While single-family housing has long been the domain of individual owners, the past few decades have seen an increasingly large share of corporate and institutional investors move into the residential space.

Like all trends accelerated by the pandemic, the pace of institutional interest in the asset class significantly quickened over the past year. According to Redfin, investors put a record $77 billion into the single-family market over the past six months, with institutional acquisitions in the space jumping by 2.7% in Q1 2021, compared to Q1 2020.[1]

Though the housing sector presents a unique institutional opportunity in everything from single-family rental (SFR) conversions and build-to-rent (BTR) developments, it is also facing a historic supply/demand challenge. In the nearly twenty years between 2001 and 2020, the US built an average of 276,000 fewer homes per year compared to the three decades between 1968 and 2000.[2] This is 5.5 million units short of historic levels, according to a recent report from the National Association of REALTORS®.[3] To make up for this shortage, and to accommodate for the influx of would-be homeowners contained within the large millennial cohort—the next generation of homeowners—the US will need to build 2.1 million homes each year for ten years.

Solving for this would be an unprecedented building boom that could only be made possible through new policies, including tax credits, loans, and grants for builders, as well as denser and more amenable zoning laws in urban areas—including the possibility of converting disused office and retail assets (such as shopping malls) to residential uses.

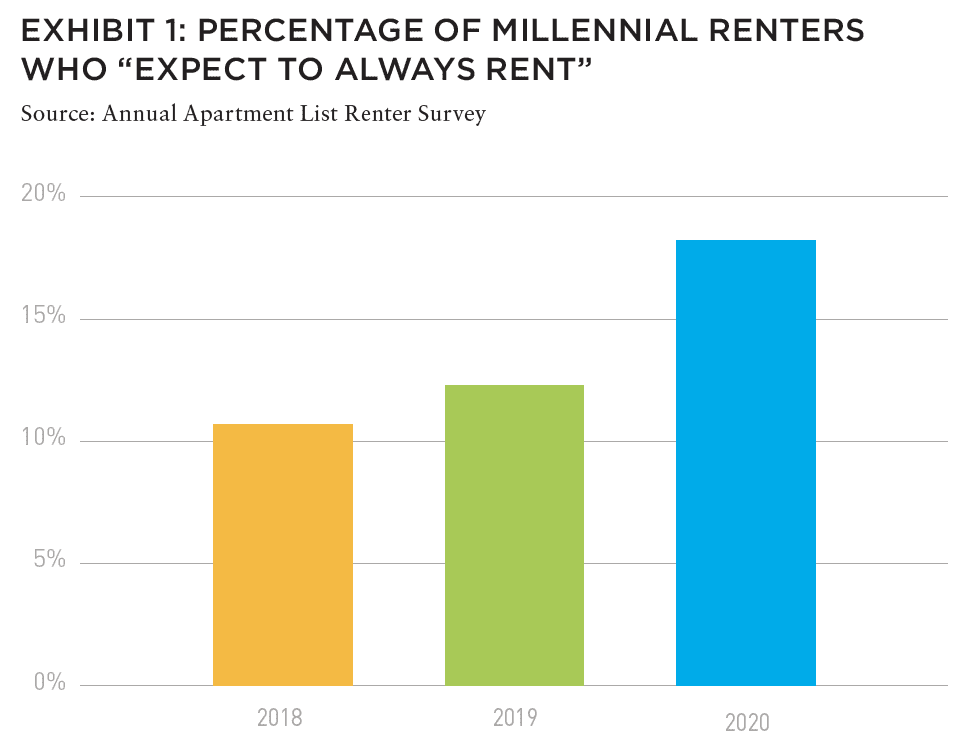

As residential demand continues to outpace supply, the sector also faces a convergence with larger macro-economic trends, including affordability, which investors rank as one of the leading concerns for real estate over the next few years (see “Shining in the Darkness”). For example, the share of millennial renters who have entirely given up on homeownership has gone from 10.7% to 18.2% in the past two years (Exhibit 1)—though according to Freddie Mac, “as more millennials reach age 40, their household formation rate will accelerate due to higher marriage rates and more stable incomes.”[4]

Despite this impending generational shift in forecasted homeownership, the single-family sector will need to find smart solutions to counter (or solve for) these trends, especially because median household income[5] rose only 19% between 2010, while median home sales prices[6] rose 44% in the same period—and they continue to trend upwards.

With these questions in mind, this special four-part section of Summit Journal presents a few key ideas that point towards possible futures for the single-family sector, and the role investors can have in solving some key problems—while also generating target yields.

CLICK BELOW TO BEGIN EXPLORING THE HOUSING ISSUE

NOTES

1. “Institutional Buyers are Flooding the Single-Family Market,” The Real Deal, 24 May 2021, therealdeal.com/2021/05/21/institutional-buyers-are-flooding-single-family-market/; redfin.com/news/investor-home-purchases-q2-2021/

2. “US Housing Market Needs 5.5 Million More Units, Says New Report,” Wall Street Journal, 16 June 2021, wsj.com/articles/u-s-housing-market-needs-5-5-million-more-units-says-new-report-11623835800

3. “Housing is Critical Infrastructure: Social and Economic Benefits of Building More Housing,” National Association of REALTORS, June 2021, cdn.nar.realtor/sites/default/files/documents/Housing-is-Critical-Infrastructure-Social-and-Economic-Benefits-of-Building-More-Housing-6-15-2021.pdf

4. “Millennials and Housing: Homeownership Demographic Research,” Freddie Mac, May 2021, sf.freddiemac.com/content/assets/resources/pdf/fact-sheet/millennialplaybook millennials-and-housing.pdf

5. “Real Median Household Income in the United States,” Federal Reserve Bank of St. Louis, Retrieved 22 June 2021, fred.stlouisfed.org/series/MEHOINUSA672N#0

6. “Median Sales Price of Houses Sold for the United States,” Federal Reserve Bank of St. Louis, Retrieved 22 June 2021, fred.stlouisfed.org/series/MSPUS#0

ALSO IN THIS ISSUE (SUMMER 2021)

NOTE FROM THE EDITOR / The Housing Issue

AFIRE | Benjamin van Loon

INVESTOR SENTIMENT / Shining Through Darkness

The 2021 AFIRE International Investor Survey underscores a sense of calculated optimism for CRE investment in the year ahead.

AFIRE | Gunnar Branson

ECONOMY / Revisiting Inflation

For commercial real estate investors, inflation fears are real— but are they rational?

Aegon Asset Management | Martha Peyton, PhD

DEURBANIZATION / Herd Community

Uncertainty surrounding remote work and politics suggest a wide range of potential outcomes for big cities, which may upend the long-running megatrend toward urbanization.

Green Street | Dave Bragg and Jared Giles

HOUSING / How to Rebuild

Could an idea to “bring back” New York after the pandemic work in other cities?

Aria | Joshua Benaim

HOUSING / Single Family, Multiple Questions

Institutional ownership in single-family rentals accounts for less than 5% of the segment, but answers to key questions could change start to change that balance.

Berkshire Residential Investments | Gleb Nechayev, CRE

HOUSING / Institutionalizing Single Family

Over the past two decades, the single-family rental industry has evolved into an institutional-caliber asset class—so where is the sector going next?

Tricon Residential | Jonathan Ellenzweig

HOUSING / Build-to-Rent Boom

The future is bright for build-to-rent and institutional investors are increasingly looking at investing in this sector.

Squire Patton Boggs | John Thomas and Stacy Krumin

OFFICE / Recovering the Office

While most agree that the office sector has a difficult road ahead, there is less consensus about future demand in the sector. What are the indicators investors should be tracking?

Barings Real Estate | Phillip Conner and Ryan Ma

OFFICE / London Calling

With Brexit and pandemic resolutions coming into focus, pricing disparities could dissipate based on improved cross-border liquidity and cap rate compression in the London office market.

Madison International Realty | Christopher Muoio

LOGISTICS / Supply Change

Urbanization, digitalization, and demographics are the key trends to watch for understanding the future of logistics real estate.

Prologis | Melinda McLaughlin and Heather Belfor

CLIMATE / Accounting for Environmental Risk

When it comes to guards against environmental risk, Boston, Indianapolis, Minneapolis, and Portland are some of the most prepared US cities. What makes them different?

Yardi Matrix | Paul Fiorilla, Claire Anhalt, and Maddie Harper

ESG / Putting People First

Though “impact investing” is no longer totally distinct from investing in general, investors still have a lot of work to do for fulfilling the social and governance aspects of ESG expectations.

Grosvenor Americas | Lauren Krause and Brian Biggs

MULTIFAMILY / Influencing Multifamily

As we come out of the pandemic to a new economy, it seems likely that the creator economy will continue to grow. This will have a major impact on the multifamily sector.

citizenM Hotels | Ernest Lee

TALENT AND RECRUITMENT / Enhancing Life Sciences

As the global life sciences sector continues to grow in real estate, highly specialized skills and experience will be the keys to success.

Sheffield Haworth | Max Shepherd and Jannah Babasa

EDUCATION / Real Estate Education Goes Global

The evolution of global real estate education over the past three decades will be integral to developing a rich pipeline of talent for the future of commercial real estate.

Georgetown University | Julian Josephs, FRICS