Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Focus on the COVID-19 recession, policies to truncate it, and the path of recovery have dominated the attention of analysts for more than two years. Macroeconomic factors continue to dominate our attention now as inflation in the aftermath of the COVID-recession has been further complicated by Russia’s invasion into Ukraine. All eyes are on the prospects for the US Federal Reserve to accomplish a soft landing.

With these trends well-examined at this point, we know that US commercial real estate investors are well-versed in understanding the importance of economic growth to property investment performance. And today, commercial real estate (CRE) in the US is beginning to confront another foundational challenge: weakening demographics.

In this article, we identify the components of weakening demographics measured nationally and highlight differences across US metro areas. The differences illustrate the importance of careful metro market selection to counter demographic headwinds in the years ahead.

FOUR DEMOGRAPHIC CHALLENGES

A review of detailed data points to four demographic trends that are increasingly worrisome for US economic growth prospects and the vitality of its US CRE sector:

- Overall population growth has been slowing alongside labor force growth, which will impair economic growth prospects unless productivity improvements provide

an offset. - Legal immigration has been declining along with foreign student applications to US colleges. Quotas set in US policy have been difficult to increase and prospects for more immigrant friendly sentiment appear unlikely.

- Generationally, Baby Boomers are retiring and dying; Millennials have largely matured into prime working age, while up-and-coming Gen Z is smaller than the Millennial generation which it follows.

- Beyond Gen Z, the birth rate has shrunk for a variety

of cultural and economic reasons suggesting that a future baby boom is unlikely to juice up economic growth prospects.

SLOWING POPULATION GROWTH

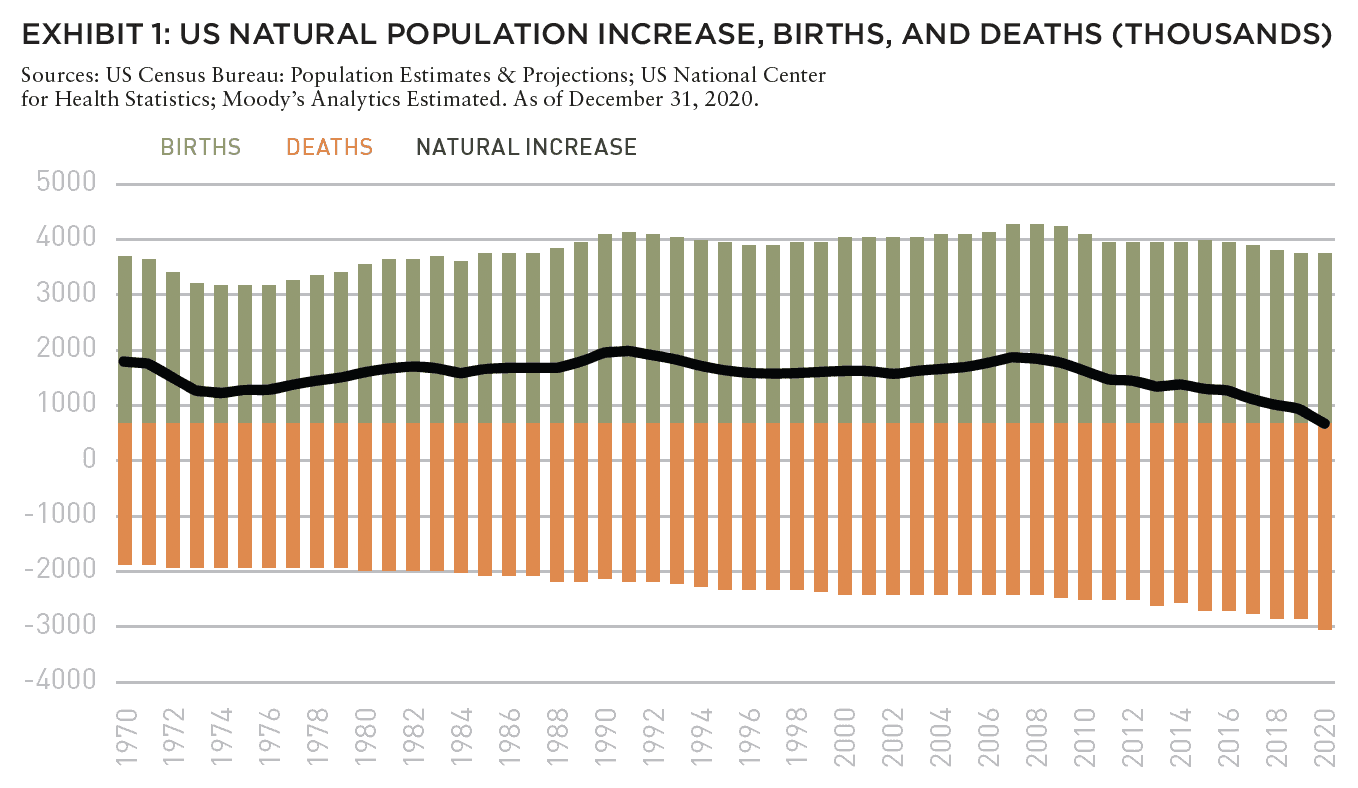

Population growth has generally been slowing since hitting a year-over-year high of 1.38% in 1992. It has been slowing precipitously since 2016, reaching a fifty-year low of 0.35% in 2020, and data points for 2021 are expected to be even lower. The slowing growth is being caused by the components of population change: births, deaths, and net migration. As Exhibit 1 illustrates, the number of births has been stagnant or declining since 2008. Meanwhile, the number of deaths has been steadily increasing, even before the COVID pandemic, due to the aging population. The natural increase in population, or the difference between births and deaths, reached a fifty-year low in 2020, which is the most recent reported data.

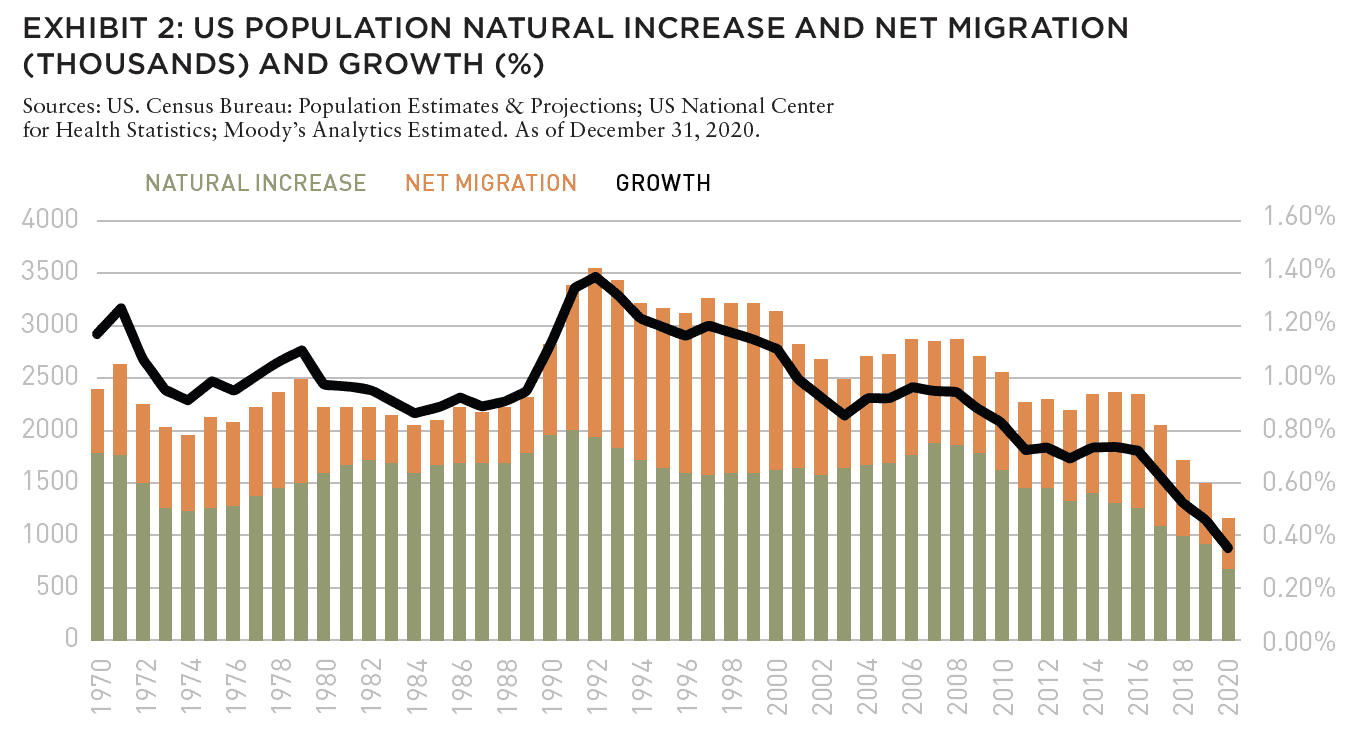

While the natural increase in population has been declining, net migration (the number of immigrants minus the number of emigrants) has been diminishing rapidly (Exhibit 2). The policies of the Trump administration were associated with a steep 47% fall in net migration between 2016 and 2019, and restrictions on international travel due to the COVID pandemic caused immigration to nearly come to a complete halt.

GENERATIONAL TRENDS

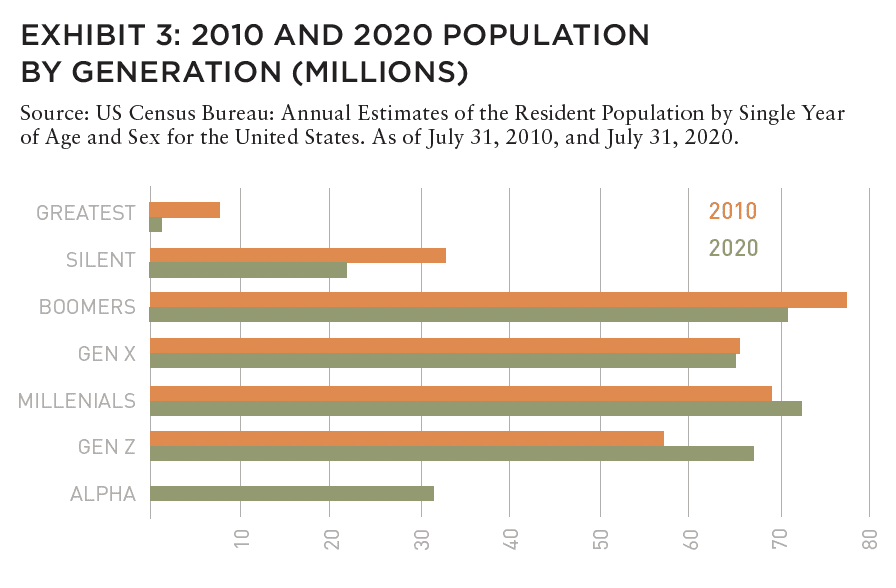

In addition to the slowing growth rate of the overall population, there are significant demographic changes underway that will transform the economy and US CRE prospects (Exhibit 3). The most important change is aging of the Baby Boomer generation. Until recently, the Boomers, defined as those born between 1946 and 1964, was the largest generation in US history.1

Boomers have dominated the labor force since the 1970’s and have enabled much of the economic expansion seen since then. However, they are now reaching retirement age, which will have ongoing effects on the labor market. The oldest Boomers began to reach the traditional retirement age of 65 in 2011 and all the boomers will have reached that age by 2029.

The second demographic sea-change focuses on Millennials, defined as those born between 1981 and 1996,1 and now comprising a larger cohort than boomers. Millennials have now all matured into the prime working age category (defined as 25 to 54). As they continue to form and expand their households, they will reach their prime earning and spending years over the next two decades. As the Boomer generation declines in size, spending power, and influence, the dominance of the Millennial generation will grow and its influence over the economy and trends in CRE will strengthen.

The third demographic trend that will shape the future is Generation Z, defined as those born between 1997 and 2012.1 The most crucial characteristic of Gen Z is its relatively smaller size compared with both Millennials and Boomers. Therefore, as Boomers retire there will be fewer workers to take their place in the labor force. This will cause significant headwinds for the economy and CRE prospects.

ECONOMIC GROWTH PROSPECTS

Economic growth is dependent on population growth, the growth of the labor force, and labor productivity. The current demographic trends suggest that the economy will be grappling with a contracting labor force for years to come. Labor productivity spurred by investment in technological innovation helped the US economy sustain its 2% real growth over the last two decades. However, as shown in Exhibit 4, population growth and labor force growth weakened in the most recent decade with a negative skew. Productivity gains weakened as well.

Increasing the amount of legal immigration would be the most immediate and impactful solution, but the quotas defined in US policy have been difficult to increase and prospects for more immigrant friendly sentiment appear unlikely.

Looking even further ahead, the US birth rate has shrunk for a variety of cultural and economic reasons suggesting that a future baby boom is unlikely to juice up the labor force. That leaves us with productivity as the primary prospect for economic growth in the future. Surely improvements in technology will create significant increases in productivity, especially as robotics and artificial intelligence take root. However, the industries that stand to lose the largest number of workers due to retirement—education and health services, and professional and business services—are also likely to be the hardest to automate. Altogether, expectations of a return to the 2% real growth trend, even after current economic woes are eased, will be a challenge.

DEMOGRAPHIC CHALLENGES DIFFER ENORMOUSLY ACROSS US METRO AREAS

PLACE MATTERS

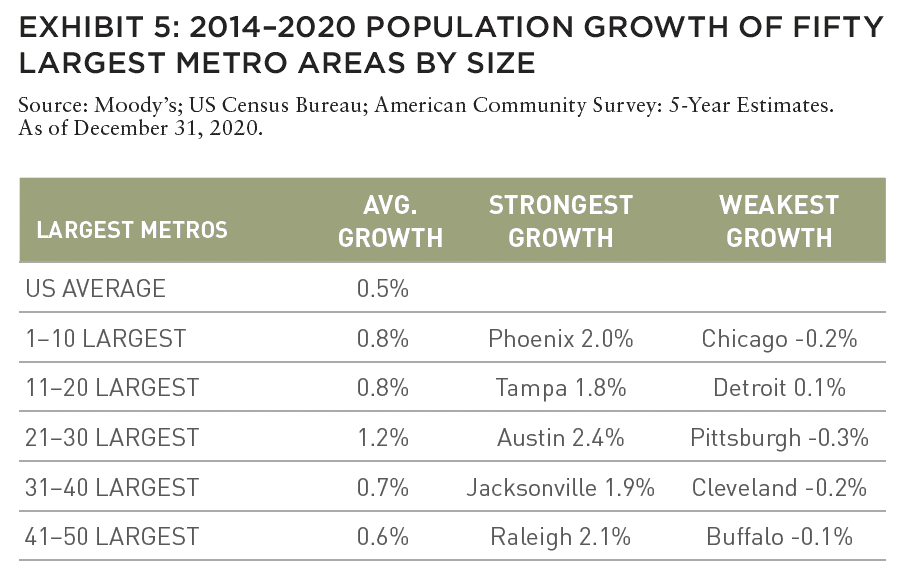

Demographic headwinds will not affect all localities the same way. While the future distribution of population growth is subject to divergence, the recent past can give us hints. Exhibit 5 shows that among the fifty largest metro areas in the US, population growth has varied significantly in recent years.

On average, the twenty-first to the thirtieth largest metros saw the largest growth rate of 1.2% between 2015 and 2020. That is more than double the pace of the national increase, 0.5%.

Within this cohort, blockbuster population growth has occurred in Austin at 2.4% and Orlando at 2.2%. But other medium-sized metros in this group have fared very differently; Pittsburgh has declined while St. Louis and Cincinnati have barely grown at all. Within the ten largest metros, growth rates have also been quite varied, with Phoenix and Dallas enjoying growth rates of 2.0% and 1.8%, respectively, while the New York and Chicago metros have declined.

As investors work to designate target markets, this metric of pre-COVID population growth offers insight into the relative attractiveness of metro areas for both population, and economic growth associated with population growth. Researchers have identified the key drivers of relative attractiveness to include the cost of living, the cost of doing business, and the concentration of industries. Austin is a case in point; it has an agglomeration of tech industries along with cost of living and cost of doing business advantages compared to the tech centers on the West Coast.

APARTMENT SECTOR

Apartment demand is directly fed by population growth, employment, and income, which direct demand to the various quality-rent cohorts that comprise apartment supply. These demographic drivers are not uniform across localities, resulting in stronger demand for new supply in growing areas compared to declining demand in shrinking areas. Middle-market apartments in particular will benefit from relatively stronger demographics in some metros compared to relatively weaker demographics in others.

The past decade’s growth in multifamily apartment demand has been fueled by the large Millennial generation’s initial household formation. With the youngest Millennials now age 26, they are now all in or surpassing the prime renting ages of 25 to 34. They will increasingly be looking for more space and ownership opportunities as they mature and grow their families.

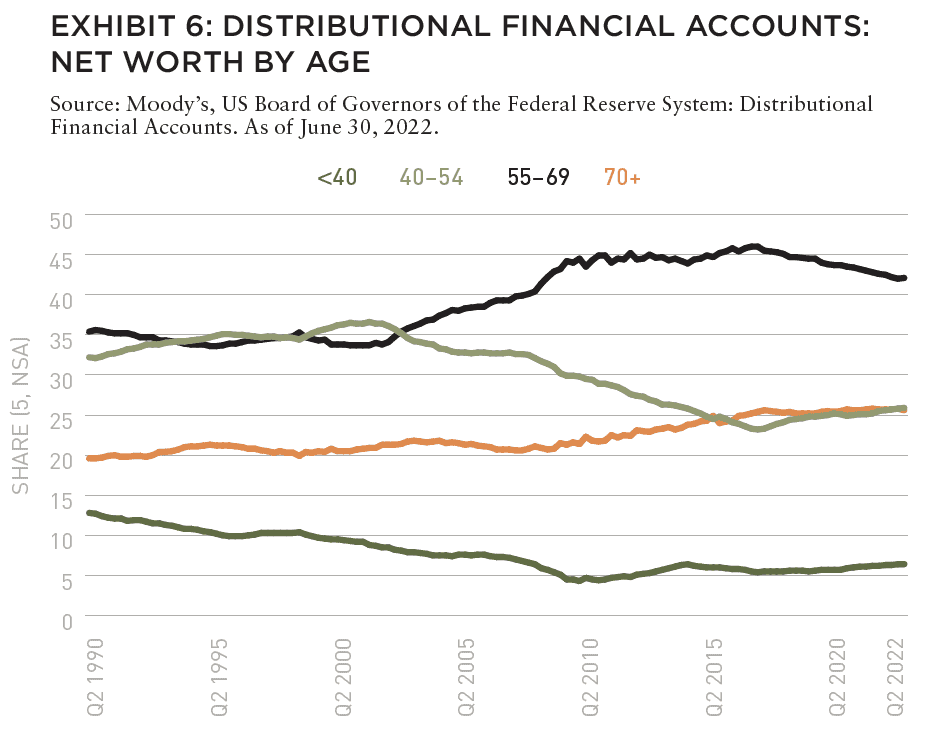

The resulting increase in demand for single family ownership was boosted by historically low mortgage borrowing rates during the COVID recovery, and home prices soared. Higher borrowing costs and more expensive home prices are now stifling demand. Additionally, the overall economic well-being of the Millennial generation in young adulthood has been weaker compared with prior generations at the same age (Exhibit 6). With more debt, lower earnings, fewer assets, and less wealth than previous generations, Millennials have had to delay many life milestones and will continue to rent longer than previous generations.2 This is positive for apartment investments.

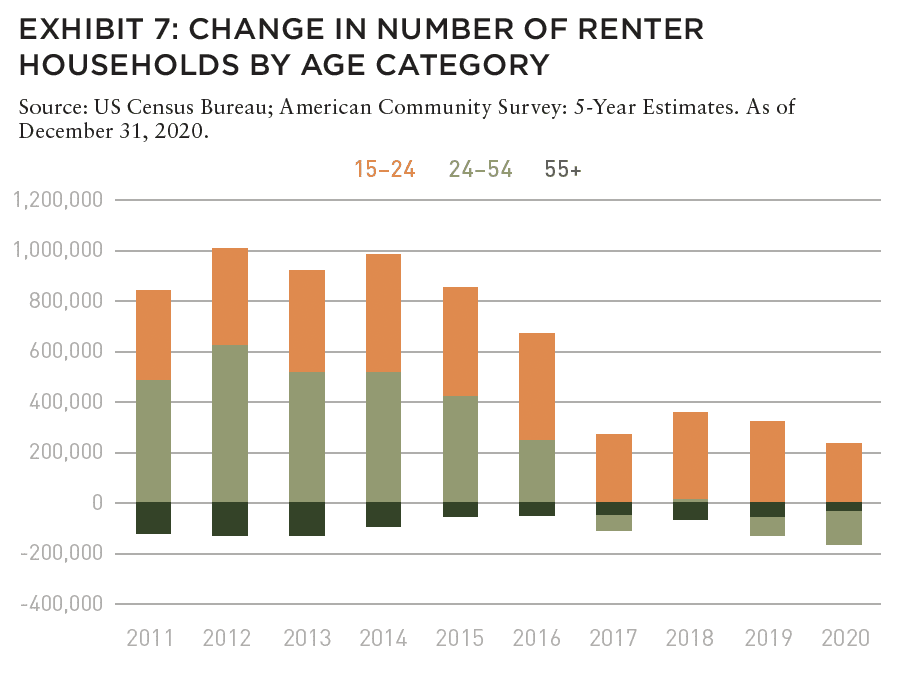

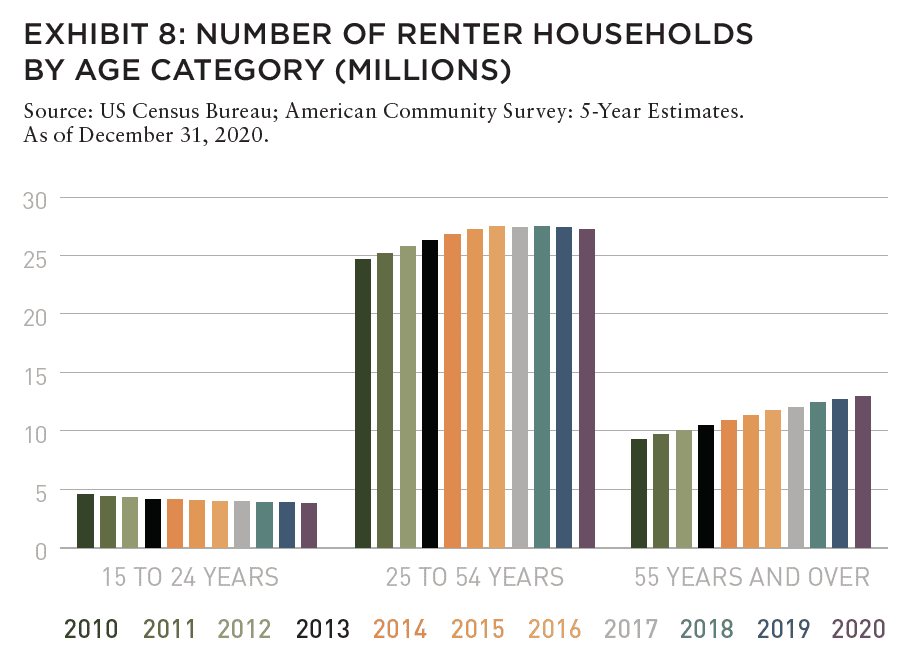

The smaller Gen Z population will mean that there will be fewer new households formed in the coming years. As Exhibits 7 and 8 illustrate, demand from younger people for apartments has been slowing, and will be stagnant at best, in the coming years. But, on the other hand, Gen Z might earn higher incomes sooner than Millennials, due to the tightening labor market, and will subsequently be able to form households sooner. They might even be more mobile than previous generations due to work-from-home opportunities persisting beyond COVID.

Beyond dealing with the uncertainties of Gen Z, rental markets will need to cater to the growing older population as well. There is a significant population of baby boomers that are already renting but their needs may change as they age. There will be some opportunity created by Boomers downsizing from homeownership to apartment rental.

As older adults provide a larger portion of the demand for rental housing, more multifamily properties will be designed or rehabbed with their needs in mind. Basic accessibility features that allow people to age in place, such as step-free entrances and levered door handles, will become more important. Landlords may also consider more extensive accessibility features to attract seniors.

As older adults provide a larger portion of the demand for rental housing, more multifamily properties will be designed or rehabbed with their needs in mind. Basic accessibility features that allow people to age in place, such as step-free entrances and levered door handles, will become more important. Landlords may also consider more extensive accessibility features to attract seniors.

INDUSTRIAL, OFFICE, AND RETAIL SECTORS

Industrial, office, and retail space demand are indirectly affected by shifting demographics primarily through the impact on economic growth. With demographic prospects differing across localities, prospects for these sectors are also subject to wide geographic differences. While the apartment sector is the most sensitive to demographic changes, grocery-anchored retail is affected by gains or losses in numbers and spending power of local shoppers. Some locales will have demand for new grocery-anchored centers; other locales will see diminishing vitality in that sector as population declines.

EXPLORE THE LATEST ISSUE

MAKE SUSTAINABILITY REAL

With the case for sustainability already well-established, how can (and should) real estate continue to lead?

Gunnar Branson | AFIRE

RETURN GENERATION POTENTIAL

In addition to offering inflation protection and lower volatility, real estate also offers something that other asset classes can’t: the opportunity to invest in tangible, positive change.

Shane Taylor | CBRE Investment Management

CATCH A FALLING *R

The future path of long-term interest rates in the US and why it matters.

Alexis Crow, PhD | PwC

TIDAL PATTERNS

Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Martha S. Peyton and Caitlin Ritter | Aegon Asset Management

WORKPLACE VALUES

The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

Dags Chen, CFA | Barings Real Estate

OFFICE GAMES

Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

William Maher and Scot Bommarito | RCLCO

EMISSION CRITICAL

Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

Kevin Fagan, Xiaodi Li, and Natalie Ambrosio Preudhomme | Moody’s

MOVING TARGETS

A close-in look at twenty major US metros and thousands of properties shows how the overall impact of rising expense loads have narrowed NOI margins. Investors should take note.

Gleb Nechayev, CRE and Webster Hughes, PhD | Berkshire Residential Investments

SAND STATES

In the wake of the Great FinancialCrisis, certain metros in the Sand States suffered disproportionally. It may not be as bad this time.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

STORM WARNING

Not all storms are the same, and some are so tragic that they force a moment of universal recalibration. Hurricane Ian was one of those storms—but what does that mean for real estate?

Rajeev Ranade and Owen Woolcock | Climate Core Capital

PACIFIC THEATER

The Asia-Pacific region is already home to some of the world’s largest economies and now set to lead global economic growth. What’s moving the needle now for the APAC region?

Simon Treacy and Yu Jin Ow | CapitaLand Investment

STABLE SPACE

For e-commerce property investors, the past decade was outstanding, but even as market dynamics are slowing industrial’s momentum, market fundamentals remain sound.

Mehta Randhawa | JLL

COMBATTING THE HEADWINDS

US CRE investors monitor economic growth closely with the understanding that it drives demand for space. Beginning in 2020, the impact of the COVID pandemic was the focus of attention as it impaired economic growth globally. Now, as the pandemic fades in importance, attention is focused on inflation, monetary policy, and the disruption in food and energy sectors due to the war in Ukraine. These near-term challenges will pass with time and investors will need to direct their focus to the US CRE demand drivers that emerge. In this paper, we identify population growth prospects over the medium term as a potential pain point for US CRE. Slow population growth is underway in the US and will likely continue. Productivity growth is also relatively slow. Together they create a constraint on economic growth prospects and the demand it creates for CRE.

The demographic constraint on top line economic growth will make it imperative for investors to pay close attention to the very different prospects for individual property subsectors in individual metro areas. Demographic evolution for the US as a whole will not affect all locales equally. The differences in turn translate into different investment prospects. Specifically, both middle-market apartments and grocery-anchored retail will benefit from relatively stronger demographics in some metros versus relatively weaker demographics in others. It is worth noting that the locational decisions of Millennials have been a determinant of stronger versus weaker metros in the recent past. Similarly, the locational decisions of Gen Z will drive relative growth in the future.

—

ABOUT THE AUTHOR

Martha Peyton, PhD, is Managing Director of Real Assets Applied Research for Aegon Asset Management, the global investment management brand of Aegon Group.

—

NOTES

1. Dimock, Michael. “Defining Generations: Where Millennials End and Generation Z Begins.” Pew Research Center, April 21, 2022. pewresearch.org/facttank/ 2019/01/17/where-millennials-end-and-generation-z-begins/.

2. Kurz, Christopher, Geng Li, and Daniel J. Vine. “Are Millennials Different?” Board of Governors of the Federal Reserve System. Federal Reserve, November 1, 2018. doi.org/10.17016/FEDS.2018.080

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Our focus on delivering results is driven by our values, entrepreneurial spirit and our clients’ diverse needs. Together, our team specializes in holistic real assets solutions within and across five real assets investment categories, with a distinct approach to driving performance and long-term value.

CBRE Investment Management is a leading global real assets investment management firm with $143.9 billion in assets under management as of September 30, 2022, operating in more than 30 offices and 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

CBRE Investment Management is an independently operated affiliate of CBRE Group, Inc. (NYSE:CBRE), the world’s largest commercial real estate services and investment firm (based on 2021 revenue). CBRE has more than 105,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE Investment Management harnesses CBRE’s data and market insights, investment sourcing and other resources for the benefit of its clients. For more information, please visit cbreim.com.