The future of residential investments is all about demographics—and the forces behind them.

With more and more time spent at home, capital appetite has grown for all things residential, with new living schemes entering the fray at a rapid pace.

Yet not all living investments are as safe as houses. It is important to consider demographic wave crests and troughs and how these forces will impact prospects for the various components of the residential spectrum going forward.

MULTIFAMILY IN THE US

To holders of US real estate, multifamily properties have long been a mainstay of mixed-asset portfolios. The sector’s fulfillment of a basic necessity provides a resilient demand profile that has withstood economic volatility throughout cycles reasonably well and exhibited a quicker propensity to rebound, given the shorter nature of leases.

As institutional capital appetites and demographic cohorts have evolved, so too has the sector, moving beyond traditional urban and suburban-style multifamily buildings to encompass virtually all types of rentable living. Some operating models are newer additions, such as co-living and purpose-built single-family rentals (SFRs), while others, such as student and senior housing, had—until recently—been relegated to the role of niche investments. With ongoing challenges in the retail and hotel sectors, and elevated uncertainty clouding the near-term outlook for offices, investors’ allocations to all things “residential” appear poised to rise.

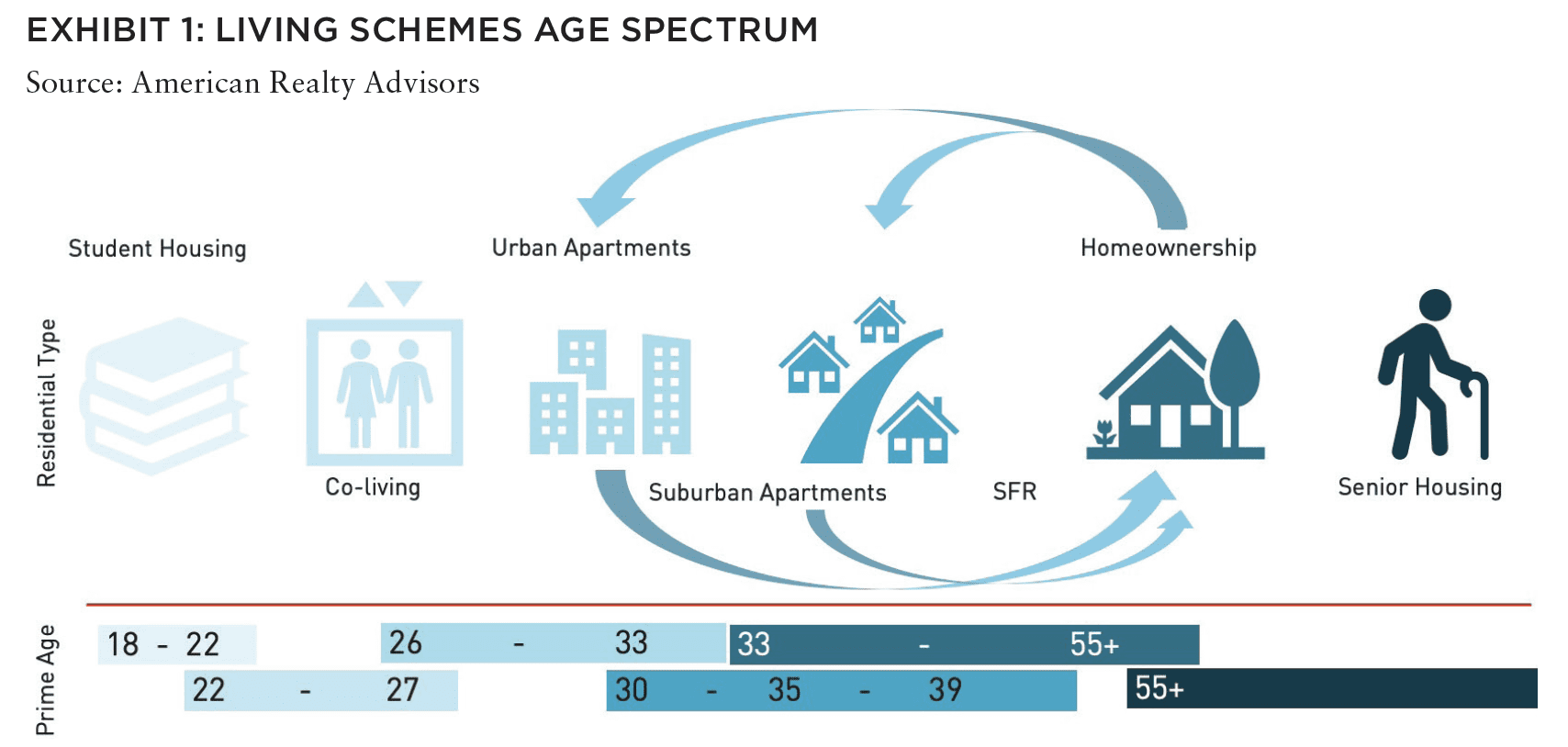

Demographics are perhaps the single-most important driver of residential real estate demand, full stop. While it may be challenging to pinpoint what future generations may want in terms of their consumption or working habits, it is less challenging to know when different cohorts will reach critical life milestones, and that they will need different types of housing along the way. It is purely a matter of simple arithmetic. This is encouraging for investors, as it allows us to anticipate changes in demand for different types of residential real estate along the age spectrum before they occur.

To think about what the composition of the US population today tells us about the prospects for residential real estate tomorrow, we need to first understand how age aligns with the different investable living schemes on the market today. While there are always exceptions to the rule, the age spans shown in Exhibit 1 reflect the core profile of renters for the various types of residential real estate.

SOME KEY TRENDS AND TAKEAWAYS

Target renter age groups tend to overlap with one another to a certain degree. This accounts for regional variations in lifestyle preferences, income, job mobility, and other trends.

Certain residential sub-types have a much more finite and thus measurable demand pool by virtue of specific limitations. For example, purpose-built student housing is dedicated exclusively to college-aged renters (typically aged 18–22), while senior housing (for which there are further delineations at the sub-subtype level) is generally restricted to those aged 55 or older.

The renter cycle doesn’t necessarily end at homeownership. There is a fair degree of fluidity back to urban/suburban apartments and SFRs after homeownership, particularly for older households. According to the National Association of Realtors, sellers between 40 and 73 comprised nearly 70% of home sellers in the twelve-month period ending July 2019, and just over half of the buyers,[1] suggesting that approximately 20% are moving from ownership into some type of for-rent housing.

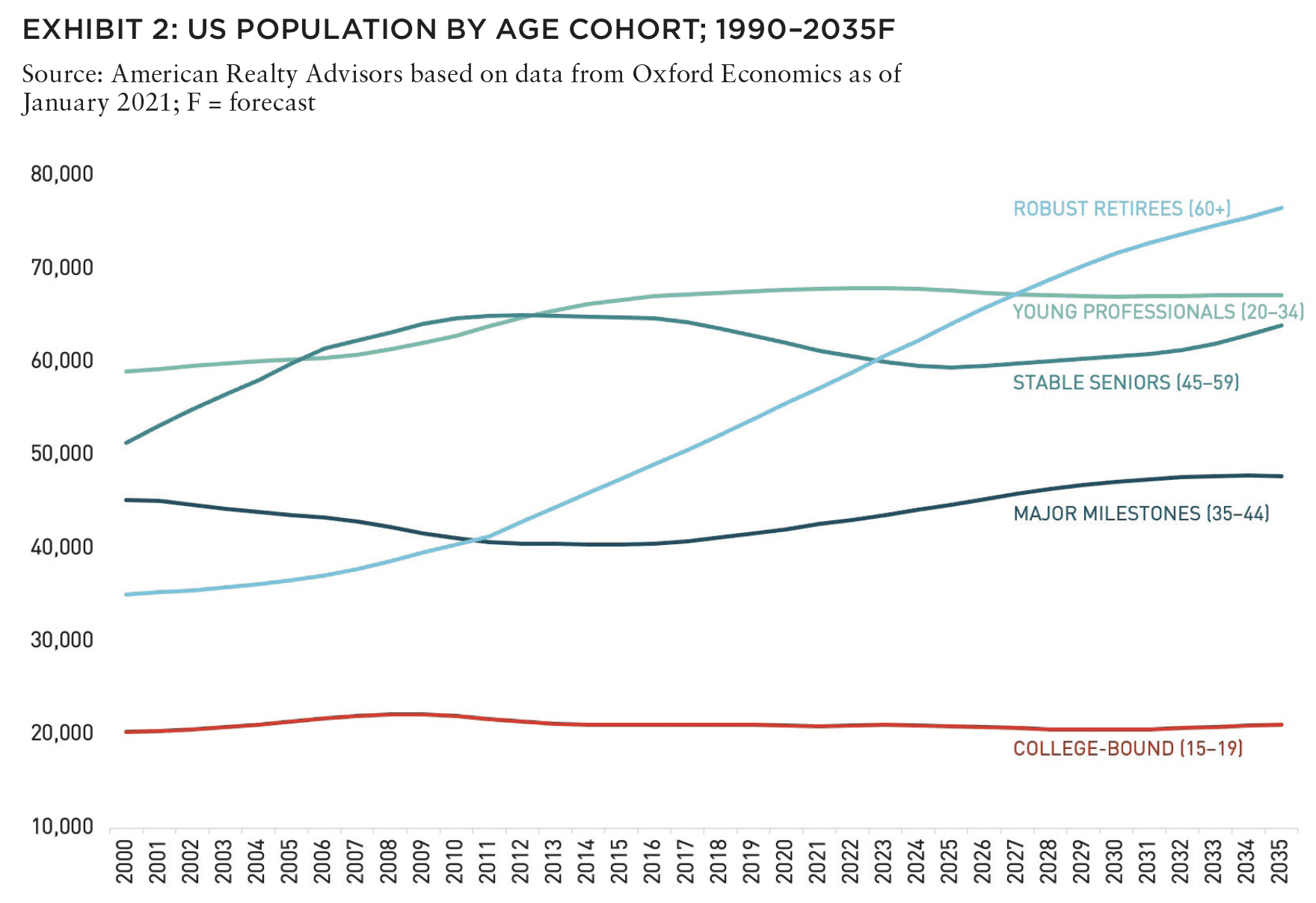

The next step is to then look at population projections by cohort. Forecasts from Oxford Economics suggests that, by 2024, the age group we’ve characterized as “Robust Retirees” (60+) will be the single largest demographic force in the country, while the college-aged population (designated as those 15–19 to account for recent, current and future enrollment) is slated to remain the smallest. Young professionals (20–34) are expected to remain a stable mainstay (as Gen Z progresses beyond their college years) while the large millennial cohort moves firmly into major milestone territory (Exhibit 2).

Standard logic suggests that, where age-based demand is expected to decline, there may be weakness for investors to avoid, and where demand is expected to grow, there are opportunities to pursue. However, these large categories, while useful in visually depicting generational shifts, mask the granularities that undoubtedly drive the potential for under-or over-performance in the coming years.

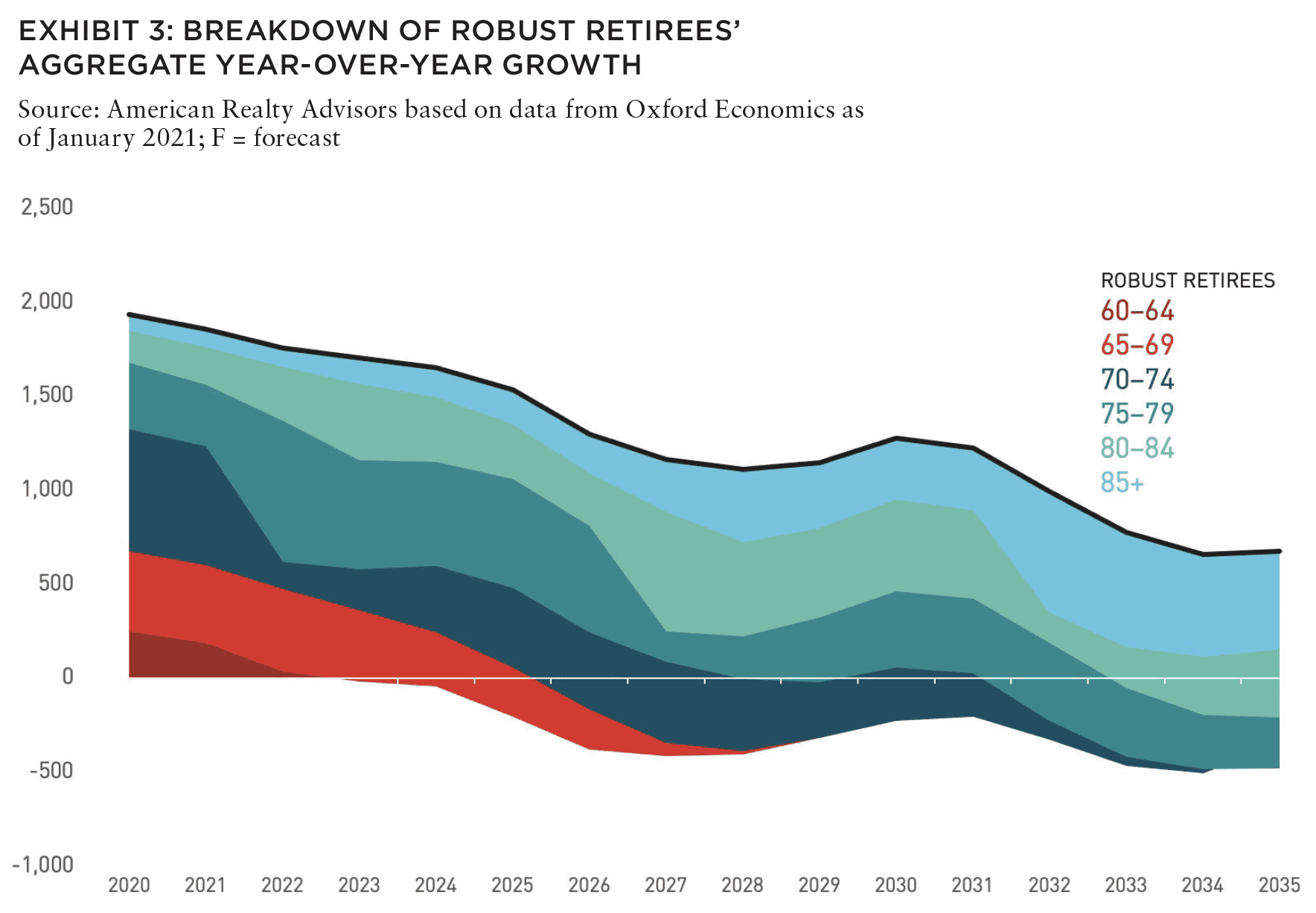

Take for example the Robust Retirees—in aggregate, this group’s trajectory is slated to trend meaningfully upward. Yet when we break down this group into smaller brackets, we can see that the lion’s share of year-over-year growth is actually being driven by the older end of the segment; those 80 years old and older (Exhibit 3). In fact, all of the growth for this cohort by the end of the decade will be fueled by those retirees 75 and older, with the 60–75 age group shrinking.

This trend has meaningful implications for an investor who may be compelled by the headline figures to embark upon constructing a senior living strategy. With the average entry age into Independent Living (the least intensive of the higher-intensity skilled/medical care-based senior facilities) pegged around 83, an acceleration in demand for this product may not occur until nearer to 2030. This is sufficiently close enough to consider for future portfolio allocations, but perhaps too far in the future to benefit investors’ portfolios today or over the next several years. Alternatively, with an average move-in age in the low- to mid-70’s, age-restricted/ active adult communities may benefit from stronger demand sooner, as the 70–75-year-old subset of Robust Retirees is expected to be one of the faster-growing cohorts between 2022 and 2025 (not to mention providing the benefits of a less-onerous operating model).

A similarly nuanced interpretation is also necessary when considering the demand backdrop for other types of residential real estate. Both age lines in Exhibit 2 seem to suggest a relatively steady profile going forward—not expanding at the rate of retirees, but holding steady relative to recent history.

ALSO IN SUMMIT (SPRING 2021)

GREAT LAKES / Tightening the Belts: How are shorthand labels like the “Sun Belt” and the “Rust Belt” shaping investment decisions? Should they?

AFIRE | Gunnar Branson and Benjamin van Loon

SOCIAL ISSUES / The Great Real Estate Reset: A data-driven initiative to remake how and what we build.

Brookings | Christopher Coes, Jennifer S. Vey, and Tracy Hadden Loh

SOCIAL ISSUES / Confronting the Myth: The events of the past year have driven businesses to confront racial inequity, but some still shy away from the challenges needed to make real progress.

Alfred Dewitt Ard Consulting | Shumeca Pickett

INDUSTRY OUTLOOK / CRE Prospects Post-COVID-19: How is commercial real estate set to perform in the post-COVID world?

Aegon Asset Management | Martha Peyton

HOSPITALITY / Time to Check In: If history is a guide, the time to invest in hotels is when things look bleak. This appears to be one of those times.

Barings Real Estate | Jim O’Shaughnessy

HOSPITALITY / Hoteling 2.0: The pandemic has impacted the hospitality, but a growing wave of non-traditional investors has shown heightened interest in the evolving industry.

JLL Hotels & Hospitality Group | Gilda Perez-Alvarado

RESIDENTIAL / Safe as Houses?: The future of residential investments is all about demographics—and the forces behind them.

American Realty Advisors | Sabrina Unger

RESIDENTIAL / Housing for Goldilocks : The pandemic highlights the advantages of single-family and appears to have accelerated migration to less dense, more affordable areas.

GTIS | Eliot Heher and Robert Sun

DATA CENTERS / Data Centers, Stage Center: Data center investments have proven resilient in periods of volatility—and they’re only going to become more essential and important into the future.

Principal Real Estate Investors | Bob Wobschall

CLIMATE CHANGE (WHITE PAPER) / Rather Than the Flood: A comprehensive look at climate-induced water disasters and their potential impact on CRE in the US.

New York Life Real Estate Investors | Stewart Rubin and Dakota Firenze

LOGISTICS / Reforging the Supply Chain: The only way to deliver on the service promises of a booming logistics sector requires a complete reimagination of the supply chain.

Stockbridge | David Egan

DEBT AND LEVERAGE / Leveraging Control: Though leverage is an important part of capital funding, it’s important to ask LPs if (and how) they should take control of their real estate leverage.

RCLCO Fund Advisors | William Maher and Ben Maslan

DEVELOPMENT / Recasting Risk and Return: The investment community can have an active role in economic recovery—but it will require recasting the traditional risk/return framework.

Standard REI | Shubrhra Jha

CORPORATE TRANSPARENCY ACT / Transparency Rules: Non-US-based investors face the disclosure regime of the Corporate Transparency Act. What do you need to know?

Pillsbury | Andrew Weiner

PENSIONS (WHITE PAPER) / Rising Pressures: The latest joint, in-depth report from Praedium and SitusAMC looks at rising fiscal pressures on state and local governments.

Praedium Group and SitusAMC Insights | Russell Appel, Peter Muoio, and Cory Loviglio | SitusAMC Insights

TALENT AND HR / Plugging the Skills Gap: Several trends are forcing change in the global commercial real estate industry, driving demand for new skills. How is the industry responding?

Sheffield Haworth | Max Shepherd

ESG / Operationalizing the Sustainability Agenda: During a time of unprecedented disruption, how should businesses approach the “new metrics” ESG of performance?

AccountAbility | Sunil A. Misser

WHAT DO THE TRAJECTORIES TELL US ABOUT FUTURE RISKS AND OPPORTUNITIES?

It is not solely the trajectories of the lines that are telling, but also their relative level and composition (not unlike our senior housing example). From 2020 through 2035, those aged 20–34-are slated to be the second-largest population group, nearly 68 million deep. By comparison, those aged 15–19 (which encompasses student housing demand) are one-third the size of our Young Professional cohort. This, coupled with a multi-year trend of declining college enrollment and declining birthrates worldwide, suggests the outlook for student housing is not as compelling as traditional urban or suburban multifamily apartments.

Splitting the Young Professionals grouping down into even-smaller age brackets provides further insight as it relates to the different types of rentals. Of the three five-year age bands aggregated in the Young Professionals grouping, the 30–34 category is expected to experience a net increase between now and 2025, while the number of newly minted graduates in the 20–24 range are expected to shrink, suggestive of resilient demand for suburban apartments and SFRs, but a reduced tenant pool for co-living.

The coming generational changeovers create both opportunities and risks for holders of residential real estate. Being able to identify how these forces will influence future demand is but one of the considerations that need to be accounted for when evaluating the composition of one’s residential investments. While we believe there will always be compelling opportunities in all the subsectors we noted at the right price and in the right location, macro forces are not to be ignored—particularly for the long-term investor. Given the significant capital appetite for the living sector, anticipating demographic tipping points can assist in triggering prudent acquisitions timing to maximize exposure to growing demand while minimizing exposure to segments poised for a pullback.

DEMOGRAPHIC IMPLICATIONS FOR RESIDENTIAL REAL ESTATE

• Senior housing demand will increase, though not until nearer the end of the decade for some higher-intensity models.

The simple combination of an aging domestic population alongside longer life expectancies should create long-run demand for the various types of senior housing (age-restricted, independent/ assisted living, and skilled nursing). However, the average Independent Living entry age is 83, with Assisted Living/Skilled Nursing entry even later. With the first baby boomer not reaching 83 until 2029 and the crest of this demographic wave not surpassing that threshold until 2039,[2] investors are likely better off in targeting the more imminent opportunity in the active adult segment.

• Student housing and co-living may see demand moderate.

With offerings that cater to a shrinking youth cohort, both student housing and co-living are likely to experience a softening in demand in the years ahead. For the former, declining student enrollments preCOVID already portended a weakening demand backdrop; in fact, fall 2020 marked the ninth consecutive year of enrollment declines at degree-granting institutions.[3] Meanwhile, co-living will need to contend with the one-two punch of a shrinking demand base and near-term downward price and occupancy pressure from a more competitive traditional urban apartment landscape.

• Increasing appetite for rental housing that caters to aging millennials’ delayed lifestyle milestones.

The number of those aged 20–24 nationwide is expected to decline by nearly 1 million between now and 2030 as the millennial cohort (typically defined as those born between 1981 and 1996) ages into the next bracket. Well-documented student loan burdens and weakened job prospects post-GFC have stunted this group’s earning potential relative to prior generations, with the effect of delaying critical life milestones such as marriage, childrearing, and homeownership. With millennials now moving towards those events in greater numbers, larger suburban apartments in good school districts and SFRs that offer the trappings of homeownership with the lessened down-payment burden are poised to benefit.

—

ABOUT THE AUTHOR

Sabrina Unger is Managing Director, Head of Research and Strategy for American Realty Advisors, one of the largest privately held real estate investment management firms in the US.

NOTES

1 “2020 Home Buyer and Sellers Generational Trends Report,” National Association of Realtors 2020 Generational Trends Report, March 2020, nar.realtor/sites/default/files/documents/2020-generational-trendsreport-03-05-2020.pdf

2 US Census Bureau based on number of live births per year, 1946–1964, census.gov/search-results.html?q=1946-1964&page=1&stateGeo=none&searchtype=web&cssp=SERP&charset=UTF-8

3 National Student Clearinghouse Research Center, October 2020, nscresearchcenter.org/