Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

US office performance has lagged other property types and the overall NCREIF Property Index (NPI) in both total returns and net operating income (NOI) growth for the past twenty years. This overall trend, however, masks variations within the sector as office properties bifurcate between “have” and “have not.” Have-not properties struggle to maintain current values as NOI growth is weak (or negative) and required capital expenses detract from value, while “have” properties are able to grow NOI and increase values. Using NCREIF data, this article examines the bifurcation of office performance based on property age and market.1

THE OFFICE SECTOR

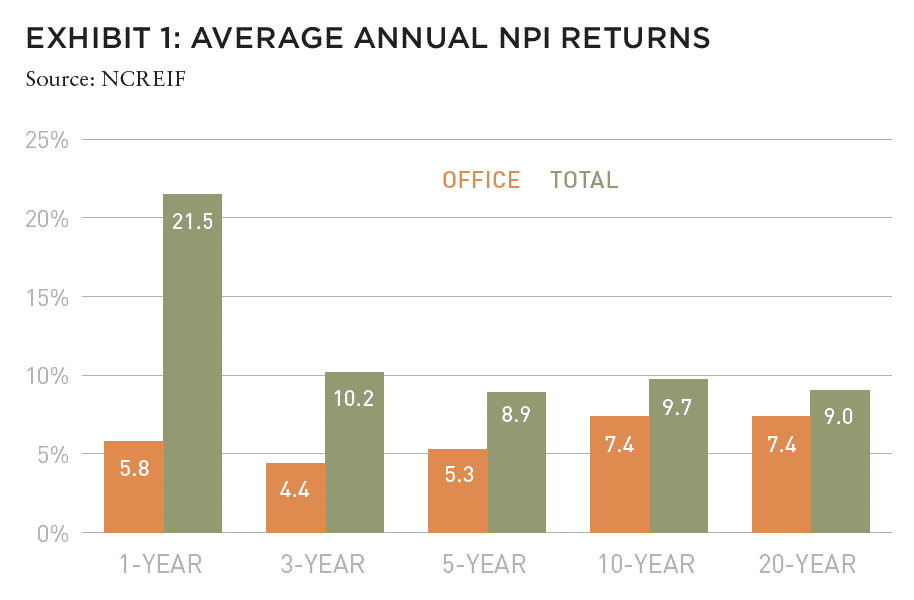

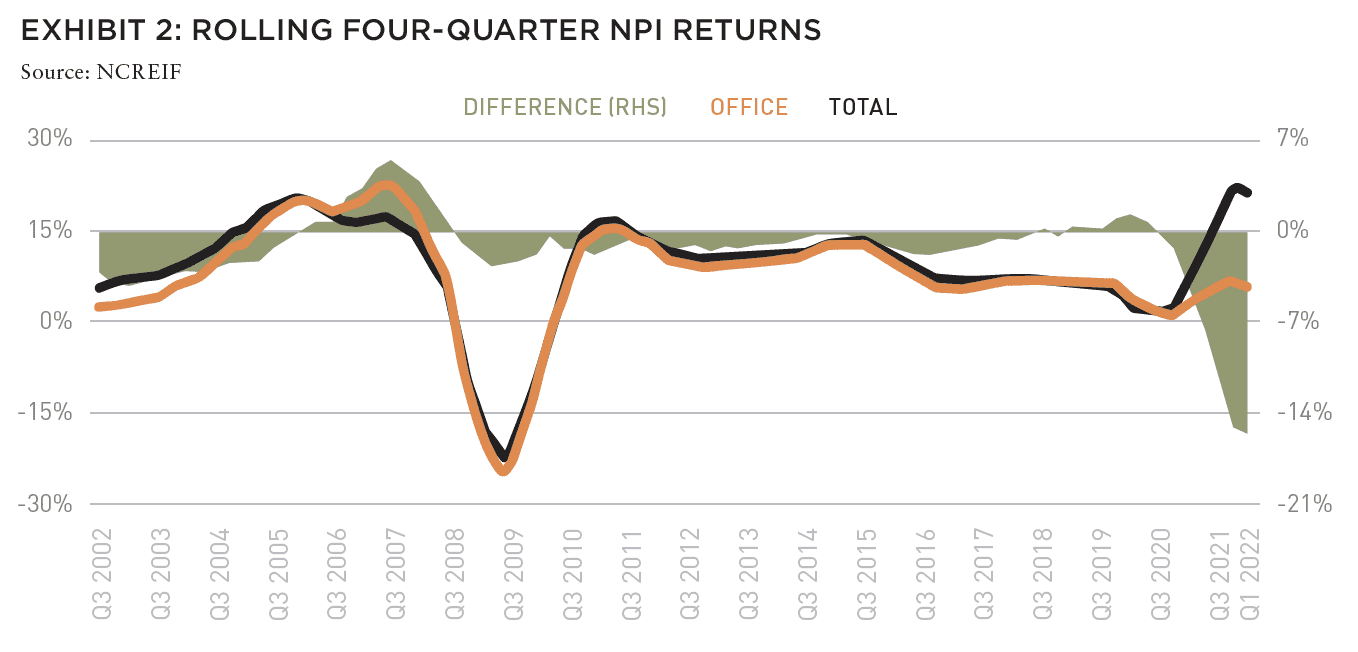

The US office sector has underperformed overall real estate over the last two decades, with returns averaging 7.4% annually, trailing total NPI returns by 160 BPS (Exhibit 1). There were brief periods of moderate out-performance just prior to the Global Financial Crisis and the COVID-19 pandemic, but office underperformed the overall index for most of the past twenty years (Exhibit 2). The margin of underperformance widened more recently.

Partly due to underperformance (as well as investor shifts to industrial and apartments), the office’s share of NPI declined precipitously over the past several years. Office’s market value in NPI continues to increase in absolute terms, but its share of total market value decreased to 27% in 2022 from 42% in 2000.

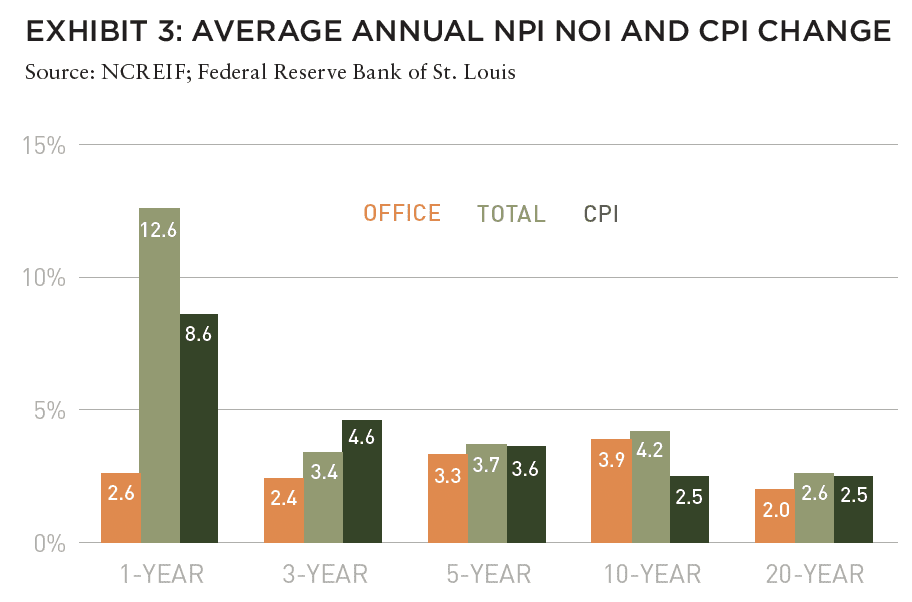

Recent industrial outperformance has been one contributing factor to office under-performance, but weak office NOI growth and elevated capital expenditures also dragged on office returns. Office NOI growth2 has averaged 2% annually over the past twenty years, trailing CPI inflation by 50 BPS and total NPI NOI growth by 60 BPS (Exhibit 3). Most recently, total NOI growth hit a twenty-year high, increasing 12.6% over the last year due in part to apartment and retail properties recovering from COVID-related declines. In contrast, office NOI grew only 2.6% over the past four quarters.

THE OFFICE SECTOR

Despite the poor performance of office as a whole, newer office properties (what we call Next Generation/NextGen properties) have materially outperformed the overall sector in terms of total returns and NOI growth. In addition to being newer (<10 years old), NextGen office caters to more recent work trends like the growing demand for collaborative and flexible office space, outdoor areas, and access to other lifestyle amenities like gyms and restaurants.

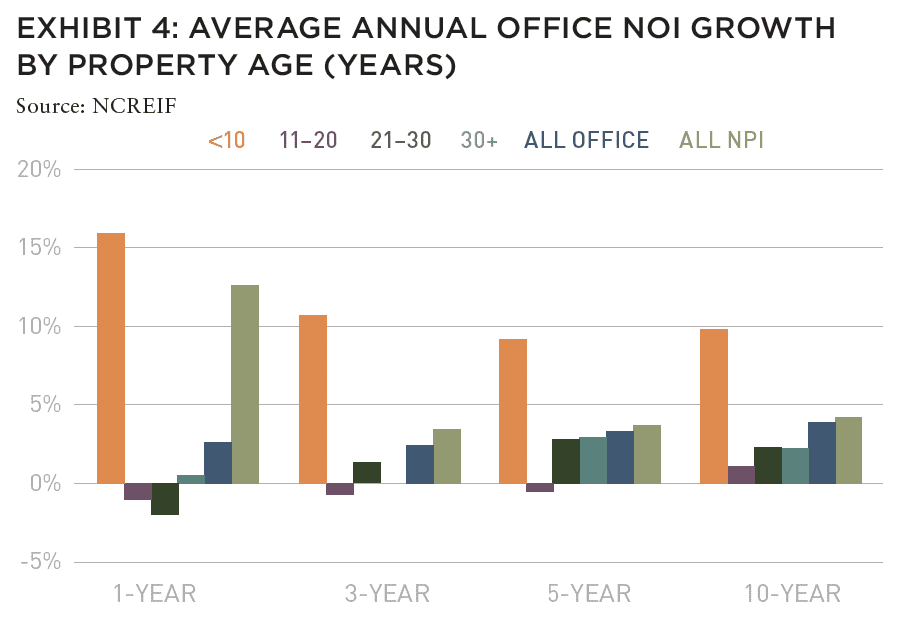

Based on NCREIF performance data, NextGen office has outperformed other office properties and, in some cases, the overall NCREIF universe, over the past ten years. NOI growth in recently built offices has outpaced growth in older office properties, averaging 9.2% annually over the last five years (Exhibit 4), nearly three times the average growth rate for all office and two and a half times total NPI NOI growth. However, as most of the US office stock is older, office buildings that are ten years old or less make up only 15% of NPI office market value (Exhibit 5), potentially placing a scarcity premium on these properties.

By market value, nearly 60% of NPI office is more than thirty years old, and t his older stock often suffers from muted demand because it lacks many of the modern amenities increasingly desired by office tenants. Notably, office buildings between eleven and twenty years old have seen the lowest NOI growth over most time horizons with average annual NOI growth of -0.5% over the past five years and 1.1% over the past ten years. This is possibly due to significant tenant turnover during that time frame as initial leases expire.

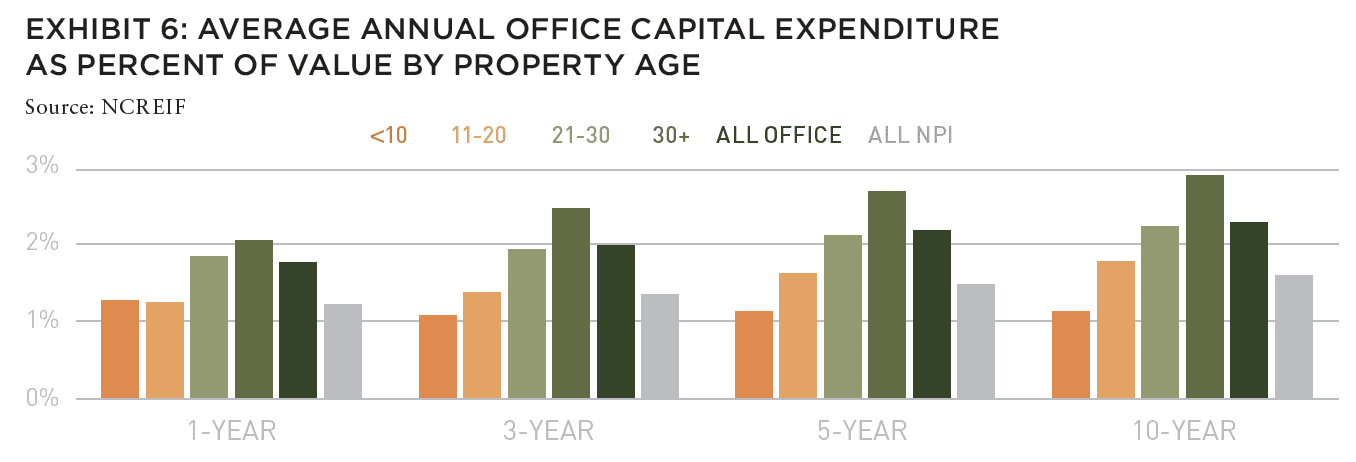

In addition to weak NOI growth, older offices have elevated capital expenditures (Exhibit 6). NPI office as a whole averaged annual capital expenditures at 2.2% of market value over the last five years, the highest of the four main property types and well above the total NPI average of 1.5%. Offices older than thirty years old recorded even higher capex, averaging 2.7% of market value. Conversely, newly built office capital expenditures have been around 1.1% of value over the past five years, below the total NPI average.

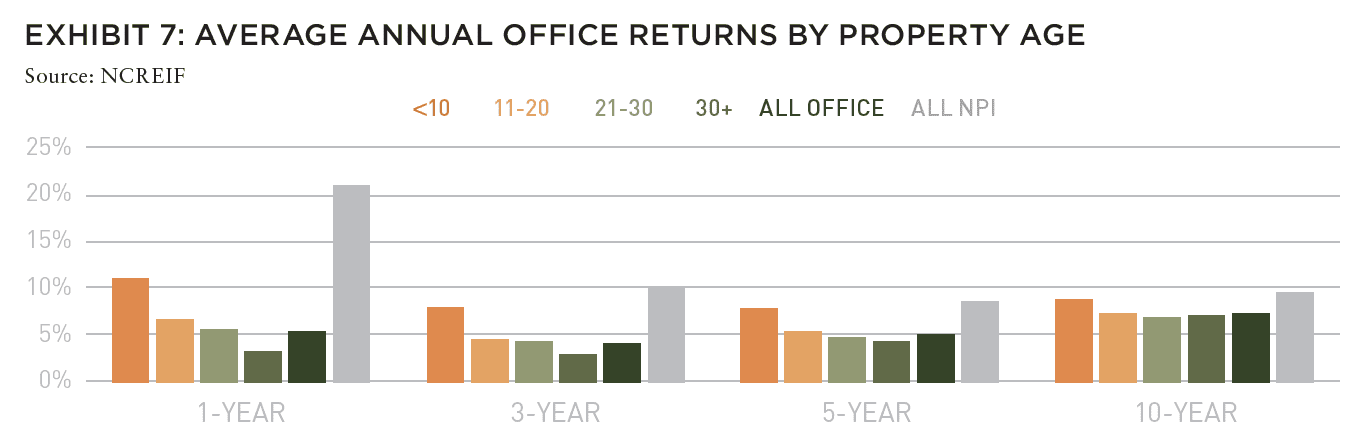

Taken together, weak NOI growth and high capex have led to low returns, particularly for older office product (Exhibit 7). Newer office has outperformed older office but has fallen short of total NCREIF Property Index (NPI) returns in both the short and medium term. Over the four quarters ending in 2Q 2022, total NPI grew to record highs, posting a 21% return. The total return of office properties in the NPI remained far more modest at just 5.3%, but returns for newly built office were over double that figure at 11%. Apartments and industrial both outperformed new office in the recent real estate rally with trailing one-year returns of 24.4% and 47.7%, respectively. Over the longer term, newer office properties have out-performed older buildings, with a ten-year return of 8.7%, but have lagged the overall NPI, which delivered a 9.5% average annual return.

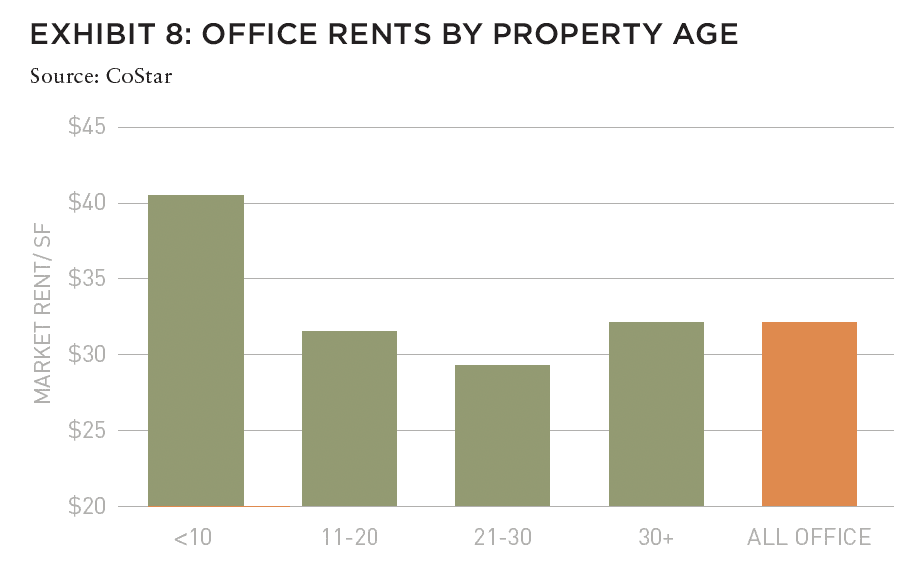

New office buildings charge premium rents and are forecasted to see marginally stronger rent growth than older offices over the next five years (Exhibit 8). Nationally, market rents average approximately $40/SF in offices 10 years old or newer, 25% above all office average rents. According to CoStar, newer office rents are also projected to grow 1.6% annually over the next five years, surpassing all office average rent growth by 40 BPS. Elevated rents and faster rent growth will in turn drive continued NOI growth and ultimately returns.

EXPLORE THE LATEST ISSUE

MAKE SUSTAINABILITY REAL

With the case for sustainability already well-established, how can (and should) real estate continue to lead?

Gunnar Branson | AFIRE

RETURN GENERATION POTENTIAL

In addition to offering inflation protection and lower volatility, real estate also offers something that other asset classes can’t: the opportunity to invest in tangible, positive change.

Shane Taylor | CBRE Investment Management

CATCH A FALLING *R

The future path of long-term interest rates in the US and why it matters.

Alexis Crow, PhD | PwC

TIDAL PATTERNS

Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Martha S. Peyton and Caitlin Ritter | Aegon Asset Management

WORKPLACE VALUES

The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

Dags Chen, CFA | Barings Real Estate

OFFICE GAMES

Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

William Maher and Scot Bommarito | RCLCO

EMISSION CRITICAL

Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

Kevin Fagan, Xiaodi Li, and Natalie Ambrosio Preudhomme | Moody’s

MOVING TARGETS

A close-in look at twenty major US metros and thousands of properties shows how the overall impact of rising expense loads have narrowed NOI margins. Investors should take note.

Gleb Nechayev, CRE and Webster Hughes, PhD | Berkshire Residential Investments

SAND STATES

In the wake of the Great FinancialCrisis, certain metros in the Sand States suffered disproportionally. It may not be as bad this time.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

STORM WARNING

Not all storms are the same, and some are so tragic that they force a moment of universal recalibration. Hurricane Ian was one of those storms—but what does that mean for real estate?

Rajeev Ranade and Owen Woolcock | Climate Core Capital

PACIFIC THEATER

The Asia-Pacific region is already home to some of the world’s largest economies and now set to lead global economic growth. What’s moving the needle now for the APAC region?

Simon Treacy and Yu Jin Ow | CapitaLand Investment

STABLE SPACE

For e-commerce property investors, the past decade was outstanding, but even as market dynamics are slowing industrial’s momentum, market fundamentals remain sound.

Mehta Randhawa | JLL

OFFICE PERFORMANCE BY MARKET

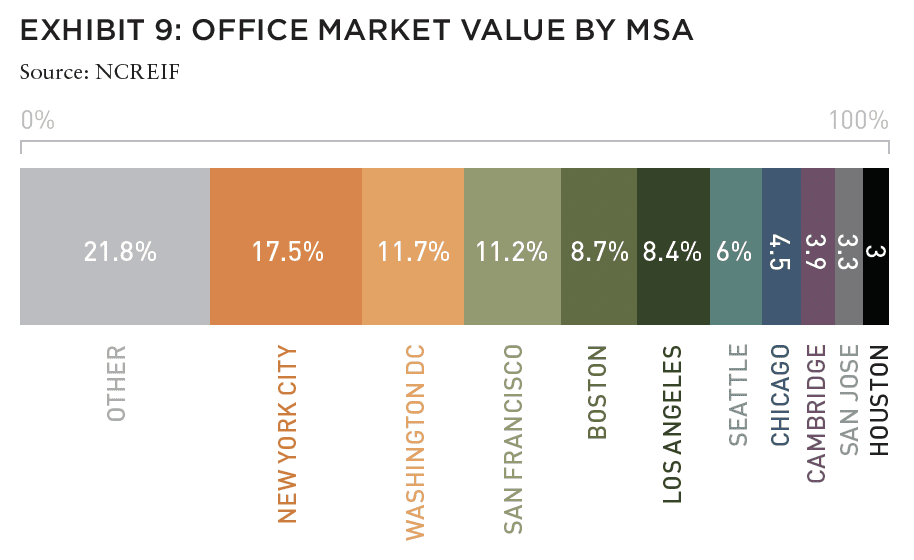

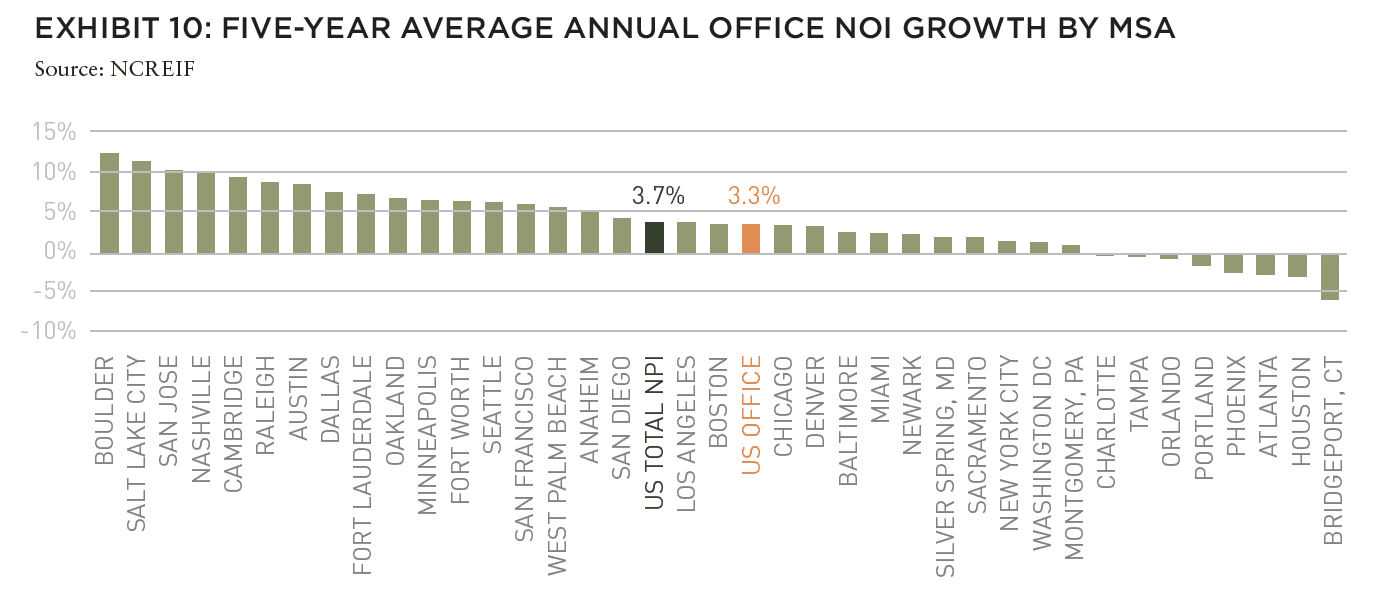

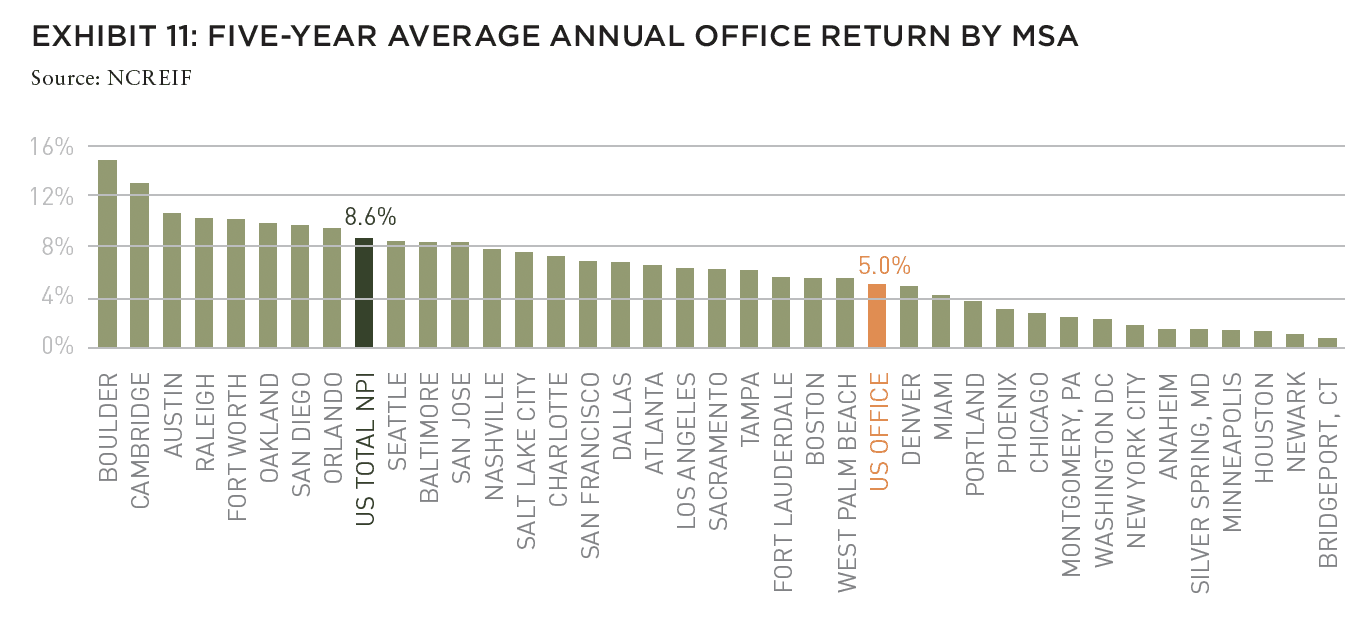

In addition to age of building, office performance also varies widely by market. Nearly three-quarters of NPI office market value is concentrated in the traditional gateway markets (Exhibit 9). The two largest markets—New York City and Washington, DC—have performed poorly over the last five years with low NOI growth (Exhibit 10) and total returns (Exhibit 11). Despite making up 29% of office market value, they have driven just 10% of NPI office’s NOI growth and 11% of total returns over the last five years. Other large markets—notably San Francisco, San Jose, Los Angeles, and Cambridge—have performed better. Cambridge, San Jose, and Oakland collectively constitute 9% of NPI office market value, but over the last five years, these markets drove 22% of office NOI growth and 18% of total returns.

Many of the top performing office MSAs are “quality of life” markets with robust life science and tech sectors. Office NOI growth has been strongest in large life science markets such as Cambridge and the San Francisco Bay Area, and in smaller but growing life science markets, such as Boulder and Raleigh. The same trend holds for total office returns. Cambridge, a major biotech hub, is the largest office market to earn outsized five-year average returns, outperforming total NPI by 440 BPS. Several smaller office markets with active life science sectors also outperformed the NPI: notably Boulder, Raleigh, and San Diego.

The strong performance of life science markets is not surprising. Both scientific breakthroughs and venture capital activity has favored life science/biotech companies. Most biotech work requires access to physical lab and office space, supporting office demand and shielding the sector from “work from anywhere” trends. Office in several biotech markets has outperformed total NPI over the last five years, suggesting that life science office may be an attractive investment opportunity within the broader office sector.

INVESTMENT IMPLICATIONS

Over the last two decades (or longer), the office sector has consistently lagged total NPI on both total returns and NOI growth. Investors have taken note, and office’s share of NPI market value has steadily declined while apartment and industrial shares have grown.

Within the office sector, the story is not unequivocally negative.

Strong NOI growth has driven higher returns for NextGen office properties built within the last ten years. In contrast, NOI growth and total returns at older office properties (particularly 11- to 20-year-old buildings) have been much lower (and at times negative).

While newer office buildings have outperformed older ones in total returns, they have underperformed the overall NPI. Office has also performed better in markets with strong tech and life science activity. Cambridge and the San Francisco Bay Area are two notable examples.

While a preponderance of older buildings will likely lead to underperformance for office as a whole for the foreseeable future, newly built offices and spaces in tech and life science markets have shown more favorable signs however, they must be evaluated relative to other property types.

These office subsectors may not prove to be diamonds, but they certainly seem to merit a closer look by investors.

—

ABOUT THE AUTHORS

William Maher is Director of Strategy and Research and Scot Bommarito is Senior Research Associate for RCLCO Fund Advisors (RFA). RFA is an affiliate of RCLCO (formerly Robert Charles Lesser & Co.), which has been the “first call” for real estate developers, investors, the public sector, and non-real estate companies and organizations seeking strategic and tactical advice regarding property investment, planning, and development since 1967.

—

NOTES

1. All NCREIF data are as of 2022 Q2.

2. Based on NCREIF’s Same Property methodology.

—

REVIEWER RESPONSE

The authors succinctly reemphasize what many of us have become acutely aware of in the wake of the pandemic: the deepening bifurcation between winners and losers in the office sector, using the dual lenses of property vintage and market to quantify this gap. As the data clearly shows, older buildings have increasingly fallen out of favor for the same reasons things always fall out of favor—tastes shift, new offerings evolve to meet the market, and laggards without vision (and a nice stockpile of capital to afford reinvention) get left behind as relics of a former time.

While the piece does its best to highlight bright spots in an otherwise dimly lit sector, even this does little to instill confidence in the relative upside for even those fewer newer assets, because “[though] newer office has outperformed older office, [it] has fallen short of total NCREIF Property Index (NPI) returns in both the short and medium term.”

What may have been additive for investors and owners of office would have been for the authors to dig one layer further into this newer subset of buildings and determine if, beyond vintage, there are other qualities or characteristics that create the potential for upper-quintile performance in this top-of-class subset. In an environment where work-from-home and hybrid arrangements are already chipping away at the net demand picture and a potential recession threatens to knock demand further off course, using vintage as a starting point is exactly that: just the starting point.

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Our focus on delivering results is driven by our values, entrepreneurial spirit and our clients’ diverse needs. Together, our team specializes in holistic real assets solutions within and across five real assets investment categories, with a distinct approach to driving performance and long-term value.

CBRE Investment Management is a leading global real assets investment management firm with $143.9 billion in assets under management as of September 30, 2022, operating in more than 30 offices and 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

CBRE Investment Management is an independently operated affiliate of CBRE Group, Inc. (NYSE:CBRE), the world’s largest commercial real estate services and investment firm (based on 2021 revenue). CBRE has more than 105,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE Investment Management harnesses CBRE’s data and market insights, investment sourcing and other resources for the benefit of its clients. For more information, please visit cbreim.com.