This article appears in Summit Journal (Summer 2020) | Download PDF

COVID-19 AND LOGISTICS: WHAT HAVE WE LEARNED SO FAR, AND WHAT WILL BE THE LASTING IMPACT ON THE SECTOR AS IT FACES A NEW STAY-AT-HOME ECONOMY?

COVID-19 has put an end to the lengthy global economic expansion. Estimates of the magnitude and duration of the negative impact of the pandemic span a broad range.

On the demand side, economic activity has been suppressed as consumers are constrained by restrictions, fear, and/or job loss. On the supply side, disruption in the production and movement of goods (and people) around the world has tested complex supply chains. Logistics real estate users have had to handle both a shortage of goods and a subsequent replenishment surge. Demand for space will continue to evolve as consumer behaviors and supply chains shift.

To build an understanding of the impact of COVID-19 on logistics real estate, it helps to divide the timeline of the pandemic into three phases: the Stay-at-Home Economy, the Recovery, and the New Normal.

In each phase, there are key trends that could lead to either increased or decreased demand for logistics real estate. With this methodology applied to Prologis’ global portfolio, which includes approximately 1 billion SF/92.9 million SM of logistics space, alongside data derived from the company’s diverse customer base, where no single industry accounts for more than 15% of base rent, we can extrapolate an understanding of how COVID-19 has impacted both logistics real estate and global supply chains—and what these impacts could mean for the future of the sector.

INDUSTRY PERFORMANCE DURING COVID-19

SUPPLY AND DEMAND IN THE STAY-AT-HOME ECONOMY

When countries around the world issued stay-at-home orders earlier in 2020, a sudden shift took place that resulted in a demand surge across certain industries. This shift emphasized the crucial role that logistics real estate plays in everyday life.

New sources of demand were driven by:

- Stockpiling. Consumers rushed to stock up on grocery and consumer products. (They purchased these items at retailers that collectively represent more than 24% of the Prologis customer base.)[1] In March, US grocery sales jumped by nearly 30%.[2] Rapid replenishment operations restocked store shelves, while grocery deliveries from stores to homes skyrocketed.

- Medical Support. Demand for medical supplies, pharmaceuticals, and personal protective equipment spiked. Shifting COVID-19 hot spots in various states and countries also highlighted the need for responsive supply chains.

- Inventory Building. Volatility caused by China’s work stoppages led to shipments doubling at a time when many customers had no store shelves to fill. This drove increased need for short-term space across a range of industries, with a sharp increase in demand from logistics companies that specialize in supply chain management. Within the Prologis global portfolio, short-term leases rose 40% year-over-year in the 30 days through April 17, 2020.

- Office and School Closures. Almost overnight, households around the world went from transporting family members to work and school and attending social events to concentrating all of these activities at home. Retail sales of select products within the diversified retail category and electronics/appliances (each of which represents roughly 8% of the Prologis customer base), increased sharply (e.g., school supplies, computers, monitors, desks, and chairs).

- Limited Mobility. Estimates suggest e-commerce sales rose by around 50% in April and May 2020 (versus the recent trend of approximately 15%),[3] including outsized gains in previously under-penetrated categories such as grocery. E-fulfilment operations accounted for nearly 40% of new leasing in March and April within the Prologis portfolio. In addition, at 11% and 5% of the Prologis customer base, respectively, many transportation/distribution and packaging/paper customers are encountering increased parcel volumes.

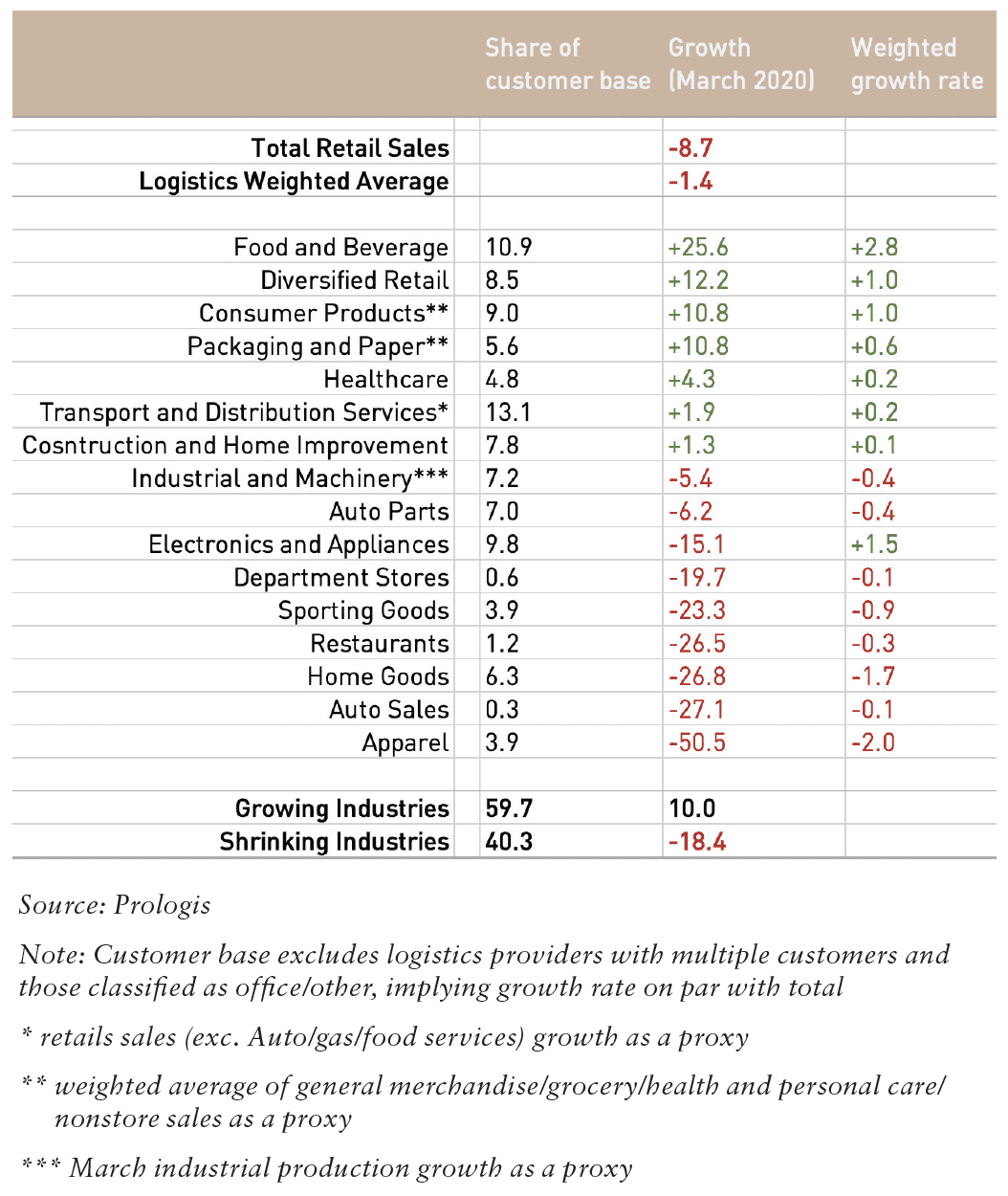

March retail sales highlight the resilience and outperformance of the logistics sector. US retail sales revealed a sharp bifurcation of industry growth during the Stay-at-Home phase. The following table lists retail sales changes (along with share of the logistics real estate customer base) as of March 31, 2020.[4] Approximately 60% of these customers experienced growth, while 40% saw revenues decline. In total, logistics real estate-weighted industries outperformed the national average by 730 BPS, with a decline of 1.4% versus -8.7% for all of retail.

New behaviors symptomatic of the stay-at-home phase have created significant challenges in some industries. In total, direct logistics real estate exposure to the most hard- hit industries is small (e.g., 3-4% of the Prologis customer base). Those hit hardest include auto sales, travel/tourism/conventions/entertainment, restaurants, department stores, and aerospace/oil and gas. Particular segments of these industries will likely also face challenges, including small- to mid-sized businesses that, irrespective of government support, don’t have the operational flexibility to handle a pandemic. Industries with a notable concentration of these affected segments include transportation/distribution, food and beverage, and apparel/sporting goods.

RE-TOOLING SUPPLY CHAINS FROM EFFICIENCY TO RESILIENCY

The pandemic has exposed the trade-offs supply chains have made in tuning for efficiency. Several customer groups stand out for having very lean supply chains at present, including food and beverage, electronics/appliances, healthcare, and diversified retail. Going forward, many businesses are likely to build higher inventory levels to ensure resilient supply chains.

Each 100 BPS of growth in inventories is estimated to require an additional 57 million SF/5.3 million SM of US logistics demand. In addition, carrying costs will remain low given record-low interest rates. In our own research, we modeled 5-10% inventory growth, which would produce additional space needs of 285-570 million SF/26.5-53 million SM in the US. This shift could lead to broad-based logistics real estate demand growth, with an emphasis on large consumer populations, access to transportation, and modern facilities.

Accelerated e-commerce adoption and higher inventory levels have the potential to generate 400 million SF/37.1 million or more of additional US logistics real estate demand, or 150-200 million 13.9-18.6 million SM per year for two to three years. Re-tooling supply chains for increased e-fulfilment should create incremental net demand of 140-185 million SF/13-17.2 million in total.[5] E-fulfilment demand should be highest in locations near end consumers. Inventories could increase by 5-10% in a bid for resiliency, producing 285-570 million SF/26.5-53 million SM of aggregate incremental demand.[6] New demand from inventory growth could be spread more evenly throughout distribution networks.

Grocery, healthcare, consumer products, and diversified retail are among the top segments poised for lasting e-commerce impact and/or inventory re-assessment. (Accounting for approximately one-third of the Prologis portfolio, these customer groups already represent an overweight portion of the logistics real estate customer base, relative to the overall economy, and should be well-positioned for outperformance throughout the recovery period.) As a result, adjustments to supply chains could happen quickly as uncertainty abates.

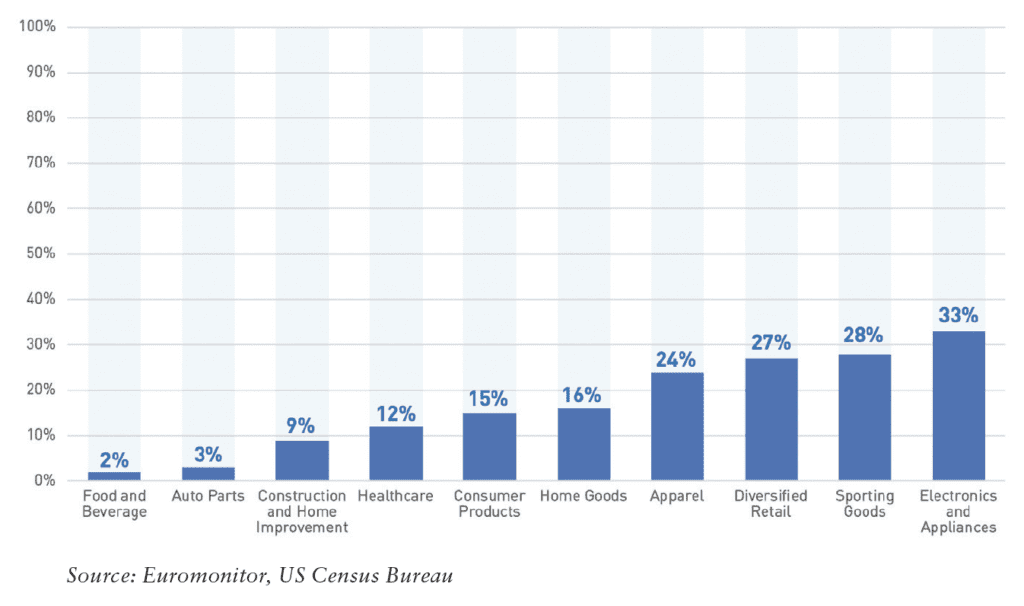

IMPACT OF ACCELERATED E-COMMERCE ADOPTION ON SUPPLY CHAINS AND LOGISTICS REAL ESTATE

Faster e-commerce adoption should require greater supply chain investments from low-penetration industries such as grocery. Grocers have recently announced 3-4x year-on-year increases in online sales. Several industries are still in the early phases of e-commerce adoption, including food/beverage and construction/home improvement. With the caveat that this growth may not be permanent, much of it could in fact become permanent as new adopters become familiar with the benefits of e-commerce.

E-COMMERCE SHARE OF RETAIL SALES (AS OF 2019)

Growth in these categories will reinforce same- and next-day service requirements. Legacy 3- to 5-day delivery times were a barrier to adoption for these categories, where consumers typically have short planning horizons. These categories have relatively small e-fulfilment operations, and re-tooling supply chains will require substantial real estate investments. Third-party logistics specialists could benefit from this shift.

Each 100 BPS of share shift from traditional brick-and-mortar to e-commerce translates to 46 million SF/4.27 million SM of net demand in the US. With the penetration rate already rising by 100-150 BPS annually,[7] March through mid-April’s e-commerce growth of more than 30% [8] suggests the rate could rise by 300-400 BPS in 2020, generating an incremental 140-185 million SF/13-17.2 million SM of net demand (accounting for cannibalization of brick-and-mortar).

Some of this demand has already surfaced in the race to respond to the coronavirus pandemic, but the reality of implementing this expansion in distribution capabilities may take more than a year to complete. In addition to growing retailer demand, parcel delivery and paper/packaging businesses should benefit from increased direct-to-consumer shipments. Service requirements and the need to optimize transportation costs will likely increase demand for distribution facilities in urban areas near end consumers.

WHAT’S NEXT FOR LOGISTICS?

The logistics real estate customer base comprises companies that are both benefiting from and being challenged by sudden shifts in behavior, with net outperformance in:

- The Stay-at-Home Economy. Demand is surging in large customer industries such as food and beverage, diversified retail, consumer products, and transportation/distribution. Retail sales data indicate that 60% of industries within logistics real estate are growing, while 40% are shrinking.

- The Recovery Stage. Businesses that were able to adapt to new patterns of consumer behavior should increasingly focus on optimizing their supply chains for the “new normal,” including a re-assessment of ideal inventory- to-sales ratios. Businesses that serve essential and basic daily needs historically have outperformed in terms of retail sales growth during recessions.

The lessons learned from the pandemic will also add demand tailwinds to logistics real estate. For example, as we look at the future, Prologis Research estimates that 400 million SF/37.1 million SM or more of total additional US logistics real estate demand will be created in the next two to three years as companies adjust to greater e-commerce volumes and higher inventory levels.

—

ABOUT THE AUTHOR

Melinda McLaughlin is Vice President of Research for Prologis, the global leader in logistics real estate with a focus on high-barrier, high-growth markets.

NOTES

1. Prologis global portfolio as of April 15, 2020.

2. US Census Bureau, Advance Retail Sales report (March 2020); census.gov/retail/index.html.

3. Giselle Abramovich, “Online Shopping During COVID-19 Exceeds 2019 Holiday Season Levels,” Adobe Blog (June 12, 2020), theblog.adobe.com/onlineshopping- during-covid-19-exceeds-2019-holiday-season-levels.

4. Prologis portfolio, by base rent.

5. Based on US$5.5T 2019 retail sales, of which 100 bps is US$55 billion in retail sales. Intensity of use as follows: 1.168 million SF per billion for online and 328,000 SF per billion in-store (840,000 SF net per billion). revenue; market rent growth weighted by PLD NOI is ~8%.

6. Based on coefficients from a two-factor OLS regression of real retailer inventories and real retail sales on US logistics real estate demand growth, spanning from 1992 to 2019.

7. US Census Bureau Quarterly E-commerce Report; census.gov/retail/ecommerce/historic_releases.html.

8. Rakuten Intelligence

—