Anticipated moderation in new developments and the positive outlook for rent growth signal a more balanced multifamily market. Until then, investors should maintain a strategic and long-term perspective.

Multifamily has remained a staple in most investors’ US portfolios, and with good reason. Unlike other property types whose basic function may evolve with changing market dynamics or technological advancements, multifamily properties consistently satisfy a fundamental human need for housing.

Today, this need is complemented by a for-sale market marked by low inventory and high prices, providing some resiliency against an otherwise uncertain investment backdrop. Even still, the sector has its growing pains. Multifamily deliveries for 2023, on an absolute basis, set high water marks in many markets, and projects under construction suggest another meaningful year of new supply into 2024. Assuredly the next year and a half will challenge investors’ commitment to the sector, but a closer look at historical development cycles suggests there is reason for optimism in the medium term.

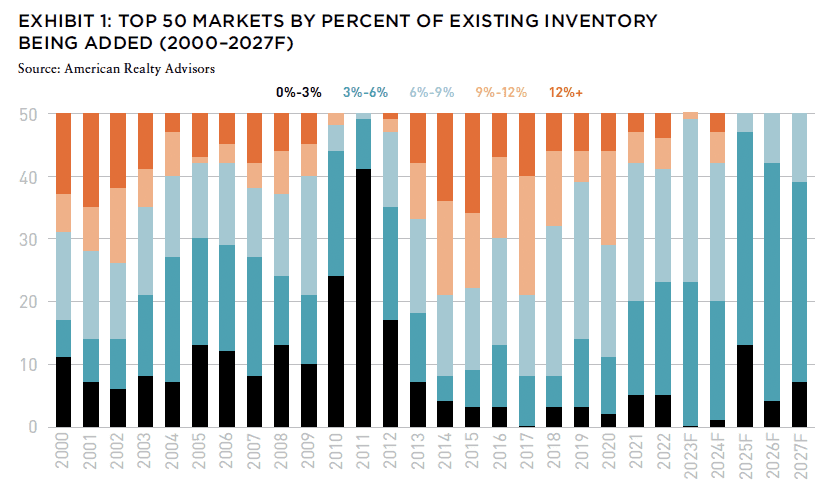

To fully understand the context of the latest supply wave in the multifamily market, this analysis measures the volume of incoming units relative to each market’s existing inventory, expressed as a percentage. This method provides a contextualized view of supply impacts on local fundamentals, compared to how an exclusive focus on the absolute number typically masks these impacts, allowing for consistent comparisons across markets. The effect of adding a thousand new units in a market with only one thousand existing units (an addition of 100%) is likely to be materially different than adding the same number into a market of ten thousand existing units (where the new supply represents the addition of 10% of inventory).

CURRENT AND FUTURE WAVES

Though the current wave of new supply represents a peak regardless of an absolute or relative evaluative lens, it otherwise seems to fit a very logical and routine national supply cycle.

A detailed look into the supply data from 2000 to 2027—inclusive of a five-year forecast period—underscores this point. During the four-year period from 2014 to 2017, more than half of the top fifty US markets experienced an increase in their inventory of 9% or more; a scale comparable to the current situation where 68% of markets are seeing similar levels of supply growth (Exhibit 1). A similar trend of heightened supply growth is also evident in 2001 and 2002, suggesting that such surges in supply are typical occurrences within the multifamily sector.

In periods marked by significant supply increases, a subsequent reduction in construction activity typically follows. This cyclical ebb and flow becomes clear when noting that, after each surge, the number of markets with robust supply growth exceeding 9% of existing inventory dwindled to fewer than 12.

At the same time, the number of markets experiencing more subdued supply growth—specifically, increases of 6% or less relative to existing inventory—rose to encompass nearly half of major markets in tandem.

The forecasts from this present analysis for 2025 through 2027 align with this historical pattern, predicting a similar pullback in new multifamily developments following the surge in 2023 and 2024.

By 2025, 47 of 50 markets are expected to reduce their development pipelines to 6% or less of existing inventory, with this trend projected to continue in 2026 (42 markets) and 2027 (39 markets). The anticipated moderation in development activity across this broad swath of the national apartment landscape is likely to stabilize supply levels and jumpstart a return to a more balanced market fundamentals.

DETAILING THE CONSENSUS VIEW

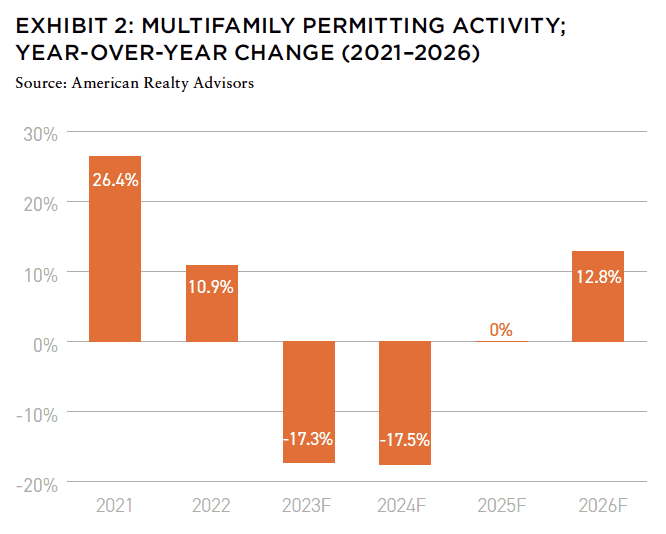

Recent permitting data supports the forecasted decline in deliveries from 2025 to 2027. Multifamily permitting activity is anticipated to contract by 17.3% this year, falling a further 17.50% in 2024 and flat in 2025 (Exhibit 2).

Considering that permitting typically precedes multifamily development by an average of seventeen months, this pattern in contracting activity bolsters the credibility of forecasts anticipating a reduction in supply pipelines in the outer years.1

This is good news for multifamily asset holders, as it signals a period of less aggressive supply growth, allowing for the existing inventory to be more fully absorbed and potentially leading to a more predictable and manageable market environment.

While a 6% average market-wide addition may not seem like a meaningful enough reduction to be conducive to rent growth, the data show that this has been a fairly healthy level.

On average, 32 of 50 markets, or 64% of markets, experience an average annual growth rate of 6%–9% to their inventories in a given year over the long term. This suggests that a 6–9% stock addition reflects general market stasis and is generally supportive of fundamentals.

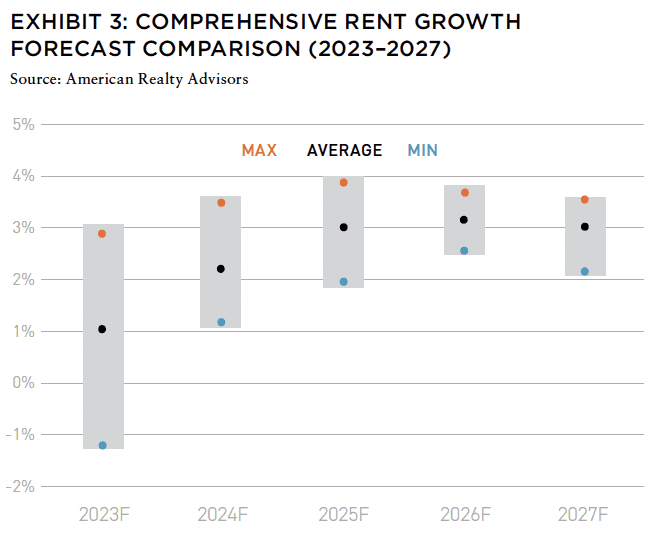

The consensus view is for this relative improvement in delivery pipelines to create an upswing in and a generally more convicted outlook for rent growth—another point for the pro-multifamily camp. Even three quarters into the year, the volume of supply today is creating materially different views of where annual rent growth will land.

The spread between the most optimistic and most pessimistic views is considerable, denoting a 411-basis point possibility range (Exhibit 3). Wider outcome bands denote greater uncertainty, which tends to influence sentiment; but there is reason to believe the future looks brighter.

From 2024 onwards, the gap between the highest and lowest forecasts begins to close. This general alignment among providers demonstrates a collective confidence in the market’s resilience and future direction that should help calm jittery nerves. While it’s unlikely we will see the anomalously high rent growth levels recorded in the past two years, the consensus is that rent growth will recover and return to more normal, sustainable levels.

LOOKING FORWARD

As we navigate the current multifamily landscape, it’s clear that the market is undergoing a period of adjustment. It’s important for investors to remember that the current surge in multifamily supply, while significant, is part of a cyclical market phase presenting both challenges and opportunities.

History has shown that the multifamily sector is resilient, capable of adapting to and absorbing fluctuations in supply. While some markets may temporarily experience oversupply, this is largely a transient stage in the broader market cycle.

Looking forward, the anticipated moderation in new developments and the positive outlook for rent growth signal a return to a more balanced multifamily market. Until then, investors should be encouraged to maintain a strategic and long-term perspective.

The multifamily market is on a path to stabilization and growth, and those who navigate this phase with patience and insight may be well positioned for the future.

IN THIS ISSUE

NOTE FROM THE EDITOR: WELCOME TO #14

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: CLIMATE-RESPONSIVE REAL ESTATE INVESTMENT

Benjamin van Loon | AFIRE

INSURING FOR ELSEWHERE: STRIPPING THE CASHFLOW FROM THE DEAL

Paul Fiorilla | Yardi

MARKET OUTLOOK: MODEST GROWTH AND RETREATING INFLATION IN 2024

Martha Peyton, CRE, PhD | LGIM America

UNDERPERFORMANCE PARADOX: NEW RESEARCH QUESTIONS THE VALUE OF PRIVATE REAL ESTATE FUNDS

William Maher, Taylor Mammen, Ben Maslan | RCLCO Fund Advisors

NAVIGATING THE CURVE: RESILIENCE, ADAPTATION, AND PREPARING FOR 2024

Jack Robinson, PhD | Bridge Investment Group

LIQUIDITY FREEZE: POTENTIAL SOLUTIONS FOR COMMERCIAL REAL ESTATE

Christopher Muoio | Madison International Realty

SUPPLY WAVE: REASON FOR OPTIMISM IN THE MULTIFAMILY SECTOR

Sabrina Unger, Britteni Lupe | American Realty Advisors

MANAGE WHAT YOU MEASURE: UNDERSTANDING EXPENSE INFLATION IN APARTMENTS

Gleb Nechayev | Berkshire Residential + Webster Hughes, PhD | ThirtyCapital

PARSING OFFICE DISTRESS: PLANNING FOR THE NEXT GENERATION OF OFFICE SPACE

Dags Chen, Lincoln Janes, CFA | Barings Real Estat

MODEL STATES: USING ECONOMIC STATE MODELS TO ASSESS THE US OFFICE OUTLOOK

Armel Traore Dit Nignan | Principal Real Estate

OUTWARD SHIFT: WILL THE LOGISTICS SECTOR CONTINUE TO OUTPERFORM?

Kerrie Shaw | AXA IM Alts

HARNESSING THE WIND: TECHNOLOGICAL CHANGE AND THE PROMISE AND PERIL OF AI FOR REAL ESTATE

Nikodem Szumilo | University College London + Chris Urwin | Real Global Advantage

MIND YOUR DATA: REAL ESTATE INVESTING, FROM THE POINT OF VIEW OF A DATA NERD

Ron Bekkerman, PhD

OPERATING EXPENSES RISING THE OTHER MAJOR COMPONENT OF NOI GETS MORE FOCUS

Stewart Rubin, Dakota Firenze | New York Life Real Estate Investors

IN MEMORIAM: JANICE STANTON

+ LATEST ISSUE

+ ALL ARTICLES

+ PAST ISSUES

+ LEADERSHIP

+ POLICIES

+ GUIDELINES

+ MEDIA KIT (PDF)

+ CONTACT

—

ABOUT THE AUTHORS

Sabrina Unger is Managing Director, Research and Strategy, and Britteni Lupe is Associate, Research and Strategy, for American Realty Advisors.

—

NOTES

1. National Association of Home Builders. “Cautious Optimism for Builders in February.” NAHB Press Releases. February 2023. www.nahb.org/news-and-economics/press-releases/2023/02/cautious-optimism-for-builders-in-february. Accessed January 30, 2024.

—