A new model for underwriting offices, based on a framework commonly seen in hospitality assets, can maximize value by giving occupiers what they want.

It is becoming a universally accepted reality that many office assets are potentially impaired for the long-run due to shifts in tenant demand, rising costs of capital, and an overall fear that oversupplied markets will equate to a protracted period of falling effective rents and NOIs.

This article offers a potential solution to this problem—and slightly contrarian take—by arguing that office assets are largely in trouble because the traditional framework for leasing, underwriting, and valuation is finally obsolete.

A new model, based on a framework commonly seen in hospitality assets, that focuses on maximizing current revenues (as opposed to long Weighted Average Lease Terms) from rents and ancillary revenues can maximize value by giving occupiers what they want. An increasingly outdated underwriting model is proving to be a large roadblock for innovation, but there is a potential new framework that can be adapted by owners, equity investors, and lenders to make such repositions feasible.

THE TRADITIONAL OFFICE MODEL IS EVOLVING— AND OWNERS ARE UNAWARE (FOR NOW)

While much of the current talk of office distress is blamed on changes in work trends due to the pandemic, the office model has been undergoing significant change for well over a decade. These changes, which include open-plan layouts, open addressing, and even flexible work-from-home arrangements, were kicked off by post ’08-GFC cost saving measures and accelerated by technological advances (i.e., smart phones, thin laptops, and fast home WiFi).

Tenant Demands and Landlord Expectations are Mismatched

The fundamental problem is that landlords and tenants have never been more mismatched in their desires for leasing office space. Landlords want long-term leases with escalating rents that shift as much operational cost exposure to tenants as possible, while tenants want short-term, highly flexible arrangements that acknowledge the general level of uncertainty in managing a knowledge-based enterprise with shifting employee preferences and work patterns.

Said simply, landlords are seeking to maximize long-term value and tenants are seeking to optimize short-term needs. This is not an intractable problem, however; if landlords adapt their offerings to the needs of their customers, they could potentially make greater revenues and thus profits. The issue is not willingness or ability to pay, it is willingness to accept a fixed offering for a fixed term.

Traditional Underwriting Standards and Framework are a Roadblock

The above should be no surprise to anyone in the real estate industry. Coworking operators have literally built businesses on capturing the consumer surplus between landlord needs and tenant desires (i.e., leasing long from landlord and renting short to users for a markup). Thus, why haven’t landlords just cut out the coworking middlemen?

Underwriting standards, and specifically Weighted Average Lease Term (WALT) is a key metric in office underwriting. With WALT, longer the better; when an asset’s remaining WALT falls too low (generally under fi ve years) its value and salability can be substantially impacted. As a result, landlords seek to force long-term leases while rejecting short-term offers, often at great costs (i.e., large tenant improvement allowances and free rent periods as incentives to lease). In fact, the aversion to short WALTs is so strong, assets have been known to trade for higher prices with vacancy (as can be leased long-term) than with comparable space leased with short expirations. This mindset and reliance on such underwriting standards must be changed if the office market is to stabilize and maximize values going forward.

THE NEW UNDERWRITING MODEL FOR OFFICE ASSETS

The current office underwriting standards must be augmented and replaced. While long-term credit leases will certainly remain valuable, income generated via shorter-term leases and ancillary/service offerings (meaning non-rent) must be more equally valued when making leasing and management decisions. The hospitality industry offers the most useful guide for making adaptations to the office standards and are thus the basis for the ideas presented herein.

Total Revenues Matter, Weighted Average Lease Term Does Not

The single biggest change needed to the office underwriting standard is the recognition of total revenues irrespective of source. Meaning, whether via leases of one day, one year, or twenty years, the most important metric is how much actual cash is collected. Further, revenues from parking, vendor arrangements, and ancillary services also count as equally as dollars from space rented via leases. This is the basis of underwriting in hospitality assets and, to a greater extent, multifamily (though customs and regulations preclude much flexibility in offering shorter than a year leases in most instances).

Thus, an underwriter would look at an asset’s trailing income history and make forward projections based on economic and market variables to generate a multi-year forecast. This could supplement or outright supplant the current lease-by-lease renewal analysis generally preformed and made easy by software platforms like Argus.

Why Hospitality Values RevPAR, and Office Owners Should Too

The hotel industry has long valued Revenue Per Available Room-night (RevPAR) as a preferred metric of analyzing “top-line” revenue generation by an asset (or market). This metric takes the total room revenue collected/forecasted and divides by the available number of room nights and thus automatically factors rate charged and actual occupancy.

A similar metric such as Revenue Per Available Foot (RevPAF1 ) needs to become a standard in office underwriting. However, while the hotel metric generally only accounts for room revenues (omitting food and beverage, event rentals, etc.), an office building’s total revenues regardless of source (i.e., rent and services) should be factored as the ability to generate bottom-line NOIs will depend more on total revenue collections than simply looking at pure rental revenues. This metric would make better apples-to-apples comparisons of buildings and give owners better incentives to invest in revenue generating activities via rents and services to maximize profits.

Potential for Long-Term Value Creation

While co-working operators have experienced tumultuous financial results, they have in fact proven a successful operating model. Tenant experience matters, flexibility can be priced at a premium, and many users (including Fortune 100 firms) will actually forego privacy of a sperate office environment if the space meets the overall needs of their employees.

But the most important thing office landlords must learn from co-working is that space that can be “common” should be common (or at least tenants should have the option to use as such, for a fee). This includes breakrooms, open seating areas, conference rooms, and even private offices (rented daily/monthly as needed). These flexible arrangements can generate revenue premiums, thus maximizing RevPAF and overall office values.

SUCCESSFULLY REPOSITIONING TROUBLED OFFICE ASSETS

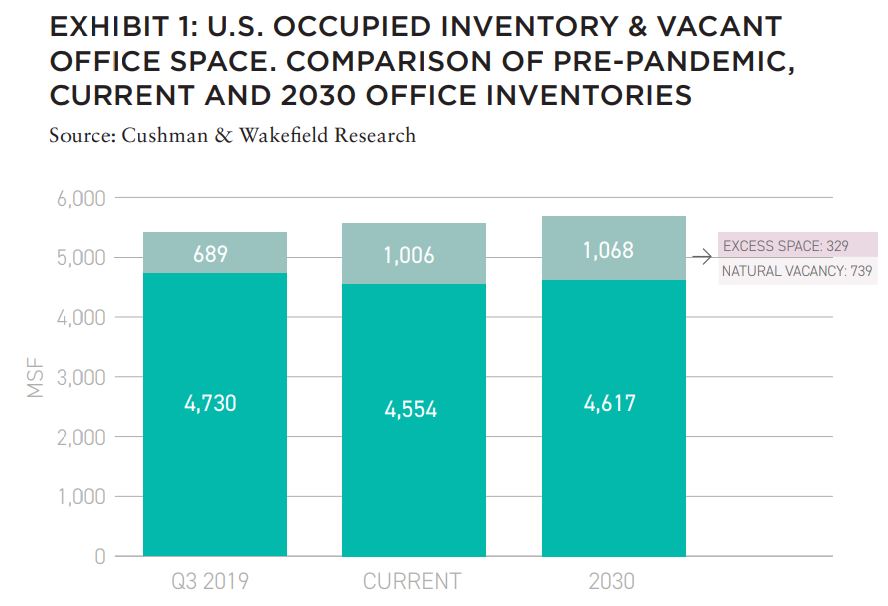

At present, it is difficult to estimate how many troubled office assets there are or will be in the coming years, yet capital markets and owners have begun to realize that substantial impairments and devaluations are likely underway as a result of shifting demand. Cushman and Wakefield has estimated that an additional 330 million square feet of office space will be vacant due to hybrid working by 2030.2 Further, their report identifies approximately 3.4 billion SF of commodity office space they call “The Middle”; a set which represents about 60% of all US office space that most stands to benefit from a hospitality transition.

Implementing a New Leasing Framework

The first step is the easiest to implement, but the most difficult to mentally accept; that is, the willingness to lease space on short-term basis to more tenants, including those without the traditional credit profile sought by institutional investors. This is a necessary reality, and adoption of the hospitality underwriting framework discussed herein should make it less painful.

The are other upsides, besides higher immediate occupancies and cashflow; mainly, the landlord’s ability to regain control of capital expenditure cycles as short-term tenants cannot (and will not) demand large tenant improvement or free rent packages. These factors have led office assets to underperform other asset classes for years.

Creating Monetizable Common and Shared Spaces

The use of short-term leases alone will not necessarily restore values or grow profitability, for that to happen, landlords must look at revenue maximization by monetizing common and shared spaces. This will be more difficult as it requires on-site management infrastructure to support such operations, however technology has made this far easier in current years than ever before.

Current operators and managers may chose to partner or subcontract with existing co-working operators, while others will see the long-term value in creating such platforms themselves. For some assets, this will yield substantially higher RevPAFs than utilizing simple fixed-address leases alone.

Creating and Enhancing Ancillary Revenue Streams

The hospitality industry has long understood that room-night revenue is just one potential profit center in operating a hotel asset. In many ways, office buildings and hotels have similar fundamentals to allow for ancillary revenue streams to become profit centers. These include food and beverage sales, event space rental, technology fees, and even ad hoc professional services such as executive assistance, design and graphics, and so forth.

While many buildings have food vendors and other such items, these are generally separate leases or concessions with minimal revenue impacts. Under an enhanced hospitality model, the landlord would own the vendor/concessions (or joint venture with revenue share) and thus be better aligned to offer greater services to users and employees of the building, leading to higher overall revenue and profit maximization.

WILL INVESTORS AND LENDERS ACCEPT THE NEW MODEL?

The final question and concern office owners face in adopting any of the ideas proposed herein is simple: will the intuitional investors and lenders accept such new models?

Given the wide ownership of office assets and loans secured by office buildings, investors and lenders will likely need to do so to maintain and restore values of their existing assets. In fact, lenders who regain ownership of highly vacant office buildings may be the class of owner most likely to embrace such non-standard leasing and operating tactics.

With the benefit of time comes hindsight, and hindsight could offer proof if such methods worked. If an owner can show a successful one- to three-year operating history by utilizing more short-term leases and generating more service revenues, then it is likely that buyers, lenders, and appraisers will believe it has greater growth potential as well. Unfortunately, there is no short-term magic solution being offered.

The office industry is at a point of decision: does it attempt to force its customers into offerings they increasingly do not want, or does it accept the new reality and tailor solutions that meet the needs, aspirations, and desires of its occupants?

As is often the case, those owners and managers that move first may gain a substantial advantage over those who wait.

EXLORE THE FULL ISSUE

ALSO IN THIS ISSUE

AFIRE INTERNATIONAL INVESTOR SURVEY: Q1 2023 PULSE REPORT

Gunnar Branson and Benjamin van Loon | AFIRE

VALUATION CHALLENGE: SOLVING THE CRISIS IN COMMERCIAL REAL ESTATE VALUATION

Matt Pomeroy, MAI and Jackie Bowie | Chatham Financial

CONVERSION CALCULATOR: LEGAL OR NOT, A DYNAMIC CITY WILL CONVERT UNUSED OFFICES

Jim Costello | MSCI Real Assets

UNDERWRITING ROADBLOCKS: CAN THE HOSPITALITY MODEL OF UNDERWRITING SAVE OFFICE VALUES?

Joshua Harris, PhD | Lakemont Group & Fordham University

VACANT SPACE: OFFICE-USING JOBS AND DEMAND INCONGRUITY

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

HIKING TRAILS: SHOULD INVESTORS CONSIDER ALLOCATIONS TO FLOATING-RATE DEBT?

Dags Chen, CFA | Barings Real Estate

RECESSION PREPPING: HOW VULNERABLE ARE COMMERCIAL MORTGAGE INVESTMENTS

Martha Peyton, PhD | Aegon Asset Management

MEASURING GENTRIFICATION: USING DATA SCIENCE TO PREDICT THE IMPACTS OF GENTRIFICATION

Ron Bekkerman | Cherre + Donal Warde | Tenney 110 + Maxime C. Cohen | McGill University

THE FUTURE IS EUROPEAN: THEMES FROM THE OLD WORLD SHAPING US MARKETS

Brian Klinksiek | LaSalle Investment Management

CULTURE SHOCK: THE CHALLENGE AND IMPORTANCE OF TRANSLATING ESG ACROSS BORDERS

AFIRE ESG Committee

FINE TUNING: GLOBAL REACH AND LOCAL EXPERTISE CAN CREATE UNIFIED REAL ESTATE EXPERIENCES

Mark Zettl | JLL

ACCESSING SUCCES: EXPLORING DIVERSITY TRENDS IN REAL ESTATE TALENT

Zoe Huges | NAREIM

RESCUE CAPITAL: RESPONDING TO THE NEW REAL ESTATE REALITY

Andrew Weiner and Joshua M. R. Becker | Pillsbury

CONVEX CURVES: A REMINDER ON PRICE CONVEXIVITY AND CAP-RATE VOLATILITY

Joseph Pagliari, PhD, CFA, CPA | University of Chicago

IN MEMORIAM: ANDREA MARIE CHEGUT, PhD, MIT

—

ABOUT THE AUTHORS

Dr. Joshua Harris is the Managing partner of the Lakemont Group and a leading real estate economist and investment strategist specializing in real estate development, finance, capital markets, and business organizational leadership and strategy. Dr. Harris excels at assessing feasibility/profitability of projects, markets, and investment strategies/funds; examining the state of the macroeconomy and its impacts on real estate markets; delivering dynamic presentations for industry audiences; and providing strategic guidance and business development services for large organizations. Dr. Harris has been routinely called on as an expert witness and for media interviews in the field of real estate, finance, and economics. His clients include national real estate developers, real estate investment trusts, private equity firms, law firms, and hospitality institutions as well as local governments and real estate companies.

—

NOTES

1. Note, this term, RevPAF, has been widely used by Green Street Advisors as a market metric for years. This article is proposing the use of a such a metric in the management and underwriting of office buildings. While these concepts are very similar, the author is not attempting to suggest the specific use of the Green Street Advisors methodology or anyone else’s.

2. Cushman & Wakefield. “Obsolescence Equals Opportunity.” Cushman & Wakefield, 2020, https://www.cushmanwakefield.com/en/united-states/insights/obsolescenceequals-opportunity.

—