This article appears in Summit Journal (Fall 2020) | Download PDF |

The shock provided by the global pandemic has roiled real estate markets around the world—which means that the quality and location of properties has never been more important.

As the world inches closer to its first year of dealing with the COVID-19 pandemic, it’s natural for the real estate industry to focus on the risks—whether to the global economy or to specific sectors like office or retail. But it’s also worth considering some of the opportunities that are coming into view as a result of the seismic shifts in real estate markets this year.

A LONG YEAR

It seems like years rather than months ago, but if we look back to early 2020, conditions in real estate markets, particularly for value-add deals, were healthy, and arguably even approaching frothy territory in some spots. Investor demand outweighed the supply of transactions, and core investors dipped into value-add territory seeking incremental returns.

That all changed in March as market participants grasped the extent and severity of the pandemic. Following that initial shock and the subsequent standstill in transaction volumes, activity has now returned with more transactions pricing by the day, but notably, the composition of investor demand looks much different now than it did before COVID.

Gone from value-add transactions are core and core+ investors, and competition for many of these assets has notably decreased—partially a result of less-available financing. Yields on such deals have also started to rise as investors have become more cautious on the execution of new developments or asset repositionings with the pandemic still looming in the background.

Conversely, prime—or core—assets have benefited from a flight to quality. Spurred in part by lower interest rates, yields on recent tier-1 transactions have been even tighter than pre-COVID levels in some sectors.

For value-add investors, such a bifurcation should be a welcome development. When too much capital was awash in the system and too many investors exhibited “risk-on” behavior, creating value through new developments or asset repositionings became more difficult. But with lower asset prices at the outset, there is now a more obvious gap to fill via such property improvements, especially when older assets in good locations can be repositioned to become core properties.

The question for investors to consider is where and how they can deploy capital, not only to benefit from potentially more attractive pricing dynamics, but also to capitalize on the long-term structural trends that will drive tenant behavior and thus demand for real estate assets in years ahead.

A GROWING OPPORTUNITY SET IN EUROPE

As we look forward, it’s clear that different trends will drive performance in different markets. In Europe, there are opportunities in less efficient parts of the market. For instance, given the region’s historically less-developed institutional capital base, many real estate assets remain in the hands of private companies or individuals. With the advent of the global pandemic, many of these property owners are now looking at options to monetize assets in an effort to redeploy capital into their core businesses. For investors, this trend is likely to help unlock a new stock of potential opportunities, including in the logistics sector, where private property owners are increasingly considering structured sale and leaseback transactions.

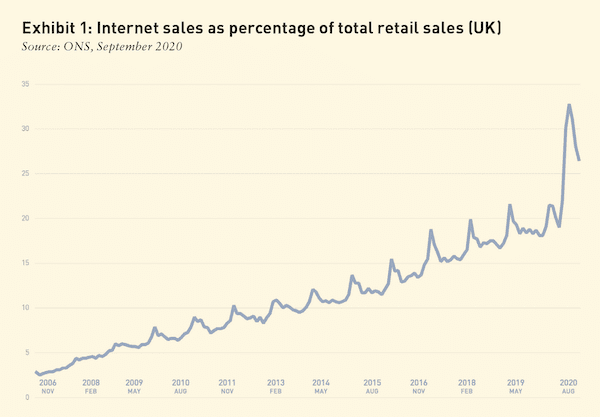

The pandemic has also accelerated several structural growth trends already in place. The most glaring of these may be the step change in e-commerce. Already on a long march higher, e-commerce penetration spiked across all major European markets during the pandemic. This included less-penetrated markets, such as Italy, where e-commerce sales is expected to grow by 26% year-over-year in 2020, [1] and more-saturated markets, such as the UK, where e-commerce sales as a percentage of total retail sales jumped from 20% to 33% (before giving up some of that gain).

While it remains uncertain exactly how much of these gains will stick, it does seem clear that COVID-19 has effectively accelerated e-commerce growth by multiple years depending on the specific geography. An increase in the on-shoring of manufacturing is also supporting the need for logistics space, especially in light of BREXIT. That means that logistics assets and last-mile delivery infrastructure will be in even heavier demand in the years ahead—and this is playing out in real-time as the pricing of such assets continues to be firm with some signs of cap rate compression.

SOCIAL SUSTAINABILITY

Of course, the pandemic’s lasting legacy will be much greater than a few more Amazon packages on our front doorsteps. A massive reassessment is underway in how we live, work and play. After the largely successful work-from-home experiment, office workers across the world are thinking twice about two-hour commute times. Such reassessments are likely to result in at least some lasting behavioral changes, with impacts—both positive and negative—for real estate investors in the years ahead.

Many smaller European cities are already well-positioned for this shift toward greater “quality of life,” but even the continent’s largest cities, such as Paris, are considering how they can offer a “city in 15 minutes” or in other words, everything a resident would need to live, work and play within just a short distance.

With government-led public health policies, at least in the short-term, actively advising employees to work from home if they can, an emphasis on nearby schools, retail, and healthcare is growing. And while we fully expect city centers will return to their vibrant pre-pandemic selves, one of the lasting effects of COVID-19 may prove to be a more empowered employee, focused on shorter commutes and more flexible working arrangements. This may prove to be a supportive trend for smaller cities or amenity-rich nodes outside the city center.

It’s not just among the working population where more attention is being paid to “social sustainability.” Student housing, for instance, is likely to change in the years ahead. No longer will commoditized, single-use properties be acceptable, but rather, property owners are more likely to see demand for a greater integration of leisure, restaurants, and even office and hotel space.

The same is true for senior living. Future demand is likely to be less for single-use senior living facilities and more for mixed-use properties that provide quick and easy access to healthcare and retail, integrated into a wider community of all ages.

These trends will inevitably offer a wide variety of development opportunities in the coming decade for real estate investors, including both ground-up construction as well as creative asset repositionings.

IN THE US, SKILLED WORKFORCE CLUSTERS WILL DRIVE OPPORTUNITY

In the US, similar trends are beginning to play out as the workforce reassesses what the future should look like. Location will remain a critical factor in the office sector, but employers may be focused less on “face time” and more on creating the conditions for maintaining and protecting an important corporate culture, as well as providing an environment that facilitates collaborative innovation.

For instance, in industries focused on technology or media content, we anticipate that leading companies will still want to bring skilled employees together to foster communication and innovation, and that maintaining a physical presence will be a critical part of this strategy.

One of the key questions for employers to consider is where this skilled workforce—or a creative class—will want to live. Surely, skilled workers will want to optimize for the best live-work-play arrangements, and as such, we will likely see more clustering of talent. Smaller cities such Austin, Nashville, Portland, and others look set to benefit, in part due to lower square-foot costs than New York City, Boston, or San Francisco. Suburban areas offering urbanized “nodes,” such as Reston, Virginia, or Raleigh, North Carolina may also thrive as they offer both a high quality of life and access to talent in specific sectors such as technology and life sciences.

For real estate investors, this means that properties must be created—or repositioned—in exactly the right locations where these skilled workers want to be, but also to provide exactly the right type of space.

CREATIVELY REPOSITIONING SPACE FOR OPTIMAL USE

It’s not just in the office sector where quality—or delivering the “right” asset—will be paramount going forward. Even in the industrial space, location demands for last-mile delivery will create significant pricing and rent differentials within the sector. For instance, while industrial space in large cities such as New York may be less economical on its face than owning a facility in central New Jersey, rising consumer expectations for delivery times means that proximity is at a premium. In some dense urban areas, that premium may justify development of multi-level industrial facilities to meet demand.

Critically, this increasingly sophisticated demand is likely to drive higher rents for optimized properties across all sectors. Office tenants may pay 100% more in rent for a building that provides an innovative environment to attract and retain skilled workers, versus a nearby building offering commodity space. This economic disparity will create real value for those who can figure out how to redevelop, reposition, and reinvent assets to cater to the demand requirements that were already being driven by innovative users before COVID and will likely become even more important post-COVID.

LOCATION AND QUALITY ARE PARAMOUNT; COMMODITIZED REAL ESTATE IS ON THE DECLINE

It’s clear that real estate managers will need to deliver the “right” assets in the “right” locations to be successful in the years ahead. COVID-19 has, in many cases, changed the definition of “right” in both instances, and the premium for those locations and assets that align with tenants’ increasingly sophisticated needs will likely widen going forward. For real estate investors seeking value-add returns, near-term weakness in the investment markets and evolving occupier preferences will create attractive opportunities to manufacture high quality, durable “core” income streams through repositioning and redevelopment of assets that meet those needs.

—

ABOUT THE AUTHOR

Valeria Falcone is a Portfolio Manager for Barings Real Estate‘s equity team and serves as the firm’s Italy country head. Joe Gorin is the head of portfolio management and value-add investing for Barings’ US real estate equity team.

NOTES

1. B2c Commerce Observatory, Politecnico di Milan, July 2020.

—