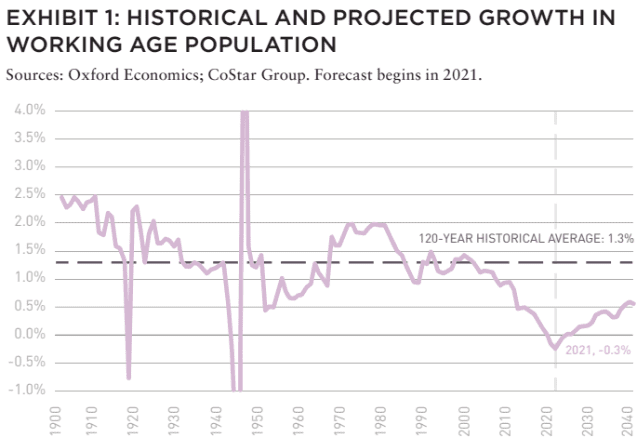

Except during two World Wars in the first half of the last century, when troops were deployed overseas, the US working age population has never declined.1 As of 2021, that statement is no longer true.

According to data recently released by the US Census Bureau, the total US population grew by only 0.1% between 2020 and 2021. Looking specifically at the working age population cohort (ages20 to 64),Exhibit 1shows the annual growth rate since in 1900.2 Over the past 120-year period, the working age population grew an average 1.3% per year. The annual growth rate in working age population has declined since 2000 and turned negative for the first time in 2019.

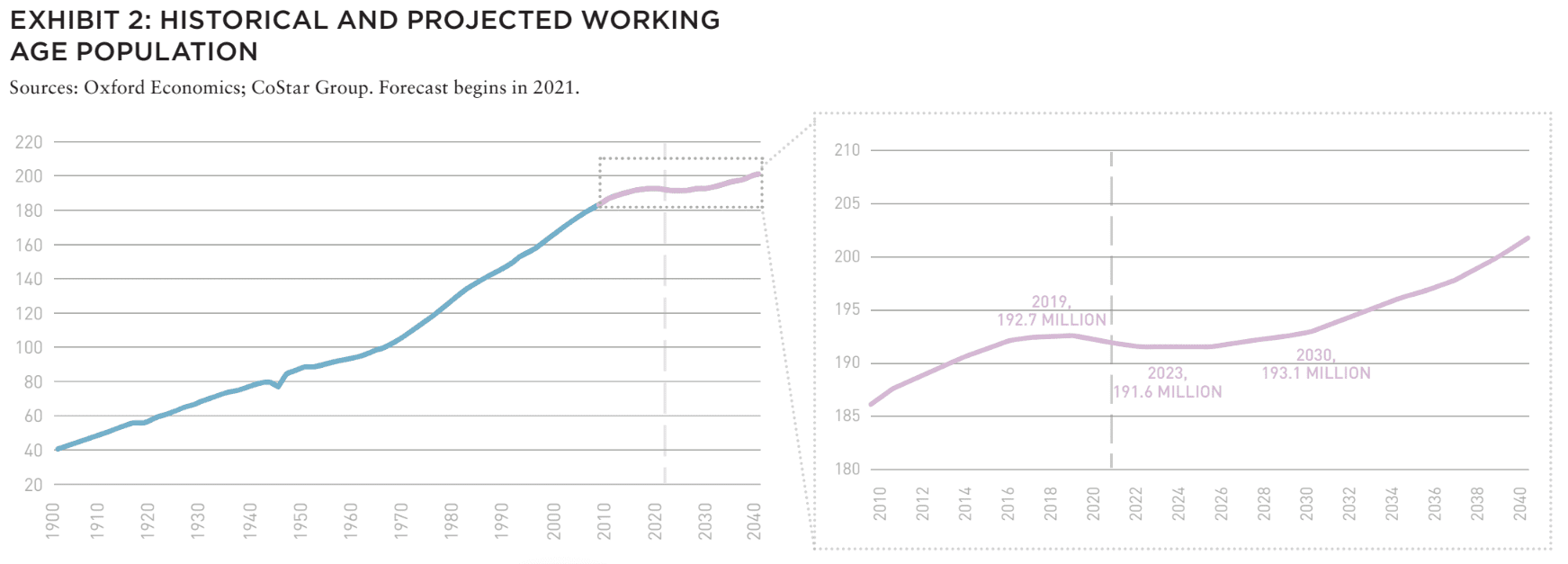

The working age population in the US peaked in 2019 at 192.7 million before starting its decline. This population is forecast to decline to 191.6 million by 2023 before resuming its ascent, and returning to its 2019 level by 2030, according to projections from Oxford Economics.

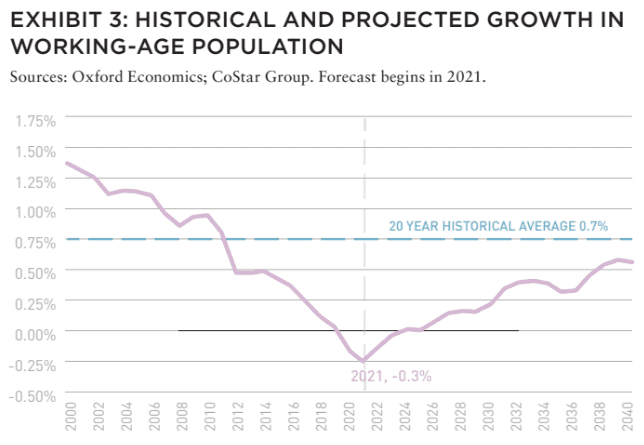

Not only has the working age population declined for the first time during a non-war time period, but its projected growth starting in 2023 is expected to be substantially lower over the next twenty years than it was during the previous two decades. Working age population growth has generally ranged from 1.0% and 1.5% in the seven years before the GFC, but then declined precipitously until turning negative in 2019. The growth rate was expected to bottom out at -0.3% in 2021 and then begin to recover thereafter. The twenty-year historical average of 0.7% is not expected to be regained over the next twenty years. In fact, growth in excess of 0.5% per annum is not expected to be achieved until 2037.

NATURAL POPULATION GROWTH CONTINUES TO DECLINE

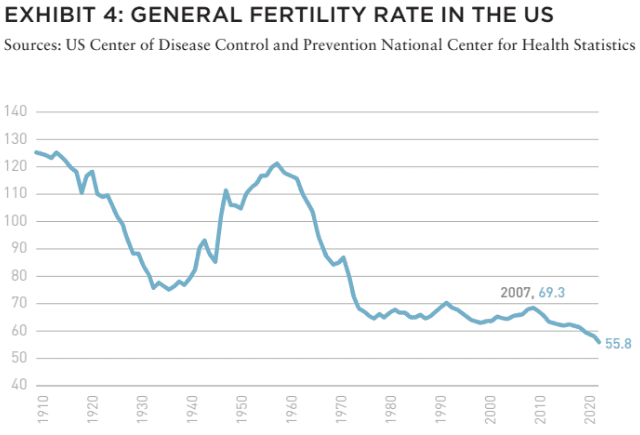

Contributing factors to forecasted stagnating growth in working age population include a decline in the fertility rate over the last few decades. After reaching a recent high of 69.3 births per 1,000 women in 2007, the fertility rate has steadily declined. In 2020 alone, the general fertility rate decreased to 55.8 from 58.3 in 2019—a reduction of 4.3%, the largest single-year decline since 1973.

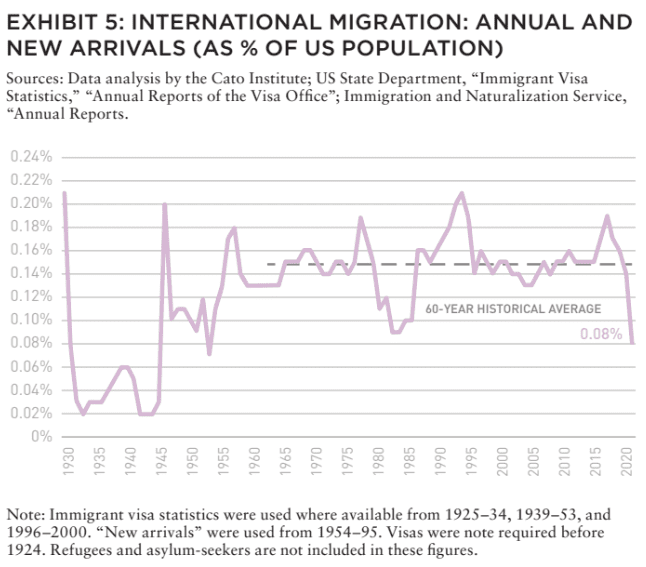

INTERNATIONAL IMMIGRATION OFFERS LITTLE SUPPORT

Another factor contributing to slower growth in the working age population is the reduction of legal international immigration into the US. Historically, new immigration arrivals have accounted for roughly 0.15% of the US population. In the years leading up to 2016, this number increased to a recent high of 0.19%, or about 618,000 new arrivals that year. Beginning in 2017, with less immigration-friendly policies under the Trump administration, and compounded by limitations due to COVID-19, this figure has declined precipitously in the past four years. In 2020, fewer than 264,000 new arrivals represents a 67-year low of 0.08% of the population.

RETIREMENTS ARE ON THE RISE

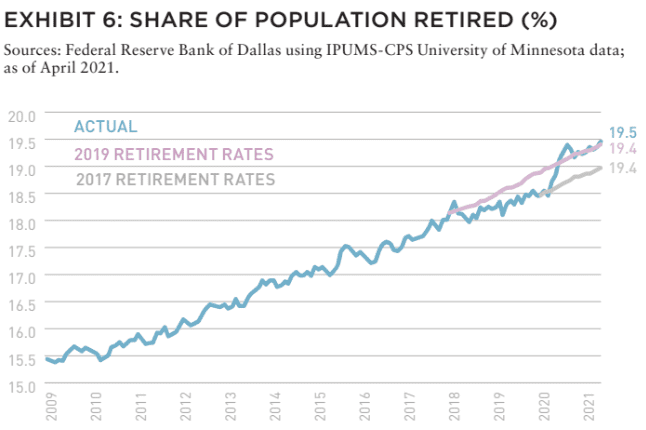

According to data from the Federal Reserve Bank of Dallas, 2.7 million more individuals reported being retired relative to pre-COVID levels.3 Assuming 2019 retirement rates, the Dallas Fed estimates that 1.2 million would have retired regardless of the pandemic. The additional 1.5 million retirements that currented during this period represent an increase of 125% over 2019 retirement rates.

However, the chart below shows how a strong labor market in2018 and 2019 likely prompted some older workers to delay retirement, “causing the share of the population in retirement to increase more slowly than the rate of aging would have implied,” according to the Dallas Fed.4 In the time since COVID began, the rate of retirement has returned to its 2017 trend.

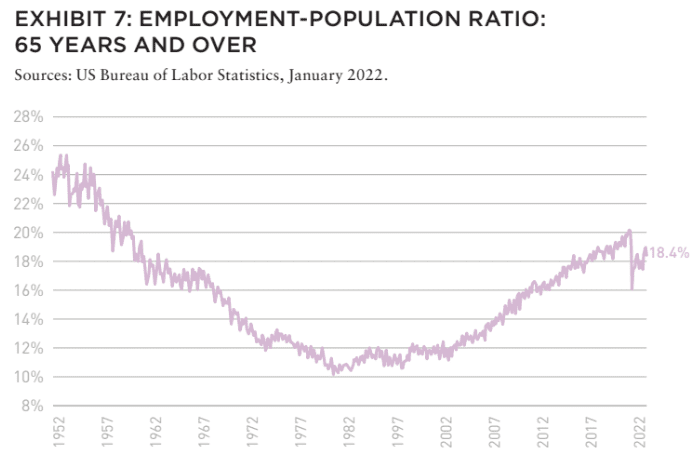

Nevertheless, even if the increased level of retirement seen during the pandemic does not represent a significant departure from the longer-term retirement trend, it still constitutes fewer workers in the labor market. As evidenced by the employment to population ratio for age 65+, this age cohort has experienced a 1.7% decline from its pre-COVID high of 20.1% to 18.4% as of January 2022. This reduction in employment-to-population ratio translates into roughly 570,000 fewer employed workers from this age cohort.

By historical context, the employment to population ratio for age65+ remains elevated. Prior to 2015, the last time this level was observed among older workers was in 1964 during the Johnson administration.5

LABOR MARKET

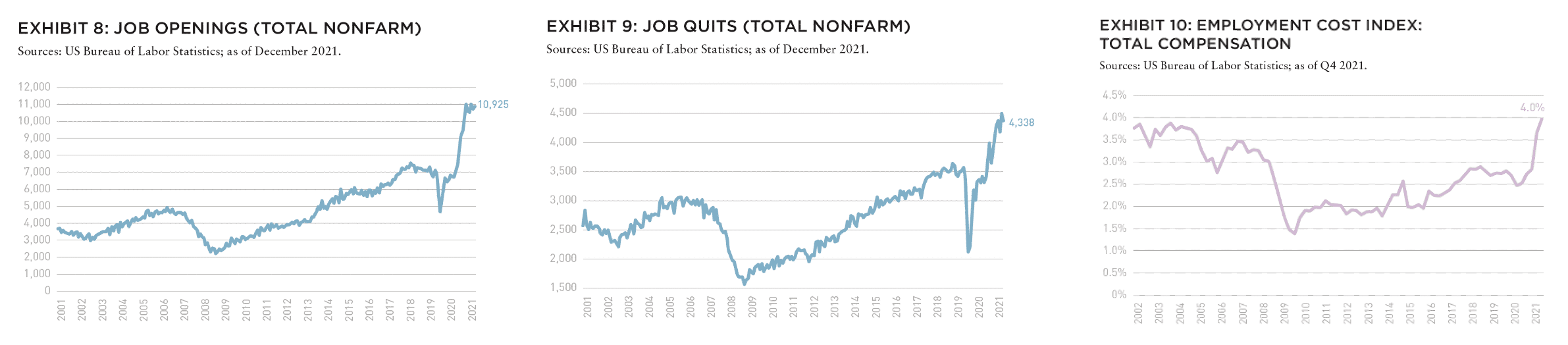

The impact of a declining working age population may be apparent in the historically high level of job openings along with historically high job quits rate, as detailed in Exhibits 8 and 9. As a result, wage pressure in the labor market has already been exhibited. The employment cost index increased 4.0% year-over-year in Q4 2021, the highest level in the history of the time series, and notably higher than the 2.7% average over the three years prior to COVID.6 In addition to offering higher wages, some employers may respond to labor shortages with incentives to keep older workers from retiring. Furthermore, in the face of higher labor costs, certain companies may accelerate plans to introduce further automation into their businesses.

DOMESTIC MIGRATION

Regional differences in the growth of working age population exist across the US Positive net domestic migration to regions like the Southeast, Southwest, and Intermountain West provide population growth tailwinds to those regions that may offset the headwinds listed above.7 Likewise, regions like the Pacific Coast, Northeast, and Midwest may experience declines in working age population worse than the national figures cited above.

Ultimately, the first decline of the US working age population since WWII has been exacerbated by declining international immigration and an increase in retirements. A declining fertility rate could also imply that future challenges remain, even as the impact of the declining working age population may already be impacting labor supply and wages. Companies may respond to worker shortages by providing incentives to keep workers and stave off retirements, or by increasing automation.

—

An attention-grabbing headline and insightful perspectives about an important first—but not one to be celebrated. Both slower growth and aging of the population in many countries have been on the radar for global investors, but the outright decline in the working age cohort in the US that the authors highlight might be new information to these investors. While the oft-used phrase “demographics is destiny” may overstate the importance, there is no denying that population dynamics are crucial to the health of the macroeconomy overall—and local real estate markets, in particular.

Looking under the hood to get into the details, the authors highlight the secular decline in fertility rates and more recent policy induced elephant in the room, that being the sharp drop in international immigration. The sheer number of immigrants not arriving in the US over the past five years represents a cumulative deficit of about two million people—adding diversity, youth, entrepreneurial drive—assuming the number of new arrivals at 0.15% of the US population, the average over the past sixty years.

The article touches on domestic migration and the differential contribution of immigration to regional and metro population dynamics, a topic that warrants further research effort, as does the real estate investment implications of these phenomenon. I suspect that the authors are well aware and already at work on these follow-ons. Prior to Donald Trump becoming President, immigration was playing an outsized role in propping up population in California, Illinois, and the Northeast. Without strong flows of new international arrivals, population would have been declining (NYC) or declining more (Chicago), given the strength of domestic out-migration. The authors’ conclusion is consistent with a warning that, without a reversal in policy, and maybe even a more robust immigration flow, there would seem to be significant risk of decline in some regions of the economy.

—

ABOUT THE AUTHORS

Stewart Rubin is Senior Director and Head of Strategy and Research, and Dakota Firenze is a Senior Associate, for New York Life Real Estate Investors, a division of NYL Investors LLC, a wholly-owned subsidiary of New York Life Insurance Company.

—

NOTES

1US working age population in this chart as non-institutionalized (not in the military, incarcerated, or in a long-term health institution) adults ages 20-64. Obviously, there are many people under 20 and over 65 who work, however, since many people in those categories are in school or retired, the aforementioned age category is used.

2Working age population figures (historical and forecast) are based on Oxford Economics data provided by CoStar Advisory Services. Last historical year is 2020. 2021 and onward are forecasts from Oxford Economics.2

3Based on data from February 2020 to April 2021, the observation period used in the analysis by the Dallas Fed.

4Robert S. Kaplan, Tyler Atkinson, Jim Dolmas, Marc P. Giannoni and Karel Mertens, “The Labor Market May Be Tighter than the Level of Employment Suggests” Federal Reserve Bank of Dallas. May 27, 2021.

5The employment to population ratio for 65+ is calculated with the numerator represented by those over 65 who are working and is skewed heavily towards those aged 65-70. At the same time the denominator of the ratio includes everyone over 65. The ratio during earlier time periods is inflated since the denominator includes all those age 65+ and life expectancy at birth was 70.1 years in 1964 versus 77.0 in 2020. Because life expectancy was lower in 1964, the age cohort 65-70 (who are more likely to be employed) represented a greater portion of the broader 65+ age cohort than it does today. In 2021, with relatively more individuals older than 70 or 75 than in 1964, achieving a similar employment to population ratio is even more notable.

6The employment cost index is a measure of employer’s costs for employee wages and salaries, as well as employer costs for benefits.

7Based on data from the US Census Bureau.

EXPLORE THE FULL ISSUE (SPRING 2022)

MARCHING BACKWARDS INTO THE FUTURE

The new 2022 AFIRE International Investor Survey Report reveals future institutional investment trends as the pandemic transformed how we live, work, and play.

Gunnar Branson and Benjamin van Loon | AFIRE

CITIES THAT WORK

What is it that makes London, Stockholm, Berlin, Amsterdam, and Paris the top European cities for office investment? And what could this mean for other global cities?

Dr. Megan Walters | Allianz Real Estate

SURVEY SURFEIT

Be careful about advice you hear from surveys— it will not always play out as expected.

Jim Costello | MSCI Real Estate

NEW WORKING AGE

Outside of WWI and II, the US working age population has never declined. As of 2021, that statement is no longer true.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

SELECTIVE FRAMEWORK

Two years after offices closed due to the COVID pandemic, the debate over the longterm future of the office continues. What should office investment look like going forward?

Dags Chen, CFA; Ryan Ma, CFA; and Ryan LaRue | Barings Real Estate

GARDEN VIEW

US garden apartment investments are offering outsized return potential –but access remains a challenge.

Martha Peyton, PhD | Aegon Asset Management

SINGLE-FAMILY DEMAND

As an increasingly popular asset class for institutional investors, single-family rentals are supported by strong future demand drivers to propel sector outperformance.

Daniel Manware | Nuveen Real Estate

ESSENTIAL HOUSING

The US is in the middle of one of the biggest housing crises that the country has ever seen. It needs a more resilient approach to housing.

Todd Williams | Grubb Properties

LODGING TAKES THE LEAD

As a labor-intensive and service oriented asset class, hospitality is uniquely positioned to be a leader in advancing sustainability goals for investors.

Charlotte Kang, Geraldine Guichardo, Lori Mabardi, and Emily Chadwick | JLL

CARRY ON, CARRY OVER

While continuation vehicles were once viewed as a signal of delay or failure, market sentiment is rapidly changing.

Max LaVictoire and Ashley Anderson | Hodes Weill & Associates

RENEWING ETHICS

A note from AFIRE’s Ethics Chair on the need for maximizing ethics in an age where globalization is under threat.

El Rosenheim | Profimex