There is a growing variance between valuations and real-time pricing. Can the global institutional real estate industry achieve universal standards and consistency?

Commercial and multifamily real estate market conditions through the first quarter of 2023 have shown that the market must address and better align disparate approaches to underwriting and calculating returns and current real estate valuation practices.

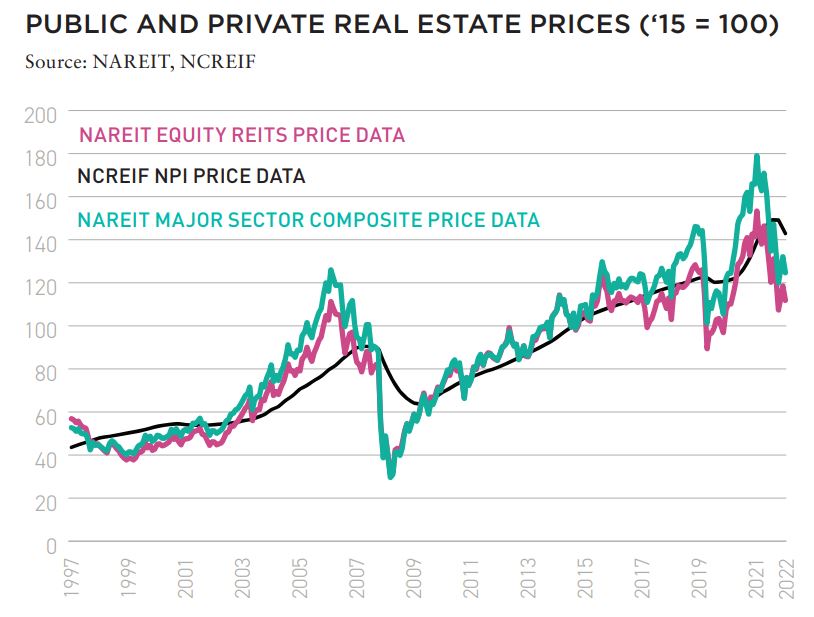

Through an increase in market volatility and interest rates, as well as a reduction in investment sales volume and observable data points, we’ve seen a growing variance between valuations and real-time pricing.

This variance results in inconsistencies and material disagreements among market participants, including investment managers, valuation service providers, consultants, and auditors. Investors in private real estate investment vehicles and separately managed accounts may be most affected by this disconnect. Their investment values, returns, and performance may be impacted or misrepresented.

Our observation is that investment underwriting and fund returns are most often calculated with consideration of the impacts of leverage. However, current market standard valuation practices are almost always conducted on an unlevered basis, with debt and derivative valuations layered in separately. Adding debt and derivative marks to market valuations may be appropriate in a stabilized market environment. The components, however, become disconnected when property valuations lag real-time market shifts, as we’ve seen the past few quarters. Reconciliation will best be found in evolving commercial real estate valuation practices toward consideration of levered equity methods with more timely inputs, even if they are less directly observable yet more indicative of market dynamics when sale transaction data is not available.

When interest rates rise as they have, existing loans are marked to market, which has a positive impact on net asset value. However, if property values don’t also commensurately decline, as would be expected if the cost of capital has increased, the implied levered equity yields compress to levels that are inconsistent, sometimes wildly so, with expected levered equity yields.

When property values (and unlevered yields, or discount rates) don’t change in a volatile market because of lack of transaction data points, two issues are created: 1) NAVs may go up or stay level when intuition tells us they should be declining, and 2) implied levered equity yields compress to levels that are inconsistent with market expectations. To clarify, the levered equity yield is a variable in the weighted average cost of capital formula that includes unlevered discount rates and interest rates.

Simply, if property values and unlevered returns are fixed, as interest rates go up, the only place to account for this increase in the cost of financing is a reduction in the equity position’s return. Given the current market volatility and rising interest rates, it is reasonable to expect that levered equity return expectations may not only remain steady but potentially increase, considering the challenges that these economic factors can pose to commercial real estate occupiers.

Debt and derivative information is available at more frequent intervals. Interest rate and foreign exchange hedge information is essentially measurable up-to-the-minute, even in volatile market conditions. Debt interest rates essentially are measurable up to the week or more frequently. The problem is not in the greater observability and timeliness of debt and hedge valuations, but rather that property valuations do not consider this information. It is the lag (or absence) of timely asset valuation updates, due to the application of outdated market standard valuation practices, that are the problem.

This is not to assume that real estate should now be considered a liquid asset class, but rather that a more data-driven valuation technique can yield more frequent and more accurate valuation updates, particularly when done considering the impact of leverage via a levered equity approach.

So, what’s the solution? We contend that a concerted and concentrated global effort between some of the largest real estate investment managers, valuation service providers, auditors, and the valuation industry organizations is the only path to redefining and aligning valuation practices for more timely, accurate, and consistent results across the global commercial real estate industry.

Across every other industry, we see aggregation and integration of timely data, predictive algorithms (dare we say artificial intelligence?), open source code, and consistency of key data structures and definitions. In the global institutional real estate industry, we still struggle at times with global standards and consistency of data definitions.

Although incremental change and broader consideration of leverage in property valuations would be valuable, this is not a challenge to be solved and implemented by a few market participants, and then gradually adopted across the industry. Consistency in approach is best for all market participants, especially large investors who are assessing performance across various investment managers.

The bottom line is that more timely, consistent, data-informed valuations that are more aligned with how investments are priced and monitored (inclusive of leverage considerations) are better for the industry, for valuation service providers, investment managers, and ultimately those providing the capital fueling this market: institutional and retail investors.

—

ABOUT THE AUTHORS

Matt Pomeroy, MAI, is Director of Valuation, Reporting, and Analytics, and Jackie Bowie is Managing Partner, Board Member, Head of EMEA, for Chatham Financial, a global financial risk management firm.

—

EXLORE THE FULL ISSUE

ALSO IN THIS ISSUE

AFIRE INTERNATIONAL INVESTOR SURVEY: Q1 2023 PULSE REPORT

Gunnar Branson and Benjamin van Loon | AFIRE

VALUATION CHALLENGE: SOLVING THE CRISIS IN COMMERCIAL REAL ESTATE VALUATION

Matt Pomeroy, MAI and Jackie Bowie | Chatham Financial

CONVERSION CALCULATOR: LEGAL OR NOT, A DYNAMIC CITY WILL CONVERT UNUSED OFFICES

Jim Costello | MSCI Real Assets

UNDERWRITING ROADBLOCKS: CAN THE HOSPITALITY MODEL OF UNDERWRITING SAVE OFFICE VALUES?

Joshua Harris, PhD | Lakemont Group & Fordham University

VACANT SPACE: OFFICE-USING JOBS AND DEMAND INCONGRUITY

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

HIKING TRAILS: SHOULD INVESTORS CONSIDER ALLOCATIONS TO FLOATING-RATE DEBT?

Dags Chen, CFA | Barings Real Estate

RECESSION PREPPING: HOW VULNERABLE ARE COMMERCIAL MORTGAGE INVESTMENTS

Martha Peyton, PhD | Aegon Asset Management

MEASURING GENTRIFICATION: USING DATA SCIENCE TO PREDICT THE IMPACTS OF GENTRIFICATION

Ron Bekkerman | Cherre + Donal Warde | Tenney 110 + Maxime C. Cohen | McGill University

THE FUTURE IS EUROPEAN: THEMES FROM THE OLD WORLD SHAPING US MARKETS

Brian Klinksiek | LaSalle Investment Management

CULTURE SHOCK: THE CHALLENGE AND IMPORTANCE OF TRANSLATING ESG ACROSS BORDERS

AFIRE ESG Committee

FINE TUNING: GLOBAL REACH AND LOCAL EXPERTISE CAN CREATE UNIFIED REAL ESTATE EXPERIENCES

Mark Zettl | JLL

ACCESSING SUCCES: EXPLORING DIVERSITY TRENDS IN REAL ESTATE TALENT

Zoe Huges | NAREIM

RESCUE CAPITAL: RESPONDING TO THE NEW REAL ESTATE REALITY

Andrew Weiner and Joshua M. R. Becker | Pillsbury

CONVEX CURVES: A REMINDER ON PRICE CONVEXIVITY AND CAP-RATE VOLATILITY

Joseph Pagliari, PhD, CFA, CPA | University of Chicago