The 2021 AFIRE International Investor Survey offers a sense of calculated optimism for CRE investment in the year ahead.

COVID-19 is not over. New variants; second, third, and fourth waves; and the logistical challenges of vaccinating 7.8 billion people around the world means that “post-COVID” is likely a way off. As some US cities begin to approach herd immunity with vaccination programs, some parts of normal life are returning, but with travel restrictions and supply chains disrupted by months of COVID lockdowns, cross-border investing is difficult and certainly not “normal.”

And yet, institutional investors are remarkably optimistic. As AFIRE members responded to the 2021 International Investor Survey, the reported intent was to keep crossing borders and keep finding high quality investments. Reports of transaction activity so far this year indicate that investors are finding them.

In order to keep up the investment pace in difficult times, investors are changing their approach (click any of the charts below to view at a larger size):

In the past, large institutions focused on large office buildings in the best gateway cities. Although a major portion of those assets are and will remain in institutional hands, the appetite for more of the same is waning.

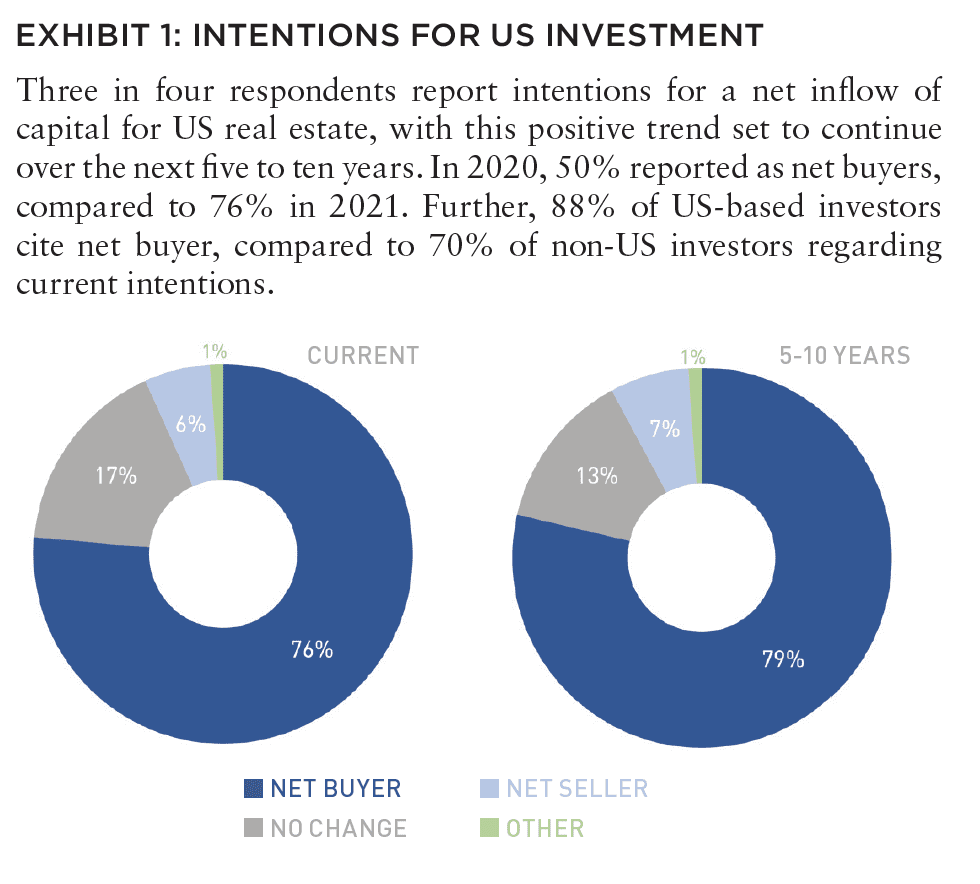

Institutional investors are remarkably optimistic. For example, 76% of AFIRE International Investor Survey [1] respondents declared they would be a net buyer of US real estate in 2021, compared to 50% before COVID. When asked about their outlook for five to ten years from now, 79% expected to be net buyers. In 2021, they have allocated roughly the same amount of capital they allocated in 2020 even though they were only able to invest half of what they allocated last year due to the pandemic. In the UK, 38% of investors plan to increase investment in US property markets over the next three to five years. When asked whether they will be net buyers or sellers of US real estate, 76% of global investors raised their hands as buyers. This is a marked departure from months before COVID when only 50% intended to be net buyers.

In past economic recoveries, investors took advantage of distressed assets and forced sales to acquired properties and loans at a significant discount. That has generally not been the case so far, and few expect it to be so in the future. This is interesting to consider as high levels of allocations are in place without the prospect of significant discounting.

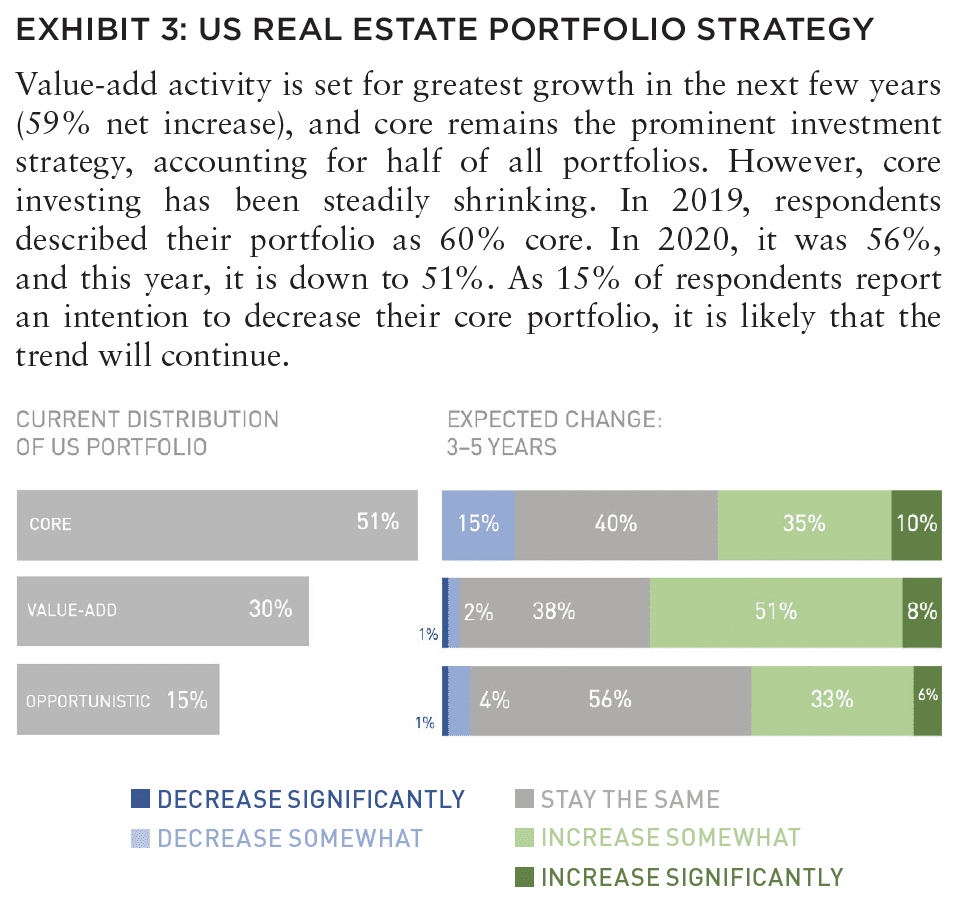

Investors are also shifting from a “core” strategy to more “value-add” and “opportunistic” investments. For decades, a majority of their property portfolios were in core stabilized assets in the top US cities, such as New York, Los Angeles, and San Francisco. In the last few years, core portfolios have steadily dropped on a percentage basis. In 2019, the respondents averaged 60% in core. In 2020, it was 56%, and this year it is 51%. Value-add and opportunistic portfolios have grown in kind, and it is not unreasonable to presume that we may see a continuation of this trend in the years to come.

Why are institutions expanding value-add and opportunistic investments? Long-term investors need higher yields than many core investments are able to produce right now, and they are willing to move up the risk curve to find it. Competition is fierce and most high-quality core assets are already owned by long-term institutional owners. It’s hard to buy what isn’t for sale. In a pervasive low-yield environment, core assets have climbed in price, to the point where sometimes the only way to buy one is to build one, and construction isn’t core (at least, not at first).

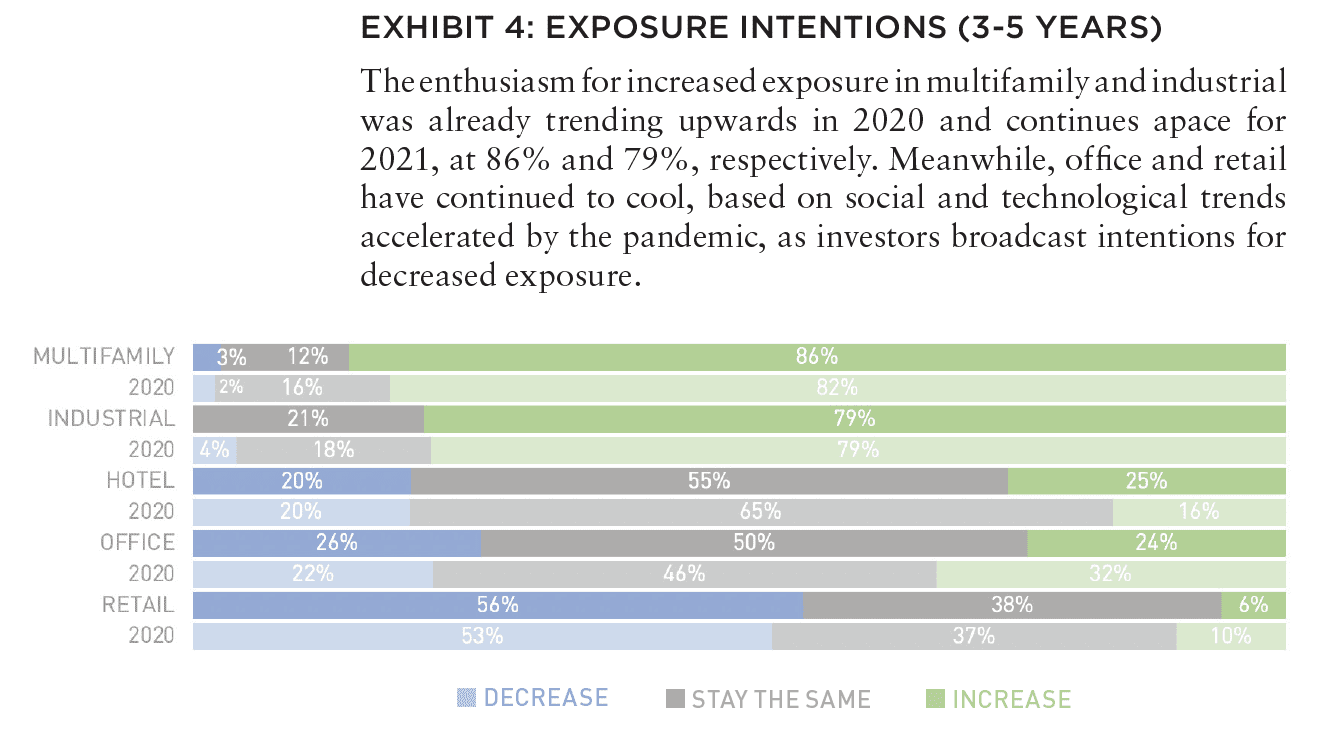

At the same time, institutions are shifting to other investment categories that don’t sit as squarely in the core category, including housing and industrial/logistics. The survey shows 86% of respondents plan to increase their investments in multifamily over the next three to five years. There is a lack of housing options in many cities and at most economic levels except for the very fortunate. According to the US Department of Housing and Urban Development, 580,466 people in the US are homeless [2], while those in the middle-class struggle to afford homes in major cities as well. A steady migration from northern and coastal cities to less expensive locations elsewhere in the US has increased during the pandemic. Collectively, these trends underscore a clear demand for more housing and institutional investors are paying attention.

Through the pandemic, online shopping globally grew at an average of 16.5% leading to US$3.914 trillion of sales predicted for 2021.[3] Only 6% of investors intend to expand their holdings in retail. But another asset class has benefited, as demand for data centers and distribution warehouses have, of course, followed: 79% of respondents plan to increase their exposure to industrial in that same time frame, compared to 24% who plan to expand their office portfolio. Office is certainly an institutional asset class and continues to be important for investors’ portfolios, but there is less enthusiasm to grow in this area in part due to the uncertainty of office demand and tenant requirements in the years to come.

Given the global slowdown of hospitality due to COVID, it is surprising to see that slightly more investors (25%) indicated they wanted to expand their hotel portfolios, compared to those who wanted to expand office. A predicted industry-wide restructuring of hotels has not materialized. Owners have been able to hold on through the lockdowns and many are already experiencing an uptick in bookings. A quarter of investors see a return to health in the months and years to come.

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS

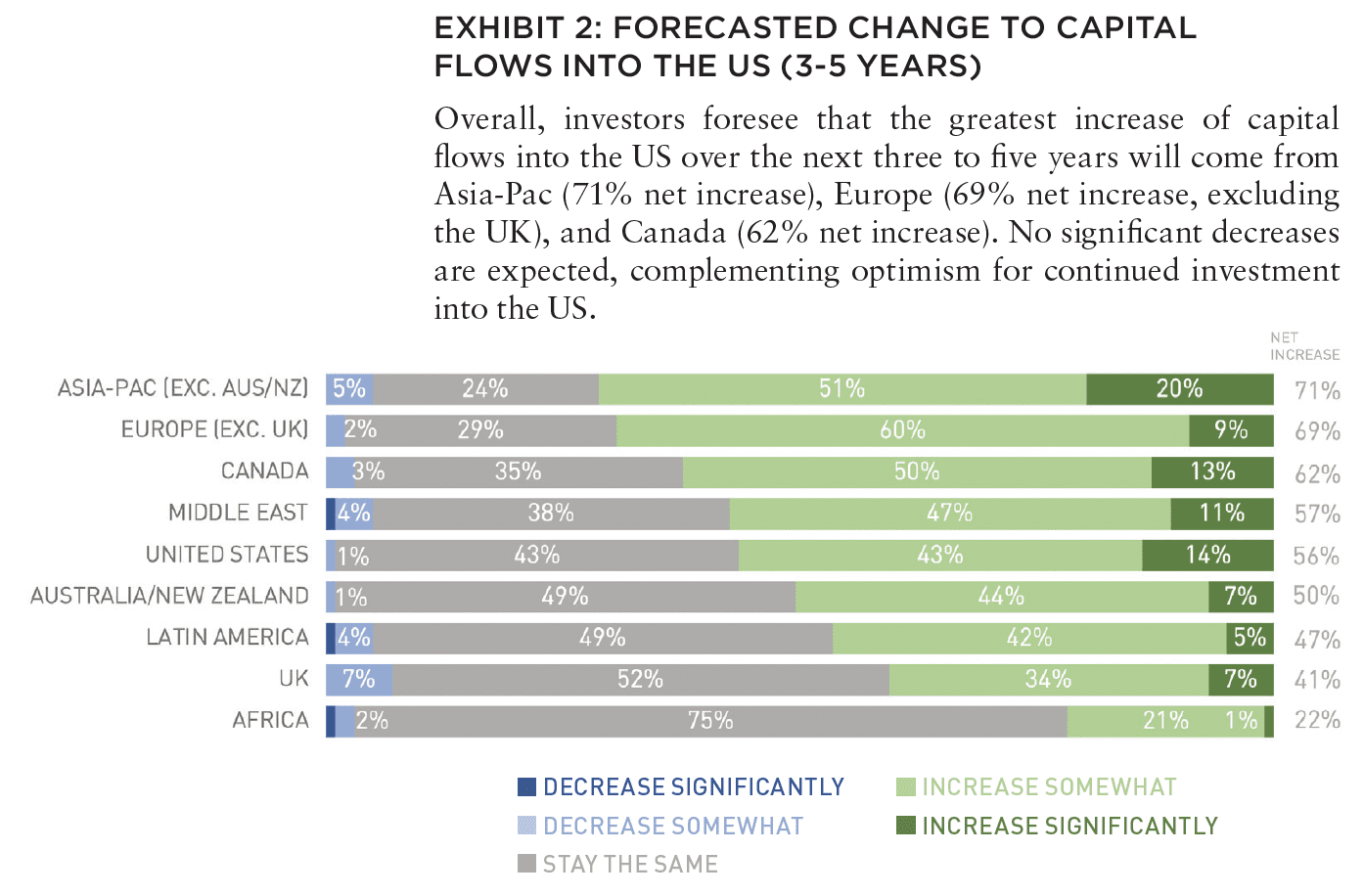

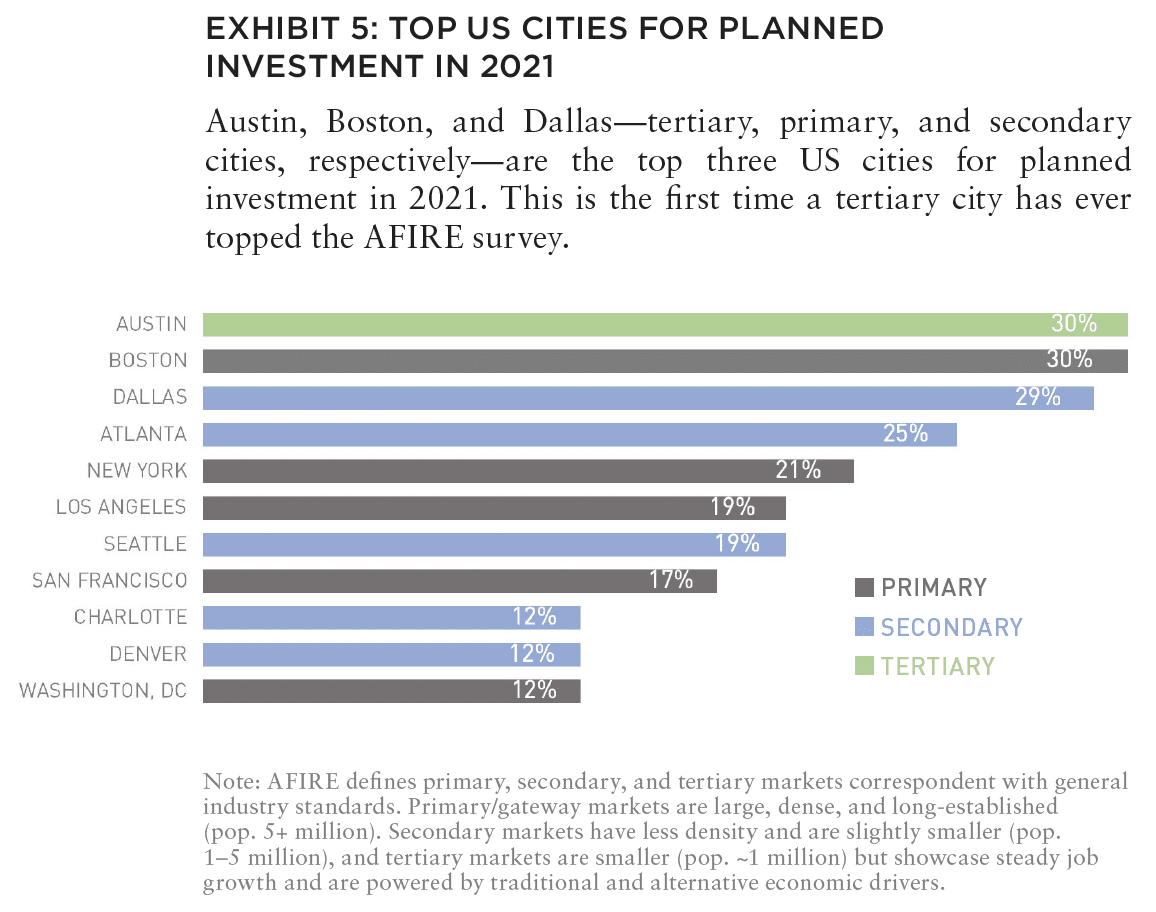

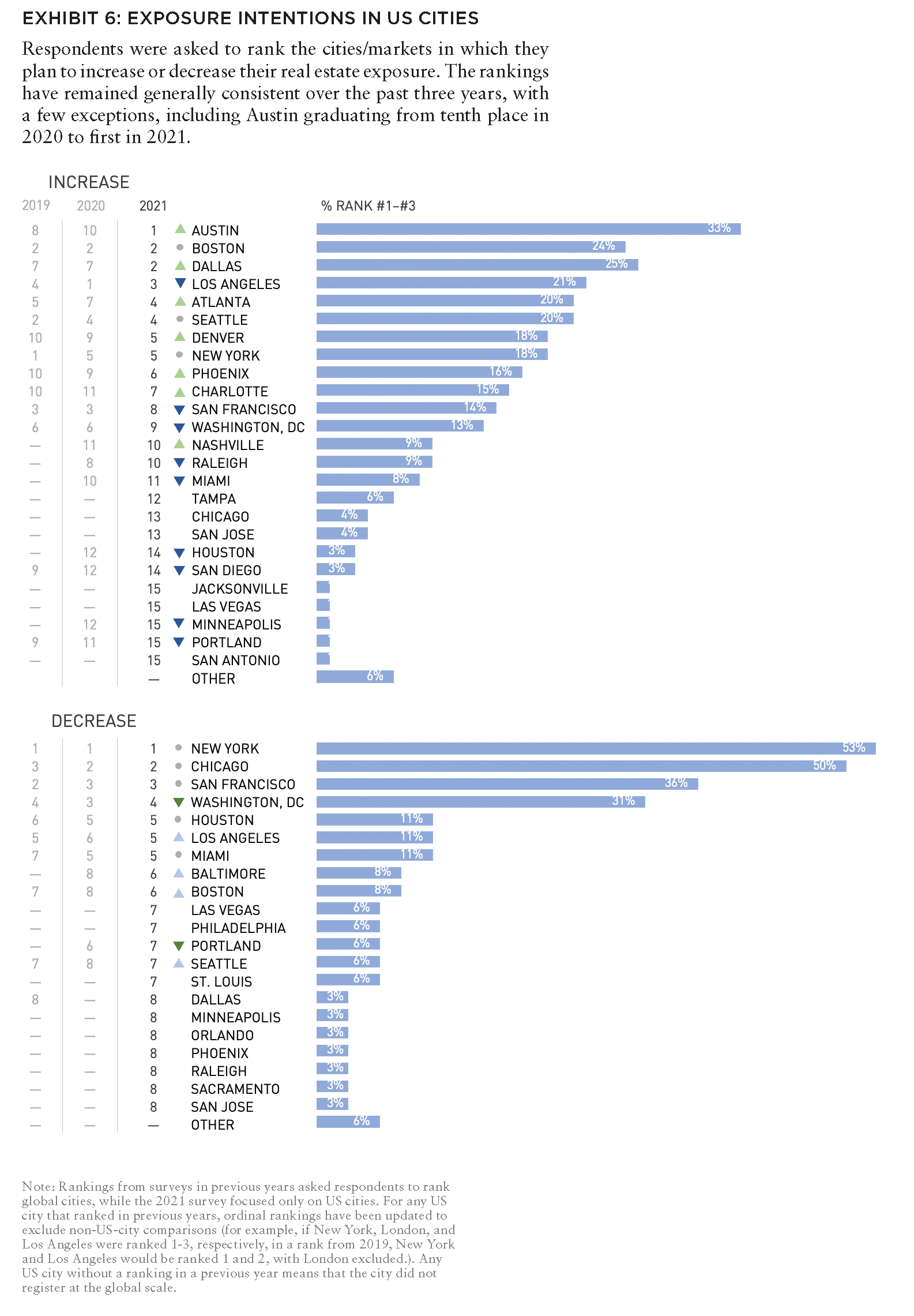

In addition to shifting priorities for property types, investors are changing their preferred cities and markets. In the 30 years that AFIRE has conducted its survey, only primary gateway cities have topped the list of US cities for future investments. Typically, cities such New York, Washington, DC, San Francisco, Los Angeles, Boston, and Chicago occupy the top spots. Given the size and focus of global institutional markets, this is to be expected. Except this year. Austin, Texas, is the leading US city for investments in 2021. As a smaller tertiary city with a top-level university, an expanding tech and biotech sector, a younger and well-educated population, and limited taxes, Austin is experiencing explosive growth. In a general environment of limited rent growth, Austin stands out from other comparable cities.

Following Austin is Boston, Massachusetts (rich in education, tech, bio-tech); Dallas, Texas (rich in education, tech, finance); and Atlanta, Georgia (rich in education, fintech, healthcare). They are very different cities, with interesting cultures, dialects, and cuisine, but to an investor they look remarkably similar: Powered by rapid growth and fueled by well-educated young people focused primarily on technology. Even though cities such as Austin might represent smaller markets with fewer acquisition opportunities, they have precisely what investors hope to find.

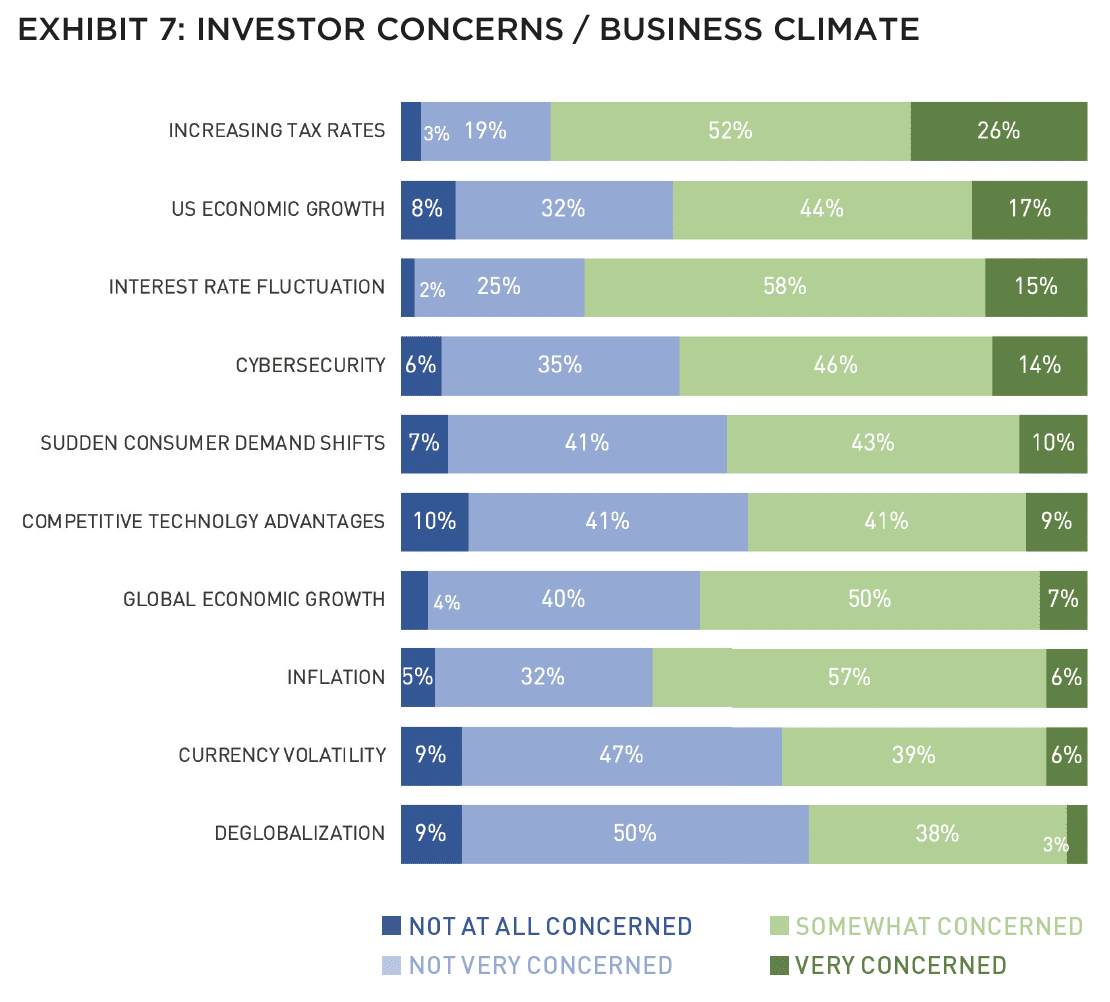

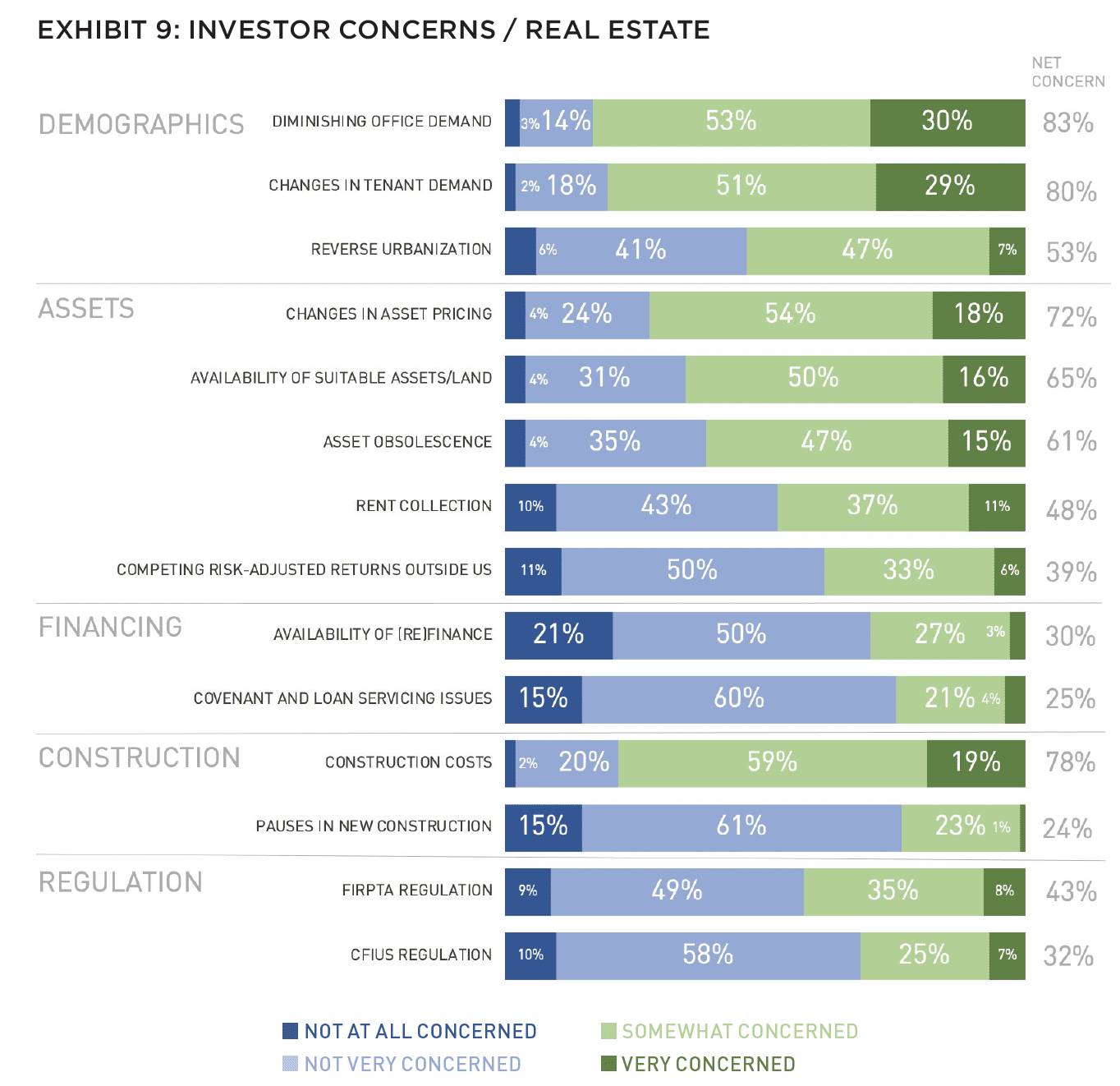

Institutional investors are optimistic, but they have serious concerns as well. Their perennial worries about increasing tax rates, economic growth, and interest rate increases may have more weight as governments around the world invest in economic and infrastructure recovery. Almost as high on their lists, and perhaps more illustrative of the times, respondents ranked cybersecurity as a concern higher than in any previous year of the survey, alongside disruptive technology and changes in consumer demand. All three of those issues have already impacted the world and will likely continue to do so.

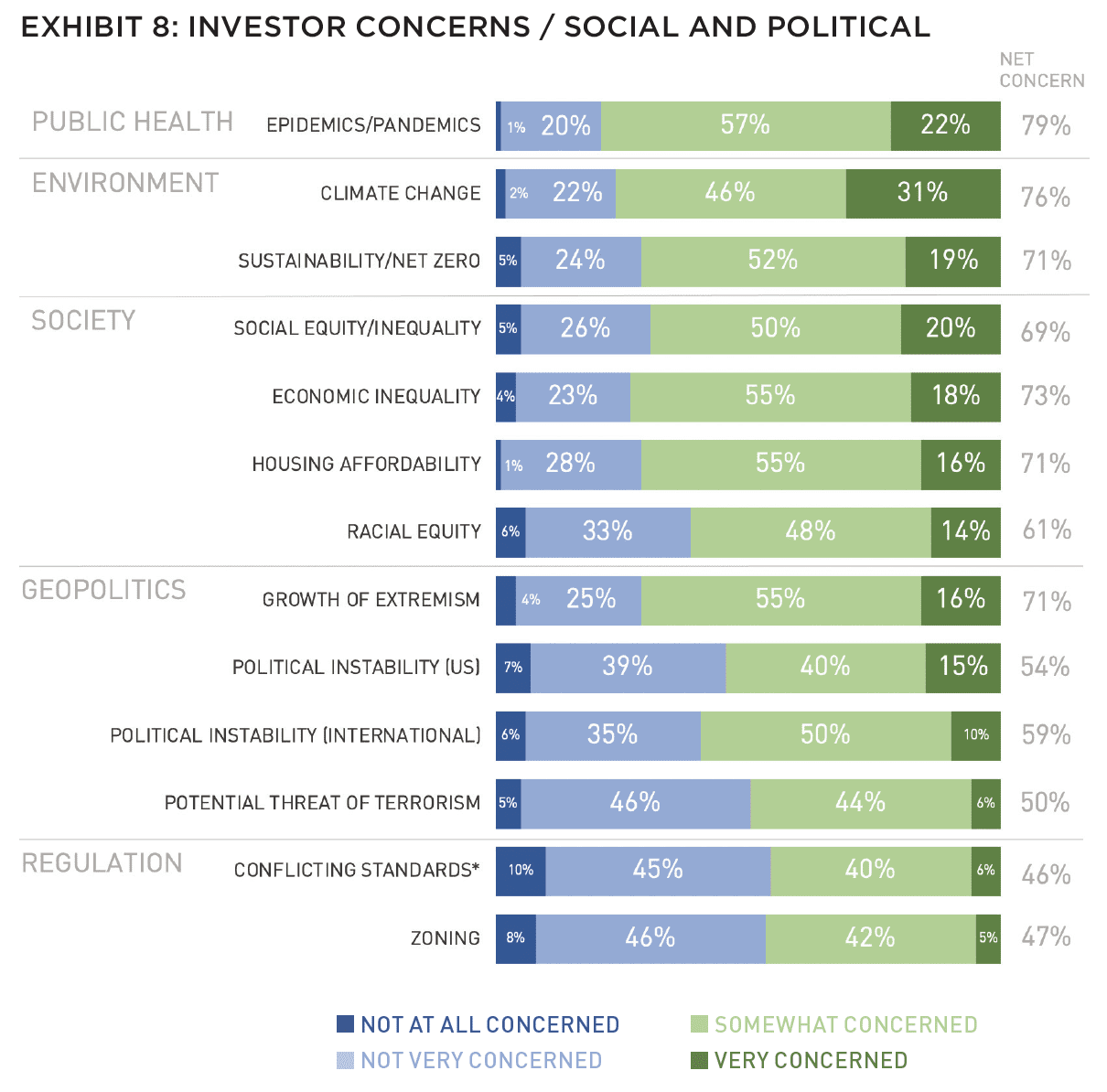

When asked about political and social concerns, respondents put pandemics at the top of the list, followed closely by social change, and sustainability, social inequality, economic inequality, housing affordability, and racial equity. Politics and regulations fell lower on their priority list of concerns. However, each of the concerns indicated by respondents have a tangible impact on tenants and users of real estate. What ails society, ails real estate. Especially as ESG dominates everyone’s agendas, leaders in this space are intentionally focused on strategies that support a healthier society.

The commitment to ESG is almost universal now: 93% of survey respondents said that ESG criteria are important for new investments, while 31% said that new investments are r equired to meet them. Most of their focus has been on the impact of their buildings on the environment over the last decade, but more focus has shifted to issues related to the social and governance principles of ESG trends.

Optimism about the future should not be confused with a yearning for the way things used to be. It requires an acceptance of the way things are and a courage to take new action. Institutional investors know where innovation is taking place, and even though real estate is not known for quick changes, they are managing to intelligently position themselves for the post COVID world. It won’t be easy, and it certainly won’t be the same, but it certainly will be interesting.

The 2021 AFIRE International Investor Survey was conducted in March 2021 and underwritten by Holland Partner Group. To learn more, visit afire.org/of-note/2021afiresurvey.

—

ABOUT THE AUTHOR

Gunnar Branson is the CEO of AFIRE and the publisher of Summit Journal.

—

NOTES

1. AFIRE’s International Investor Survey has been conducted for 30 years to gather the pulse of AFIRE members and the industry itself. There are 200 AFIRE members from 23 countries that collectively represent approximately US$3 trillion in assets under management. The focus of the membership and the survey is on cross-border investments into the US property markets. The survey was conducted in March of 2021 with over 100 respondents. Half of the respondents have under US$20 billion AUM and the other half have over US$20 billion AUM. Of the respondents, 64% represent institutions in Europe, the Middle East, Canada and Asia. The remainder are US based investors that work with global institutions.

2. “Homelessness Increasing Even Prior to COVID-19 Pandemic,” US Department of Housing and Urban Development (HUD) 2020 Annual Homeless Assessment Report Part 1 to Congress. hud.gov/press/press_releases_media_advisories/hud_no_21_041

3. Alexandra Samet, “Global e-commerce market report: e-commerce sales trends and growth statistics for 2021,” Insider Intelligence, December 2020; businessinsider.com/global-ecommerce-2020-report