Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

With the uncertainty around the future of work, the common understanding of how many in-office days make up a “work week” is in flux. As recently highlighted by the Washington Post, workers’ preference for going into the office in the middle of the week, rather than either end, may create new expectations for the CRE industry.1

Even before the COVID-19 pandemic, companies and employees were floating the idea of a “four-day workweek.” The topic has been in discussion for years (in fact, many decades2), and now some start-ups and tech firms have begun doing away with Fridays altogether.3 In one way, this could add a new element of underwriting analysis for office and multifamily properties in NYC. With new emissions regulations looming, a four-day workweek could shift a large portion of energy use (and potential fines) from offices to apartments.

Workers spending less time in the office post-pandemic may seem entirely negative for the office sector but in one way, a four-day workweek can be a boon for some office property owners. One less office workday and possibly as much as 20% less office utilization and energy usage could bring unexpected relief to those New York office landlords who were facing fines for exceeding their greenhouse gas (GHG) emissions statutory limits under Local Law 97 (LL97). Conversely, if most of those in-office Fridays are replaced with people working from their NYC apartment living rooms, the burden of energy usage (and fines) could be passed to the multifamily sector.

REMIND ME: WHAT IS LOCAL LAW 97 AGAIN?

LL97 is part of the greater NYC Climate Mobilization Act4 which includes five local laws and is one of the largest city-level emissions reductions acts globally. In a city unique because the majority of its emissions come from its buildings rather than is transportation,5 it’s not surprising that all five local laws target buildings. The other laws in the package focus on energy efficiency, solar panels and green roofs, and creating a Property Assessed Clean Energy Fund for New York City.6 Importantly, this fund launched in 2021 and provides a funding mechanism for owners looking to implement energy retrofits to comply with LL97.

LL97 itself has provided an example for similar laws popping up in cities around the country. Under the groundbreaking legislation, most buildings with more than 25,000 square feet will be required to meet new energy efficiency and greenhouse gas emissions limits by 2024, with tighter limits in 2030. The stated goal7 is to reduce the emissions produced by the city’s largest buildings by 40% by 2030 and 80% by 2050. Building owners will need to report their emissions by May first every year beginning in 2025,8 which is the year LL97 will impose financial penalties for building owners that are not compliant with the law.

The annual penalty is the difference between a building’s annual tonnage of carbon emissions (estimated as a multiple of the energy usage depending on energy source) and its emissions limits (which are based on property type9), multiplied by $268. In 2021, Moody’s Investors Service (MIS) did an analysis10 of the potential fines associated with this penalty and found them to be relatively minor compared to the average NYC rent per square foot, though not an insignificant portion of property net revenue on average. Based on this analysis, most fines for exceeding 2024 and 2030 emissions caps will be less than 3% of NOI. However, for a handful of NYC buildings, the fines could be quite burdensome—potentially more than 10% of NOI.

As investors integrate this information into their due diligence and strive to understand the financial implications of LL97, other factors will adjust their analyses. As building owners and tenants explore the future of work and consider adopting long-term hybrid plans for office use, Moody’s initial findings on the financial impact might change.

BY THE NUMBERS: HOW MUCH OF A SHIFT COULD THERE BE?

For illustrative purposes, we assume a 20% reduction or increase in energy usage based on shifting one workday from the office to home. It’s important to caveat that this 20% energy shift is a ceiling, and somewhat unrealistic, given that many building systems consume energy whether or not humans are in the building.

However, it’s clear that the future of work is hybrid, so a lot of energy savings are likely found during the rest of the week besides Fridays.

For apartments, it’s more likely the increase is much smaller than 20%, as shown by studies of energy usage during the pandemic.11 But, for now we’ll stick with the 20% assumption just to illustrate the extreme version of energy usage shifting due to a 20% shorter in-office workweek.

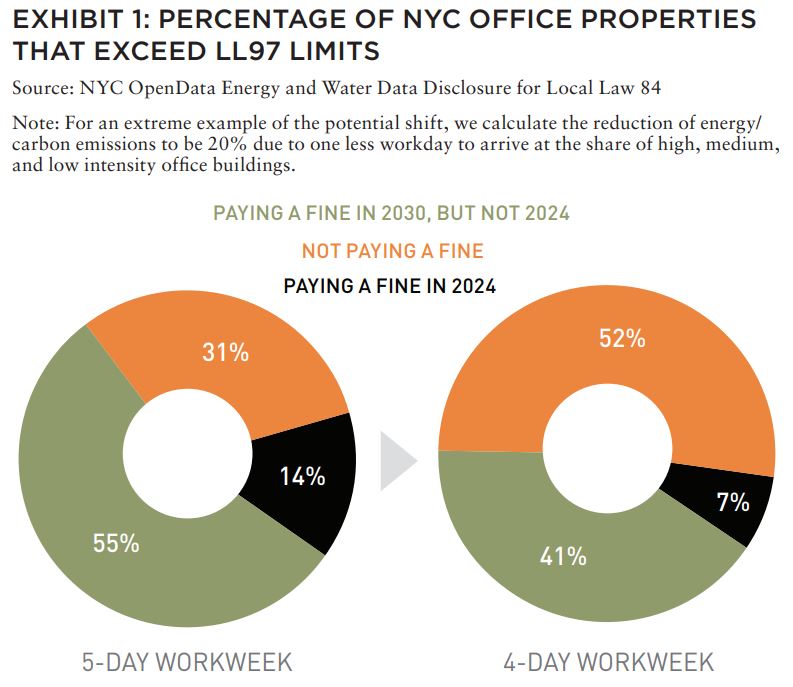

As shown in Exhibit 1, when people go to work five days a week, 14% of NYC office properties are subject to pay fines based on LL97 2024 limits, another 55% will be subject to fines in 2030. If a four-day workweek becomes the norm, and energy usage drops 20%, the number of fined office properties will be halved to just 7% in 2024. In 2030, 14% more property owners would be spared the fines from the estimated 55% down to 41%.12

Based on Moody’s Investors Service’s 2021 paper,13 among offices exceeding their 2024 greenhouse gas (GHG) emissions limits, the average fi ne was $1.15 per square foot (PSF). With a 20% reduction of energy usage, the average fine would decrease 23% to $0.88 PSF. For the 2030 limits, the average fines would decline 29% from $0.89 PSF to $0.63 PSF.14

For NYC multifamily properties, we estimate that 21% are currently subject to pay fines based on 2024 emissions limits, and 77% in 2030 (including properties that exceed 2024 limits). If there is a 20% increase in multifamily energy use as a result of a four-day workweek, the percentage of multifamily owners that will be on the hook rise from 21% to 40%. By 2030, that number will rise by 9 percentage points—from 77% to 86%.

Among multifamily buildings exceeding their 2024 GHG emissions limits, the average fine based on Moody’s Investors Service’s 2021 analysis is $0.37 PSF, which would increase 29% to $0.52 PSF with a 20% increase in energy usage. For the 2030 limits, the average fines would rise 25% from $0.48 PSF to $0.64 PSF.

THE IMPLICATIONS FOR MULTIFAMILY OWNERS

Multifamily building owners in NYC already have other challenges with mitigating the potential costs of LL97, such as:

- Some of the highest potential fines PSF among property types

- More complicated energy retrofits

- Less ability in NYC to legally pass along capex to tenants

- Less ability in NYC to raise rents aggressively with legal caps

Recognizing that the four-day in-office workweek, or another hybrid arrangement, may be here to stay, and that it may push apartment buildings past their emissions limits, multifamily building owners now have an opportunity to make gradual changes to mitigate the financial burden they face from increased work-from-home and the associated energy use. This knowledge also provides investors with additional questions to ask during their due diligence or targeted engagement encouraging building owners to get ahead of these risks.

For example, owners can consider gradual replacement of equipment like air handler units and water heaters with more efficient options as these devices reach the end of their life cycles. They can also promote their sustainability measures in their marketing to potential tenants, which is an important issue for many tenants, commercial and residential alike. This preference is so strong that there is a growing premium for buildings that have taken sustainability measures, all else equal.

This premium can help owners economically justify significant one-time retrofit investments by avoiding LL97 fines, saving on energy costs, and getting a rent premium for sustainability efforts.

ABOUT THE AUTHORS

Kevin Fagan is Senior Director, Head of CRE Economic Analysis; Xiaodi Li is Associate Director, Senior Economist; and Natalie Ambrosio Preudhomme is Associate Director for Moody’s Analytics, which provides financial intelligence and analytics.

—

NOTES

1. Bhattarai, Abha. “Nobody Wants To Be In The Office on Fridays.” The Washington Post, July 15, 2022. https://www.washingtonpost.com/business/2022/07/15/its-official-fridays-office-are-over/.

2. Meisenzahl, Mary. “People Have Toyed With the Idea of a 4-Day Workweek for Over 80 Years.” Business Insider. Accessed December 6, 2022. https://www.businessinsider.com/history-4-day-workweek-microsoft-japan-great-depression-2019-11.

3. Williams, Trey. “The New Trends in Flexible Work Could Mean More Employees Choose a 4-Day Week.” Fortune, July 1, 2022. https://fortune.com/2022/07/01/is-the-five-day-workweek-in-trouble/.

4. “Local Law 97.” NYC.gov. Accessed December 6, 2022. https://www.nyc.gov/site/sustainablebuildings/ll97/local-law-97.page.

5. Cohen, Steve, Christopher M. Fragomeni, and Dan Pinkel. “Reducing Greenhouse Gas Emissions from NYC’s Buildings.” Columbia University, August 22, 2022. https://news.climate.columbia.edu/2022/08/22/reducing-greenhouse-gas-emissions-from-nycs-buildings/

6. “NYC Accelerator Pace Financing – New York City.” NYC.gov. Accessed December 6, 2022. https://www1.nyc.gov/assets/nycaccelerator/downloads/pdf/pace-program-guidelines_v1-0_20210422.pdf.

7. NYC.gov. New York City’s Roadmap to 80 x 50. Accessed December 6, 2022. https://www1.nyc.gov/assets/sustainability/downloads/pdf/publications/New%20 York%20City%27s%20Roadmap%20to%2080%20x%2050_Final.pdf.

8. “Compliance: Local Law 97.” NYC.gov. Accessed December 6, 2022. https://www1.nyc.gov/site/sustainablebuildings/requirements/compliance.page. Note that many buildings are already required to report emissions as part of the NYC Benchmarking Law, Local Law 84.

9. The specifics of the property type classifications and emissions limits are still being defined. On Nov 14th there was a public hearing about proposed updates to the rule related to these technicalities. Our analysis is based on the definitions and guidelines included in the original 2019 law. The proposed updates from October can be found here: https://www1.nyc.gov/assets/buildings/pdf/proposed_greenhouse_gas.pdf.

10. “Moody’s Research.” Moody’s. Accessed December 6, 2022. https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBS_1266408.

11. Calculation is based on NYC OpenData Energy and Water Data Disclosure for Local Law 84 (Data for Calendar Year 2019). See also: https://data.cityofnewyork.us/browse?q=Energy%20and%20Water%20Data%20Disclosure&sortBy=relevance; https://www1.nyc.gov/assets/sustainability/downloads/pdf/publications/New%20 York%20City%27s%20Roadmap%20to%2080%20x%2050_Final.pdf.

12. “Moody’s Research.” Moody’s. Accessed December 6, 2022. https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBS_1266408.

13. Special thanks to John Boyle in Moody’s Investors Service for his original 2021 work and consultation.

EXPLORE THE LATEST ISSUE

MAKE SUSTAINABILITY REAL

With the case for sustainability already well-established, how can (and should) real estate continue to lead?

Gunnar Branson | AFIRE

RETURN GENERATION POTENTIAL

In addition to offering inflation protection and lower volatility, real estate also offers something that other asset classes can’t: the opportunity to invest in tangible, positive change.

Shane Taylor | CBRE Investment Management

CATCH A FALLING *R

The future path of long-term interest rates in the US and why it matters.

Alexis Crow, PhD | PwC

TIDAL PATTERNS

Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Martha S. Peyton and Caitlin Ritter | Aegon Asset Management

WORKPLACE VALUES

The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

Dags Chen, CFA | Barings Real Estate

OFFICE GAMES

Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

William Maher and Scot Bommarito | RCLCO

EMISSION CRITICAL

Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

Kevin Fagan, Xiaodi Li, and Natalie Ambrosio Preudhomme | Moody’s

MOVING TARGETS

A close-in look at twenty major US metros and thousands of properties shows how the overall impact of rising expense loads have narrowed NOI margins. Investors should take note.

Gleb Nechayev, CRE and Webster Hughes, PhD | Berkshire Residential Investments

SAND STATES

In the wake of the Great FinancialCrisis, certain metros in the Sand States suffered disproportionally. It may not be as bad this time.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

STORM WARNING

Not all storms are the same, and some are so tragic that they force a moment of universal recalibration. Hurricane Ian was one of those storms—but what does that mean for real estate?

Rajeev Ranade and Owen Woolcock | Climate Core Capital

PACIFIC THEATER

The Asia-Pacific region is already home to some of the world’s largest economies and now set to lead global economic growth. What’s moving the needle now for the APAC region?

Simon Treacy and Yu Jin Ow | CapitaLand Investment

STABLE SPACE

For e-commerce property investors, the past decade was outstanding, but even as market dynamics are slowing industrial’s momentum, market fundamentals remain sound.

Mehta Randhawa | JLL

—

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Our focus on delivering results is driven by our values, entrepreneurial spirit and our clients’ diverse needs. Together, our team specializes in holistic real assets solutions within and across five real assets investment categories, with a distinct approach to driving performance and long-term value.

CBRE Investment Management is a leading global real assets investment management firm with $143.9 billion in assets under management as of September 30, 2022, operating in more than 30 offices and 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

CBRE Investment Management is an independently operated affiliate of CBRE Group, Inc. (NYSE:CBRE), the world’s largest commercial real estate services and investment firm (based on 2021 revenue). CBRE has more than 105,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE Investment Management harnesses CBRE’s data and market insights, investment sourcing and other resources for the benefit of its clients. For more information, please visit cbreim.com.