The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

The ambivalence and lag of appraisal-based price indices are misleading investors over the damage done to their private real estate exposure from rising inflation and interest rates. It is happening at a particularly precarious time for global financial markets. During this moment, investors need transparency regarding the values of their holdings.

Investment managers have a responsibility to provide as accurate assessment of current value despite the lack of transactional data points, which are usually sparse during periods of turmoil.

As of Q3 2022, office properties in the NCREIF Property Index (NPI) posted a total return of 3.2% over the prior twelve months, consisting of an income return of 4.3% and an appreciation return of -1.1%. For those who own institutional-quality conventional Class A office buildings in almost any major market, this is implausible. Traditional office values are way down. Evidence indicates space needs and preferences have changed and as a result, office transaction activity over the past year has once again collapsed while a composite share price index of public office REITs has fallen by more than 30% over the same period.1

The US Federal Reserve is dealing with broad, persistent inflation unlike anything the nation has experienced in four decades. To restore price and, dare we say it, financial system stability, the central bank cannot follow the same monetary easing playbook as it has since the GFC. This time things are necessarily different. Rapid monetary tightening is stressing risk valuations across all risk assets and “yesterday’s prices” are not holding up. If asset managers wait for transactions data to draw conclusions about values, they will likely have missed giving their investors information during this critical juncture.

Those who issue and endorse appraisal values should not be the primary arbiters of market values in such moments. Nor do we need a precise understanding of the future path of the office sector. The industry already has abundant information about where values are. At least, we understand where they are not.

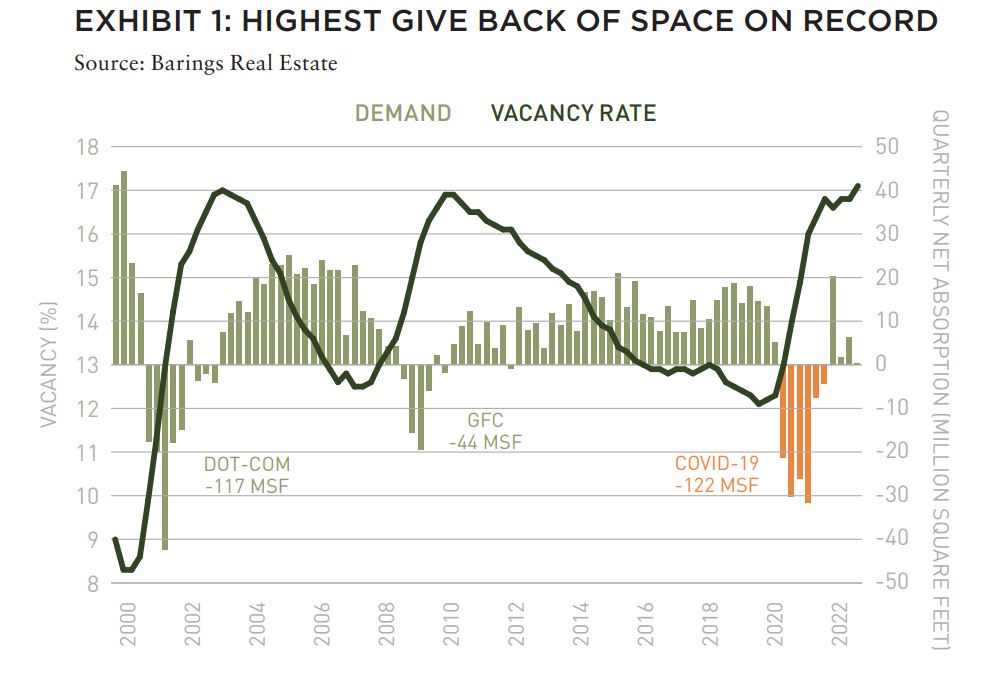

THE WORST EPISODE OF DEMAND DESTRUCTION ON RECORD

The COVID pandemic has caused office employers to reassess their space needs even as they try to entice employees back to the office. The return to office has been slower than broadly anticipated, thanks largely to a historically tight labor market that has favored employees rather than employers. As of September, the unemployment rate for those with at least a bachelor’s degree was 1.8%.2 Employees have overwhelmingly favored hybrid work arrangements, but the obstacles around returning to office are not only a matter of preference. Challenges around commuting, concerns regarding public health and safety, and the difficulties of finding child and/or eldercare—among a multitude of other factors—have hampered the return to in-office work even for many who otherwise want to go back at least part-time.

From Q2 2020 to Q3 2021, firms in multi-tenant office buildings gave back a cumulative 122 million SF (MSF) of space. This is the worst episode of demand destruction on record, exceeding the dot-com bust of 2001, when office-using firms gave back 117 MSF of space over nine quarters. However, sublease vacancy, an indicator of office shadow supply, peaked in early 2002, signaling an impending recovery for the market. Today, sublease vacancy continues to climb with few indications of stabilization. Shadow supply—space that is leased or owned but unoccupied—looms large, meaning that vacancy is likely under-represented by topline numbers.

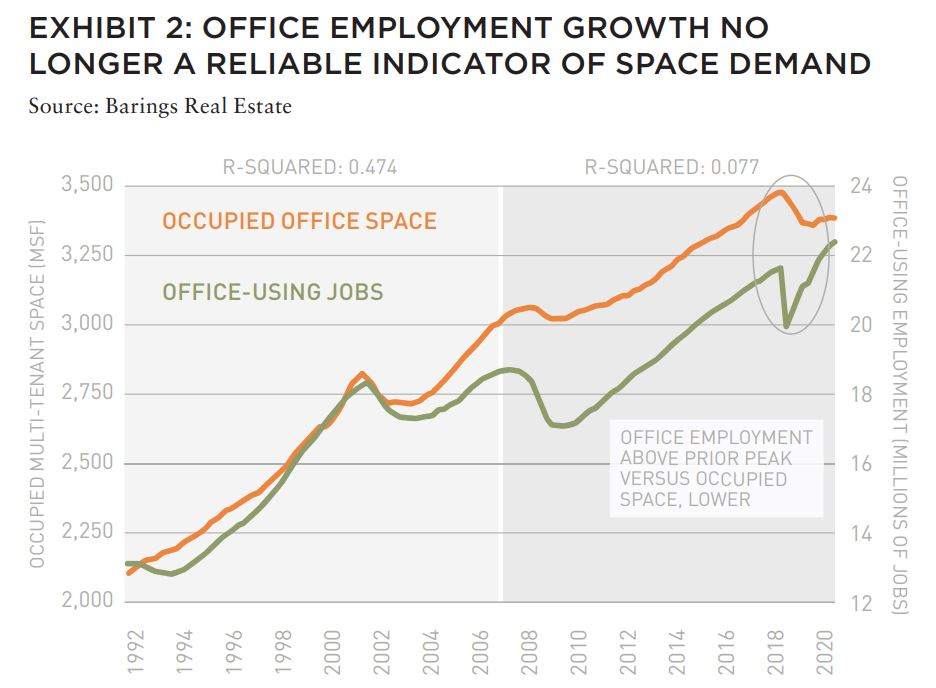

OFFICE DEMAND DECOUPLING FROM EMPLOYMENT

Even before the pandemic, the statistical relationship between office employment and occupied office space was weakening. From 1990 to 2007, the regression coefficient (r-squared) between the quarterly change in office-using employment and the change in occupied space was 0.474 (Exhibit 2). From 2007 to 2022, the r-squared dropped to a mere 0.077. During the intervening years between the GFC and the pandemic, we saw higher densification of office workspaces. There were two primary objectives: to increase the amount of in-person collaboration and to save on space costs. But in the years following, gains in office jobs have not had meaningful carry over into absorption trends.

Since the COVID pandemic, office-using employment has climbed by 3.4% above its prior peak while occupied space is down from its February 2020 peak by 2.7%, which is likely understated considering shadow space. Some may argue that there hasn’t been sufficient time to assess whether the decoupling of office employment and space demand will continue in the post-pandemic era. In reality, the statistical relationship between these trends was already deteriorating well before February 2020. Hybrid work arrangements and accelerating functional obsolescence suggest that conventional office investors should no longer assume that general office employment gains will drive some terminal rate of base demand growth in the post-pandemic era.

OFFICE VALUE HIT HARDER BY RISING RATES THAN OTHER PROPERTY TYPES

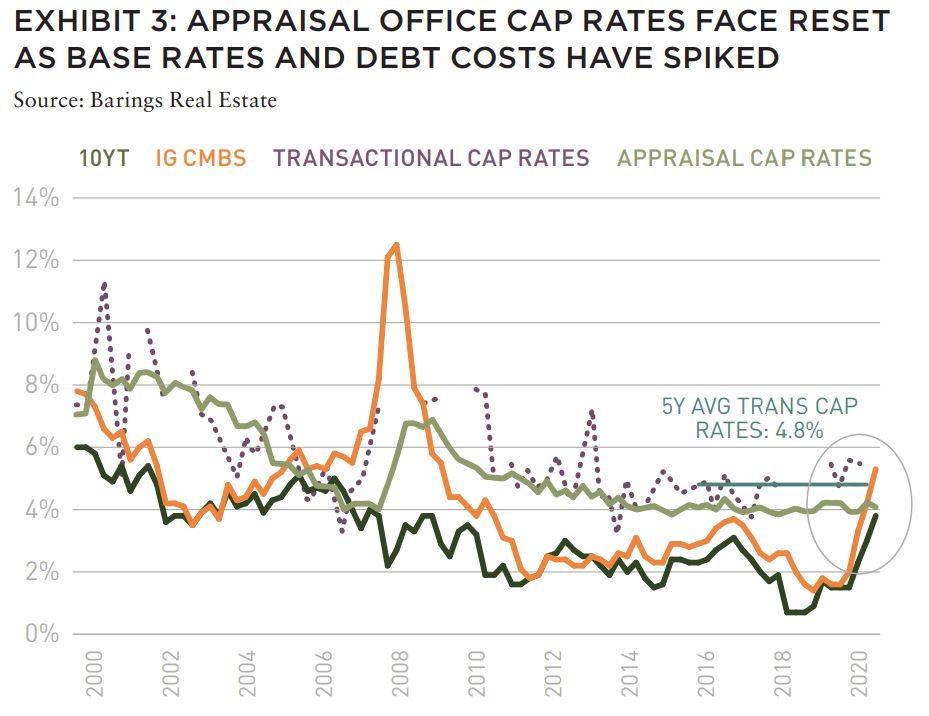

Globally, investors have awakened to the risks of a “higher-for-longer” interest rate environment. The speed and degree to which the Federal Reserve is hiking rates are the most intense since the 1980s. As a direct consequence, real estate debt costs have risen to their highest in more than a decade. Almost all property types are being repriced in the current environment, but investors are willing to tolerate lower cap rates for those sectors that can benefit from secular demand tailwinds such as industrial, apartment, and self-storage. Apartment and Industrial core cap rates have compressed by 63 basis points (bps) and 139 bps, respectively, since Q1 2020 on account of demand prospects. In some cases, cap rates have declined but expected IRRs stayed level.

Unlike other sectors, Office cap rates compressed by only 12 bps over the same period. Though low interest rates were a tailwind for office investment, declining demand and rising capital expenditure costs are putting more and more upward pressure on property yields. A “lower-for-longer” interest rate environment permitted a proliferation of office investments that were a “spread play” by which borrowers could leverage thin equity returns due to low borrowing costs. With the FFR possibly rising above 5%, the jump in base rates has resulted in “negative leverage” as property cash flows have remained anemic despite the acceleration in inflation. Even recent transactions, indicated by the dotted line in Exhibit 3, did not anticipate such a surge in interest rates and financing costs.

Distress within the office sector is increasing while broad market data lags the reality on the ground. Anecdotal evidence of distressed and troubled loans is widening, and LTVs that were once considered conservative are being tested as liquidity and the risk profile for office investment deteriorate rapidly.

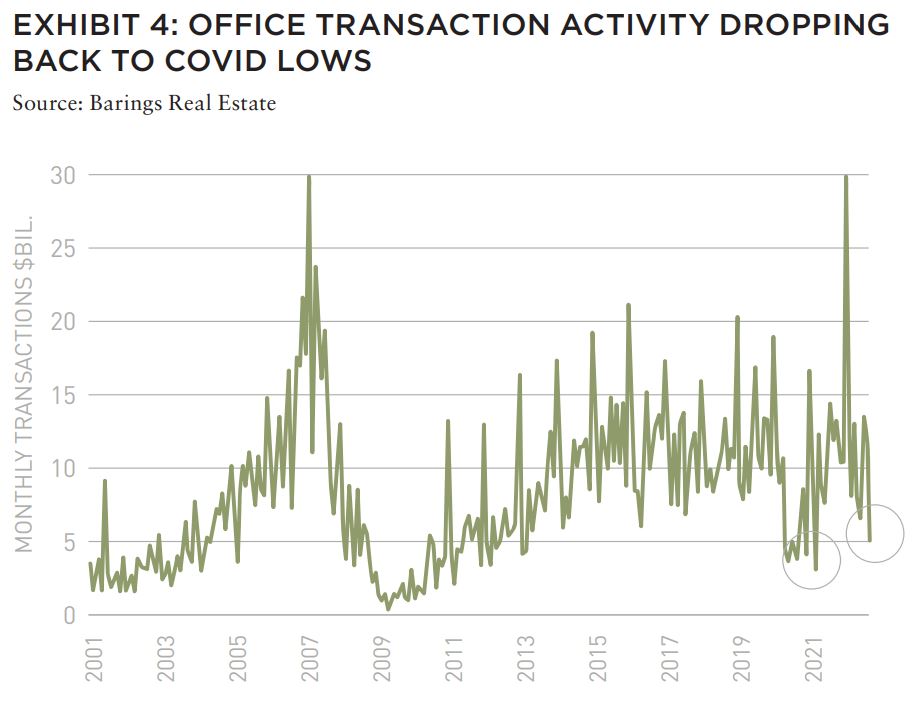

Office transaction activity excluding medical office in September dropped to $5.7 billion, marking the slowest month for office sales since February 2021. Over the quarter, office transactions excluding medical office totaled only $19.8 billion, down 43.3% year-over-year and under the 2015 to 2019 quarterly average of $32.5 billion. Office transaction activity will continue to fall to its pandemic levels as deals closed today were commenced months earlier under more benign capital market circumstances. Sales volume is likely overstating liquidity levels as the uncertainty over the future value of risk assets, not only office properties, is bringing sales activity to a halt.

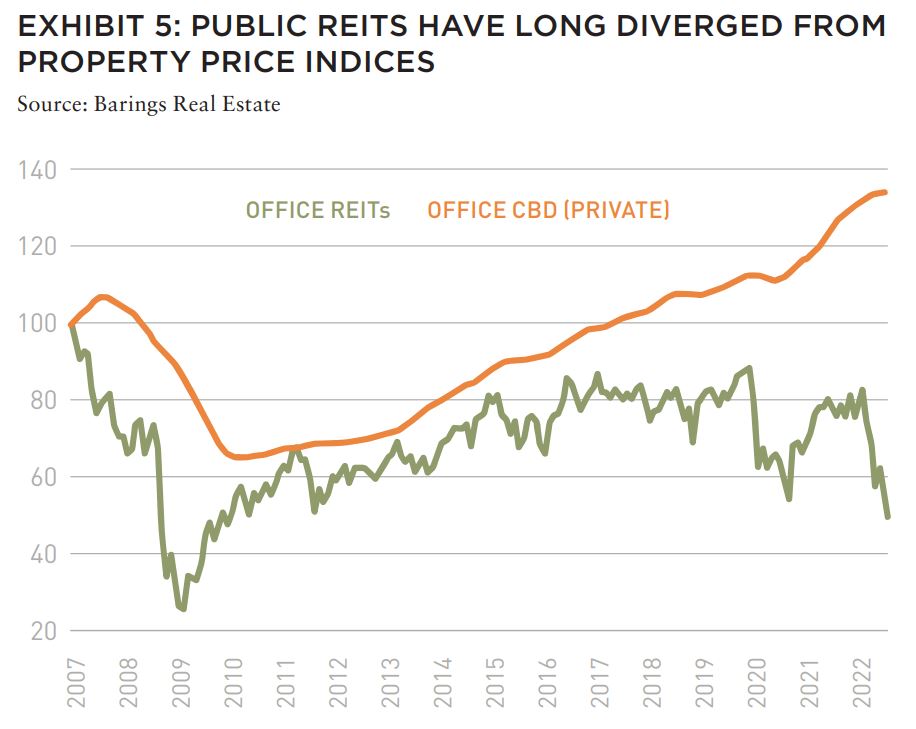

Property price indices, especially those that are appraisal-based, do not register rapid declines in sales activity. In contrast, public REIT share prices do react to periods of elevated volatility and lower liquidity. They can tend to overshoot during moments of pricing dislocation, but public REITs are directionally relevant to private real estate values. During the pandemic, the office subsector component of the FTSE/NAREIT All Equity REIT price index declined by 38.4% from January 2020 to October 2020, but then rebounded by 39.2% over the following 12 months on account of a public sector stimulus-fueled economic rebound. This time around, the office subsector index has fallen by 38.7% under very different capital market circumstances. We think it is reasonable to expect that property values will not emerge from the current market downturn unscathed.

IS OFFICE SIMPLY NOT INVESTIBLE RE-VALUING THE OFFICE SECTOR

Office transaction activity excluding medical office in September dropped to $5.7 billion, marking the slowest month for office sales since February 2021. Over the quarter, office transactions excluding medical office totaled only $19.8 billion, down 43.3% year-over-year and under the 2015 to 2019 quarterly average of $32.5 billion. Office transaction activity will continue to fall to its pandemic levels as deals closed today were commenced months earlier under more benign capital market circumstances. Sales volume is likely overstating liquidity levels as the uncertainty over the future value of risk assets, not only office properties, is bringing sales activity to a halt.

Property price indices, especially those that are appraisal-based, do not register rapid declines in sales activity. In contrast, public REIT share prices do react to periods of elevated volatility and lower liquidity. They can tend to overshoot during moments of pricing dislocation, but public REITs are directionally relevant to private real estate values. During the pandemic, the office subsector component of the FTSE/NAREIT All Equity REIT price index declined by 38.4% from January 2020 to October 2020, but then rebounded by 39.2% over the following 12 months on account of a public sector stimulus-fueled economic rebound. This time around, the office subsector index has fallen by 38.7% under very different capital market circumstances. We think it is reasonable to expect that property values will not emerge from the current market downturn unscathed.

IS THE OFFICE SIMPLY NOT INVESTIBLE?

While the opportunity set of investible offices has dramatically condensed in the post-pandemic era, we believe the property market is bifurcated between the “haves” and “have nots”. In a prior article,3 we explained how those buildings that offer flexible floorplates, collaborative spaces, substantive ESG implementation among other “next-generation” amenities are increasingly able to attract a disproportionate share of tenant demand, especially if they are in nodes with a concentration of tech (STEM) firms as well as other amenities.4 Relative to the “haves”, the “have nots” are conventional offices, including unexceptional Class A properties, that have few, if any, distinguishing characteristics.

As firms continue to downsize but move into best-in-class space, investment managers are learning that they are willing to pay up for the office space in locations that will entice their employees to return to the office and increase in-person interaction and collaboration.

RE-VALUING THE OFFICE SECTOR

The purpose of this article has not been to pin the blame on commercial real estate appraisers who provide a vital input into the investment decision-making process during normal market conditions. Investment managers who make decisions about when to buy, hold, and sell real estate have a responsibility to provide an accurate assessment of investment values when times are not normal.

The office sector is experiencing a perfect storm of declining demand, a fundamental change in tenant space and location preferences, higher interest rates, and financing costs. Future cash flows are also uncertain. We do not know precisely how this current market downturn will play out, but asset managers that have operated in and survived past real estate market cycles recognize that values need to account for a worsening macroeconomic outlook, higher degree of functional obsolescence, and the likelihood that interest rates and inflation will be higher going forward than before the pandemic.

The sooner we can recognize that prices are not where industry benchmarks have indicated, the sooner we can move forward with assessing and capitalizing on new opportunities within the office sector.

EXPLORE THE LATEST ISSUE

MAKE SUSTAINABILITY REAL

With the case for sustainability already well-established, how can (and should) real estate continue to lead?

Gunnar Branson | AFIRE

RETURN GENERATION POTENTIAL

In addition to offering inflation protection and lower volatility, real estate also offers something that other asset classes can’t: the opportunity to invest in tangible, positive change.

Shane Taylor | CBRE Investment Management

CATCH A FALLING *R

The future path of long-term interest rates in the US and why it matters.

Alexis Crow, PhD | PwC

TIDAL PATTERNS

Amidst myriad global economic and geopolitical uncertainties, US commercial real estate has an even greater challenge ahead: demographics.

Martha S. Peyton and Caitlin Ritter | Aegon Asset Management

WORKPLACE VALUES

The sooner we can recognize that values have come down collectively—even beyond the office sector—the sooner we can move forward to capitalizing on new opportunities.

Dags Chen, CFA | Barings Real Estate

OFFICE GAMES

Even as the US office sector has lagged other property types, there could be an important (and valuable) difference of office performance based on property age and market.

William Maher and Scot Bommarito | RCLCO

EMISSION CRITICAL

Workers spending less time in the office post-pandemic may seem negative for the office sector, but a four-day workweek can be a boon for some office property owners.

Kevin Fagan, Xiaodi Li, and Natalie Ambrosio Preudhomme | Moody’s

MOVING TARGETS

A close-in look at twenty major US metros and thousands of properties shows how the overall impact of rising expense loads have narrowed NOI margins. Investors should take note.

Gleb Nechayev, CRE and Webster Hughes, PhD | Berkshire Residential Investments

SAND STATES

In the wake of the Great FinancialCrisis, certain metros in the Sand States suffered disproportionally. It may not be as bad this time.

Stewart Rubin and Dakota Firenze | New York Life Real Estate Investors

STORM WARNING

Not all storms are the same, and some are so tragic that they force a moment of universal recalibration. Hurricane Ian was one of those storms—but what does that mean for real estate?

Rajeev Ranade and Owen Woolcock | Climate Core Capital

PACIFIC THEATER

The Asia-Pacific region is already home to some of the world’s largest economies and now set to lead global economic growth. What’s moving the needle now for the APAC region?

Simon Treacy and Yu Jin Ow | CapitaLand Investment

STABLE SPACE

For e-commerce property investors, the past decade was outstanding, but even as market dynamics are slowing industrial’s momentum, market fundamentals remain sound.

Mehta Randhawa | JLL

—

ABOUT THE AUTHORS

Dags Chen is Managing Director and Head of US Real Estate Research and Strategy for Barings Real Estate, a global real estate platform with extensive capabilities across both debt and equity strategies.

—

NOTES

1. Bloomberg. As of September 30, 2022.

2. Bureau of Labor Statistics. As of September 2022.

3. Chen, Dags, Ryan Ma, and Ryan LaRue. “Selective Framework.” Summit Journal. AFIRE, June 22, 2022. https://www.afire.org/summit/selectiveframework/

4. “Selective Framework” Summit Journal

—

REVIEWER RESPONSE

Beyond focusing the reader on the limitations of appraisal-based valuations, which are widely understood to lag in periods of heightened market volatility, the author dives deeper and makes the case that office values will likely be impaired on a long-term basis. In general, I agree.

However, the point about “haves” and “have nots” that the author touches on should be explored more deeply as it is central to understanding the value of specific office properties now and going forward. Geography, age, and net-zero readiness are becoming bigger factors in tenant demand and relative value.

For example, the post-pandemic shift in how and where people work is primarily a US phenomenon (Asia is very much back to pre-pandemic habits) and varies greatly across domestic cities and regions. Consider that Austin’s re-entry rate of 64.3% is more than 50% greater than San Francisco’s re-entry rate of 42%. Leasing statistics since the onset of Covid in 2020 highlight how pronounced the disparity is across building age, with positive 88 million SF of net absorption in buildings built since 2015, as compared to negative 257 million SF of net absorption in buildings built more than eight years ago. Rent premiums for new space are also at all-time highs.

I expect we will see appraised values for office adjust more dramatically in the coming quarters, as appraisers incorporate weaker recent market data, increase discount rates and increase residual cap rates. I agree that there will be compelling investment opportunities that emerge from this dislocation, but asset mangers will need to be highly selective when it comes to office. And I think they get that. After all, one could argue that ODCE fund managers have actually been ahead of the curve, proactively reducing their collective exposure to office by over one-third, from 35.4% to 23.5% of their portfolios over the past three years.

Amy Price

President, BentallGreenOak

Member, Summit Journal Editorial Board

THIS ISSUE OF SUMMIT JOURNAL IS PROUDLY SUPPORTED BY

Our focus on delivering results is driven by our values, entrepreneurial spirit and our clients’ diverse needs. Together, our team specializes in holistic real assets solutions within and across five real assets investment categories, with a distinct approach to driving performance and long-term value.

CBRE Investment Management is a leading global real assets investment management firm with $143.9 billion in assets under management as of September 30, 2022, operating in more than 30 offices and 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

CBRE Investment Management is an independently operated affiliate of CBRE Group, Inc. (NYSE:CBRE), the world’s largest commercial real estate services and investment firm (based on 2021 revenue). CBRE has more than 105,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE Investment Management harnesses CBRE’s data and market insights, investment sourcing and other resources for the benefit of its clients. For more information, please visit cbreim.com.