In addition to potentially offering inflation protection and lower return volatility, real estate may also help bring about tangible positive change and help solve some critical problems.

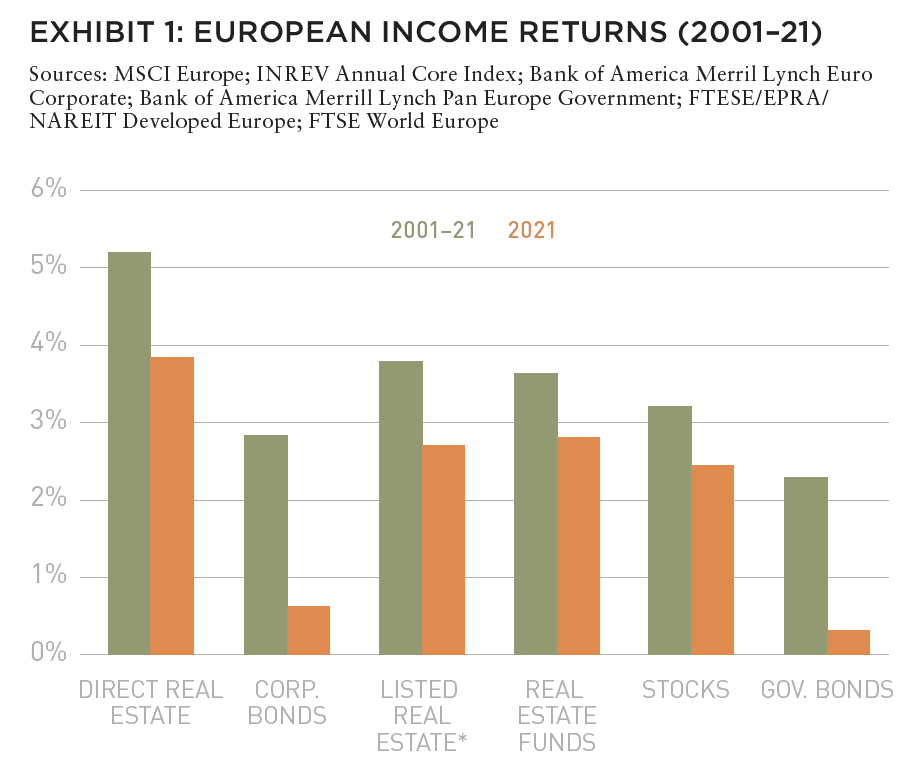

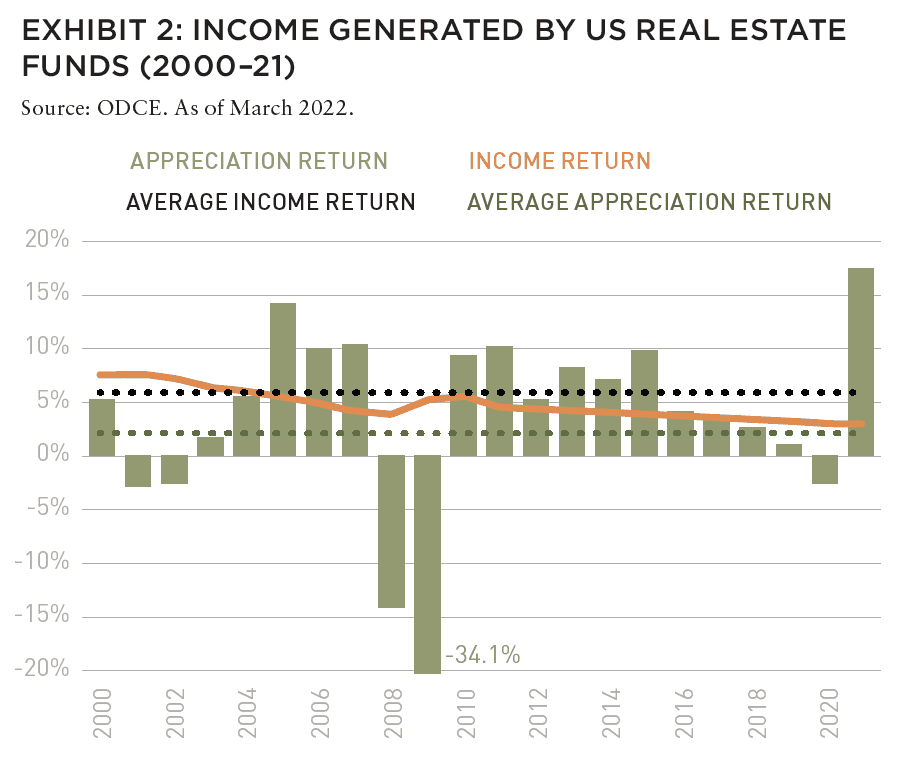

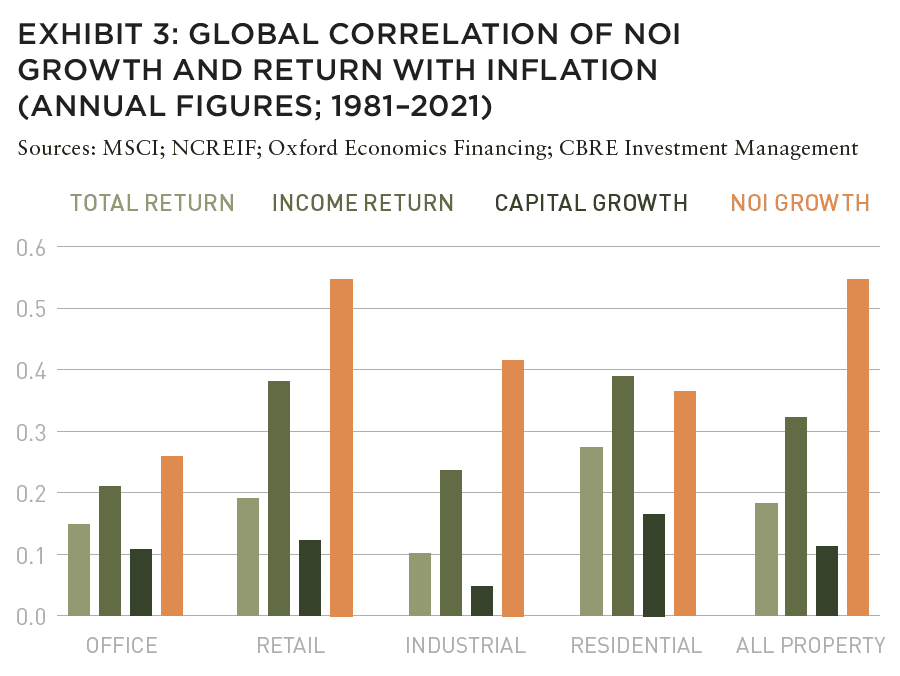

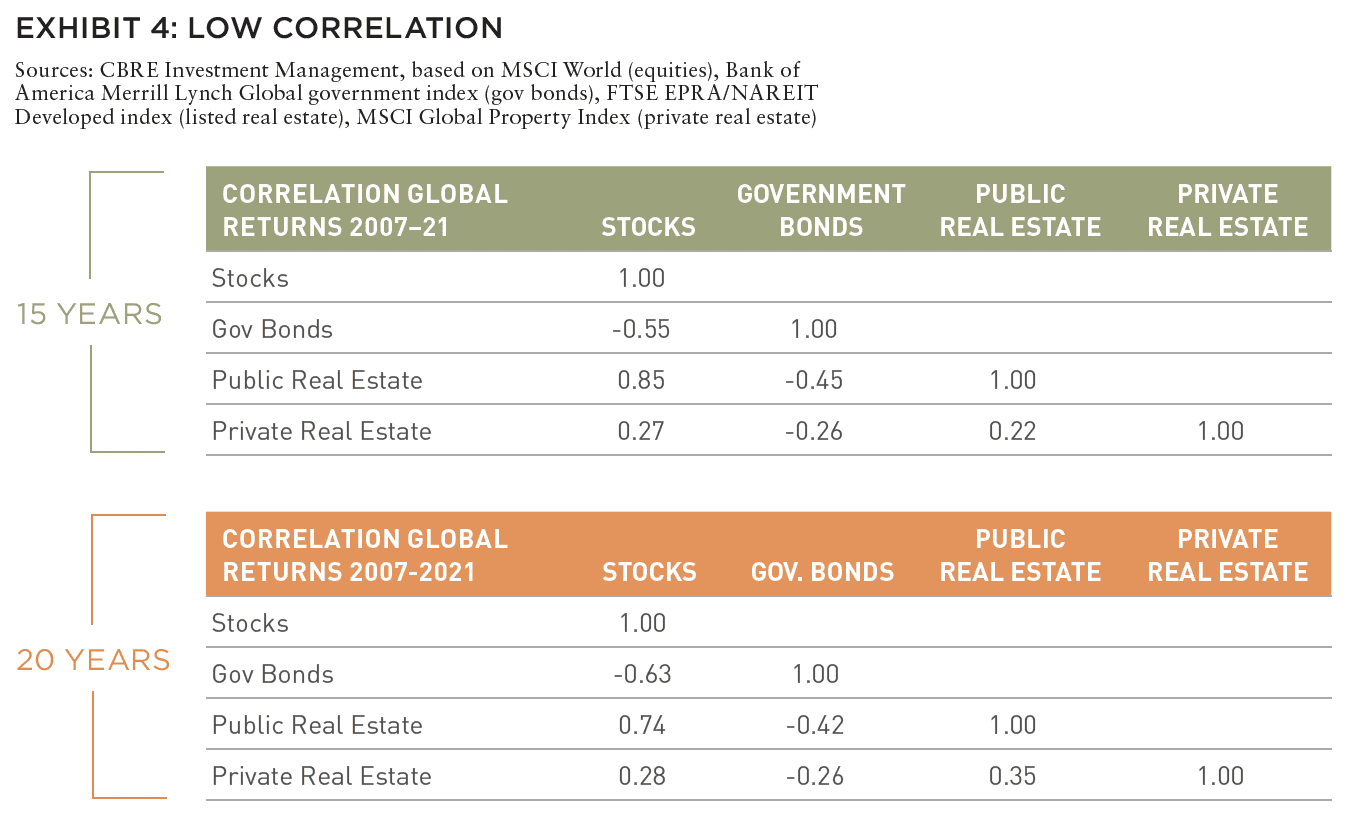

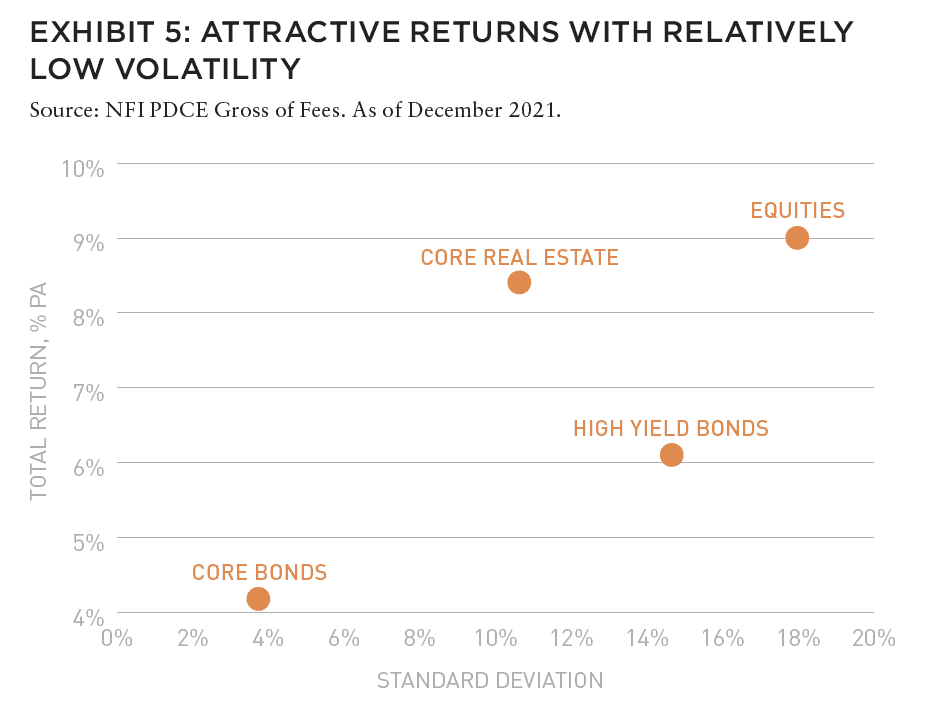

When it comes to generating attractive risk-adjusted returns, real estate has demonstrated its worth over the long run. It can deliver relatively stable income, some inflation protection, and generally lower volatility and diversification benefits—even through and beyond the pandemic—real estate also offers something that other asset classes can’t easily replicate: the opportunity to invest in tangible positive change.

The buildings in which we live, work, heal, learn, and play in all have an environmental and social footprint. Through action on the ground, this footprint can be minimized and, in some cases, turned into a positive. Whether it is constructing affordable and sustainable housing, deploying solar panels on roofs to generate energy, assist with supply chain blockages or ensuring the energy efficiency of new and existing stock, real estate can help solve some of the world’s most pressing issues.

And investing in problem-solving real estate can make financial sense, too. Buildings with strong sustainability credentials can be more likely to be sought after by occupiers and less likely to be left vacant. They also have the potential to generate enhanced returns thanks to having been constructed to higher specifications. And because investments can be channeled into areas that are truly in demand, they are potentially more cycle-resistant.

When it comes to real estate, generating attractive returns and solving problems are not mutually exclusive.

REAL ESTATE: INVESTMENT THESIS

Investors seeking high, sustainable income, inflation protection, low correlation to other asset classes, and attractive returns at relatively low volatility—for those investors seeking any of these attributes, real estate may provide a solution.

In addition to generating attractive risk-adjusted returns to meet investors’ traditional fiduciary requirements, real estate may also help mitigate economic and societal problems.

SUPPLY CHAINS

PROBLEM: STRETCHED AND VULNERABLE SUPPLY CHAINS

The vulnerabilities of supply chains based around just-in-time strategies have been bubbling up in the background for some time: bottlenecks, lack of security of supplies, environmental footprint.

The onset of the COVID-19 pandemic, heightened geopolitical tensions, and the cost of energy crises have all brought these to the foreground, triggering a re-evaluation of supply chain models. This rethink is increasingly involving a switch away from “just-in-time” to “just-in-case” strategies centered around holding higher levels of stock and inventory.

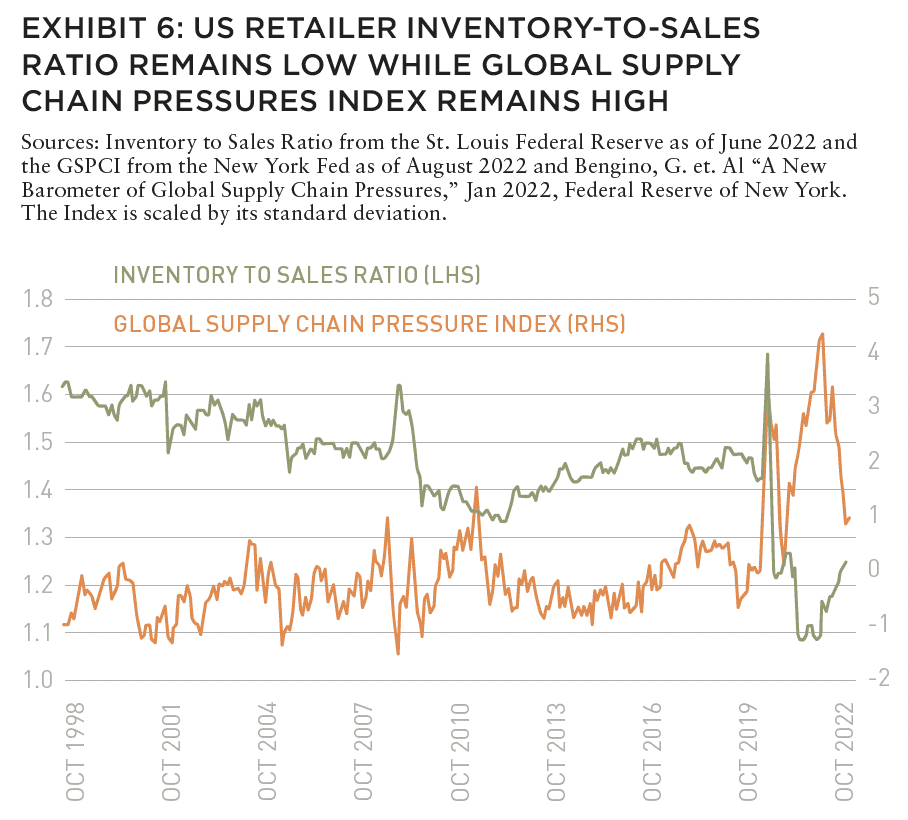

US retailers have been struggling to rebuild inventory back to long term average levels let alone build the excess inventory or safety stock they would like to have as part of this new just-in-case supply chain model.

Yet they have also been contending with a global supply chain pressures index well above (1 to 4 standard deviations above the long-term average) normal. The confluence of these two factors help to explain why recent years have seen such fierce competition among occupiers for quality, well-located space.

Holding more inventory mitigates the risk of running short on stock. It also helps to retain customer loyalty and can act as a hedge against future price rises and higher transportation costs. For example, according to Drewry Supply Chain Advisors and the Cass Freight Index, the cost to ship goods via ocean freight jumped by more than 200% in 2021, while the cost for domestic freight rose over 40%.1

SOLUTION: MODERN LOGISTICS FACILITIES

The modern logistics sector is central to reconfiguring supply chains and weathering today’s high inflation environment. Transportation costs make up 40–70% of a company’s total logistics spend. By contrast, fixed facility costs (including rent) account for only 3–6%.2 Modern logistics facilities therefore offer a cost-effective route to reducing transportation costs as well as protection against future supply chain disruption.

FINANCIAL SENSE CHECK: INVESTING IN MODERN LOGISTICS FACILITIES

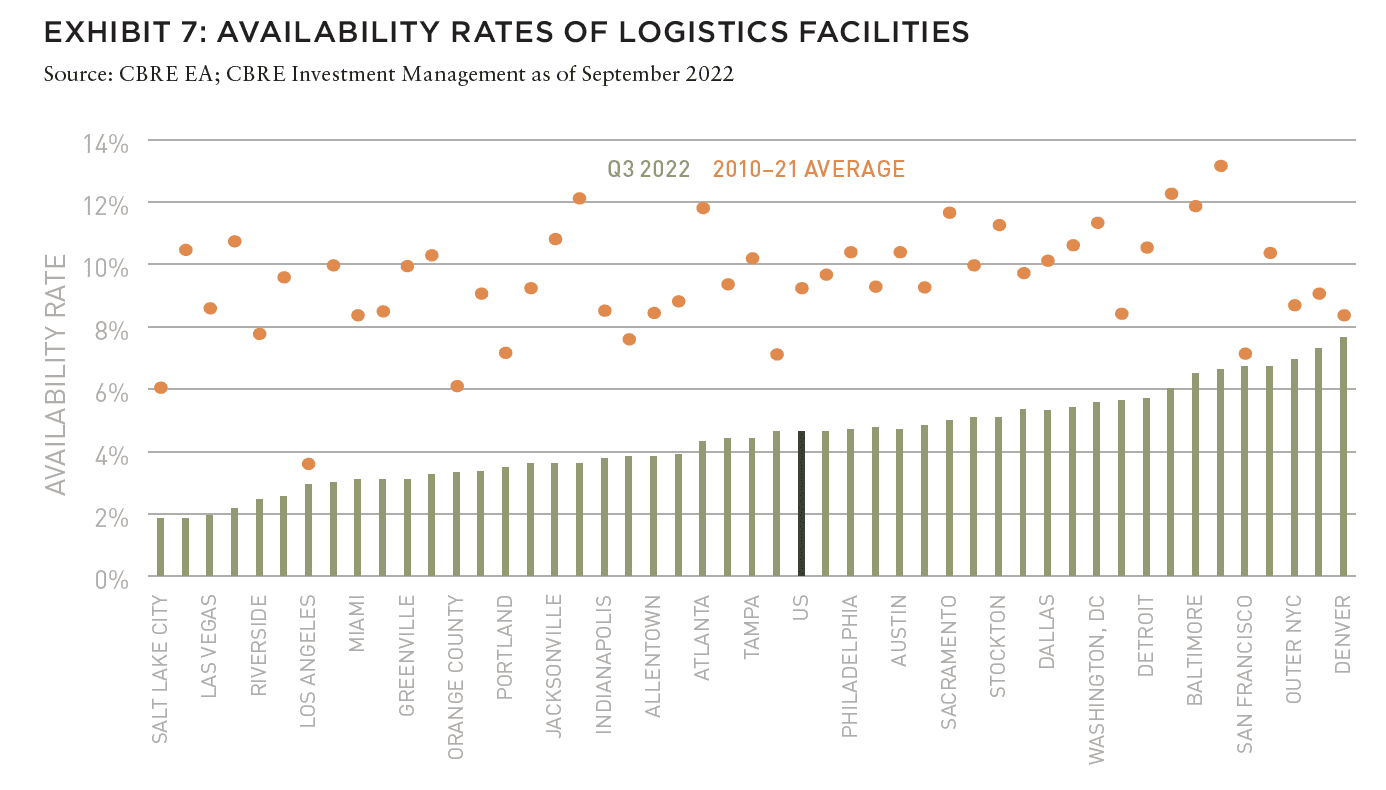

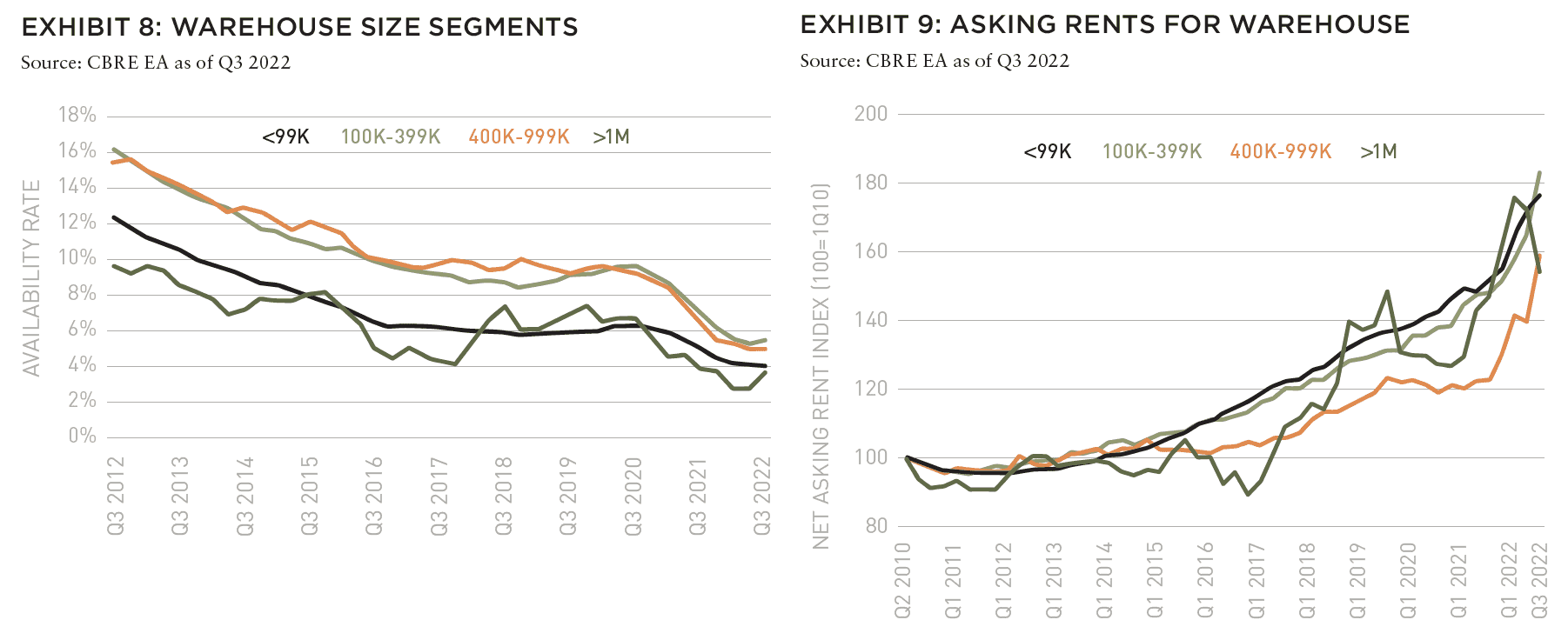

Thanks to favorable supply/demand dynamics, specifically supply struggling to keep pace with demand that is being driven by long-term structural trends, such as e-commerce and supply chain reconfiguration, availability rates are at record-lows across most major US markets (Exhibit 7) and warehouse size segments (Exhibit 8). And thanks to long-term structural drivers, further rental growth is expected.

EXPLORE THE LATEST ISSUE

MAKE SUSTAINABILITY REAL

With the case for sustainability already well-established, how can (and should) real estate continue to lead?

Gunnar Branson | AFIRE

RETURN GENERATION POTENTIAL

In addition to offering inflation protection and lower volatility, real estate also offers something that other asset classes can’t: the opportunity to invest in tangible, positive change.

Shane Taylor | CBRE Investment Management

CATCH A FALLING *R

The future path of long-term interest rates in the US and why it matters.

Alexis Crow, PhD | PwC

TIDAL PATTERNS

Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Martha S. Peyton and Caitlin Ritter | Aegon Asset Management

WORKPLACE VALUES

The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

Dags Chen, CFA | Barings Real Estate

OFFICE GAMES

Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

William Maher and Scot Bommarito | RCLCO

EMISSION CRITICAL

Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

Kevin Fagan, Xiaodi Li, and Natalie Ambrosio Preudhomme | Moody’s

MOVING TARGETS

A close-in look at twenty major US metros and thousands of properties shows how the overall impact of rising expense loads have narrowed NOI margins. Investors should take note.

Gleb Nechayev, CRE and Webster Hughes, PhD | Berkshire Residential Investments

SAND STATES

In the wake of the Great FinancialCrisis, certain metros in the Sand States suffered disproportionally. It may not be as bad this time.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

STORM WARNING

Not all storms are the same, and some are so tragic that they force a moment of universal recalibration. Hurricane Ian was one of those storms—but what does that mean for real estate?

Rajeev Ranade and Owen Woolcock | Climate Core Capital

PACIFIC THEATER

The Asia-Pacific region is already home to some of the world’s largest economies and now set to lead global economic growth. What’s moving the needle now for the APAC region?

Simon Treacy and Yu Jin Ow | CapitaLand Investment

STABLE SPACE

For e-commerce property investors, the past decade was outstanding, but even as market dynamics are slowing industrial’s momentum, market fundamentals remain sound.

Mehta Randhawa | JLL

AFFORDABLE HOUSING

PROBLEM: LACK OF AFFORDABLE AND SUSTAINABLE HOUSING

Today’s cost of living crisis and rising interest rates are exacerbating a pre-existing problem: a chronic lack of affordable and sustainable homes.

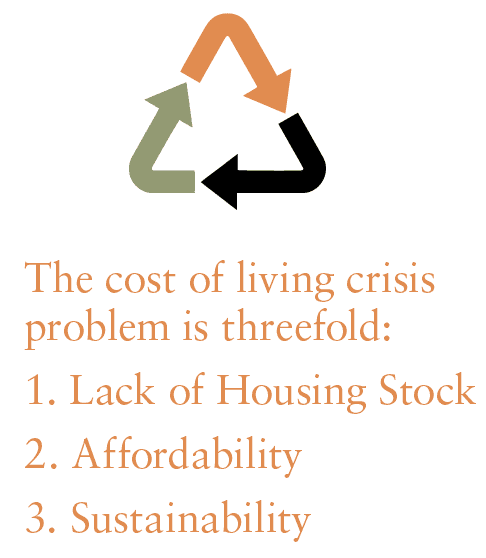

The problem is threefold: a lack of housing stock given the populations it is to serve; this drives up rents and has created an affordability challenge; meanwhile, much housing stock is in need of refurbishment and upgrade, especially given temperature volatility and climate change.

Harvard University’s “The State of the Nation’s Housing 2022” report quotes the Federal Home Loan Mortgage Corporation’s (Freddie Mac) estimate of a 3.8 million shortfall in market-rate housing both for sale and for rent in the US.3 In the UK, the House of Commons’ February 2022 Research Briefing “Tackling the Under-Supply of Housing in England” estimates “around 340,000 new homes need to be supplied in England each year, of which 145,000 should be affordable.”4

The US and UK may be among the largest investable housing markets globally but in fact are fact from the least affordable. Demographia’s 2022 report finds Hong Kong, China, and several cities in Australia, New Zealand, and Canada among the least affordable globally. The Harvard Report found that in the US in 2020, the nationwide share of cost-burdened households (that is, those paying more than 30 percent of their incomes for housing) stood at 30 percent. Moreover, 14 percent of all households were severely burdened (spending more than half their incomes on housing). Renter households were particularly hard-pressed, with 46 percent at least moderately burdened and 24 percent severely burdened. In the UK, the Hamptons Monthly Lettings Index estimates that, following record rental growth in 2021, tenants spent an average of 42% of their post-tax income on rent. The figure rises to 48% for those renting in London.5

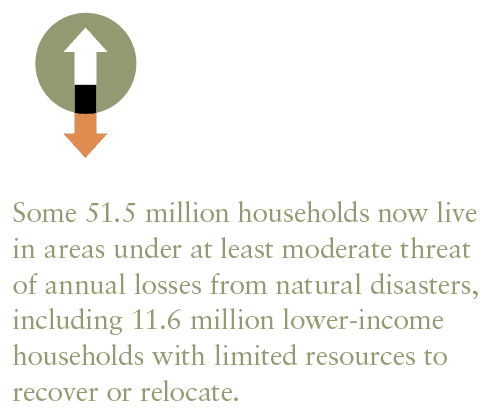

Much affordable housing stock is in need of upgrading and retrofitting. The Harvard report called for urgent upgrades to existing stock as too much of it is simply “not equipped to meet the accessibility needs of an aging population or to withstand the impacts of climate change.” The report goes on to quantify the climate change issue in terms of household numbers: “The […] immediate, large-scale challenge is to improve the resiliency of the existing stock and to mitigate the risks of future damage from extreme weather-related events. Some 51.5 million households now live in areas under at least moderate threat of annual losses from natural disasters, including 11.6 million lower-income households with limited resources to recover or relocate.”

WHY THE LACK OF SUPPLY?

Labor shortages, restrictive local land use regulations have long been factors which have challenged the production of new and affordable housing stock in many markets. During and since the pandemic, labor shortages became even more acute and additionally supply chain delays for many construction materials and spiraling costs added to these challenges.

In the UK, the House of Commons Report similarly found that the planning system is central to the failure to build enough homes, particularly where housing need is at its most severe. Other barriers include policies that enable affordable homes to be purchased by private individuals (right to buy).

SOLUTION: AFFORDABLE HOUSING FUNDS

Real estate funds focused on affordable housing offer a solution that not only increases the level of affordable stock, but also improves quality of life for people either by updating properties or by building sustainable homes. By channeling institutional client capital, funds can help plug the funding gap. Importantly, these funds continue to target the attractive returns investors expect from real estate. They also help satisfy the growing need for institutions to demonstrate the impact their respective investment strategies are having on society.

FINANCIAL SENSE CHECK: INVESTING IN AFFORDABLE HOUSING FUNDS

By providing fit-for-purpose accommodation that has been designed or upgraded with the environment and quality of life in mind, tenants are less likely to leave, more likely to look after their homes, and more inclined to recommend the development to others. These can all lead to lower maintenance costs, lower bad debts, lower void costs, and lower vacancy rates—all of which, in turn, can positively impact exit yields.

CLIMATE CHANGE

PROBLEM: CLIMATE CHANGE

The World Green Building Council (WGBC) Global Status Report 2017 states that buildings and construction together account for 36% of global final energy use (and a higher 39% of energy-related CO2 emissions when upstream power generation is included). Additionally the WGBC found that energy intensity per square meter needs to improve on average by 30% by 2030 (compared to 2015) to be on track to meet global climate ambitions set out in the Paris Agreement.6

SOLUTION: INVESTING IN NET-ZERO–ALIGNED REAL ESTATE

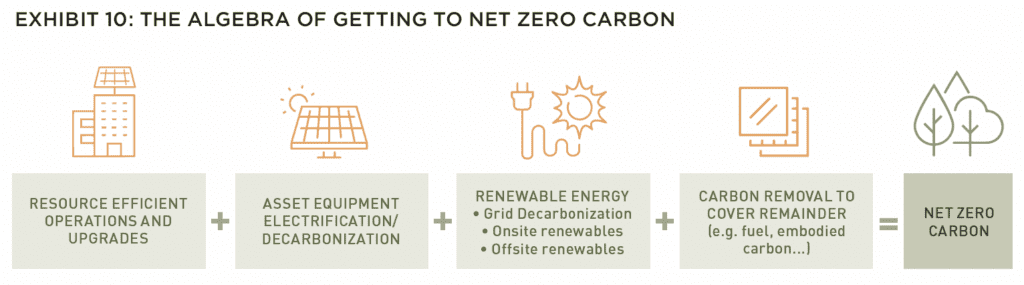

By addressing climate-related risks and opportunities and by focusing on delivering resiliency and net zero carbon performance, it is possible for real estate to switch from being a part of the problem to being a part of the solution.

Real estate has many levers that it can pull to help attain net zero carbon:

• Undertaking retrofits on existing buildings to make them energy efficient

• Deploying onsite renewable energy to generate power for the site and wider community

• Carrying out the electrification of sites including the installation of battery storage and electric-vehicle charging systems

• Increasing the use of more environmentally friendly materials

• Implementing green financing programs to fund projects targeting a reduction in the carbon footprint of buildings

FINANCIAL SENSE CHECK: INVESTING IN NET-ZERO–ALIGNED REAL ESTATE

Properties that do not have strong sustainability credentials are at risk of becoming stranded assets. According to the Carbon Risk Real Estate Monitor, “properties that will be exposed to the risk of early economic obsolescence due to climate change because they will not meet future regulatory efficiency standards or market expectations.”7

Upgrading existing buildings/constructing new properties that meet high sustainability thresholds is therefore an exercise in risk management. It can also add value. Buildings with their own energy source can generate savings and, in certain instances, additional sources of income. The asset may also be more attractive to occupiers looking to reduce their own carbon footprints, thereby minimizing vacancies which, in turn, can help with exit yields.

Research carried out on the relationship between certification from GRESB, an independent organization providing validated ESG performance data and peer benchmarks, and real estate fund returns show that strong GRESB performance correlates to enhanced returns for non-listed funds: overall, a 3% uplift was observed between the lowest and highest GRESB scoring funds.8

TALENT

PROBLEM: SKILLS SHORTAGE

According to the 2022 Global Talent Shortage Survey carried out by Fortune 500 company, Manpower Group, “[Three in four] employers report difficulty in finding the talent they need.” The survey involved more than 40,000 employers from a broad range of industries in 40 countries and territories.9 The reasons behind the skills shortage range from lack of adequate training to more people leaving the workforce – the US Bureau of Labor Statistics estimates that in December 2021, over 4.3 million workers voluntarily left their jobs.10

PROBLEM: BUILDING ECOSYSTEMS AROUND DEVELOPMENTS

By linking developments to education and training, an ecosystem can be fostered that benefits both the communities they serve as well as prospective occupiers. This can be achieved via the establishment of educational funds that invest in the teaching and training of skills relevant to the development.

FINANCIAL SENSE CHECK: BUILDING ECOSYSTEMS AROUND DEVELOPMENTS

Firstly, investing in the education and training of the local community can help projects get through the planning and funding stages.

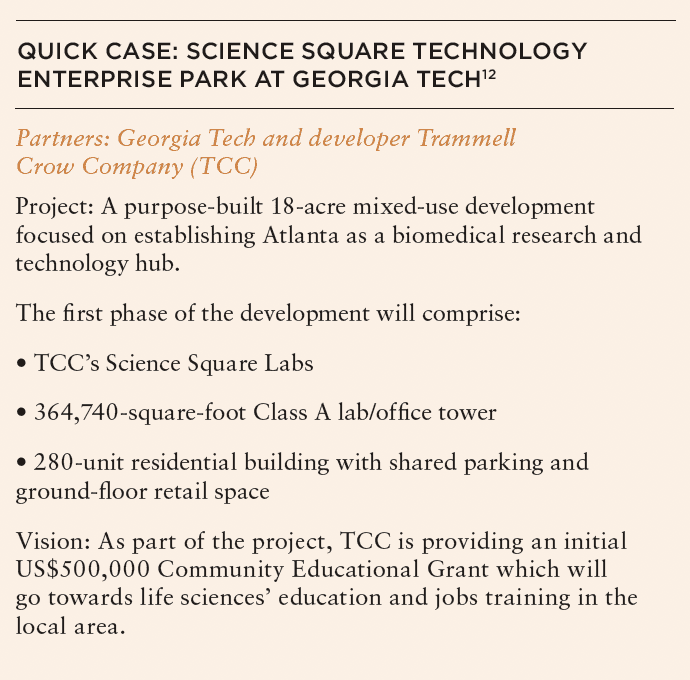

It can also enhance the attractiveness of an asset. An educational fund, as in the Science Square Technology Enterprise Park, can establish a virtuous loop: people have the opportunity to train up and raise their income potential; developers/landlords foster an ecosystem centered around the asset; a local workforce skilled in a specialist sector helps attract further investment into the ecosystem; more employment opportunities are generated; and people can continue to train up and raise their income potential, beginning the loop again.

RETHINKING REAL ESTATE AS AN ASSET CLASS

In summary, real estate is a unique asset class that not only generates attractive risk-adjusted returns but also provides investors with the opportunity to put their money to work to help solve some of the world’s most pressing societal and environmental issues.

Crucially, there doesn’t have to be a trade-off between investing for positive change and generating attractive returns. The opposite can be true. Investing for good can help future-proof assets and increase sustainability of income. This, in turn, can enhance returns for investors.

With real estate, it is possible to invest in assets that not only benefit investors, but the actual people, places, and communities where we live, work, and play.

—

ABOUT THE AUTHOR

Shane Taylor is Americas and APAC Head of Research for CBRE Investment Management, a leading global real assets investment management firm.

—

NOTES

1. “Cass Transportation Index Report: August 2021.” Cass Information Systems, Inc. Accessed December 8, 2022. cassinfo.com/freight-audit-payment/cass-transportation-indexes/august-2021.

2. “Supply Chain Advisory.” CBRE. Accessed December 6, 2022. cbre.us/real-

estate-services/real-estate-industries/industrial-and-logistics/supply-chain-advisory.

3. “The State of the Nation’s Housing 2022.” Joint Center for Housing Studies of Harvard University. Accessed December 6, 2022. jchs.harvard.edu/sites/default/files/reports/files/Harvard_JCHS_State_Nations_Housing_2022.pdf.

4. Barton, Cassie, Wendy Wilson, and Lorna Booth. “Tackling the Undersupply of Housing in England.” UK Parliament House of Commons Library, February 2022. commonslibrary.parliament.uk/research-briefings/cbp-7671/.

5. “Lettings.” Hamptons, April 2022. hamptons.co.uk/research/reports/market-insight-spring-2022/lettings#/.

6. “Global Status Report 2017.” World Green Building Council, March 21, 2022. https://worldgbc.org/article/global-status-report-2017/.

7. “Carbon Risk Real Estate Monitor,” Accessed December 8, 2022. crrem.org/wp-content/uploads/2019/09/CRREM-Stranding-Risk-Carbon-Science-based-decarbonising-of-the-EU-commercial-real-estate-sector.pdf.

8. Wheeler, Sam. “The Business Case for ESG in Real Estate.” GRESB, February 20, 2019. gresb.com/nl-en/the-business-case-for-esg-in-real-estate/.

9. ManpowerGroup. The 2022 Global Talent Shortage. ManpowerGroup. Accessed December 6, 2022. go.manpowergroup.com/hubfs/Talent%20Shortage%202022/MPG-Talent-Shortage-Infographic-2022.pdf.

10. Smet, Aaron De, Bonnie Dowling, Marino Mugayar-Baldocchi, and Bill Schaninger. “Gone For Now, or Gone For Good?” McKinsey & Company, April 13, 2022. mckinsey.com/capabilities/people-and-organizational-performance/our-insights/gone-for-now-or-gone-for-good-how-to-play-the-new-talent-game-and-win-back-workers.

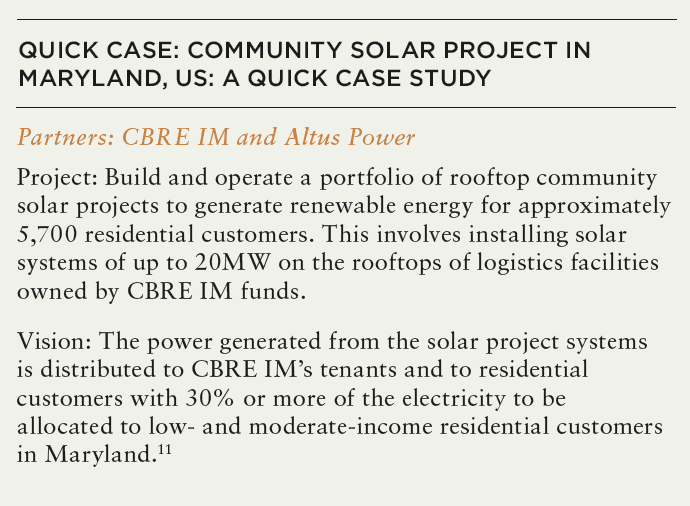

11. “CBRE Investment Management and Altus Power to Bring Additional Community Solar Projects to Maryland.” CBRE Investment Management and Altus Power to Bring Additional Community Solar Projects to Maryland | CBRE Investment Management. Accessed December 6, 2022. cbreim.com/press-releases/cbre-investment-management-and-altus-power-to-bring-additional-community-solar-projects-to-maryland.

12. “Georgia Tech Breaks Ground on Science Square.” Georgia Tech News Center. Accessed December 6, 2022. news.gatech.edu/news/2022/08/18/georgia-tech-breaks-ground-science-square-announces-fund-connecting-local-community.

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Our focus on delivering results is driven by our values, entrepreneurial spirit and our clients’ diverse needs. Together, our team specializes in holistic real assets solutions within and across five real assets investment categories, with a distinct approach to driving performance and long-term value.

CBRE Investment Management is a leading global real assets investment management firm with $143.9 billion in assets under management as of September 30, 2022, operating in more than 30 offices and 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

CBRE Investment Management is an independently operated affiliate of CBRE Group, Inc. (NYSE:CBRE), the world’s largest commercial real estate services and investment firm (based on 2021 revenue). CBRE has more than 105,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE Investment Management harnesses CBRE’s data and market insights, investment sourcing and other resources for the benefit of its clients. For more information, please visit cbreim.com.