The rapid rise in consumer prices has rekindled the old debate about whether commercial real estate provides a long-term hedge against inflation. The answer is: it depends.

To begin answering this question using the latest data, this article explores the dynamics of two key performance indicators for privately owned institutional properties in the United States: market value index (MVI) and net operating income (NOI) relative to consumer price index (CPI) inflation.

To explore these dynamics, we first compare average year-over-year changes in MVI and NOI, relative to inflation, over the entire span of historical data available for both metrics (43 years from Q1 1979 through Q1 2022), as well as periods of above-average inflation (most of which took place in the 1980s).1 Second, we calculate elasticities of year-over-year changes in MVI and NOI, relative to inflation, while also accounting for economic growth as measured by changes in real gross domestic product (GDP).

From the perspective of real estate fundamentals, there are two main interrelated reasons for the stronger inflation-adjusted performance of apartments.

On the demand side, a relatively short leasing cycle of about a year, compared to over five years in other major property sectors, allows apartments to adjust to market changes more rapidly and efficiently. In addition, inflation and interest rates tend to move together, and higher borrowing costs for home purchases also support rental demand—a factor that is not at play in other sectors.

On the supply side, a shorter residential construction cycle allows developers to respond to changing market conditions quickly, keeping price levels close to equilibrium and reducing downside volatility in rents and property revenues. Real estate investors who are concerned about the potential scenario of persistent high inflation might consider this when evaluating their portfolio allocations to different property sectors.

At the same time, it should be recognized that within the apartment sector, various product segments and regional markets also vary in terms of their ability to counter inflation. We find, for example, that while garden-style apartments have been a better inflation hedge on the value side, and NOIs at high-rise apartments were more elastic relative to inflation. Furthermore, the inflation hedging potential of apartment values and NOI can vary even more widely geographically and therefore impact market allocations as part of portfolio construction.

In summary, while both apartment values and NOIs have indeed shown the ability to keep up with or even exceed inflation over long-term horizons (unlike other sectors), this does not apply equally to any property and location.

MVI AND ROI GROWTH RELATIVE TO INFLATION

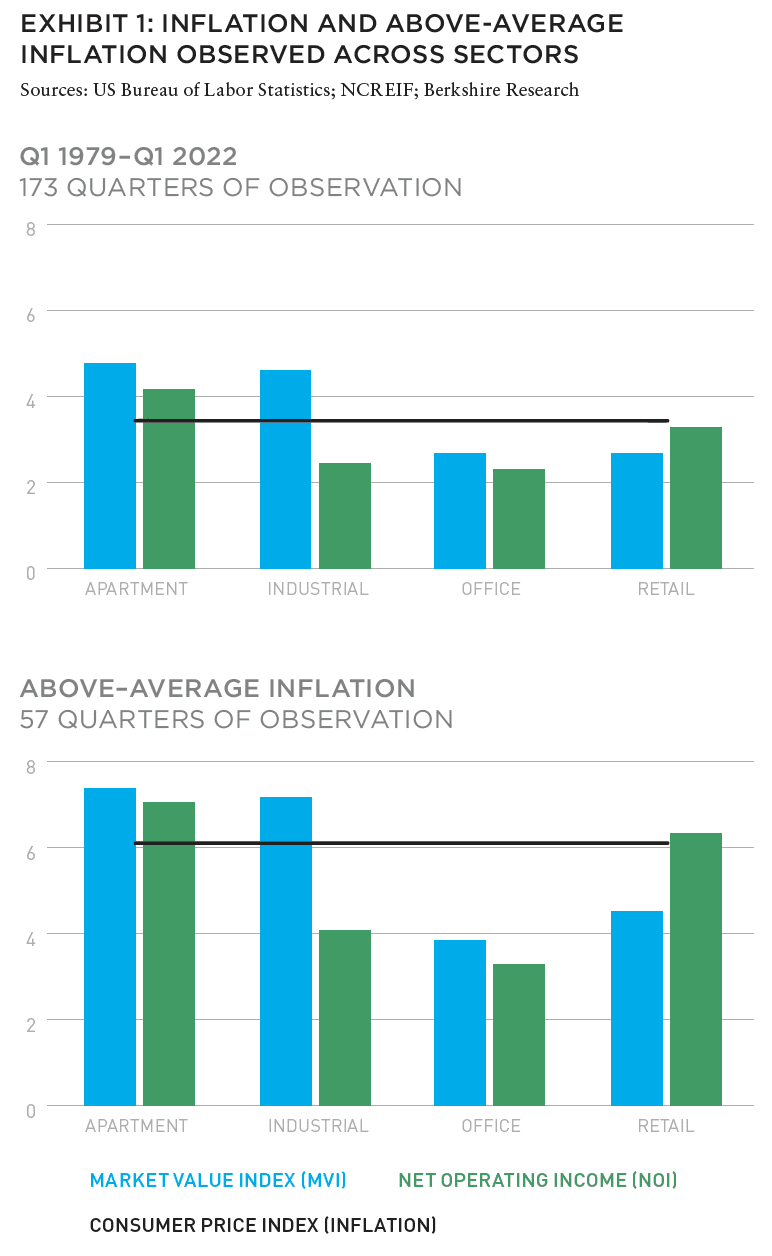

Looking at market value index (MVI), only the apartment and industrial sectors achieved appreciation that exceeded inflation both over the entire span of available history as well as periods of above-average inflation (Exhibit 1). On the NOI side, apartments were the only property sector to handily beat inflation both over the entire history as well as periods of above-average inflation. Retail NOI growth was second-best after apartments, and while it lagged inflation slightly over the entire period, it also exceeded it slightly during periods of above-average inflation.

In the case of apartments, the main driver of above-inflation MVI growth is clearly NOI growth. Meanwhile, results for industrial and retail are less obvious: industrial MVI grew above inflation while its NOI has not, but the opposite was true in the case of retail. One potential explanation for this is the impact of investor demand on both sectors, especially over the last few years.

MVI AND ROI GROWTH ELASTICITIES RELATIVE TO INFLATION

While it is helpful to know how MVI and NOI growth compared to inflation historically, answering the long-term hedge question also depends on how well that growth adjusts to the changing inflation. To answer that, we calculate growth elasticities relative to inflation using the entire span of historical data available for both metrics (Q1 1979 through Q1 2022).2

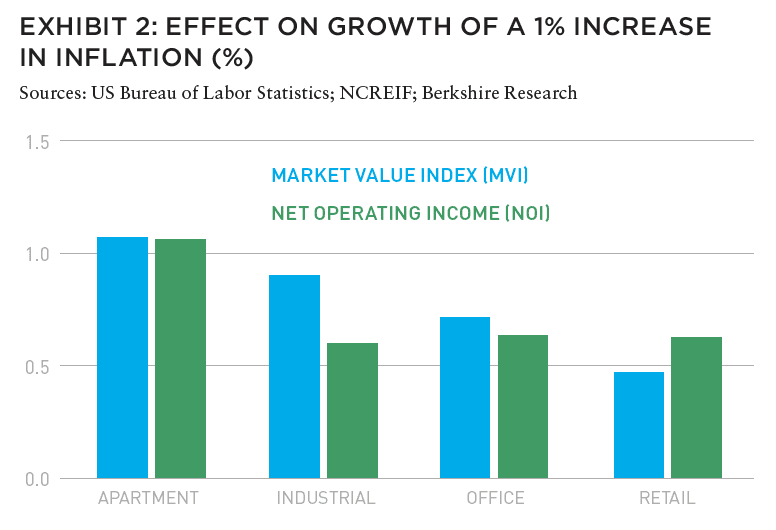

Exhibit 2 shows how much MVI and NOI growth change for every 1% increase in inflation. Once again, apartments are the only sector where both metrics have shown a propensity to basically keep up with rising inflation over time. Industrial is the second-best based on how well market values adjust to inflation (0.9% coefficient), followed by office (0.6% coefficient) while retail comes last (0.4% coefficient). At the same time, there are no substantial differences between industrial, office, and retail in terms of how their NOI growth has responded to inflation historically, with coefficients of about 0.6%.

The results suggest that multifamily is the only real estate sector that served as a real inflation hedge historically, followed by industrial (at least when it comes to market values). It is important to note, however, that different types of apartments do vary in terms of how their values and NOIs respond to inflation.

For example, available data only allow us to repeat the above analysis for garden-style and high-rise segments over the last 30 years rather than 43 years, thus missing the period of very high inflation observed in the early 1980s. This more limited analysis does show however that garden-style apartments have been a better inflation hedge on the value side, while high-rise properties were able to better keep up with inflation in terms of their NOI growth.

One potential explanation for this is that high-rise apartments tend to focus more on more affluent renters who are better able to absorb rent increases in a rising inflationary environment. At the same time, market values for garden apartments benefit more from stronger investor demand, even though their NOIs may not keep up with inflation as well as in the high-rise segment. We find similar variation across markets, with some being better inflation hedges on the value side while others adjusting better in terms of NOI.

It helps to know that apartment properties have a track record of being an inflation hedge, but the other key parameter, even more important than inflation itself, is broader economic and employment growth. Real estate can still deliver good investment returns when high inflation is accompanied by a strong economy and labor market. At the same time, when high inflation takes place during very weak or negative economic growth, and so-called “stagflation” sets in, no sector is immune to potentially stagnant or even declining property values and NOIs, after factoring for inflation. While this is not the baseline scenario for now, investors should carefully evaluate such downside risk as the global economy and capital markets deal with multiple uncertainties stemming from Russia’s war on Ukraine as well as the ongoing public health situation.

On the upside, the apartment sector is entering this uncertain period amid a record housing supply shortage that is likely to keep upward pressure on rents until inflationary pressures eventually subside. Rental housing (including apartments) has a unique distinction within real estate of being both a form of investment as well as providing “shelter,” a service that accounts for more than 30% of the broader inflation measurement. The increasing real estate portfolio allocations towards rental housing that was observed last year could be reflecting a growing recognition by investors of its relative advantages in the current environment.

This article takes a timely look at the age-old question of whether real estate is actually an effective hedge against inflation. While the conclusion is likely intuitive to most readers—that “it depends” and that multifamily is more effective than other property types—the exploration of why that’s the case, and if it can be expected to continue, raises some interesting points.

The author does a nice job making the case for investments in apartments being a proven inflation hedge, citing the ability to reset rents more frequently, and also notes an important correlation to economic and labor growth. However, for this link to continue, renters must be able to afford to pay higher asking rental rates and absorb future rent increases at a rate at least in line with inflation. Current rent-to-income ratios call this into question.

For context, US Census Bureau data and Moody’s Analytics estimates through December 2021, over the last decade, show that apartment rents have increased 71%, while incomes grew just 37%. Said another way, rental rates have increased nearly twice as much as income levels during the same period, driving rent-to-income ratios from 17% to 21%, nationally.

For apartments to continue to provide a hedge against inflation, we will need to see wage growth more in-line with inflation, which has not been the case historically.

Turning to the industrial sector, the author notes that appreciation has outpaced inflation, even as growth in NOI lagged, thereby creating a hedge. The appreciation in industrial is irrefutable, but the question to ask is what has driven that appreciation and whether the correlation to inflation will continue. The rise of e-commerce and the secular shift of distribution supply chains is another well-accepted explanation of the phenomenal escalation in industrial market values; one that is uncorrelated to inflation.

So, can we reasonably expect past correlations with inflation to continue similarly into the future? I am not so sure. In particular, inflation is being driven at least in part by exogenous factors not tied to the business cycle; the Fed is curbing growth with significant rate hikes; and apartment rent levels are already stretching incomes.

Amy Price

President, BentallGreenOak

Editorial Board Member, Summit Journal

EXPLORE THE LATEST ISSUE

CAPITAL MARKETS PULSE

Through the rest of this year, investors forecast challenges for global capital, but thoughtful investors are forging ahead.

Gunnar Branson and Benjamin van Loon | AFIRE

ON/OFF SWITCH

While the market rarely sends clear investing signals, current market conditions are replete with clues, but as timing for corrections is difficult, a move to risk-off strategies could be useful.

Joseph L. Pagliari | University of Chicago

MOBILE ZONING

Mobile information technology has upended US land use regulation, and the ramifications of this technological upheaval are finally coming into view.

Robert Seldin | Madison Highland Live Work Lofts

GET SMART

As buildings become increasingly technologized, especially after the pandemic, cyber-attacks can put entire properties at risk and require a firmwide security approach.

Noëlle Brisson and Michael Savoie | CyberReady, LLC

HEDGE TRIMMING

The rapid rise in consumer prices has rekindled the old debate about whether commercial real estate provides a long-term hedge against inflation (hint: look at multifamily).

Gleb Nechayev, CRE | Berkshire Residential Investments

THE NEW SCIENCE

While the real estate industry has long understood the need for data, it still struggles with connecting information to decision making. New strides in data science could change that.

Brian Biggs and Ashton Sein | Grosvenor

BRACE FOR IMPACT

The practice and expectations of investing across all industries is undergoing major upheaval and the key to stability will mean looking beyond profit for profit’s sake.

Michael Cooper and Richard Florida | Dream Unlimited Corporation

TRANSITION PLANS

Forecasts about the future of the office sector are often wildly conflicting, but the looming high tide of generational leadership transitions could change the script.

Sabrina Unger and Britteni Lupe | American Realty Advisors

WHAT DRIVES LOGISTICS?

The logistics sector was the winner of the pandemic recession—but is its rise built to last?

Hugues Braconnier and Dr. Megan Walters | Allianz Real Estate

RENEWED PURPOSE

From retail to office to abandoned factories and warehouses, owners of real estate are rethinking—and reinventing—the future of their investments.

John Thomas and Stacey Krumin | Squire Patton Boggs

DATABASICS

Data centers have become an increasingly institutionalized property class over the past several years, but finding success in the sector depends on talent and expertise.

Max Shepherd, Jannah Babasa, and Isabel Ruiz Halter | Sheffield Haworth

COOPERATIVE INVESTMENT

As insurance costs of residential and commercial spiral out of control, a 1400-year-old tradition is poised to offer long-term, sustainable growth for real estate investments.

Ishmam Ahmed | Georgetown University & AFIRE

DOMESTIC MIGRATION TRENDS

Dive into the report to understand if and how COVID impacted domestic migration patterns on a state, city, and zip code level.

Ethan Chernofsky | Placer.ai

UP FRONT

How does the Consumer Price Index account for the cost of housing?

David Wessel and Sophia Campbell | The Brookings Institution

—

ABOUT THE AUTHOR

Gleb Nechayev, CRE, is Head of Research and Chief Economist, Berkshire Residential Investments, a people-focused investment management company known for its vertically integrated organization and experience in US residential real estate.

—

NOTES

1. This material is for informational purposes only and is not intended to, and does not constitute financial advice, investment management services, an offer of financial products or to enter into any contract or investment agreement.

2. Our analysis follows the same approach as discussed in the article by Greg MacKinnon, “What Would Higher Inflation Mean for Real Estate?”, PREA Quarterly, Fall 2021..

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Aegon Asset Management is an active global investor that manages and advises on assets of $328 billion* for global pension plans, public funds, insurance companies, banks, wealth managers, family offices, and foundations. Aegon AM’s Real Assets platform focuses on delivering yield-oriented and total return solutions spanning the risk/return spectrum.

With an over 35-year history and $25 billion* in AUM/AUA, the Real Assets business is built on a cycle-tested platform, deep and broad market access, and long-term relationships.

Our real assets debt and equity strategies seek to deliver strong relative value and returns through a research-intensive process. The process encompasses thoughtful top-down research and intelligent bottom-up analysis deployed by an experienced multidisciplined team of over 110 investment professionals.*

Each capability is underpinned by dedicated, in-house support and service teams including applied research, engineering and environmental, valuation, accounting, client service, legal and risk management.

*As of June 30, 2022. The assets under management/advisement described herein incorporates the entities within Aegon Asset Management brand as well as the following affiliates: Aegon Asset Management Holding B.V., Aegon Asset Management Spain, and joint-venture participations in Aegon Industrial Fund Management Co. LTD, La Banque Postale Asset Management SA, and Pelargos Capital BV.