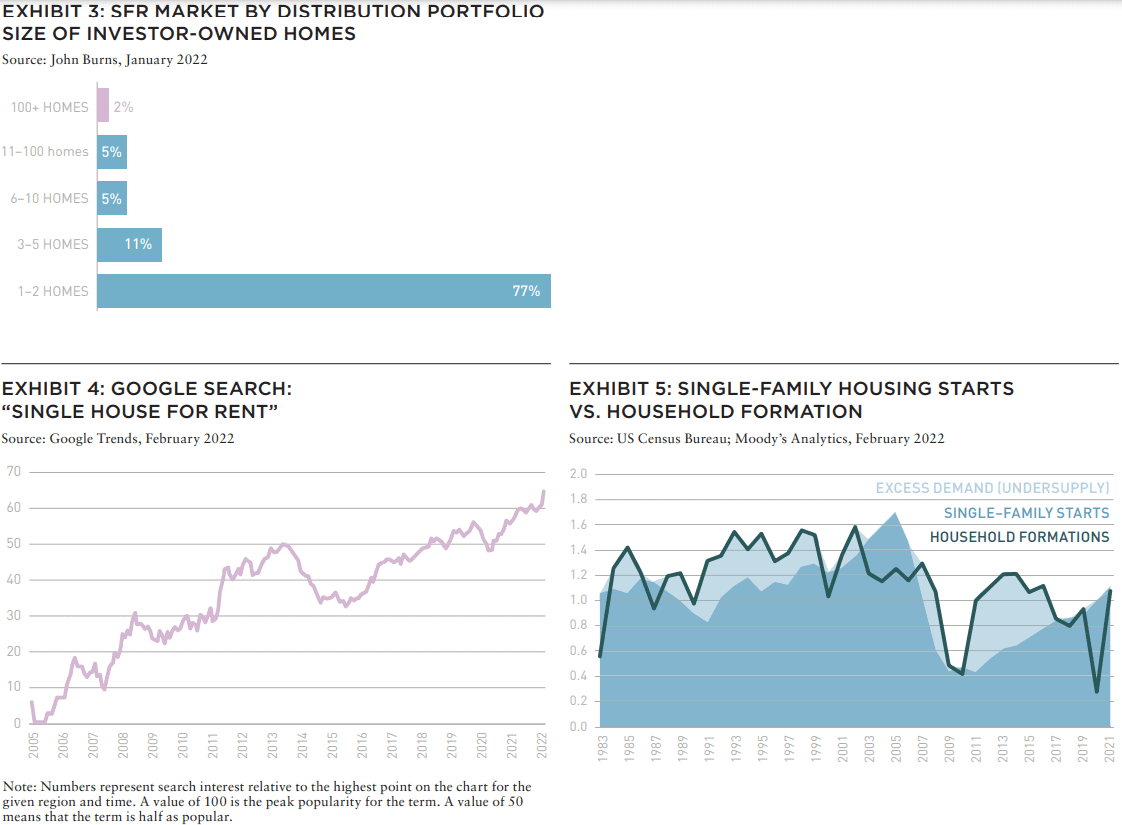

Single-family rentals (SFRs) are a sizeable investment opportunity, as the sector comprises one-third of US rental inventory with nearly 16 million units. The SFR market is currently valued at US$4.4 trillion. The majority of new SFR inventory comes from owner-occupied stock, indicating that there is potential to invest in the owner-occupied single-family housing market, currently valued at US$26.6 trillion.

In total, the single-family housing market is valued at more than US$30 trillion, which is more than double that of the traditional commercial real estate market (valued at US$13.4 trillion). The SFR market is 98% dominated by non-institutional players. In recent years, REITs and private players have entered the SFR market, starting the institutionalization of the sector.

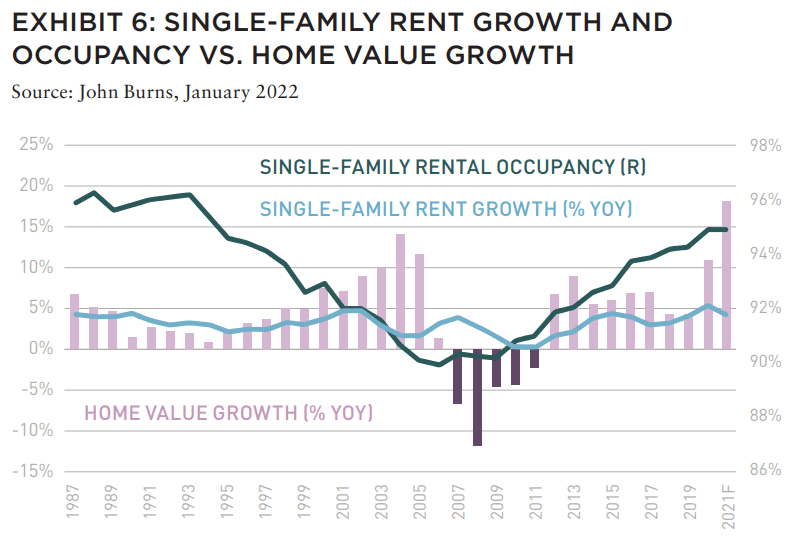

During the next decade, institutional real estate portfolios will likely transform as investors gain more familiarity with SFRs and start increasing their allocations to them. Google Search Trends data indicates that the search for “Single House for Rent” has significantly increased over the last decade (Exhibit 4), signaling the overall interest and curiosity in this property type from both potential renters and investors. We anticipate SFRs will play a more significant role in institutional real estate portfolios in the coming decades as investors have recognized their resiliency throughout the COVID-19 pandemic. But before SFRs become a part-and-parcel component of institutional real estate portfolios, investors should consider adding them to their portfolios as a way to drive outperformance and generate enhanced returns.

LACK OF SUPPLY AND OUTSIZED DEMAND

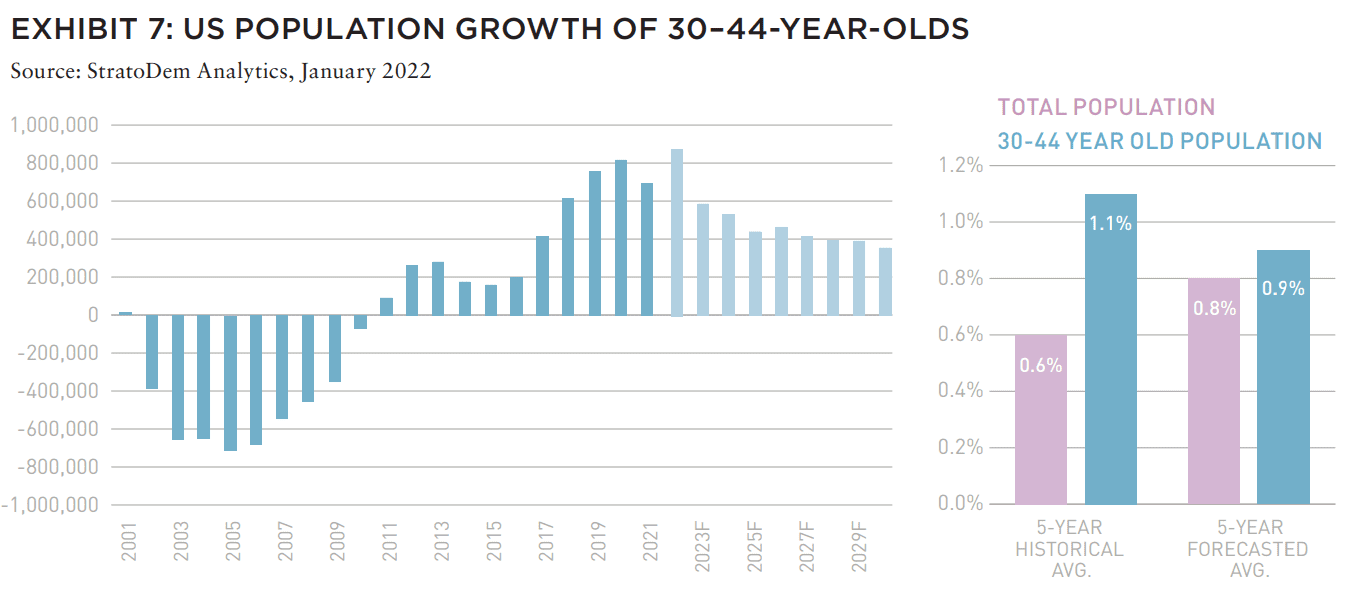

Our analysis of single-family housing starts compared to household formations (Exhibit 5) indicates that there is currently an undersupply of approximately 4.7 million homes. The lack of single-family housing supply has driven months’ supply of inventory to historical lows and home price appreciation to record highs, further inhibiting homeownership for many aspiring families. Specifically, construction for homes under 1,800 SF, an applicable proxy for a starter home, is well below historical levels.

SFRs have boasted healthy operating fundamentals throughout the last decade, including during the COVID-19 pandemic. SFR demand has improved significantly in recent years as occupancy has grown 500 BPs since the GFC from 90% to 95% in 2021 (Exhibit 6). SFR rent growth remained positive throughout prior recessionary environments, unlike overall home value growth, which turned negative.

KEY DEMAND DRIVERS

SFRs are favorably positioned to benefit from various demand drivers in the next several years including:

• Demographic wave into the prime SFR age cohort

• Continued migration to suburbs and Sunbelt markets

• Millennials outgrowing apartments

• Millennials’ financial headwinds to homeownership

DEMOGRAPHIC WAVE INTO KEY RENTER COHORT

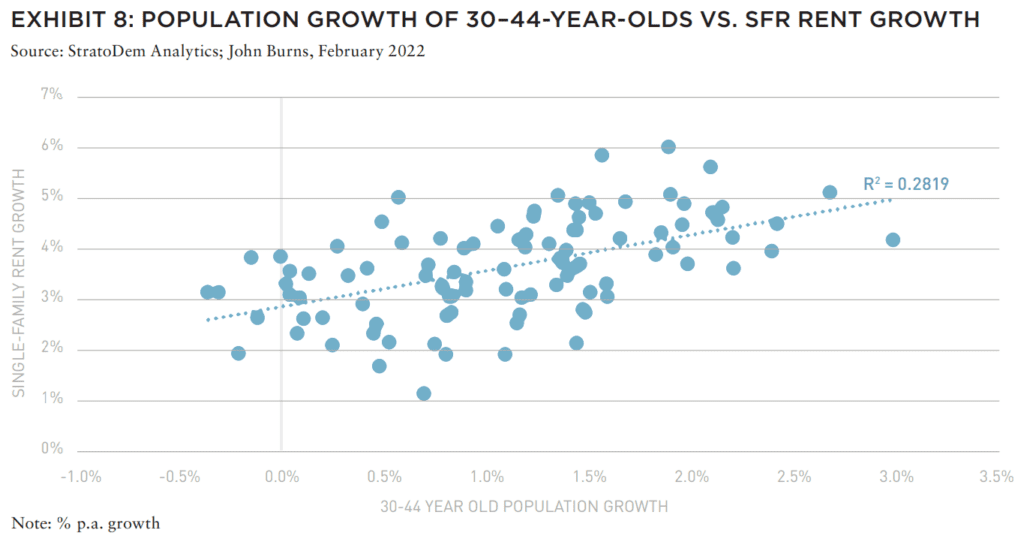

Certain key demographic shifts occurring in the US will have profound implications for alternative housing sectors, including SFRs. The aging of millennials into the key SFR cohort (ages 30– 44) is a critical secular tailwind for the sector (Exhibit 7). This key age cohort is projected to grow from 65.7 million in 2021 to 70.2 million in 2030. The growth of this cohort has outpaced the overall US population over the last five years and is projected to continue outpacing the US population over the next five years. Historically, the growth of this key age cohort has empirically proven to be a driver of SFR rent growth (Exhibit 8).

SUBURBAN RESURGENCE AND MIGRATION TO THE SUNBELT

It is important to recognize that millennials are more mobile than prior generations and are not necessarily prepared to purchase a home and settle in one area. Consequently, the top reason single-family renters prefer to rent than buy is due to the flexibility to move if desired or needed. SFRs are favorably positioned in a post-COVID-19 environment given the pandemic’s profound impact on urban areas.

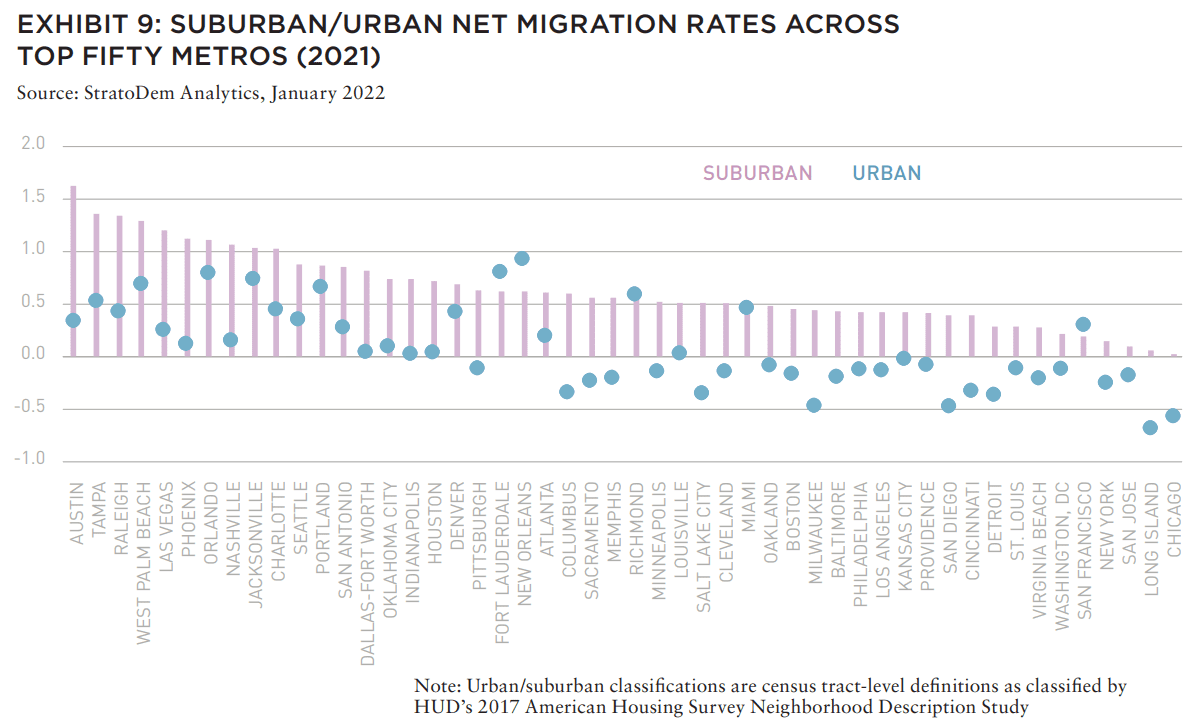

The suburban resurgence forecasted for this decade is likely to accelerate as a result of the COVID-19 pandemic, fueling demand for SFRs. During the COVID-19 pandemic, city dwellers fl ed major urban areas for nearby suburbs and Sunbelt markets. Across the majority of metropolitan areas in 2020 and 2021, net migration rates were stronger in suburban areas than urban areas. According to the National Association of Realtors (NAR), 54% of homes purchased by those ages 31 to 40 were located in suburban locations, and the leading factor that led to moving was a life change (e.g., addition to family, marriage, etc.).

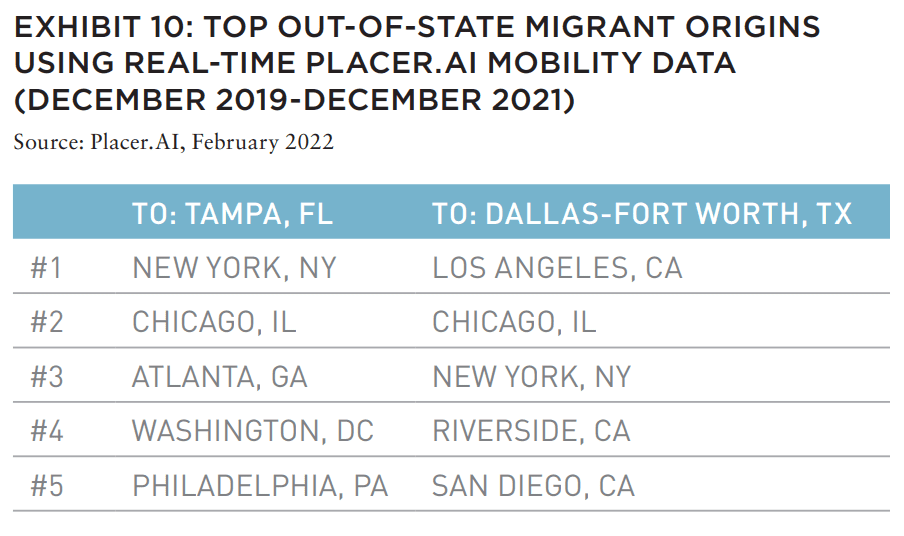

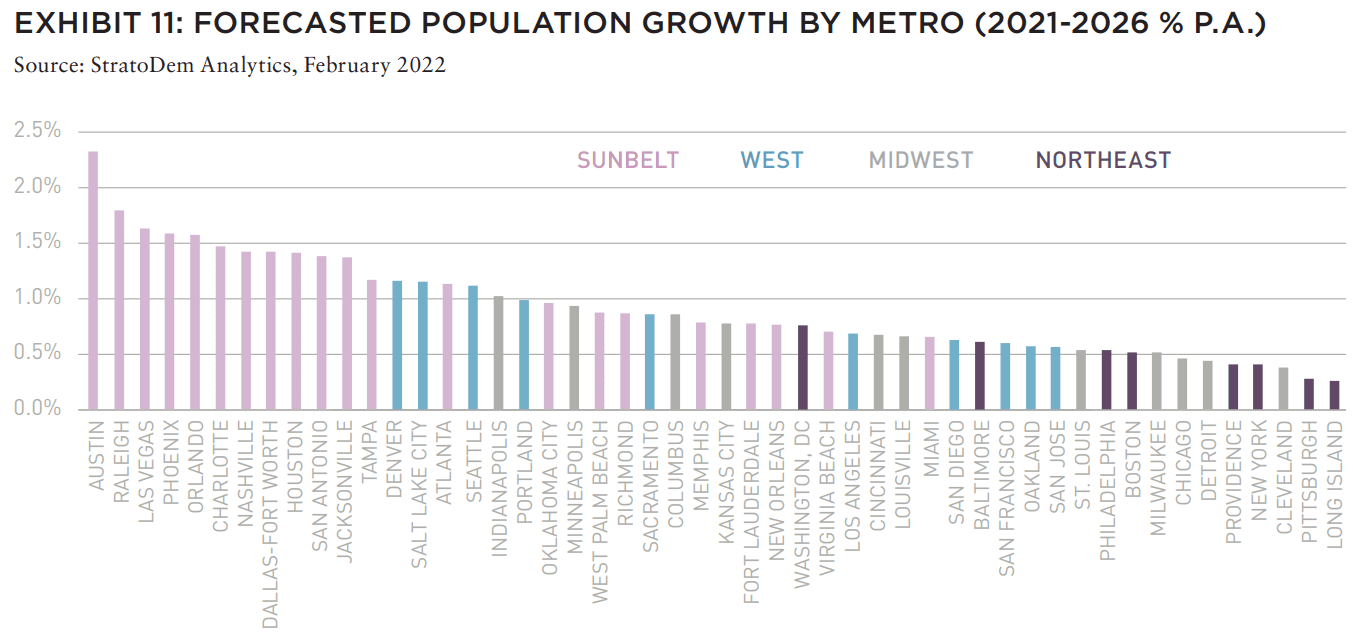

An analysis of Placer.AI geolocation mobility data validates that the majority of those moving to Sunbelt markets have migrated from more expensive coastal markets. For example, over the last two years, the most migrants to Tampa, originated from New York City, while the most migrants to Dallas-Fort Worth originated from Los Angeles. We believe the out-migration from coastal markets will accelerate due to unfavorable affordability, high taxes, and elevated impacts from the COVID-19 pandemic. Forecasted migration data indicates Sunbelt markets will continue to lead the nation for population growth. This trend is favorable for SFRs given the large opportunity set available in the Sunbelt markets.

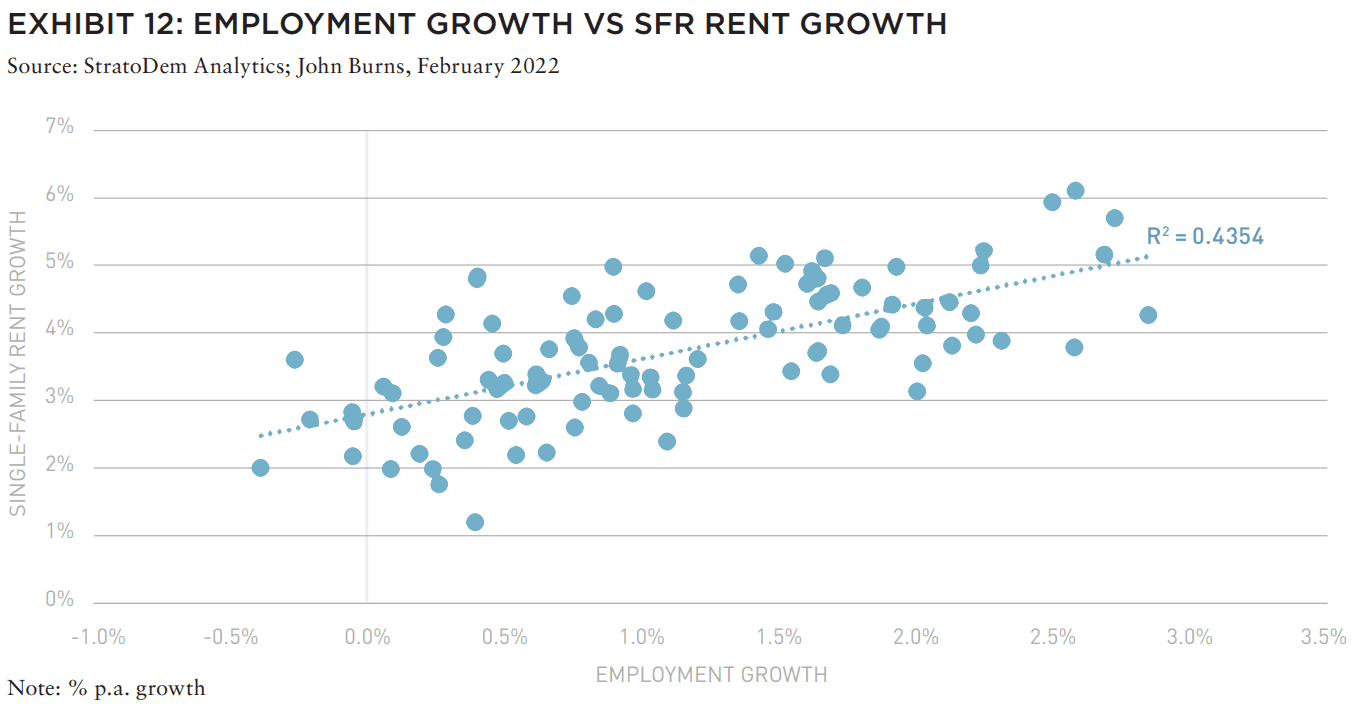

Several Sunbelt markets have benefitted from favorable employment growth tailwinds in recent years given the region’s favorable business environment and in-migration of an educated workforce. Employment growth has empirically proven to be a critical driver vs. SFR rent growth. Markets including Nashville and Charlotte have benefitted from strong employment growth and consequently have exhibited strong SFR rent growth. The COVID-19 pandemic sparked numerous company expansions and relocations to the Sunbelt markets for a more business-friendly environment. The imminent employment growth in this region as a result of these expansions and relocations will further bolster the SFR market.

MILLENNIALS OUTGROWING APARTMENTS

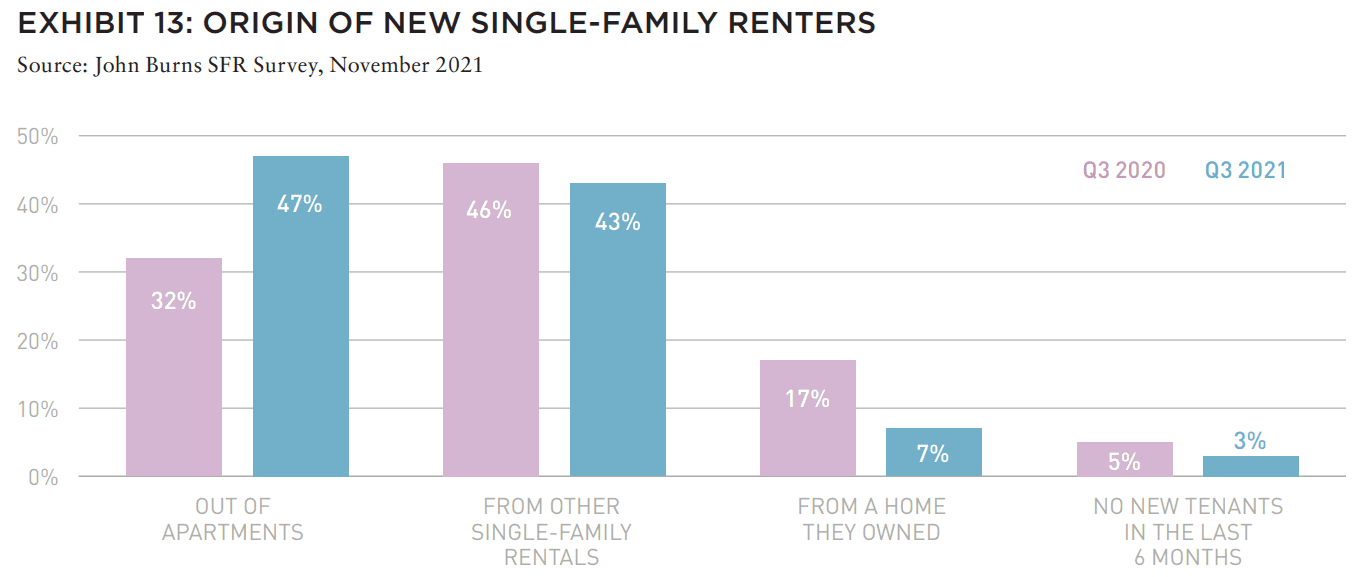

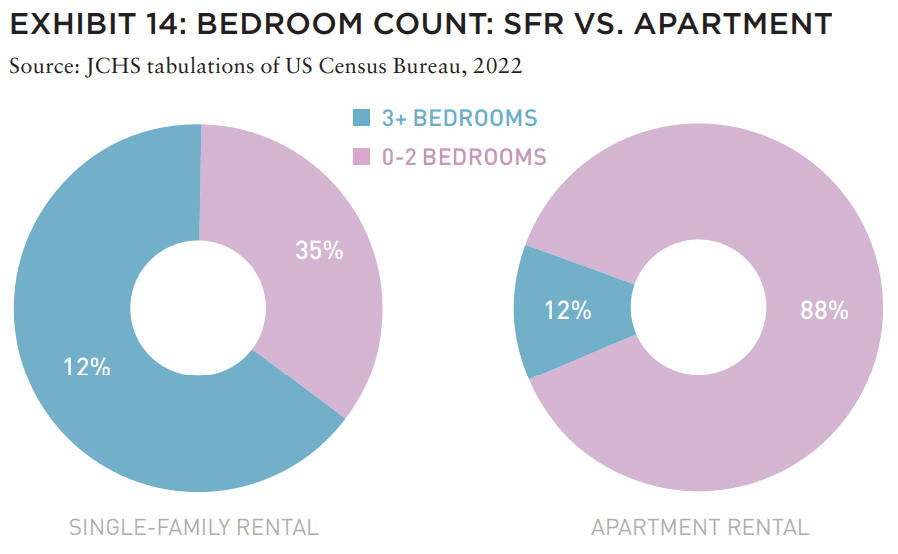

Throughout the last decade, millennials have been a major driver of conventional apartment demand. As millennials age, start families, and demand space for home offices and remote learning, they are likely to outgrow their one and two-bedroom apartments. Yet, only 12% of apartment units in the US have three or more bedrooms, compared to 65% for single-family homes. Nearly one-half of new single-family renters in Q3 2021 moved from apartments, according to John Burns’ SFR Survey. The permanent adoption of flexible WFH policies as a result of the pandemic is likely to serve as an additional tailwind for SFRs as professionals demand more space in their homes to conduct business.

MILLENNIALS’ FINANCIAL HEADWINDS TO HOMEOWNERSHIP

Purchasing a single-family home would be the next natural step for millennials as they age, but this is out of reach for many. Millennials have experienced two recessions in their young adult lives (GFC and COVID-19) and are largely unable to afford a 20% down payment and mortgage. This will be a key future driver of SFR demand.

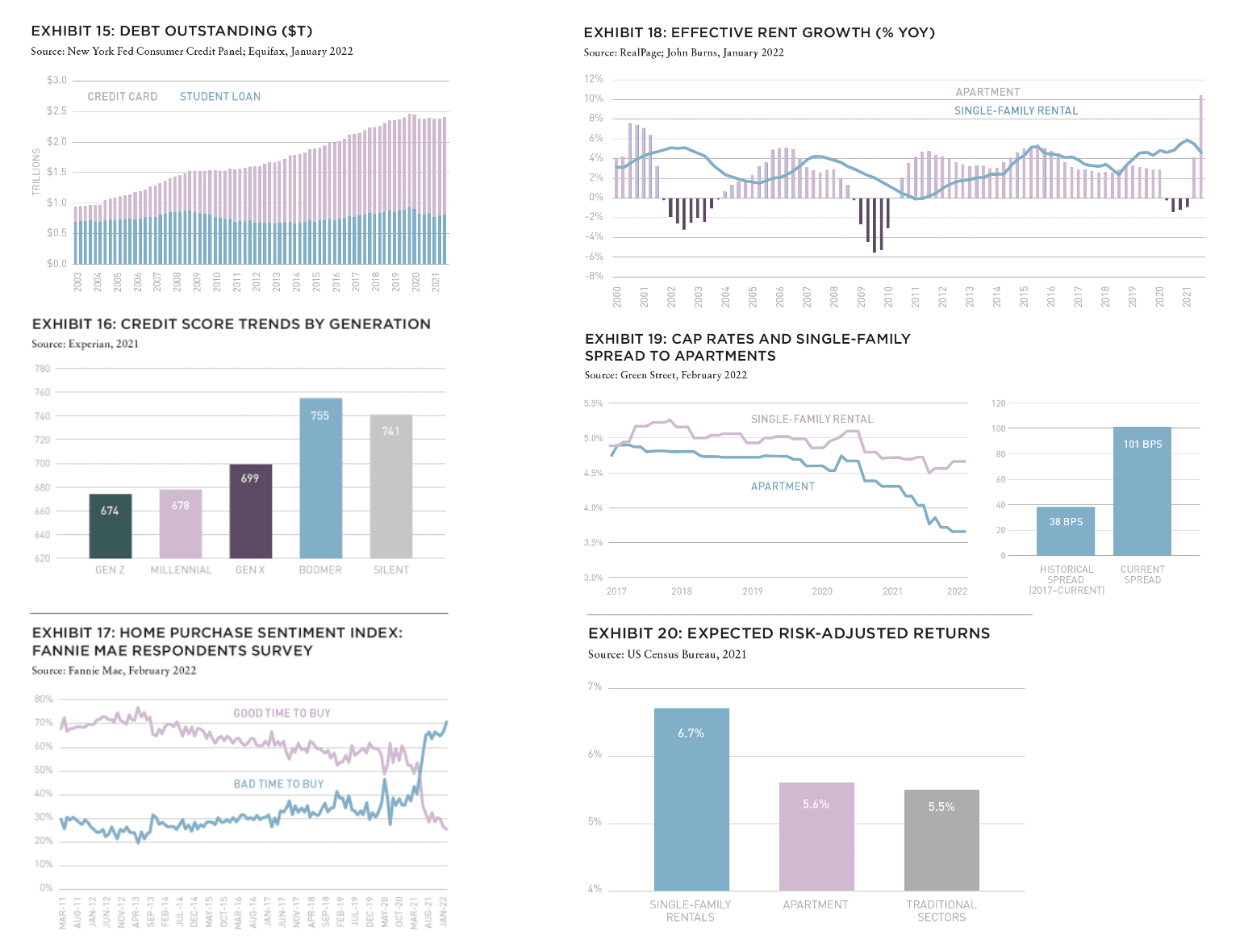

Mortgage lenders have remained conservative relative to the GFC. A poor debt-to-income ratio was the leading reason mortgage lenders rejected buyer applications for those ages 31–40, according to NAR. Experian data indicates that student loan debt continues to be the major driver of debt compared to credit cards. Poor credit is an additional headwind for millennials. Consequently, millennials currently have disadvantaged FICO scores compared to older generations, posing additional challenges for homeownership. High amounts of debt and low FICO scores will prevent millennials from owning homes at the same rate as previous generations. Our analysis of household net worth for those under 44 years old indicates that across 64% of metropolitan areas, households under 44-years-old do not have adequate funds for a 20% down payment.

As a result of these affordability headwinds, coupled with current supply constraints, younger households have grown pessimistic at near-term homeownership. A recent Fannie Mae poll indicated that a record-low 25% of respondents reported that it’s a good time to buy a home, compared to 69% of consumers who reported that it’s a good time to sell. While potential homebuyers believe that now is a bad time to buy a home due to elevated pricing, the relative pricing remains attractive for institutional investors.

Institutional investors are accustomed to placing a value on an income stream, unlike traditional homeowners. By this metric, cap rates on single-asset SFR purchases are approximately 100 BPs wide of apartment properties, indicating a compelling discount. Moreover, once a small portfolio of SFRs has been aggregated, the income stream for an investor is much more stabilized and represents a more efficient investment, resulting in a further 75–125 BP premium to a single-asset SFR purchase. As such, while home values may seem elevated to an individual owner, we believe now is a compelling time to buy single-family homes to rent.

RESILIENT HISTORICAL AND PROJECTED PERFORMANCE

Historically, SFRs have achieved stronger rent growth, NOI growth, and overall commercial property price index (CPPI) growth than apartments. SFR rent growth has consistently been extremely resilient as it has never turned negative. Throughout several recessions, apartment rent growth has turned negative and has had higher volatility compared to SFR rent growth, which was steadily positive and less volatile. Similarly, SFR NOI growth has remained positive throughout the COVID-19 pandemic, unlike apartments and traditional real estate property types overall that turned negative. Given the sector’s numerous tailwinds, SFRs have favorable NOI growth and return projections. Further, the SFR sector has historically been higher yielding than the apartment sector. Since 2017, SFRs have achieved nearly a 40 BP premium over apartments. This spread has widened since COVID-19 and is currently over a 100 BP premium.

Given the sector’s favorable pricing relative to other property types and resilient demand drivers, SFRs are expected to achieve higher risk-adjusted returns than apartments and traditional commercial real estate property types overall. Therefore, investors should consider adding SFRs to their portfolios as a way to drive outperformance and generate enhanced returns.

—

The author presents a compelling investigation of the demand drivers for SFR in the US, reasoning that millennials have outgrown urban apartments and are looking for more space, particularly in low-cost Sunbelt suburban areas. The increasing cost of home ownership, in addition to economic shocks resulting from the COVID-19 pandemic, has accelerated the demand for this type of housing. Investors in this potentially immense asset class could achieve higher returns for relatively lower risks than other types of real estate, including multifamily apartments.

While the author offers evidence that in the past two years suburban areas saw greater growth than urban areas and suggests that this is the acceleration of an existing trend, it is unclear if there is any risk of reversal. It is not impossible to imagine a scenario in which suburban dwellers once again seek easy access to amenities of urban areas (e.g., childcare), especially as pandemic restrictions dissipate. What evidence is there that this trend will remain?

The article identifies a supply shortage of new SFR homes, but does not explore the reasons. Is the shortage potentially related to COVID-19 market disruptions, which could be reversed in the short- or midterm? Or is this a structural issue that a potential investor could benefi t from as a longterm barrier to entry?

Although it is beyond the scope of this article, further investigation should also discuss the mechanics of gaining exposure to this sector. It is challenging for an institutional investor to build a platform of signifi cant scale and manage the operations of an SFR portfolio. This challenge may explain why the vast majority of SFR is not currently institutionally owned and most existing portfolios only include one to two homes.

Peter Grey-Wolf

Editorial Board Member, Summit Journal

Vice President, Wealthcap

—

ABOUT THE AUTHOR

Daniel Manware is a Director for Nuveen Real Estate. He is responsible for evaluating market dynamics and trends across all property types in order to create strategic investment recommendations for portfolio management teams.

—

EXPLORE THE FULL ISSUE (SPRING 2022)

MARCHING BACKWARDS INTO THE FUTURE

The new 2022 AFIRE International Investor Survey Report reveals future institutional investment trends as the pandemic transformed how we live, work, and play.

Gunnar Branson and Benjamin van Loon | AFIRE

CITIES THAT WORK

What is it that makes London, Stockholm, Berlin, Amsterdam, and Paris the top European cities for office investment? And what could this mean for other global cities?

Dr. Megan Walters | Allianz Real Estate

SURVEY SURFEIT

Be careful about advice you hear from surveys— it will not always play out as expected.

Jim Costello | MSCI Real Estate

NEW WORKING AGE

Outside of WWI and II, the US working age population has never declined. As of 2021, that statement is no longer true.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

SELECTIVE FRAMEWORK

Two years after offices closed due to the COVID pandemic, the debate over the longterm future of the office continues. What should office investment look like going forward?

Dags Chen, CFA; Ryan Ma, CFA; and Ryan LaRue | Barings Real Estate

GARDEN VIEW

US garden apartment investments are offering outsized return potential –but access remains a challenge.

Martha Peyton, PhD | Aegon Asset Management

SINGLE-FAMILY DEMAND

As an increasingly popular asset class for institutional investors, single-family rentals are supported by strong future demand drivers to propel sector outperformance.

Daniel Manware | Nuveen Real Estate

ESSENTIAL HOUSING

The US is in the middle of one of the biggest housing crises that the country has ever seen. It needs a more resilient approach to housing.

Todd Williams | Grubb Properties

LODGING TAKES THE LEAD

As a labor-intensive and service oriented asset class, hospitality is uniquely positioned to be a leader in advancing sustainability goals for investors.

Charlotte Kang, Geraldine Guichardo, Lori Mabardi, and Emily Chadwick | JLL

CARRY ON, CARRY OVER

While continuation vehicles were once viewed as a signal of delay or failure, market sentiment is rapidly changing.

Max LaVictoire and Ashley Anderson | Hodes Weill & Associates

RENEWING ETHICS

A note from AFIRE’s Ethics Chair on the need for maximizing ethics in an age where globalization is under threat.

El Rosenheim | Profimex