While continuation vehicles in real estate were once viewed as a signal of delay or failure, market sentiment is rapidly changing.

Over the past few years and with increasing frequency, real estate investment managers and their investors have been exploring ways to recapitalize opportunistic or value-add investments with longer-term (and often lower cost) capital.

While continuation vehicles were once viewed in a negative light, due to the potential conflicts between GP and LP interests, or to the tendency for such vehicles to be utilized only when there had been a failure or delay in accomplishing a fund’s objectives, market sentiment is rapidly changing. Blackstone’s nearly US$15 billion recapitalization of BioMed Realty at the end of 2020 took what might have been a taboo conversation with an LP and brought it to the mainstream, and their announced €21 billion recapitalization of Mileway just sixteen months later established this type of transaction as a mainstay liquidity strategy for the private equity giant.

Blackstone is by no means alone. In a January 2022 update, Landmark Partners noted that GP-led transactions involving the recapitalization of funds and property portfolios reached US$7 billion of net asset value in 2021, representing a 25% increase year-over-year and a 38% annual growth rate over the last five years.1 Anecdotally, the authors have also seen a similar increase in interest for these types of transactions among both clients and institutional LPs.

CONTINUATION FUNDS 2.0

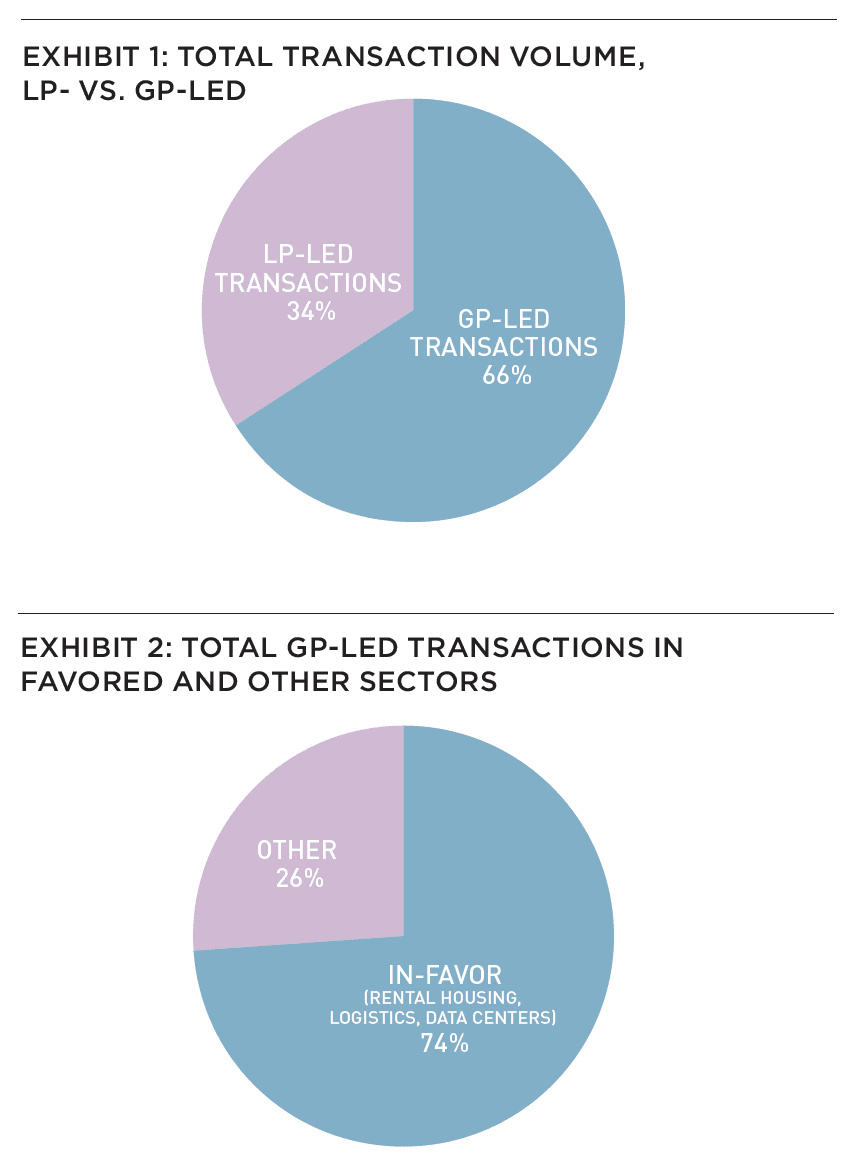

Traditionally, secondary trades have been driven primarily by end-of-life fund situations or LPs otherwise seeking liquidity. In those cases, the buyer is typically seeking higher returns for providing such liquidity. More recently, however, most secondary trades have been led by the GP (Exhibit 1), and in 2021, 74% of these trades comprised “in-favor” sectors such as rental housing, logistics, and data centers (Exhibit 2).2

Rather than end-of-life scenarios, the new iteration of recapitalization transactions typically (1) provide an early liquidity event that demonstrates strong performance for the fund and (2) provide the continuing investors with a high-quality portfolio, sometimes with potential future value creation opportunities that could not be executed in the prior fund due to an expired investment period. Increasingly, these continuation funds may serve as the formation transaction for an open-end fund, where managers can raise additional capital to make new investments over time.

As a benefit for managers, a continuation fund represents a way for the manager to recognize a capital event (and therefore earn a promote) while retaining the asset base on a go-forward basis. These transactions can also unlock tremendous enterprise value, as we have seen some of the highest EBITDA multiples for fees on perpetual capital. In addition, maintaining a larger portfolio can generate better proprietary information and increased relevancy to potential tenants—benefits which should also translate to better investor returns.

It follows that institutions should be more interested in finding ways to stay invested rather than have capital returned to them via asset sales. This is particularly true for certain sectors experiencing long-term structural changes, such as data centers or life science real estate, where systemic undersupply is creating not only a strong fundamental outlook, but a limited number of investable opportunities. Indeed, many investors have already been pursuing “built-to-core/long-term hold” strategies for similar reasons, so why not look to the assets already held in their private closed-end funds?

INVESTOR BENEFITS

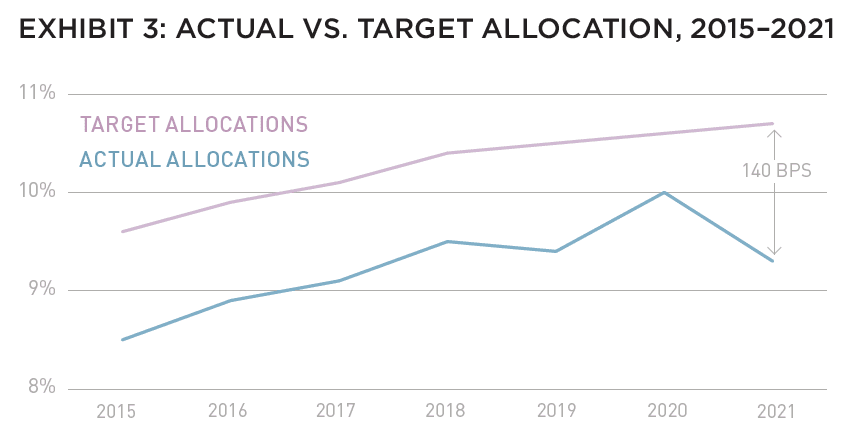

The benefits for the fund’s existing investors may be slightly less apparent but can be similarly powerful. At a high level, institutions on average remain significantly below their target allocation to real estate. According to Hodes Weill’s most recent Institutional Real Estate Allocations Monitor, conducted in partnership with Cornell University’s Baker Program in Real Estate, target allocations to real estate are at 10.7%, but actual allocations are only at 9.3%; that 140 BPS spread is the largest since we began conducting the survey nearly a decade ago.3

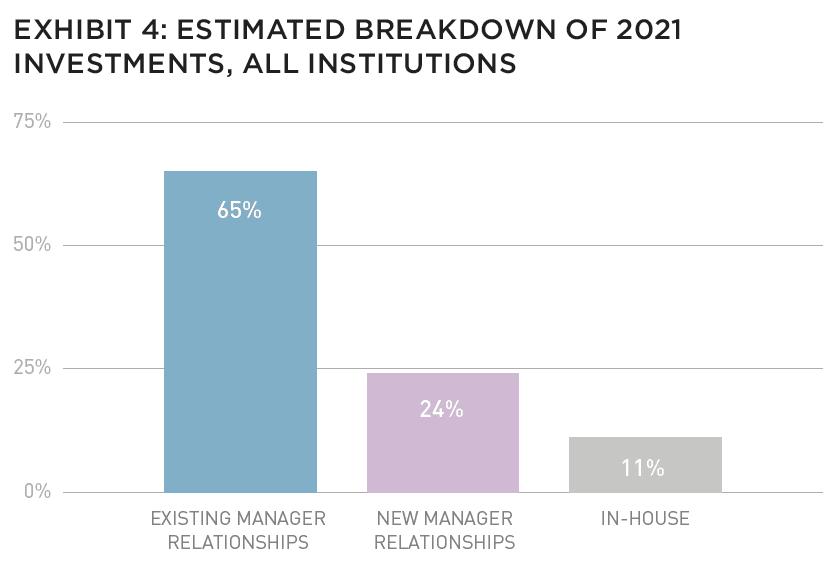

Another macro trend at play is the preference among institutions to do “more with fewer.” In 2021, 65% of investments were expected to be allocated to managers with which the institution had a pre-existing relationship. As investors expand their relationships with their current roster of managers, they stand to benefit from reduced frictional costs (e.g., diligence, legal, etc.) and streamlined portfolio management of their investments. When contemplating “doing more” with a sector specialist, expanding across various risk strategies makes sense.

Putting aside allocation decisions and preferences, continuation funds also offer certain benefits with respect to the underlying real estate. If an investor were to choose the best manager for its core real estate holdings, it would likely be the same group who initially developed or otherwise improved the asset. For investors seeking core or core-plus exposure, a fund recapitalization can provide access to a diversified portfolio of considerable scale while saving on the transaction costs of acquiring new assets. Investors may also capture certain tax benefits of recapitalizing limited partner interests not available when trading real estate.

POTENTIAL CONFLICTS

With all their potential benefits, continuation funds also pose obvious challenges to investors. With the manager on both sides of the table for a recapitalization transaction, investors are right to approach these opportunities with a certain amount of skepticism. As Thomas Albright, a private equity investment manager for the Teacher Retirement System of Texas puts it, “Our model historically has been built on alignment of incentives, and GP-led vehicles, continuation vehicles, break that model a little bit.”4 In addition, the option put to the investor of whether to cash out or roll its interest is more decision making than an LP might be accustomed to (and often in a tighter timeline than an LP typically operates).

Reflecting the sharp increase in activity for these GP-led recapitalizations and the complicated nature of these transactions, the SEC recently proposed new rules for adviser-led secondaries, which they defined as any transaction initiated by an adviser or manager that offers investors of a private fund the choice to either sell their interest in the private fund or convert their interest into another vehicle advised by the same manager. The proposed rules would result in increased reporting requirements as well as new procedures in the event of a manager-led, secondary transaction. Specifically, a registered private fund advisor would be required to provide investors a fairness opinion from an independent opinion provider, which the SEC believes provides “an important check against an adviser’s conflicts of interest in structuring and leading a transaction from which it may stand to profit at the expense of private fund investors.”5

Regardless of the adoption of these proposed rules, the industry, via investor demand, has shifted towards more rigorous processes for these transactions. Using the recent Mileway transaction as an example, existing investors were provided with two fairness opinions (one with respect to the consideration to be received and the other to the real estate value) as well as a “go shop” process run by Blackstone. Indeed, LPs expect their managers to be transparent about the options, benefits, and costs associated with continuation vehicles as well as the process being run. Managers should communicate their intentions as early as possible to allow time for LPs ample time to evaluate the opportunity, particularly in light of the very different underwriting process of a portfolio of assets compared with that of a blind pool fund, where the LP spends more time on the manager’s strategy, track record, and investment process.

NEXT STEPS

As continuation funds continue to proliferate in the market, we expect increased institutionalization and uniformity of the terms and processes for these types of transactions. Investors should not be surprised to see fund documents with language that specifies upfront how a recapitulation or continuation fund might take place.

While continuation vehicles were once viewed in a negative light—a tool to be used for hard-to-sell assets or funds at the end of their lives—they are now growing increasingly popular and are often stocked with the best assets from promising sectors. And with continued investor under-allocation to real estate, we don’t see the trend slowing anytime soon, despite the complexities.

—

ABOUT THE AUTHORS

Max LaVictoire is a Principal and Ashley Anderson is an Associate for Hodes Weill & Associates, a global real estate and real assets advisory fi rm focused on the investment and funds management industry.

—

NOTES

1. Ares, “Landmark Partners, an Ares company, Provides Update on Real Estate Secondary Market Transaction Volume,” news release, January 25, 2022, https://www.ares.com/sites/default/files/2022-01/Landmark_Partners_2022_Transaction_Volume_Release_vF.pdf, accessed April 29, 2022.

2. “2021 Institutional Real Estate Allocations Monitor,” Hodes Weill & Associates, updated November 9, 2021, hodesweill.com/single-post/2021-institutional-real-estate-allocations-monitor, accessed April 29, 2022.

3. Preeti Singh, “Investors See Both Promise and Risk in Continuation Funds,” Wall Street Journal, updated January 20, 2022, wsj.com/articles/investors-see-both-promise-and-risk-in-continuation-funds-11642680002, accessed April 29, 2022.

4. Gary Gensler, “Statement on Private Fund Advisers Proposal,” US Securities and Exchange Commission, updated February 9, 2022, sec.gov/news/statement/gensler-statement-private-fund-advisers-proposal-020922, accessed April 29, 2022.

EXPLORE THE FULL ISSUE (SPRING 2022)

MARCHING BACKWARDS INTO THE FUTURE

The new 2022 AFIRE International Investor Survey Report reveals future institutional investment trends as the pandemic transformed how we live, work, and play.

Gunnar Branson and Benjamin van Loon | AFIRE

CITIES THAT WORK

What is it that makes London, Stockholm, Berlin, Amsterdam, and Paris the top European cities for office investment? And what could this mean for other global cities?

Dr. Megan Walters | Allianz Real Estate

SURVEY SURFEIT

Be careful about advice you hear from surveys— it will not always play out as expected.

Jim Costello | MSCI Real Estate

NEW WORKING AGE

Outside of WWI and II, the US working age population has never declined. As of 2021, that statement is no longer true.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

SELECTIVE FRAMEWORK

Two years after offices closed due to the COVID pandemic, the debate over the longterm future of the office continues. What should office investment look like going forward?

Dags Chen, CFA; Ryan Ma, CFA; and Ryan LaRue | Barings Real Estate

GARDEN VIEW

US garden apartment investments are offering outsized return potential –but access remains a challenge.

Martha Peyton, PhD | Aegon Asset Management

SINGLE-FAMILY DEMAND

As an increasingly popular asset class for institutional investors, single-family rentals are supported by strong future demand drivers to propel sector outperformance.

Daniel Manware | Nuveen Real Estate

ESSENTIAL HOUSING

The US is in the middle of one of the biggest housing crises that the country has ever seen. It needs a more resilient approach to housing.

Todd Williams | Grubb Properties

LODGING TAKES THE LEAD

As a labor-intensive and service oriented asset class, hospitality is uniquely positioned to be a leader in advancing sustainability goals for investors.

Charlotte Kang, Geraldine Guichardo, Lori Mabardi, and Emily Chadwick | JLL

CARRY ON, CARRY OVER

While continuation vehicles were once viewed as a signal of delay or failure, market sentiment is rapidly changing.

Max LaVictoire and Ashley Anderson | Hodes Weill & Associates

RENEWING ETHICS

A note from AFIRE’s Ethics Chair on the need for maximizing ethics in an age where globalization is under threat.

El Rosenheim | Profimex